BAP41 - ABC Learning Centres: Financial Statements Warning Analysis

VerifiedAdded on 2023/06/03

|30

|4947

|117

Essay

AI Summary

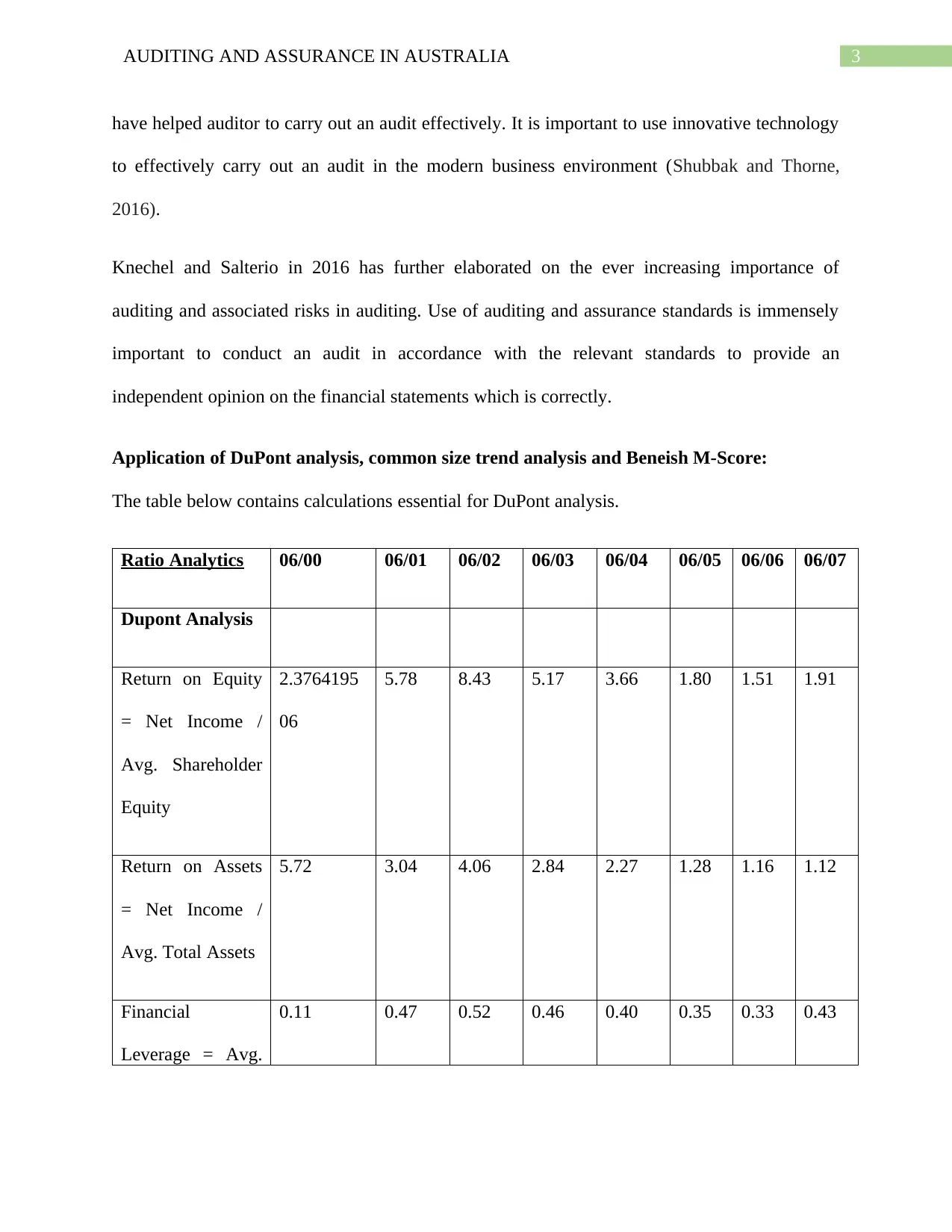

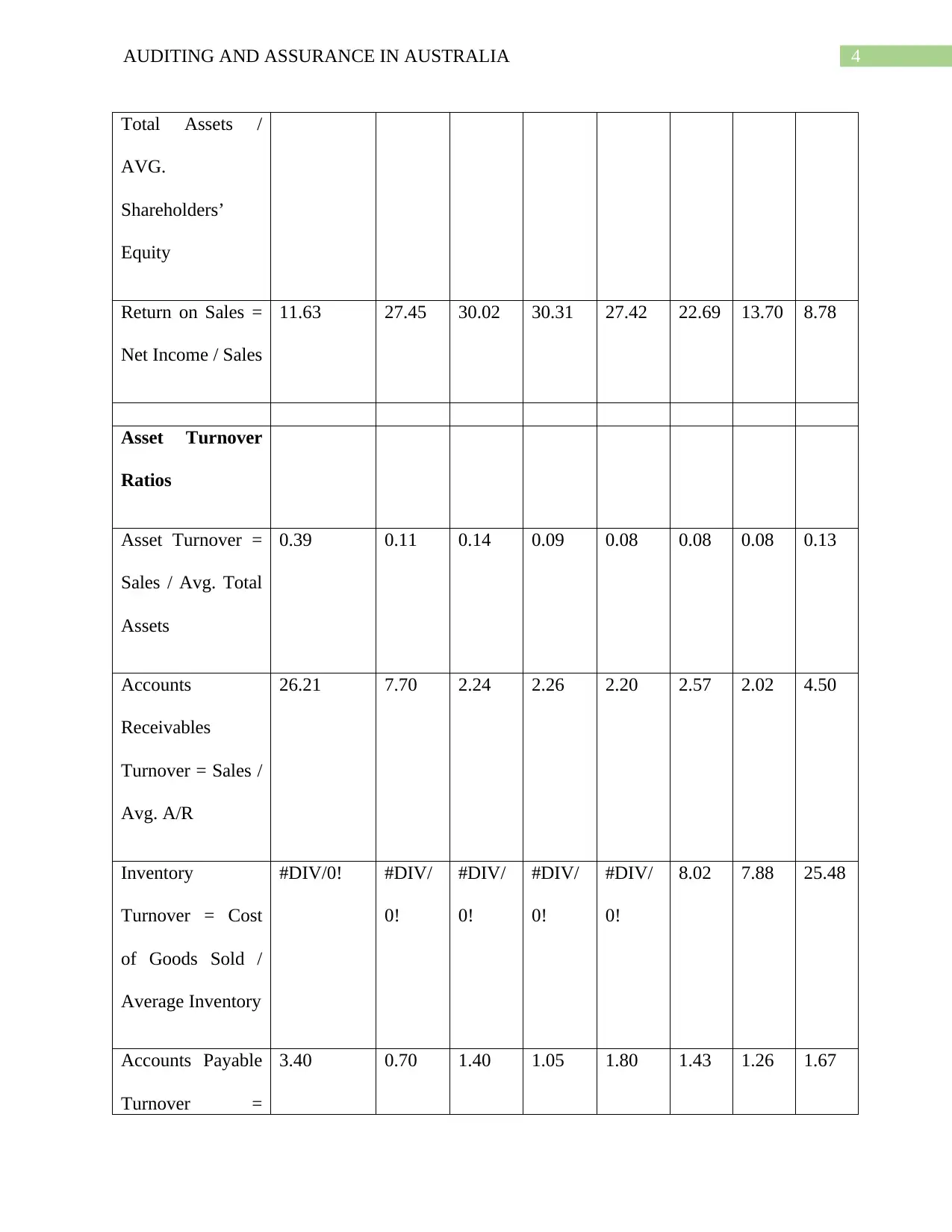

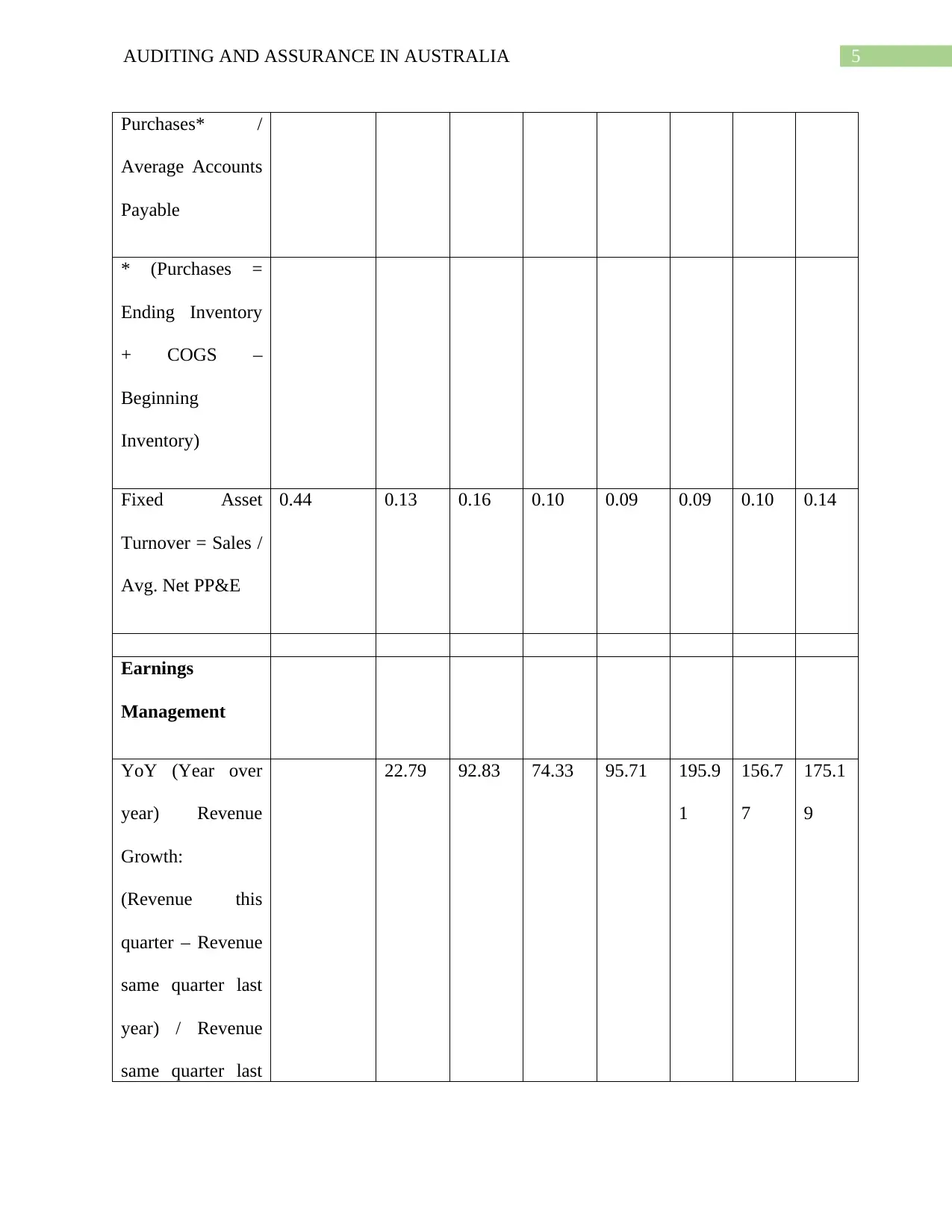

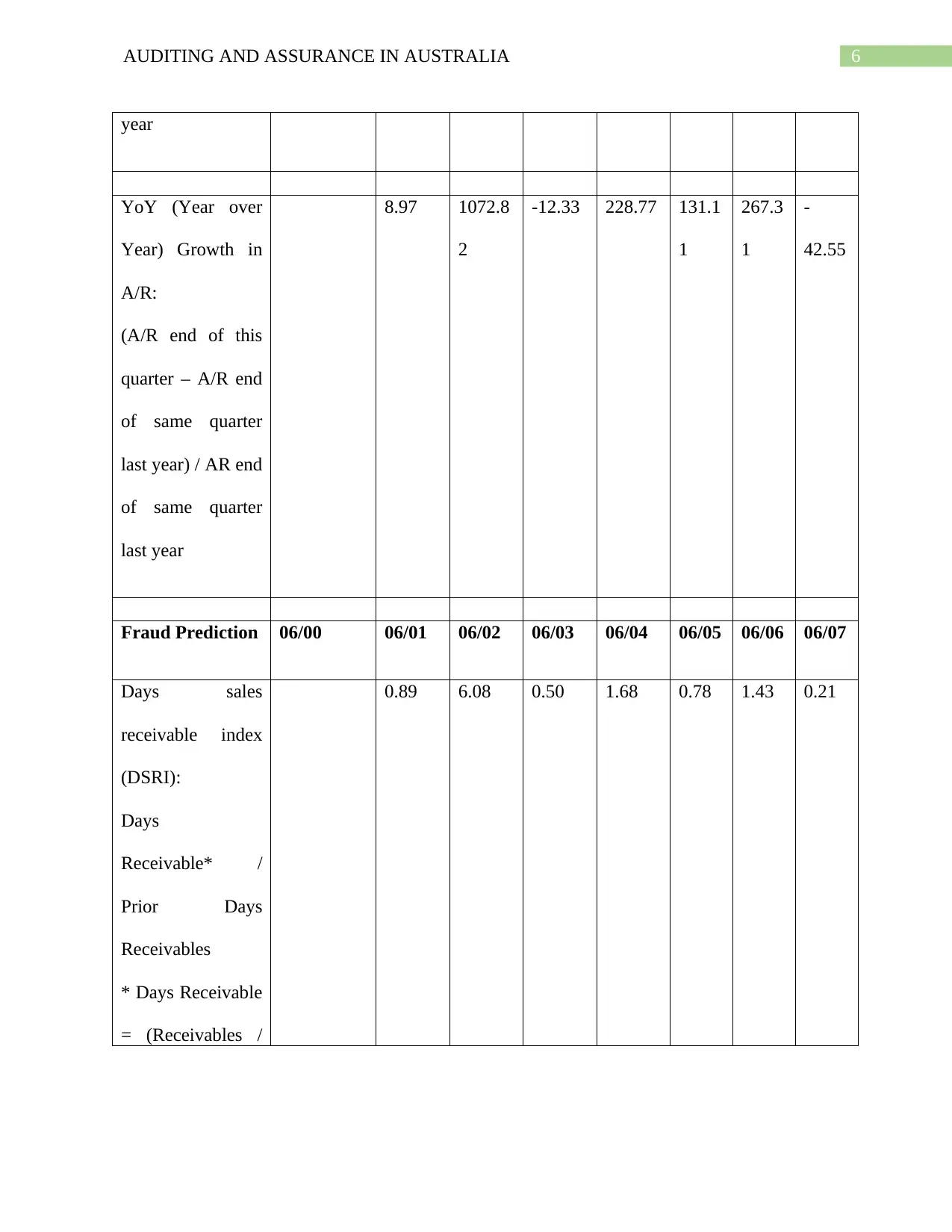

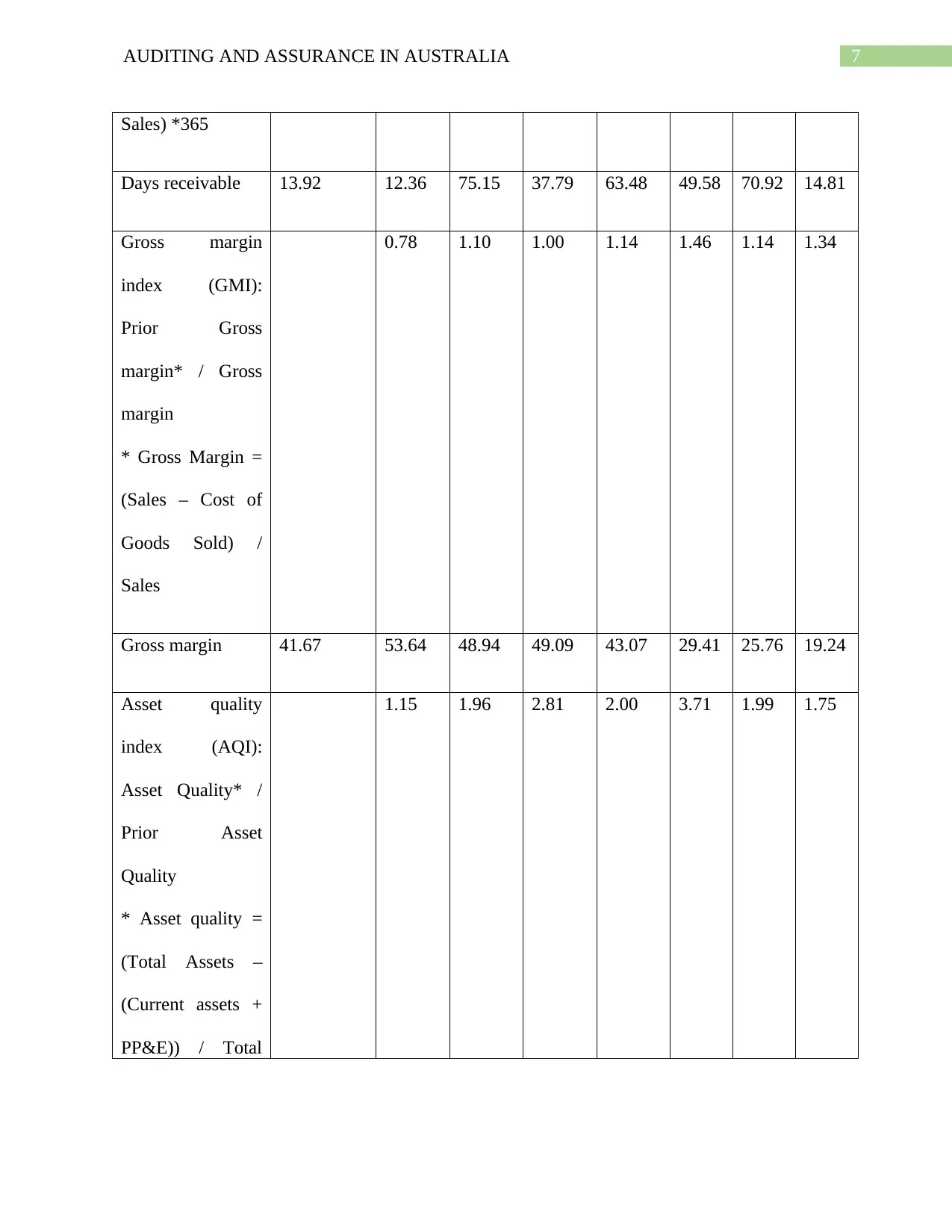

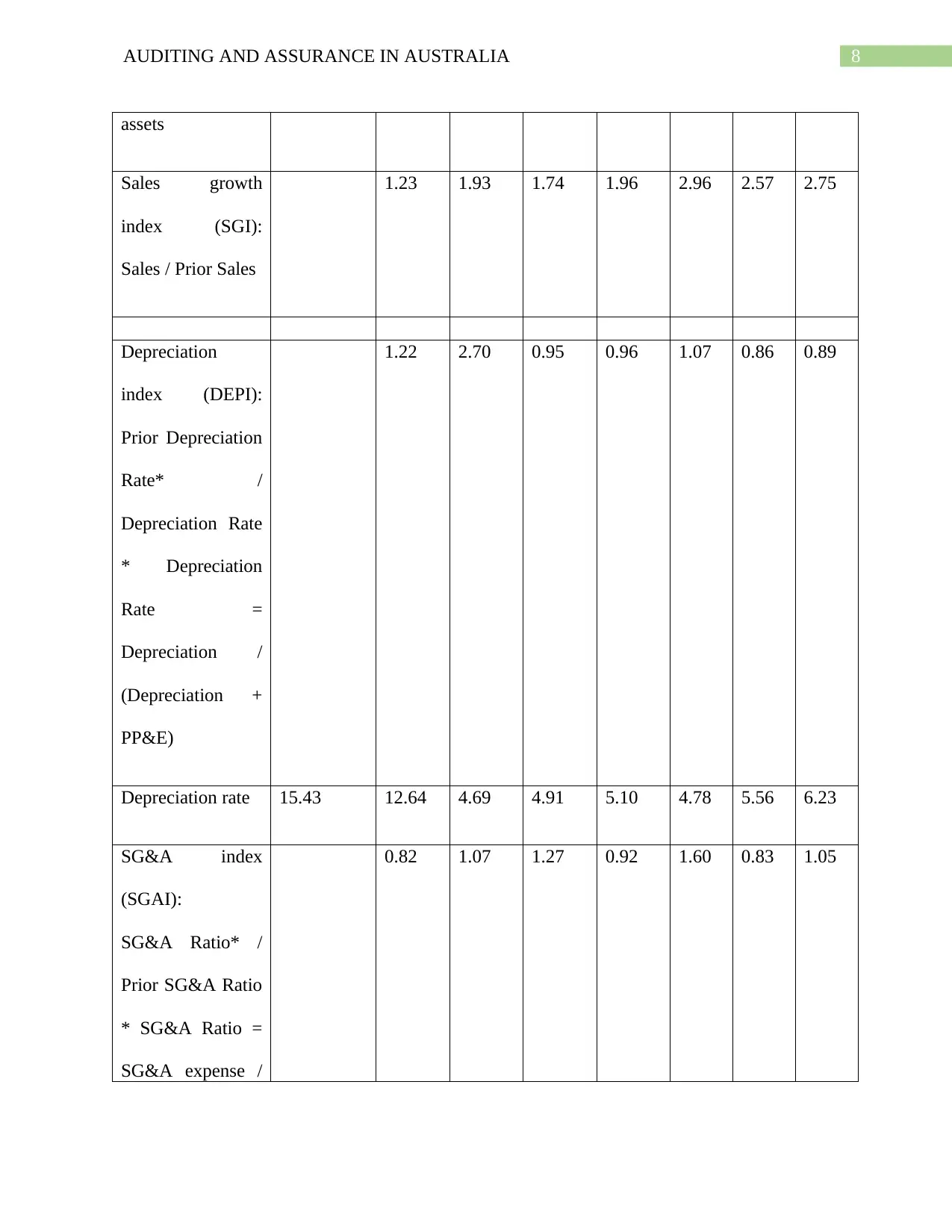

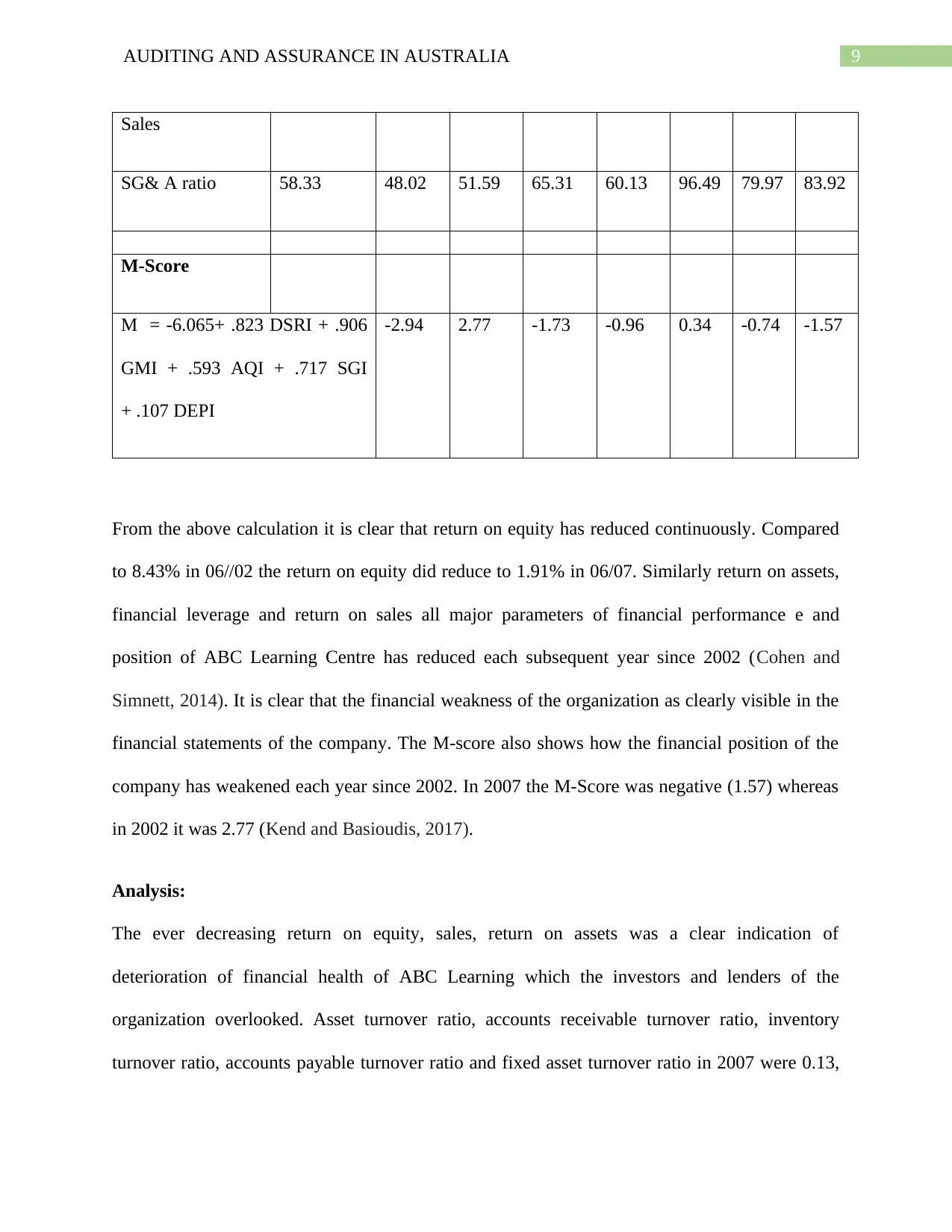

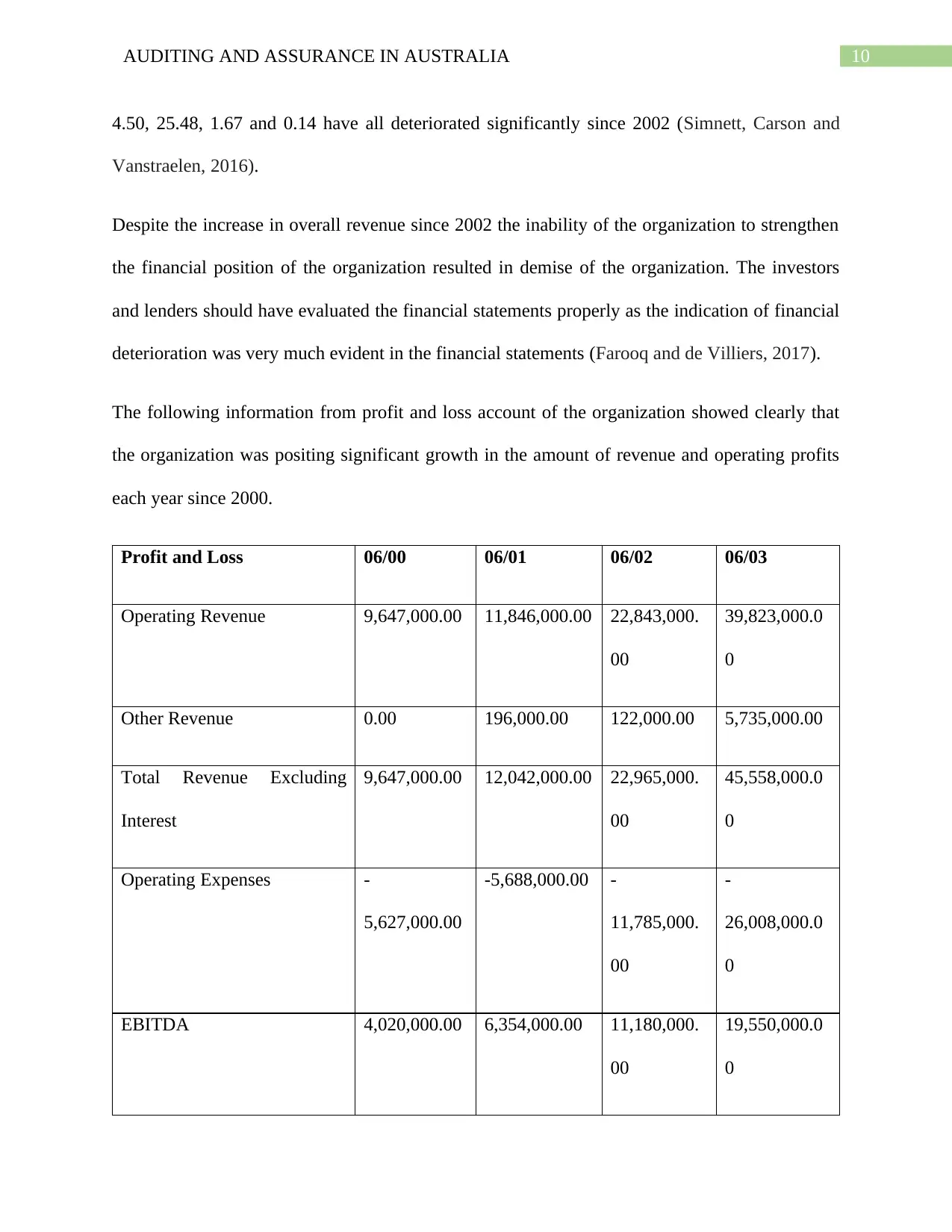

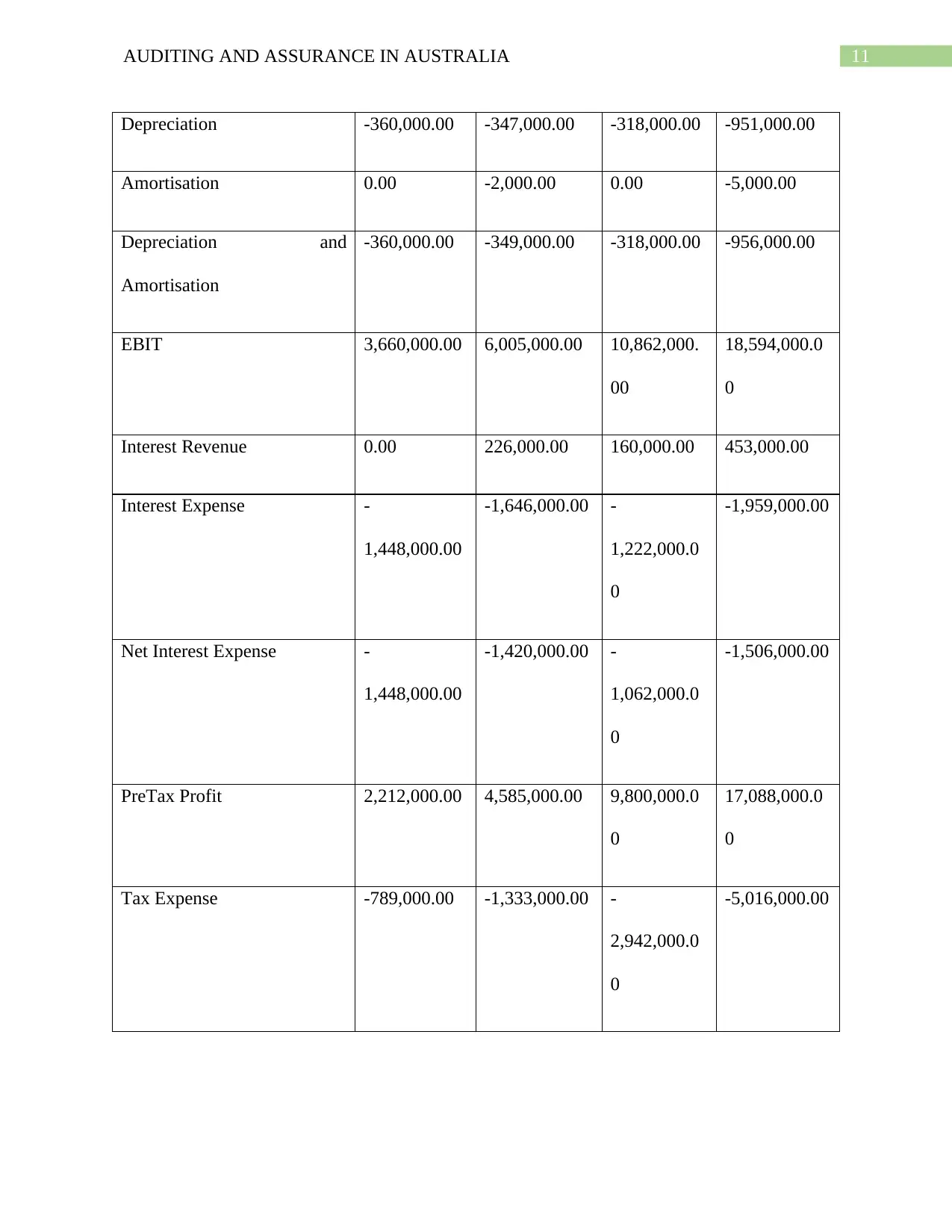

This essay provides a comprehensive analysis of the financial statements of ABC Learning Centres, aiming to determine if sufficient warning signals were present prior to its collapse. It applies DuPont analysis, common size trend analysis, and Beneish M-Score to evaluate the company's financial health from 2000 to 2007. The analysis reveals a continuous decline in key financial indicators such as return on equity, return on assets, and asset turnover ratios, despite reported revenue growth. The Beneish M-Score also indicates a weakening financial position over the years. The essay concludes that the deteriorating financial health was evident in the financial statements, suggesting that investors and lenders overlooked critical warning signs. The study recommends improved scrutiny of financial statements and the use of analytical tools for early detection of financial distress. Desklib offers a platform for students to access similar solved assignments and study resources.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.