Project Evaluation and Analysis: ABC Ltd. Expansion Plant, Finance

VerifiedAdded on 2022/12/14

|12

|2323

|426

Project

AI Summary

This finance project analyzes the expansion plan of ABC Ltd., focusing on project evaluation. The assignment begins by calculating the initial outlay, considering building and equipment costs, and net working capital. It then proceeds to calculate operating cash flow over four years, factoring in sales, variable manufacturing costs, fixed expenses, depreciation, and taxes to determine profit after tax and cash flow. The terminal cash flow is computed, incorporating the after-tax value of the building and equipment, along with working capital recovery. Subsequently, the Net Present Value (NPV) of the project is calculated to assess its financial viability. The project also includes a sensitivity analysis to assess the impact of changes in sales, variable costs, and the cost of capital, under both optimistic and pessimistic scenarios. Finally, a scenario analysis is performed to identify the best-case and worst-case scenarios. The project concludes that variable cost is the most sensitive element in the project.

1

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Task 1(a)..........................................................................................................................................3

Calculation of initial outlay.........................................................................................................3

Calculation of operating cash flow..............................................................................................3

Calculation of terminal cash flow................................................................................................4

Calculation of NPV......................................................................................................................4

Task 1(b)..........................................................................................................................................5

Sensitivity analysis......................................................................................................................5

Scenario analysis.......................................................................................................................10

References......................................................................................................................................11

Table of Contents

Task 1(a)..........................................................................................................................................3

Calculation of initial outlay.........................................................................................................3

Calculation of operating cash flow..............................................................................................3

Calculation of terminal cash flow................................................................................................4

Calculation of NPV......................................................................................................................4

Task 1(b)..........................................................................................................................................5

Sensitivity analysis......................................................................................................................5

Scenario analysis.......................................................................................................................10

References......................................................................................................................................11

3

Task 1(a)

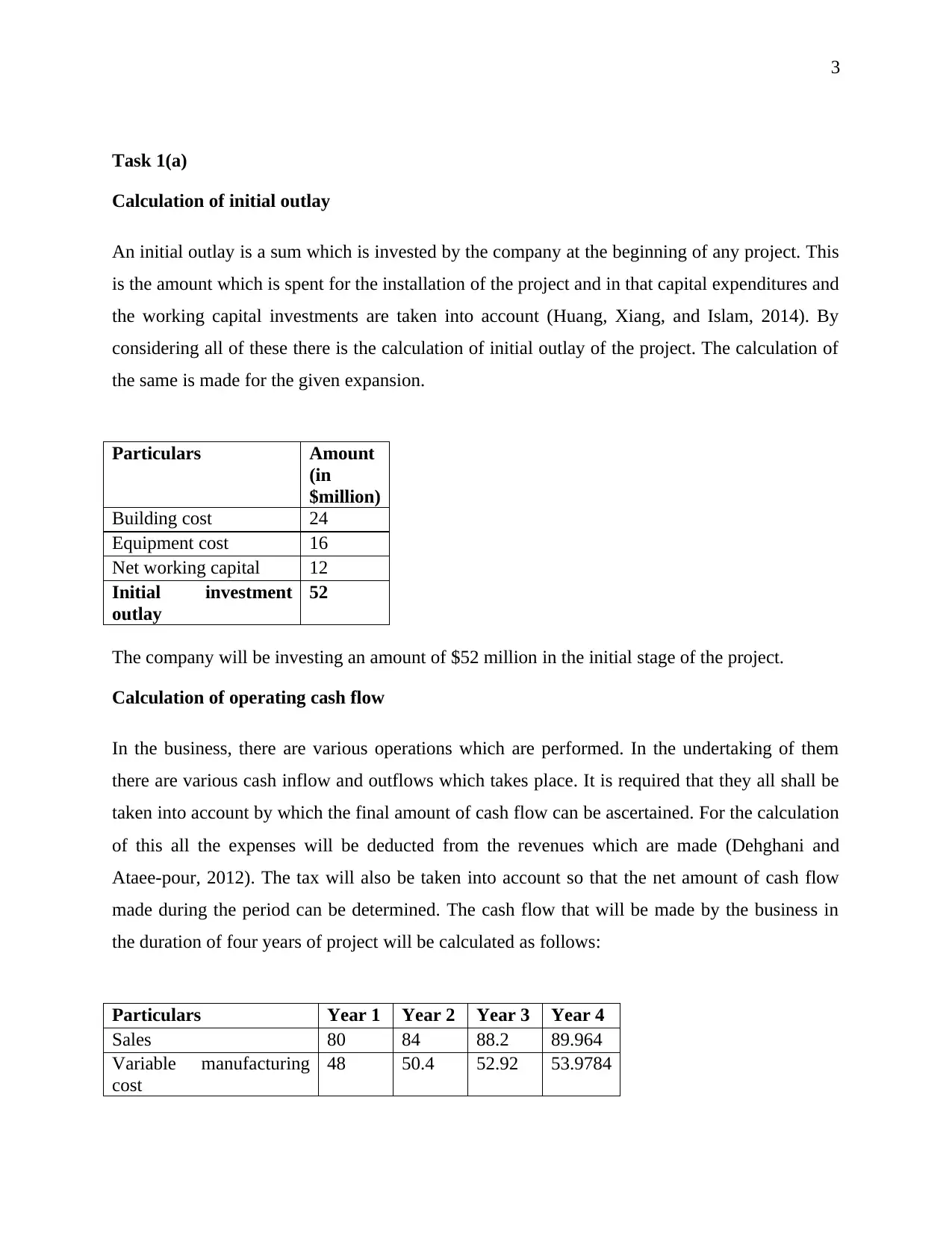

Calculation of initial outlay

An initial outlay is a sum which is invested by the company at the beginning of any project. This

is the amount which is spent for the installation of the project and in that capital expenditures and

the working capital investments are taken into account (Huang, Xiang, and Islam, 2014). By

considering all of these there is the calculation of initial outlay of the project. The calculation of

the same is made for the given expansion.

Particulars Amount

(in

$million)

Building cost 24

Equipment cost 16

Net working capital 12

Initial investment

outlay

52

The company will be investing an amount of $52 million in the initial stage of the project.

Calculation of operating cash flow

In the business, there are various operations which are performed. In the undertaking of them

there are various cash inflow and outflows which takes place. It is required that they all shall be

taken into account by which the final amount of cash flow can be ascertained. For the calculation

of this all the expenses will be deducted from the revenues which are made (Dehghani and

Ataee-pour, 2012). The tax will also be taken into account so that the net amount of cash flow

made during the period can be determined. The cash flow that will be made by the business in

the duration of four years of project will be calculated as follows:

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

48 50.4 52.92 53.9784

Task 1(a)

Calculation of initial outlay

An initial outlay is a sum which is invested by the company at the beginning of any project. This

is the amount which is spent for the installation of the project and in that capital expenditures and

the working capital investments are taken into account (Huang, Xiang, and Islam, 2014). By

considering all of these there is the calculation of initial outlay of the project. The calculation of

the same is made for the given expansion.

Particulars Amount

(in

$million)

Building cost 24

Equipment cost 16

Net working capital 12

Initial investment

outlay

52

The company will be investing an amount of $52 million in the initial stage of the project.

Calculation of operating cash flow

In the business, there are various operations which are performed. In the undertaking of them

there are various cash inflow and outflows which takes place. It is required that they all shall be

taken into account by which the final amount of cash flow can be ascertained. For the calculation

of this all the expenses will be deducted from the revenues which are made (Dehghani and

Ataee-pour, 2012). The tax will also be taken into account so that the net amount of cash flow

made during the period can be determined. The cash flow that will be made by the business in

the duration of four years of project will be calculated as follows:

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

48 50.4 52.92 53.9784

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

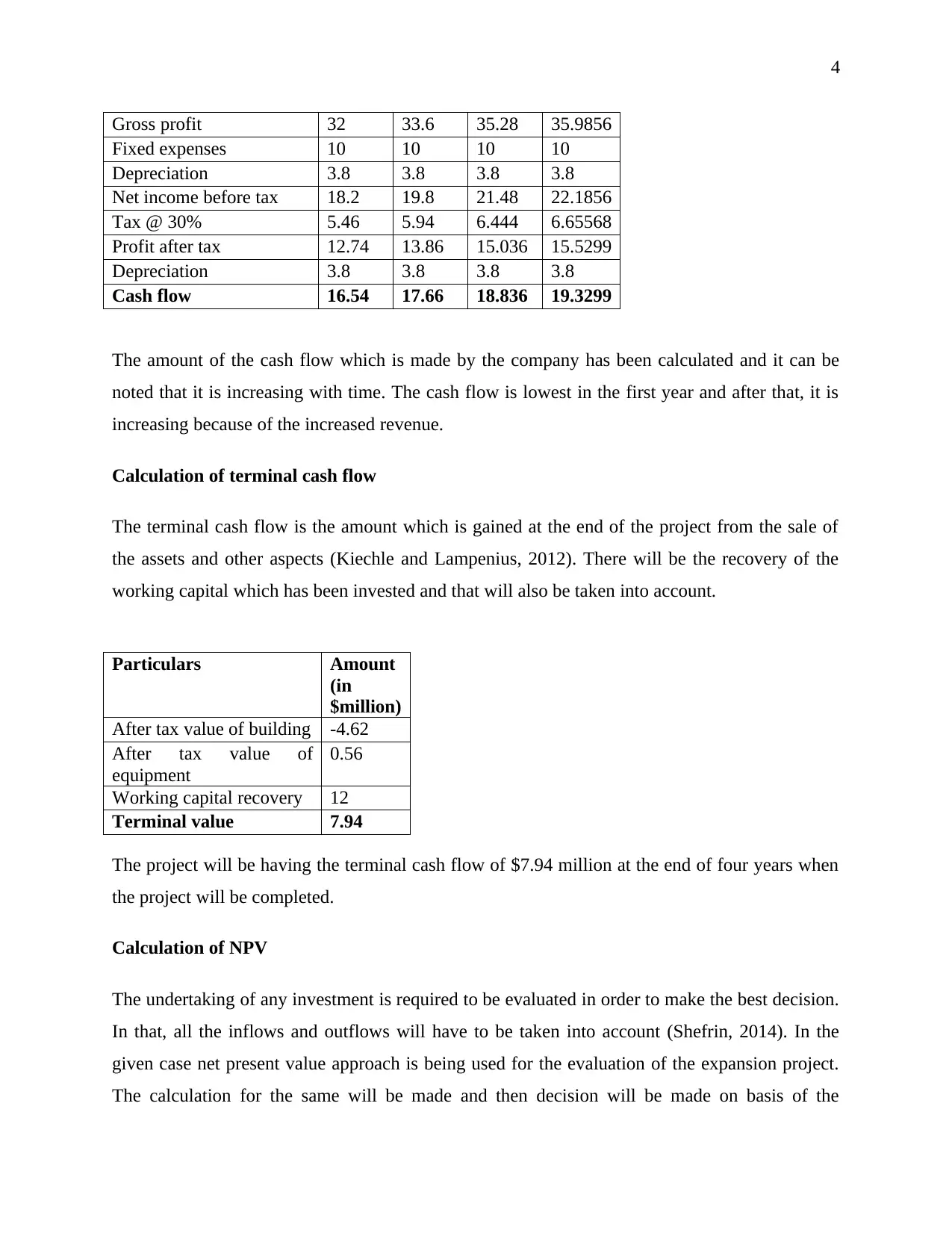

Gross profit 32 33.6 35.28 35.9856

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 18.2 19.8 21.48 22.1856

Tax @ 30% 5.46 5.94 6.444 6.65568

Profit after tax 12.74 13.86 15.036 15.5299

Depreciation 3.8 3.8 3.8 3.8

Cash flow 16.54 17.66 18.836 19.3299

The amount of the cash flow which is made by the company has been calculated and it can be

noted that it is increasing with time. The cash flow is lowest in the first year and after that, it is

increasing because of the increased revenue.

Calculation of terminal cash flow

The terminal cash flow is the amount which is gained at the end of the project from the sale of

the assets and other aspects (Kiechle and Lampenius, 2012). There will be the recovery of the

working capital which has been invested and that will also be taken into account.

Particulars Amount

(in

$million)

After tax value of building -4.62

After tax value of

equipment

0.56

Working capital recovery 12

Terminal value 7.94

The project will be having the terminal cash flow of $7.94 million at the end of four years when

the project will be completed.

Calculation of NPV

The undertaking of any investment is required to be evaluated in order to make the best decision.

In that, all the inflows and outflows will have to be taken into account (Shefrin, 2014). In the

given case net present value approach is being used for the evaluation of the expansion project.

The calculation for the same will be made and then decision will be made on basis of the

Gross profit 32 33.6 35.28 35.9856

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 18.2 19.8 21.48 22.1856

Tax @ 30% 5.46 5.94 6.444 6.65568

Profit after tax 12.74 13.86 15.036 15.5299

Depreciation 3.8 3.8 3.8 3.8

Cash flow 16.54 17.66 18.836 19.3299

The amount of the cash flow which is made by the company has been calculated and it can be

noted that it is increasing with time. The cash flow is lowest in the first year and after that, it is

increasing because of the increased revenue.

Calculation of terminal cash flow

The terminal cash flow is the amount which is gained at the end of the project from the sale of

the assets and other aspects (Kiechle and Lampenius, 2012). There will be the recovery of the

working capital which has been invested and that will also be taken into account.

Particulars Amount

(in

$million)

After tax value of building -4.62

After tax value of

equipment

0.56

Working capital recovery 12

Terminal value 7.94

The project will be having the terminal cash flow of $7.94 million at the end of four years when

the project will be completed.

Calculation of NPV

The undertaking of any investment is required to be evaluated in order to make the best decision.

In that, all the inflows and outflows will have to be taken into account (Shefrin, 2014). In the

given case net present value approach is being used for the evaluation of the expansion project.

The calculation for the same will be made and then decision will be made on basis of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

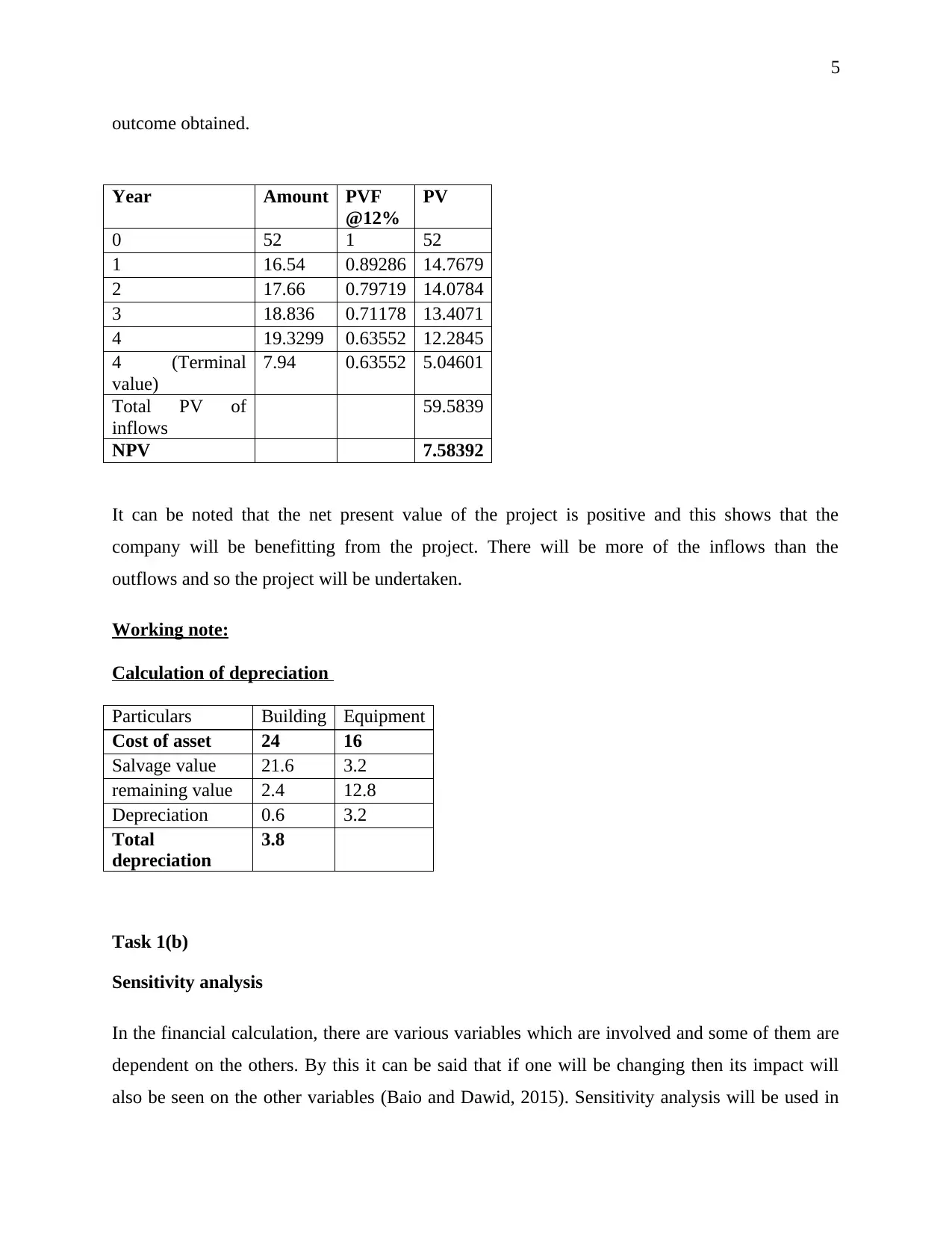

outcome obtained.

Year Amount PVF

@12%

PV

0 52 1 52

1 16.54 0.89286 14.7679

2 17.66 0.79719 14.0784

3 18.836 0.71178 13.4071

4 19.3299 0.63552 12.2845

4 (Terminal

value)

7.94 0.63552 5.04601

Total PV of

inflows

59.5839

NPV 7.58392

It can be noted that the net present value of the project is positive and this shows that the

company will be benefitting from the project. There will be more of the inflows than the

outflows and so the project will be undertaken.

Working note:

Calculation of depreciation

Particulars Building Equipment

Cost of asset 24 16

Salvage value 21.6 3.2

remaining value 2.4 12.8

Depreciation 0.6 3.2

Total

depreciation

3.8

Task 1(b)

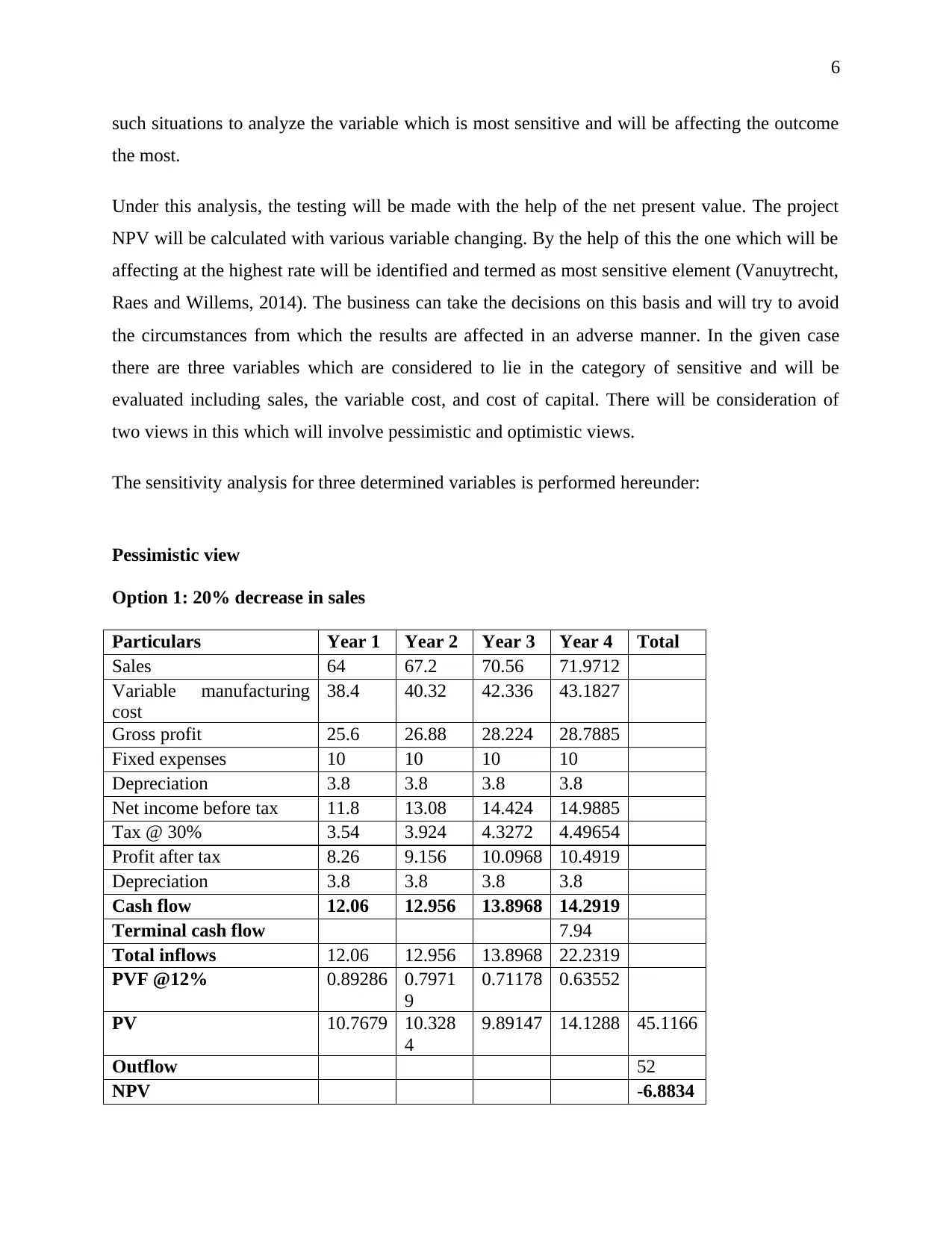

Sensitivity analysis

In the financial calculation, there are various variables which are involved and some of them are

dependent on the others. By this it can be said that if one will be changing then its impact will

also be seen on the other variables (Baio and Dawid, 2015). Sensitivity analysis will be used in

outcome obtained.

Year Amount PVF

@12%

PV

0 52 1 52

1 16.54 0.89286 14.7679

2 17.66 0.79719 14.0784

3 18.836 0.71178 13.4071

4 19.3299 0.63552 12.2845

4 (Terminal

value)

7.94 0.63552 5.04601

Total PV of

inflows

59.5839

NPV 7.58392

It can be noted that the net present value of the project is positive and this shows that the

company will be benefitting from the project. There will be more of the inflows than the

outflows and so the project will be undertaken.

Working note:

Calculation of depreciation

Particulars Building Equipment

Cost of asset 24 16

Salvage value 21.6 3.2

remaining value 2.4 12.8

Depreciation 0.6 3.2

Total

depreciation

3.8

Task 1(b)

Sensitivity analysis

In the financial calculation, there are various variables which are involved and some of them are

dependent on the others. By this it can be said that if one will be changing then its impact will

also be seen on the other variables (Baio and Dawid, 2015). Sensitivity analysis will be used in

6

such situations to analyze the variable which is most sensitive and will be affecting the outcome

the most.

Under this analysis, the testing will be made with the help of the net present value. The project

NPV will be calculated with various variable changing. By the help of this the one which will be

affecting at the highest rate will be identified and termed as most sensitive element (Vanuytrecht,

Raes and Willems, 2014). The business can take the decisions on this basis and will try to avoid

the circumstances from which the results are affected in an adverse manner. In the given case

there are three variables which are considered to lie in the category of sensitive and will be

evaluated including sales, the variable cost, and cost of capital. There will be consideration of

two views in this which will involve pessimistic and optimistic views.

The sensitivity analysis for three determined variables is performed hereunder:

Pessimistic view

Option 1: 20% decrease in sales

Particulars Year 1 Year 2 Year 3 Year 4 Total

Sales 64 67.2 70.56 71.9712

Variable manufacturing

cost

38.4 40.32 42.336 43.1827

Gross profit 25.6 26.88 28.224 28.7885

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 11.8 13.08 14.424 14.9885

Tax @ 30% 3.54 3.924 4.3272 4.49654

Profit after tax 8.26 9.156 10.0968 10.4919

Depreciation 3.8 3.8 3.8 3.8

Cash flow 12.06 12.956 13.8968 14.2919

Terminal cash flow 7.94

Total inflows 12.06 12.956 13.8968 22.2319

PVF @12% 0.89286 0.7971

9

0.71178 0.63552

PV 10.7679 10.328

4

9.89147 14.1288 45.1166

Outflow 52

NPV -6.8834

such situations to analyze the variable which is most sensitive and will be affecting the outcome

the most.

Under this analysis, the testing will be made with the help of the net present value. The project

NPV will be calculated with various variable changing. By the help of this the one which will be

affecting at the highest rate will be identified and termed as most sensitive element (Vanuytrecht,

Raes and Willems, 2014). The business can take the decisions on this basis and will try to avoid

the circumstances from which the results are affected in an adverse manner. In the given case

there are three variables which are considered to lie in the category of sensitive and will be

evaluated including sales, the variable cost, and cost of capital. There will be consideration of

two views in this which will involve pessimistic and optimistic views.

The sensitivity analysis for three determined variables is performed hereunder:

Pessimistic view

Option 1: 20% decrease in sales

Particulars Year 1 Year 2 Year 3 Year 4 Total

Sales 64 67.2 70.56 71.9712

Variable manufacturing

cost

38.4 40.32 42.336 43.1827

Gross profit 25.6 26.88 28.224 28.7885

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 11.8 13.08 14.424 14.9885

Tax @ 30% 3.54 3.924 4.3272 4.49654

Profit after tax 8.26 9.156 10.0968 10.4919

Depreciation 3.8 3.8 3.8 3.8

Cash flow 12.06 12.956 13.8968 14.2919

Terminal cash flow 7.94

Total inflows 12.06 12.956 13.8968 22.2319

PVF @12% 0.89286 0.7971

9

0.71178 0.63552

PV 10.7679 10.328

4

9.89147 14.1288 45.1166

Outflow 52

NPV -6.8834

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

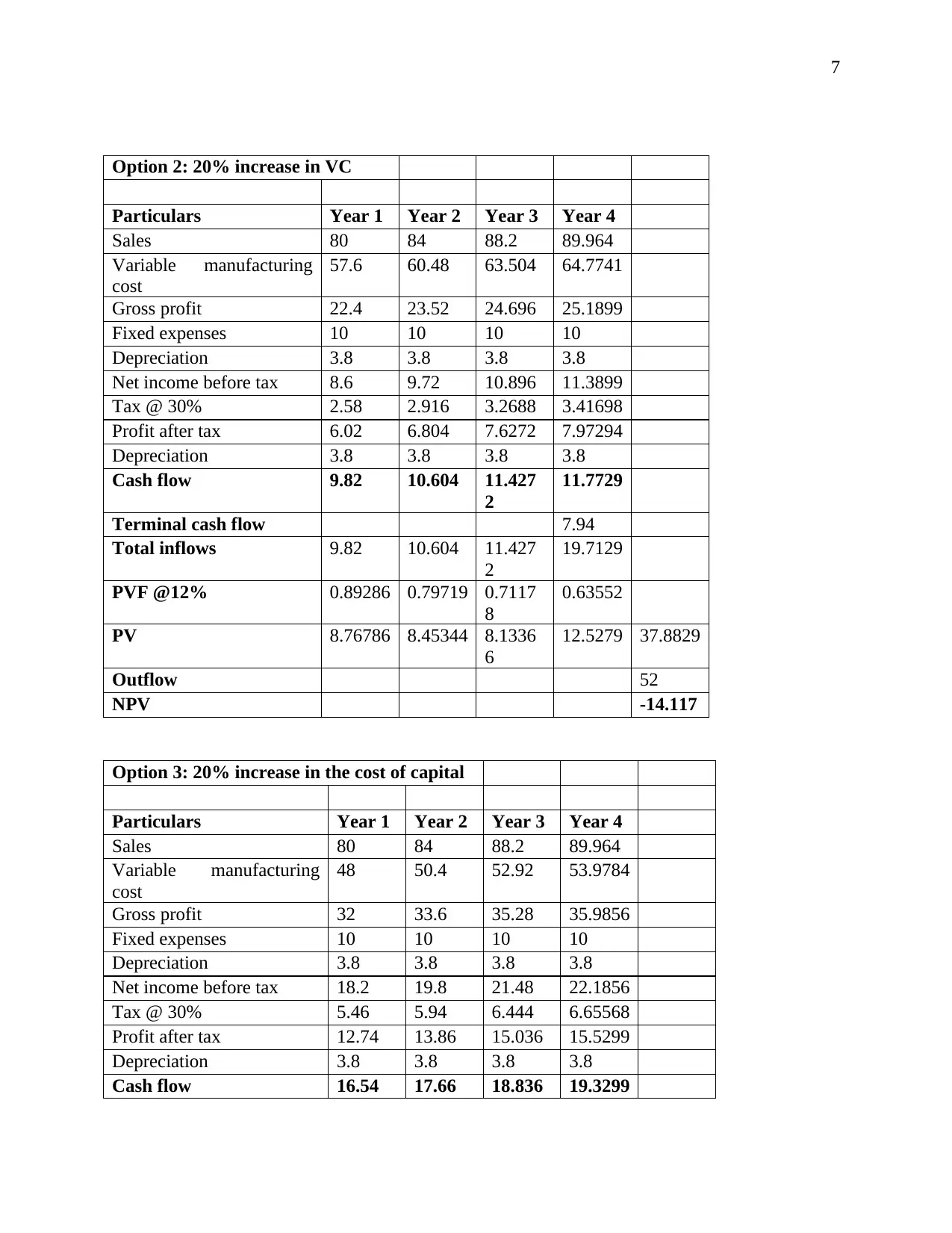

Option 2: 20% increase in VC

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

57.6 60.48 63.504 64.7741

Gross profit 22.4 23.52 24.696 25.1899

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 8.6 9.72 10.896 11.3899

Tax @ 30% 2.58 2.916 3.2688 3.41698

Profit after tax 6.02 6.804 7.6272 7.97294

Depreciation 3.8 3.8 3.8 3.8

Cash flow 9.82 10.604 11.427

2

11.7729

Terminal cash flow 7.94

Total inflows 9.82 10.604 11.427

2

19.7129

PVF @12% 0.89286 0.79719 0.7117

8

0.63552

PV 8.76786 8.45344 8.1336

6

12.5279 37.8829

Outflow 52

NPV -14.117

Option 3: 20% increase in the cost of capital

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

48 50.4 52.92 53.9784

Gross profit 32 33.6 35.28 35.9856

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 18.2 19.8 21.48 22.1856

Tax @ 30% 5.46 5.94 6.444 6.65568

Profit after tax 12.74 13.86 15.036 15.5299

Depreciation 3.8 3.8 3.8 3.8

Cash flow 16.54 17.66 18.836 19.3299

Option 2: 20% increase in VC

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

57.6 60.48 63.504 64.7741

Gross profit 22.4 23.52 24.696 25.1899

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 8.6 9.72 10.896 11.3899

Tax @ 30% 2.58 2.916 3.2688 3.41698

Profit after tax 6.02 6.804 7.6272 7.97294

Depreciation 3.8 3.8 3.8 3.8

Cash flow 9.82 10.604 11.427

2

11.7729

Terminal cash flow 7.94

Total inflows 9.82 10.604 11.427

2

19.7129

PVF @12% 0.89286 0.79719 0.7117

8

0.63552

PV 8.76786 8.45344 8.1336

6

12.5279 37.8829

Outflow 52

NPV -14.117

Option 3: 20% increase in the cost of capital

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

48 50.4 52.92 53.9784

Gross profit 32 33.6 35.28 35.9856

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 18.2 19.8 21.48 22.1856

Tax @ 30% 5.46 5.94 6.444 6.65568

Profit after tax 12.74 13.86 15.036 15.5299

Depreciation 3.8 3.8 3.8 3.8

Cash flow 16.54 17.66 18.836 19.3299

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Terminal cash flow 7.94

Total inflows 16.54 17.66 18.836 27.2699

PVF @14.4% 0.8741

3

0.7641 0.66792 0.58384

PV 14.458 13.4939 12.5809 15.9213 56.4542

Outflow 52

NPV 4.45419

Optimistic view

Option 4: 20% increase in sales

Particulars Year 1 Year 2 Year 3 Year 4 Total

Sales 96 100.8 105.84 107.957

Variable manufacturing

cost

57.6 60.48 63.504 64.7741

Gross profit 38.4 40.32 42.336 43.1827

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 24.6 26.52 28.536 29.3827

Tax @ 30% 7.38 7.956 8.5608 8.81482

Profit after tax 17.22 18.564 19.975

2

20.5679

Depreciation 3.8 3.8 3.8 3.8

Cash flow 21.02 22.364 23.775

2

24.3679

Terminal cash flow 7.94

Total inflows 21.02 22.364 23.775

2

32.3079

PVF @12% 0.89286 0.79719 0.7117

8

0.63552

PV 18.7679 17.8284 16.922

7

20.5323 74.0513

Outflow 52

NPV 22.0513

Option 5: 20% decrease in VC

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing 38.4 40.32 42.336 43.182

Terminal cash flow 7.94

Total inflows 16.54 17.66 18.836 27.2699

PVF @14.4% 0.8741

3

0.7641 0.66792 0.58384

PV 14.458 13.4939 12.5809 15.9213 56.4542

Outflow 52

NPV 4.45419

Optimistic view

Option 4: 20% increase in sales

Particulars Year 1 Year 2 Year 3 Year 4 Total

Sales 96 100.8 105.84 107.957

Variable manufacturing

cost

57.6 60.48 63.504 64.7741

Gross profit 38.4 40.32 42.336 43.1827

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 24.6 26.52 28.536 29.3827

Tax @ 30% 7.38 7.956 8.5608 8.81482

Profit after tax 17.22 18.564 19.975

2

20.5679

Depreciation 3.8 3.8 3.8 3.8

Cash flow 21.02 22.364 23.775

2

24.3679

Terminal cash flow 7.94

Total inflows 21.02 22.364 23.775

2

32.3079

PVF @12% 0.89286 0.79719 0.7117

8

0.63552

PV 18.7679 17.8284 16.922

7

20.5323 74.0513

Outflow 52

NPV 22.0513

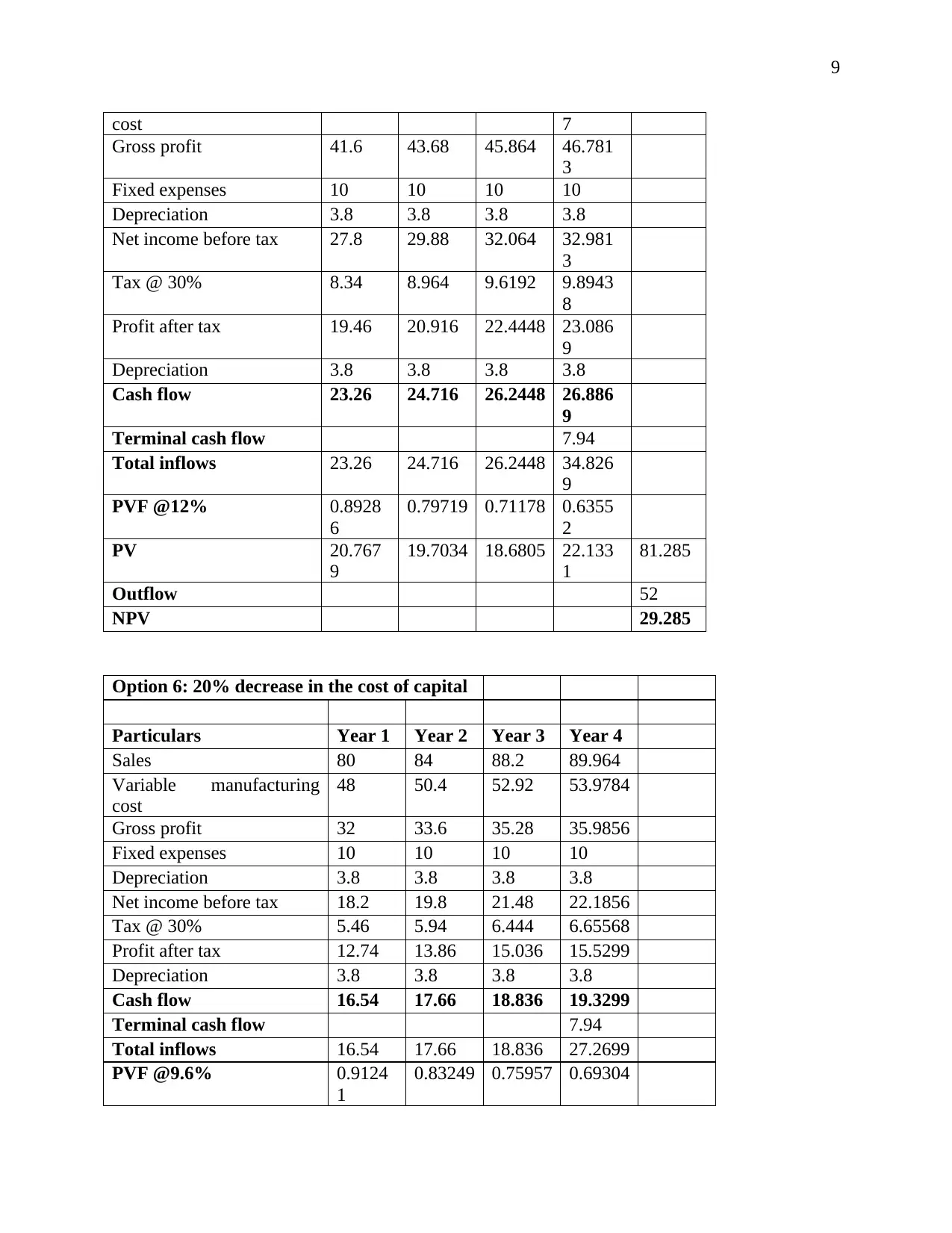

Option 5: 20% decrease in VC

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing 38.4 40.32 42.336 43.182

9

cost 7

Gross profit 41.6 43.68 45.864 46.781

3

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 27.8 29.88 32.064 32.981

3

Tax @ 30% 8.34 8.964 9.6192 9.8943

8

Profit after tax 19.46 20.916 22.4448 23.086

9

Depreciation 3.8 3.8 3.8 3.8

Cash flow 23.26 24.716 26.2448 26.886

9

Terminal cash flow 7.94

Total inflows 23.26 24.716 26.2448 34.826

9

PVF @12% 0.8928

6

0.79719 0.71178 0.6355

2

PV 20.767

9

19.7034 18.6805 22.133

1

81.285

Outflow 52

NPV 29.285

Option 6: 20% decrease in the cost of capital

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

48 50.4 52.92 53.9784

Gross profit 32 33.6 35.28 35.9856

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 18.2 19.8 21.48 22.1856

Tax @ 30% 5.46 5.94 6.444 6.65568

Profit after tax 12.74 13.86 15.036 15.5299

Depreciation 3.8 3.8 3.8 3.8

Cash flow 16.54 17.66 18.836 19.3299

Terminal cash flow 7.94

Total inflows 16.54 17.66 18.836 27.2699

PVF @9.6% 0.9124

1

0.83249 0.75957 0.69304

cost 7

Gross profit 41.6 43.68 45.864 46.781

3

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 27.8 29.88 32.064 32.981

3

Tax @ 30% 8.34 8.964 9.6192 9.8943

8

Profit after tax 19.46 20.916 22.4448 23.086

9

Depreciation 3.8 3.8 3.8 3.8

Cash flow 23.26 24.716 26.2448 26.886

9

Terminal cash flow 7.94

Total inflows 23.26 24.716 26.2448 34.826

9

PVF @12% 0.8928

6

0.79719 0.71178 0.6355

2

PV 20.767

9

19.7034 18.6805 22.133

1

81.285

Outflow 52

NPV 29.285

Option 6: 20% decrease in the cost of capital

Particulars Year 1 Year 2 Year 3 Year 4

Sales 80 84 88.2 89.964

Variable manufacturing

cost

48 50.4 52.92 53.9784

Gross profit 32 33.6 35.28 35.9856

Fixed expenses 10 10 10 10

Depreciation 3.8 3.8 3.8 3.8

Net income before tax 18.2 19.8 21.48 22.1856

Tax @ 30% 5.46 5.94 6.444 6.65568

Profit after tax 12.74 13.86 15.036 15.5299

Depreciation 3.8 3.8 3.8 3.8

Cash flow 16.54 17.66 18.836 19.3299

Terminal cash flow 7.94

Total inflows 16.54 17.66 18.836 27.2699

PVF @9.6% 0.9124

1

0.83249 0.75957 0.69304

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

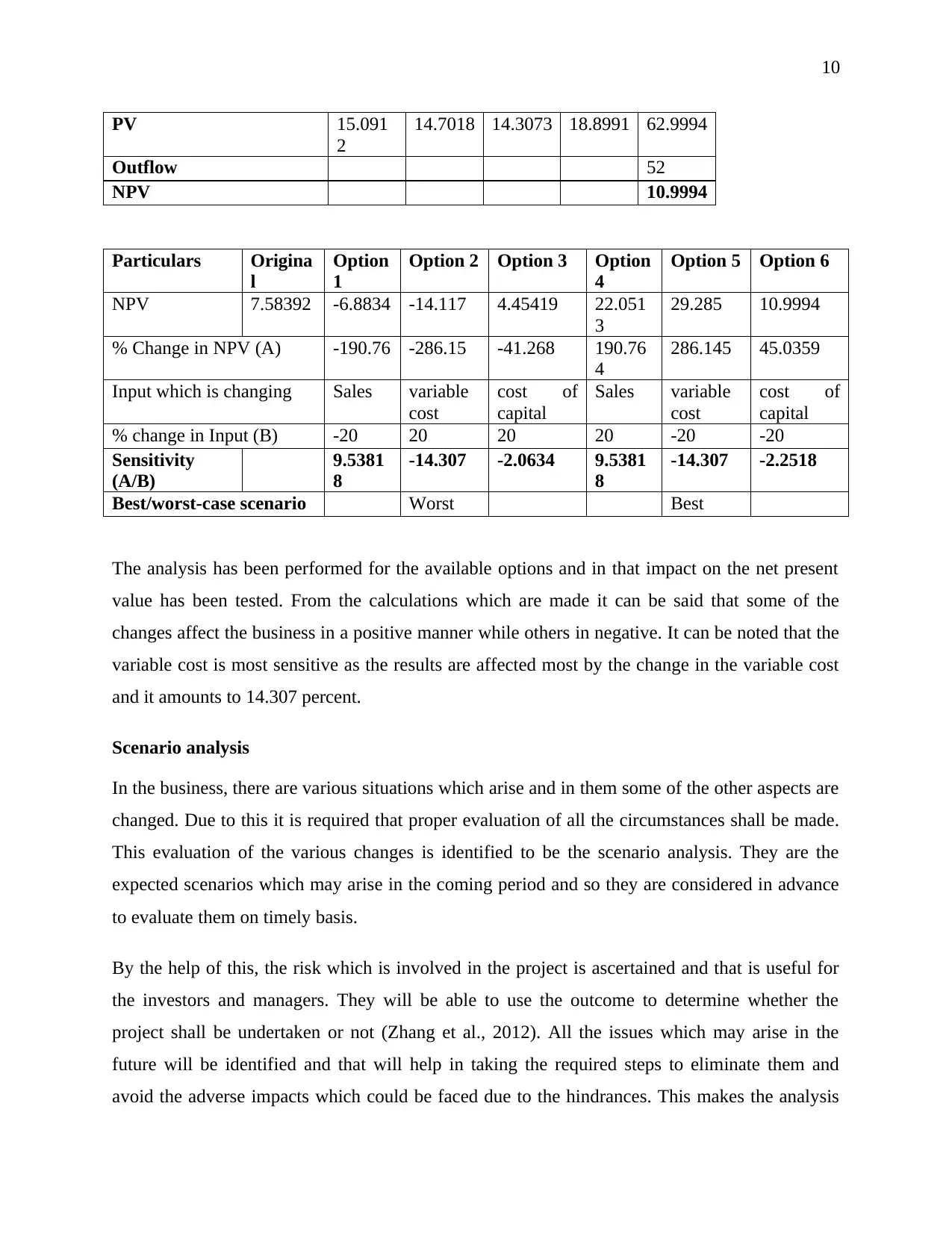

PV 15.091

2

14.7018 14.3073 18.8991 62.9994

Outflow 52

NPV 10.9994

Particulars Origina

l

Option

1

Option 2 Option 3 Option

4

Option 5 Option 6

NPV 7.58392 -6.8834 -14.117 4.45419 22.051

3

29.285 10.9994

% Change in NPV (A) -190.76 -286.15 -41.268 190.76

4

286.145 45.0359

Input which is changing Sales variable

cost

cost of

capital

Sales variable

cost

cost of

capital

% change in Input (B) -20 20 20 20 -20 -20

Sensitivity

(A/B)

9.5381

8

-14.307 -2.0634 9.5381

8

-14.307 -2.2518

Best/worst-case scenario Worst Best

The analysis has been performed for the available options and in that impact on the net present

value has been tested. From the calculations which are made it can be said that some of the

changes affect the business in a positive manner while others in negative. It can be noted that the

variable cost is most sensitive as the results are affected most by the change in the variable cost

and it amounts to 14.307 percent.

Scenario analysis

In the business, there are various situations which arise and in them some of the other aspects are

changed. Due to this it is required that proper evaluation of all the circumstances shall be made.

This evaluation of the various changes is identified to be the scenario analysis. They are the

expected scenarios which may arise in the coming period and so they are considered in advance

to evaluate them on timely basis.

By the help of this, the risk which is involved in the project is ascertained and that is useful for

the investors and managers. They will be able to use the outcome to determine whether the

project shall be undertaken or not (Zhang et al., 2012). All the issues which may arise in the

future will be identified and that will help in taking the required steps to eliminate them and

avoid the adverse impacts which could be faced due to the hindrances. This makes the analysis

PV 15.091

2

14.7018 14.3073 18.8991 62.9994

Outflow 52

NPV 10.9994

Particulars Origina

l

Option

1

Option 2 Option 3 Option

4

Option 5 Option 6

NPV 7.58392 -6.8834 -14.117 4.45419 22.051

3

29.285 10.9994

% Change in NPV (A) -190.76 -286.15 -41.268 190.76

4

286.145 45.0359

Input which is changing Sales variable

cost

cost of

capital

Sales variable

cost

cost of

capital

% change in Input (B) -20 20 20 20 -20 -20

Sensitivity

(A/B)

9.5381

8

-14.307 -2.0634 9.5381

8

-14.307 -2.2518

Best/worst-case scenario Worst Best

The analysis has been performed for the available options and in that impact on the net present

value has been tested. From the calculations which are made it can be said that some of the

changes affect the business in a positive manner while others in negative. It can be noted that the

variable cost is most sensitive as the results are affected most by the change in the variable cost

and it amounts to 14.307 percent.

Scenario analysis

In the business, there are various situations which arise and in them some of the other aspects are

changed. Due to this it is required that proper evaluation of all the circumstances shall be made.

This evaluation of the various changes is identified to be the scenario analysis. They are the

expected scenarios which may arise in the coming period and so they are considered in advance

to evaluate them on timely basis.

By the help of this, the risk which is involved in the project is ascertained and that is useful for

the investors and managers. They will be able to use the outcome to determine whether the

project shall be undertaken or not (Zhang et al., 2012). All the issues which may arise in the

future will be identified and that will help in taking the required steps to eliminate them and

avoid the adverse impacts which could be faced due to the hindrances. This makes the analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

useful and in this best-case and worst-case scenarios are identified. From the calculations which

are made above it can be noted that option 2 with increase in the variable cost by 20% is the

worst case as the net present value in such case will be negative. The decrease in the variable

cost by 20% has been made and with that highest amount of NPV is made possible. Due to this it

will be considered as the best-case scenario.

useful and in this best-case and worst-case scenarios are identified. From the calculations which

are made above it can be noted that option 2 with increase in the variable cost by 20% is the

worst case as the net present value in such case will be negative. The decrease in the variable

cost by 20% has been made and with that highest amount of NPV is made possible. Due to this it

will be considered as the best-case scenario.

12

References

Baio, G. and Dawid, A.P. (2015) Probabilistic sensitivity analysis in health

economics. Statistical methods in medical research, 24(6), pp.615-634.

Dehghani, H. and Ataee-pour, M. (2012) Determination of the effect of operating cost

uncertainty on mining project evaluation. Resources Policy, 37(1), pp.109-117.

Huang, X., Xiang, L. and Islam, S.M. (2014) Optimal project adjustment and

selection. Economic Modelling, 36, pp.391-397.

Kiechle, D. and Lampenius, N. (2012) The Terminal Value and Inflation Controversy. Journal of

Applied Corporate Finance, 24(3), pp.101-107.

Shefrin, H. (2014) Free cash Flow, Valuation and Growth Opportunities Bias. Journal of

Investment Management, 12(4), pp.4-26.

Vanuytrecht, E., Raes, D. and Willems, P. (2014) Global sensitivity analysis of yield output from

the water productivity model. Environmental Modelling & Software, 51, pp.323-332.

Zhang, Q., Ishihara, K.N., Mclellan, B.C. and Tezuka, T. (2012) Scenario analysis on future

electricity supply and demand in Japan. Energy, 38(1), pp.376-385.

References

Baio, G. and Dawid, A.P. (2015) Probabilistic sensitivity analysis in health

economics. Statistical methods in medical research, 24(6), pp.615-634.

Dehghani, H. and Ataee-pour, M. (2012) Determination of the effect of operating cost

uncertainty on mining project evaluation. Resources Policy, 37(1), pp.109-117.

Huang, X., Xiang, L. and Islam, S.M. (2014) Optimal project adjustment and

selection. Economic Modelling, 36, pp.391-397.

Kiechle, D. and Lampenius, N. (2012) The Terminal Value and Inflation Controversy. Journal of

Applied Corporate Finance, 24(3), pp.101-107.

Shefrin, H. (2014) Free cash Flow, Valuation and Growth Opportunities Bias. Journal of

Investment Management, 12(4), pp.4-26.

Vanuytrecht, E., Raes, D. and Willems, P. (2014) Global sensitivity analysis of yield output from

the water productivity model. Environmental Modelling & Software, 51, pp.323-332.

Zhang, Q., Ishihara, K.N., Mclellan, B.C. and Tezuka, T. (2012) Scenario analysis on future

electricity supply and demand in Japan. Energy, 38(1), pp.376-385.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.