Management Accounting Report: ABC Ltd Cost Analysis and Control

VerifiedAdded on 2021/02/19

|19

|5249

|87

Report

AI Summary

This report provides a comprehensive overview of management accounting practices within ABC Ltd, a medium-sized manufacturing company in the United Kingdom. It begins by defining management accounting and exploring different types of management accounting systems, including cost accounting, price optimization, inventory management, and job costing, highlighting their requirements and benefits. The report then details various methods used for preparing management accounting reports, such as budgets, performance reports, inventory and manufacturing reports, and job cost reports, emphasizing their role in performance measurement and control. Furthermore, it integrates the management accounting system with the reports to evaluate the company's performance and strategy. The core of the report focuses on calculating net profit or loss using marginal and absorption costing methods, providing practical examples for ABC Ltd. Finally, it discusses the advantages and disadvantages of different planning tools used for budgetary control and explores the application of management accounting systems in addressing financial problems, such as budget variances and changes in sales and profit, offering insights for developing the efficiency of the company. The report concludes by summarizing the key findings and providing relevant references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Explaining the meaning of management accounting and different kinds of management

accounting systems...................................................................................................................3

P2 various method used by the organization for preparation of management accounting

report.........................................................................................................................................6

Integration of management accounting system and management accounting report...............7

LO 2 ................................................................................................................................................8

P 3 Calculation of Net Profit or Loss under Marginal Costing and Absorption Costing for

ABC Ltd. ..................................................................................................................................8

LO 3 ..............................................................................................................................................12

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................12

P5 Explaining range of management accounting systems for developing efficiency of

company in responding to various financial problems...........................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

LO 1.................................................................................................................................................3

P1 Explaining the meaning of management accounting and different kinds of management

accounting systems...................................................................................................................3

P2 various method used by the organization for preparation of management accounting

report.........................................................................................................................................6

Integration of management accounting system and management accounting report...............7

LO 2 ................................................................................................................................................8

P 3 Calculation of Net Profit or Loss under Marginal Costing and Absorption Costing for

ABC Ltd. ..................................................................................................................................8

LO 3 ..............................................................................................................................................12

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................12

P5 Explaining range of management accounting systems for developing efficiency of

company in responding to various financial problems...........................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is the process recording, analysing, measuring and evaluating

the financial data by using the various tools to get the information for making decision for the

organization. The aim of management accounting is to support the manager in decision-making

process and analyse the financial data. The report is about ABC Limited, which is a medium size

manufacturing company operating in United Kingdom. The aim of report is to explain the role of

management accounting and requirement of various accounting system to the organization to

evaluate the performance and control the cost of the company. It also explains the different

method used by the company to reporting the management accounting like the balance sheet,

profit and loss account and income statements. It highlights the use of marginal and absorption

cost to prepare the income statement and various advantages and disadvantages of the planning

tool like zero base budgeting, increment budget etc. The report also help to focus on the MA

system to resolve the financial problem like variances in budget, change in sales and profit etc.

LO 1

P1 Explaining the meaning of management accounting and different kinds of management

accounting systems

Managerial accounting is defined as a procedure of systematically recording, evaluating and

analyzing the cost and financial information of an entity for the purpose of preparing accurate

internal financial reports, statistical information which is needed by the business managers for

exercising their day to day functions. Tools and techniques of management accounting also

facilitates the managers with the required information regarding log term decisions such as

acquisition of capital assets, undertaking of a particular project etc. This is done by assessing

their feasibility and profitability. Such decisions are taken with the help of financial

modeling,capital budgeting etc. (Mouritsen and Kreiner, 2016).

Difference between financial and managerial accounting :

Basis Management accounting Financial accounting

focus managerial accounting’s aim to

provide the managers with needed

financial and cost related

financial accounting focuses on

preparing the financial reports for

all the interested parties or

3

Management accounting is the process recording, analysing, measuring and evaluating

the financial data by using the various tools to get the information for making decision for the

organization. The aim of management accounting is to support the manager in decision-making

process and analyse the financial data. The report is about ABC Limited, which is a medium size

manufacturing company operating in United Kingdom. The aim of report is to explain the role of

management accounting and requirement of various accounting system to the organization to

evaluate the performance and control the cost of the company. It also explains the different

method used by the company to reporting the management accounting like the balance sheet,

profit and loss account and income statements. It highlights the use of marginal and absorption

cost to prepare the income statement and various advantages and disadvantages of the planning

tool like zero base budgeting, increment budget etc. The report also help to focus on the MA

system to resolve the financial problem like variances in budget, change in sales and profit etc.

LO 1

P1 Explaining the meaning of management accounting and different kinds of management

accounting systems

Managerial accounting is defined as a procedure of systematically recording, evaluating and

analyzing the cost and financial information of an entity for the purpose of preparing accurate

internal financial reports, statistical information which is needed by the business managers for

exercising their day to day functions. Tools and techniques of management accounting also

facilitates the managers with the required information regarding log term decisions such as

acquisition of capital assets, undertaking of a particular project etc. This is done by assessing

their feasibility and profitability. Such decisions are taken with the help of financial

modeling,capital budgeting etc. (Mouritsen and Kreiner, 2016).

Difference between financial and managerial accounting :

Basis Management accounting Financial accounting

focus managerial accounting’s aim to

provide the managers with needed

financial and cost related

financial accounting focuses on

preparing the financial reports for

all the interested parties or

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information that assists the in their

decision making process, strategy

and policy formulation, etc.

stakeholders of the business

Statutory requirement managerial accounting is practised

for the sake of assisting the

managers with meaningful

information to make qualify

decisions for the organization.

financial accounting is required by

the law and is mandatory

Different types of management accounting systems are as follows:

Cost accounting system:

It is referred to as a procedure of systematically recording, classifying, evaluating and

analyzing the costs. This system is applied by the business organization for anticipating the costs

of their products or services for the purpose of identifying the profitability, cost control, cost

reduction and inventory valuation. ABC Ltd applies this system of management accounting

within its operations for a motive of determining the costs and profitability of the products

manufactured by the company. This also helps them in exercising controlling function through

which cost-effectiveness is achieved.

Requirement and Benefits :

It is required in the business because it allows the managers in measuring and assessing the

cost efficiency within the operations. It further allows the management of ABC Ltd in

identifying the profitable and non profitable operations (Machado, 2016).

Price Optimization system :

Price optimization refers to a system employed by business organization for identifying the

retail value of the company’s products or services. In other words, it is a procedure of

determining the balance between profit and product’s value. The manager of business

organization evaluate and analyse different possible prices of the goods which consumer is

happy to pay. It also analyse and assess the lowest price which the business entity requires to fix

for preventing any possibility of losses(Borker, 2016).

Requirement and Benefits :

4

decision making process, strategy

and policy formulation, etc.

stakeholders of the business

Statutory requirement managerial accounting is practised

for the sake of assisting the

managers with meaningful

information to make qualify

decisions for the organization.

financial accounting is required by

the law and is mandatory

Different types of management accounting systems are as follows:

Cost accounting system:

It is referred to as a procedure of systematically recording, classifying, evaluating and

analyzing the costs. This system is applied by the business organization for anticipating the costs

of their products or services for the purpose of identifying the profitability, cost control, cost

reduction and inventory valuation. ABC Ltd applies this system of management accounting

within its operations for a motive of determining the costs and profitability of the products

manufactured by the company. This also helps them in exercising controlling function through

which cost-effectiveness is achieved.

Requirement and Benefits :

It is required in the business because it allows the managers in measuring and assessing the

cost efficiency within the operations. It further allows the management of ABC Ltd in

identifying the profitable and non profitable operations (Machado, 2016).

Price Optimization system :

Price optimization refers to a system employed by business organization for identifying the

retail value of the company’s products or services. In other words, it is a procedure of

determining the balance between profit and product’s value. The manager of business

organization evaluate and analyse different possible prices of the goods which consumer is

happy to pay. It also analyse and assess the lowest price which the business entity requires to fix

for preventing any possibility of losses(Borker, 2016).

Requirement and Benefits :

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization leads to better quality decisions that helps in improving the efficiency of

overall company. It allows management to set an optimum price which helps it in attracting the

attention of consumers. Further, it significantly helps the business in standing peacefully and

Strong the ultra competitive market.

Inventory management system:

It is a system of managing the non capital asset of the business organization which are stock

or inventory. It is basically a procedure of keeping and maintaining the sufficient levels of

inventory within the business so that flow in the production process does not get disturbed

(inventory management, 2019). There are different ways through which a company manages its

inventory such as:

LIFO: It is last in first out method in which recently purchased goods are removed first

from the inventory and is matched with income generated through sales which is reported on

the income statement.

Just in time purchase: This is one of the method of managing the inventory in which

organization purchase goods only when they are to be delivered to the customers for meeting

their demands. Economic reorder quantity: It is defined as such quantity that minimizes the carrying and

holding costs of materials in total. It is recognized as one of the best classical model of

scheduling production.

Requirement and Benefits :

This system is required within the business because it helps in optimally managing the

inventory which in turn reduces the unnecessary costs of handling and carrying excessive

inventory which is not required by the company. Further, it also keeps a balance between

production demand and stock of raw material that helps the business in avoiding excess

requirement of working capital. This significantly reduces the operation costs of the business

which eventually lead to higher profitability for the organization.

Job costing system:

It is such system in which costs of each product is assigned and allocated individually. Job

costing system acts as a supervising technique that assists the managers in keeping the track of

company’s expenses. ABC Ltd apply this job costing in its business through which it determines

the profitability and viability of a particular product of the company.

5

overall company. It allows management to set an optimum price which helps it in attracting the

attention of consumers. Further, it significantly helps the business in standing peacefully and

Strong the ultra competitive market.

Inventory management system:

It is a system of managing the non capital asset of the business organization which are stock

or inventory. It is basically a procedure of keeping and maintaining the sufficient levels of

inventory within the business so that flow in the production process does not get disturbed

(inventory management, 2019). There are different ways through which a company manages its

inventory such as:

LIFO: It is last in first out method in which recently purchased goods are removed first

from the inventory and is matched with income generated through sales which is reported on

the income statement.

Just in time purchase: This is one of the method of managing the inventory in which

organization purchase goods only when they are to be delivered to the customers for meeting

their demands. Economic reorder quantity: It is defined as such quantity that minimizes the carrying and

holding costs of materials in total. It is recognized as one of the best classical model of

scheduling production.

Requirement and Benefits :

This system is required within the business because it helps in optimally managing the

inventory which in turn reduces the unnecessary costs of handling and carrying excessive

inventory which is not required by the company. Further, it also keeps a balance between

production demand and stock of raw material that helps the business in avoiding excess

requirement of working capital. This significantly reduces the operation costs of the business

which eventually lead to higher profitability for the organization.

Job costing system:

It is such system in which costs of each product is assigned and allocated individually. Job

costing system acts as a supervising technique that assists the managers in keeping the track of

company’s expenses. ABC Ltd apply this job costing in its business through which it determines

the profitability and viability of a particular product of the company.

5

Requirement and Benefits :

The major benefit of this accounting system is that it enables the management in

ascertaining the profitability of each order, job or product of the manufacturing unit. This in turn

facilitates the management with the crucial information that whether a particular product should

continue or it should be closed down.

P2 various method used by the organization for preparation of management accounting report

Managemnt accounting report prepare record the data for the internal user like managers,

employees and owner to produce the information for the external users such as creditors,

customer etc. Management accounting use the data from the financial accounting to measure and

control the performance of the company and provide the effective result through the efficient

decision-making process. The various method are used by the organization for reporting such as :

Budget : It is prepared to estimate the cost of the product and determine the various

activities in the production and manufacturing process. It controls the activity and cost of the

company by estimating the cost of various resource used by the organization during the

manufacturing and distributing process. Budget help the ABC company to prepare the

management accounting report. By comparing the standard budget to the actual cost ABC

company can easily manage the performance by finding the variances and manage them by

controlling the cost (Le Quéré, and et.al., 2015).

Performance report : It is prepared by the company to measure the performance of the

organization and its employees. To manage the performance of the company they also prepare

the report as department wise. It helps them to get the performance of individual department and

their impact on the whole organization. ABC company prepare the management accounting

report to evaluate the performance of each employee and department by comparing it to previous

year performance which increases the efficiency of the company (Management accounting

report, 2017). They also use the various tools in evaluating the performance such as key

performance indicators, budgetary control etc.

Inventory and manufacturing report : It is used to manage the inventory level in the

organization and make the efficient manufacturing report. It includes the various items such as

inventory wastes, overhead cost per hour or labour cost on hourly basis. ABC company use the

inventory and manufacturing report by comparing it with different assembly lines and found the

area of improvement to gain the higher profit. By managing the inventory level in the

6

The major benefit of this accounting system is that it enables the management in

ascertaining the profitability of each order, job or product of the manufacturing unit. This in turn

facilitates the management with the crucial information that whether a particular product should

continue or it should be closed down.

P2 various method used by the organization for preparation of management accounting report

Managemnt accounting report prepare record the data for the internal user like managers,

employees and owner to produce the information for the external users such as creditors,

customer etc. Management accounting use the data from the financial accounting to measure and

control the performance of the company and provide the effective result through the efficient

decision-making process. The various method are used by the organization for reporting such as :

Budget : It is prepared to estimate the cost of the product and determine the various

activities in the production and manufacturing process. It controls the activity and cost of the

company by estimating the cost of various resource used by the organization during the

manufacturing and distributing process. Budget help the ABC company to prepare the

management accounting report. By comparing the standard budget to the actual cost ABC

company can easily manage the performance by finding the variances and manage them by

controlling the cost (Le Quéré, and et.al., 2015).

Performance report : It is prepared by the company to measure the performance of the

organization and its employees. To manage the performance of the company they also prepare

the report as department wise. It helps them to get the performance of individual department and

their impact on the whole organization. ABC company prepare the management accounting

report to evaluate the performance of each employee and department by comparing it to previous

year performance which increases the efficiency of the company (Management accounting

report, 2017). They also use the various tools in evaluating the performance such as key

performance indicators, budgetary control etc.

Inventory and manufacturing report : It is used to manage the inventory level in the

organization and make the efficient manufacturing report. It includes the various items such as

inventory wastes, overhead cost per hour or labour cost on hourly basis. ABC company use the

inventory and manufacturing report by comparing it with different assembly lines and found the

area of improvement to gain the higher profit. By managing the inventory level in the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization ABC manufacturing company can easily fulfil the demand of the customer and

order the quantity when they required.

Job cost report : It helps the company to focus on the specific project rather than to

invest time and money on different job which are less important for the company. It helps ABC

company to identify the area which provide higher earning and manage the tome and cost of the

firm. It also helps ABC company to analyse the expenses of the activities when project is

running, so they can manage the time and cost to address this problem and expenses after the

wastage become out of control.

Integration of management accounting system and management accounting report

Management accounting report and MA system is used by the ABC limited company to

formulate the policy, plan and strategy to evaluate the performance of the company via using

different reports such as budget report, inventory and manufacturing report etc. MA system help

the organization to manage the inventory level by providing different software to record the

inventory level and order quantity in the organization. It also helps them to reduce the inventory

maintenance cosy and improve the efficiency of the product and organization.

LO 2

P 3 Calculation of Net Profit or Loss under Marginal Costing and Absorption Costing for ABC

Ltd.

1. Production cost is the cost which is occurred at the time of converting raw material into

finished goods. These costs are generally direct costs for the company. Various types of

Production cost are real cost, opportunity cost, money costs etc.

The Production Cost per unit occurred in the company at the time of production

goods by ABC Ltd is -£ 46.67 per unit

The total production cost incurred by ABC Ltd at the time of production of goods is

£886730

The total cost of sales occurred in the month of January by ABC Ltd is £1026740.

2. Application of appropriate Budgeted Profit or Loss statement for January

Particulars

Budgeted Cost at 19000

unit

Budgeted Profit or Loss

for 19000 units

Material 19000 19000

7

order the quantity when they required.

Job cost report : It helps the company to focus on the specific project rather than to

invest time and money on different job which are less important for the company. It helps ABC

company to identify the area which provide higher earning and manage the tome and cost of the

firm. It also helps ABC company to analyse the expenses of the activities when project is

running, so they can manage the time and cost to address this problem and expenses after the

wastage become out of control.

Integration of management accounting system and management accounting report

Management accounting report and MA system is used by the ABC limited company to

formulate the policy, plan and strategy to evaluate the performance of the company via using

different reports such as budget report, inventory and manufacturing report etc. MA system help

the organization to manage the inventory level by providing different software to record the

inventory level and order quantity in the organization. It also helps them to reduce the inventory

maintenance cosy and improve the efficiency of the product and organization.

LO 2

P 3 Calculation of Net Profit or Loss under Marginal Costing and Absorption Costing for ABC

Ltd.

1. Production cost is the cost which is occurred at the time of converting raw material into

finished goods. These costs are generally direct costs for the company. Various types of

Production cost are real cost, opportunity cost, money costs etc.

The Production Cost per unit occurred in the company at the time of production

goods by ABC Ltd is -£ 46.67 per unit

The total production cost incurred by ABC Ltd at the time of production of goods is

£886730

The total cost of sales occurred in the month of January by ABC Ltd is £1026740.

2. Application of appropriate Budgeted Profit or Loss statement for January

Particulars

Budgeted Cost at 19000

unit

Budgeted Profit or Loss

for 19000 units

Material 19000 19000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

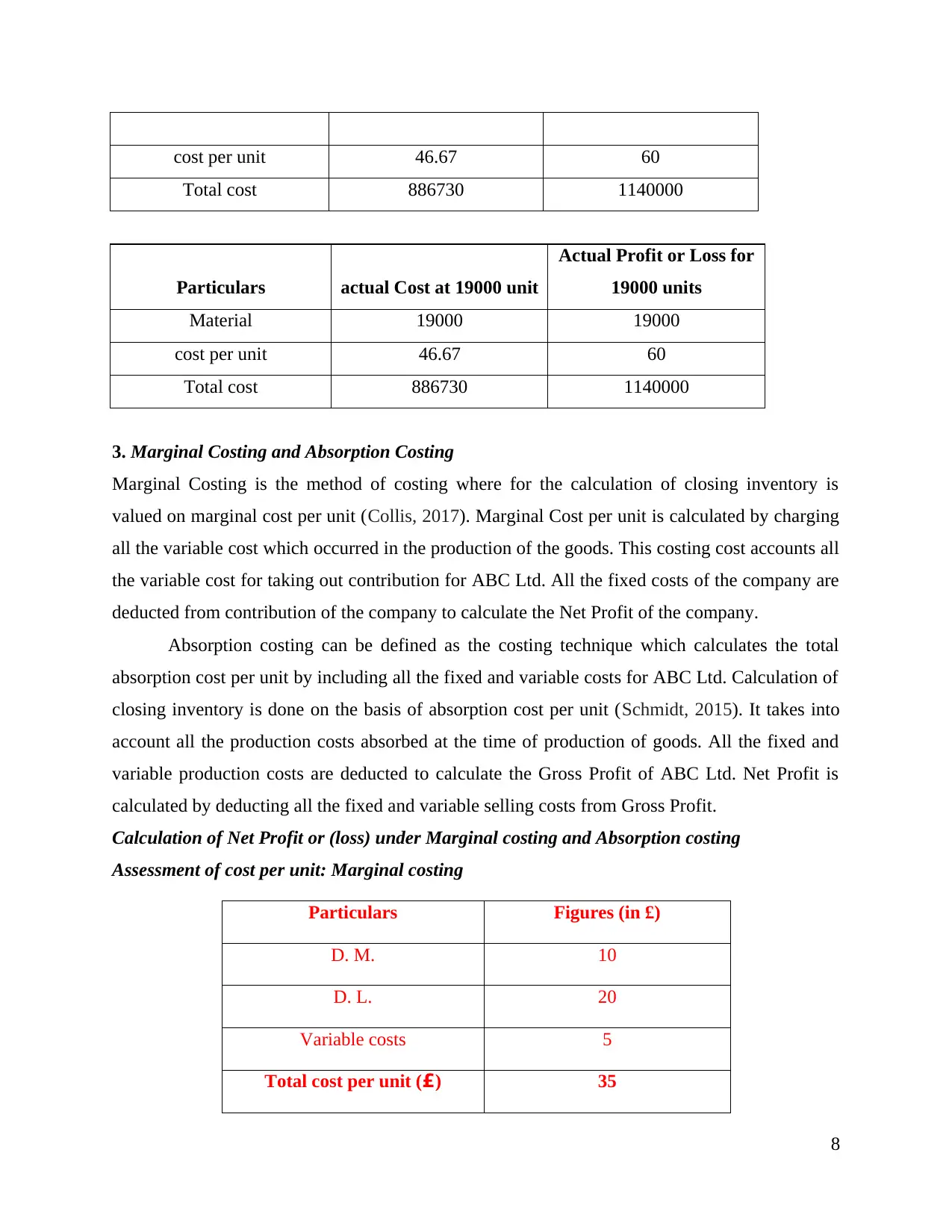

cost per unit 46.67 60

Total cost 886730 1140000

Particulars actual Cost at 19000 unit

Actual Profit or Loss for

19000 units

Material 19000 19000

cost per unit 46.67 60

Total cost 886730 1140000

3. Marginal Costing and Absorption Costing

Marginal Costing is the method of costing where for the calculation of closing inventory is

valued on marginal cost per unit (Collis, 2017). Marginal Cost per unit is calculated by charging

all the variable cost which occurred in the production of the goods. This costing cost accounts all

the variable cost for taking out contribution for ABC Ltd. All the fixed costs of the company are

deducted from contribution of the company to calculate the Net Profit of the company.

Absorption costing can be defined as the costing technique which calculates the total

absorption cost per unit by including all the fixed and variable costs for ABC Ltd. Calculation of

closing inventory is done on the basis of absorption cost per unit (Schmidt, 2015). It takes into

account all the production costs absorbed at the time of production of goods. All the fixed and

variable production costs are deducted to calculate the Gross Profit of ABC Ltd. Net Profit is

calculated by deducting all the fixed and variable selling costs from Gross Profit.

Calculation of Net Profit or (loss) under Marginal costing and Absorption costing

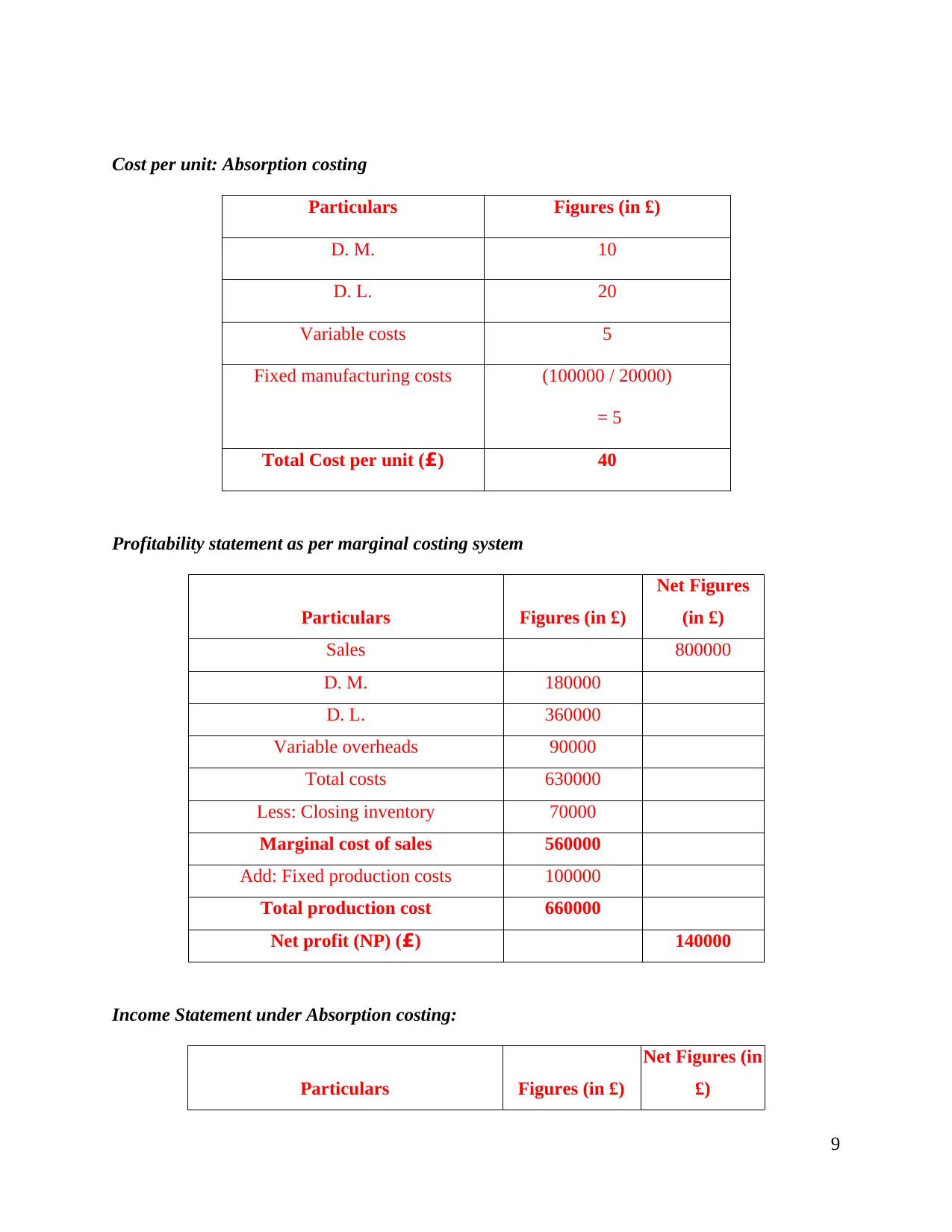

Assessment of cost per unit: Marginal costing

Particulars Figures (in £)

D. M. 10

D. L. 20

Variable costs 5

Total cost per unit (£) 35

8

Total cost 886730 1140000

Particulars actual Cost at 19000 unit

Actual Profit or Loss for

19000 units

Material 19000 19000

cost per unit 46.67 60

Total cost 886730 1140000

3. Marginal Costing and Absorption Costing

Marginal Costing is the method of costing where for the calculation of closing inventory is

valued on marginal cost per unit (Collis, 2017). Marginal Cost per unit is calculated by charging

all the variable cost which occurred in the production of the goods. This costing cost accounts all

the variable cost for taking out contribution for ABC Ltd. All the fixed costs of the company are

deducted from contribution of the company to calculate the Net Profit of the company.

Absorption costing can be defined as the costing technique which calculates the total

absorption cost per unit by including all the fixed and variable costs for ABC Ltd. Calculation of

closing inventory is done on the basis of absorption cost per unit (Schmidt, 2015). It takes into

account all the production costs absorbed at the time of production of goods. All the fixed and

variable production costs are deducted to calculate the Gross Profit of ABC Ltd. Net Profit is

calculated by deducting all the fixed and variable selling costs from Gross Profit.

Calculation of Net Profit or (loss) under Marginal costing and Absorption costing

Assessment of cost per unit: Marginal costing

Particulars Figures (in £)

D. M. 10

D. L. 20

Variable costs 5

Total cost per unit (£) 35

8

Cost per unit: Absorption costing

Particulars Figures (in £)

D. M. 10

D. L. 20

Variable costs 5

Fixed manufacturing costs (100000 / 20000)

= 5

Total Cost per unit (£) 40

Profitability statement as per marginal costing system

Particulars Figures (in £)

Net Figures

(in £)

Sales 800000

D. M. 180000

D. L. 360000

Variable overheads 90000

Total costs 630000

Less: Closing inventory 70000

Marginal cost of sales 560000

Add: Fixed production costs 100000

Total production cost 660000

Net profit (NP) (£) 140000

Income Statement under Absorption costing:

Particulars Figures (in £)

Net Figures (in

£)

9

Particulars Figures (in £)

D. M. 10

D. L. 20

Variable costs 5

Fixed manufacturing costs (100000 / 20000)

= 5

Total Cost per unit (£) 40

Profitability statement as per marginal costing system

Particulars Figures (in £)

Net Figures

(in £)

Sales 800000

D. M. 180000

D. L. 360000

Variable overheads 90000

Total costs 630000

Less: Closing inventory 70000

Marginal cost of sales 560000

Add: Fixed production costs 100000

Total production cost 660000

Net profit (NP) (£) 140000

Income Statement under Absorption costing:

Particulars Figures (in £)

Net Figures (in

£)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

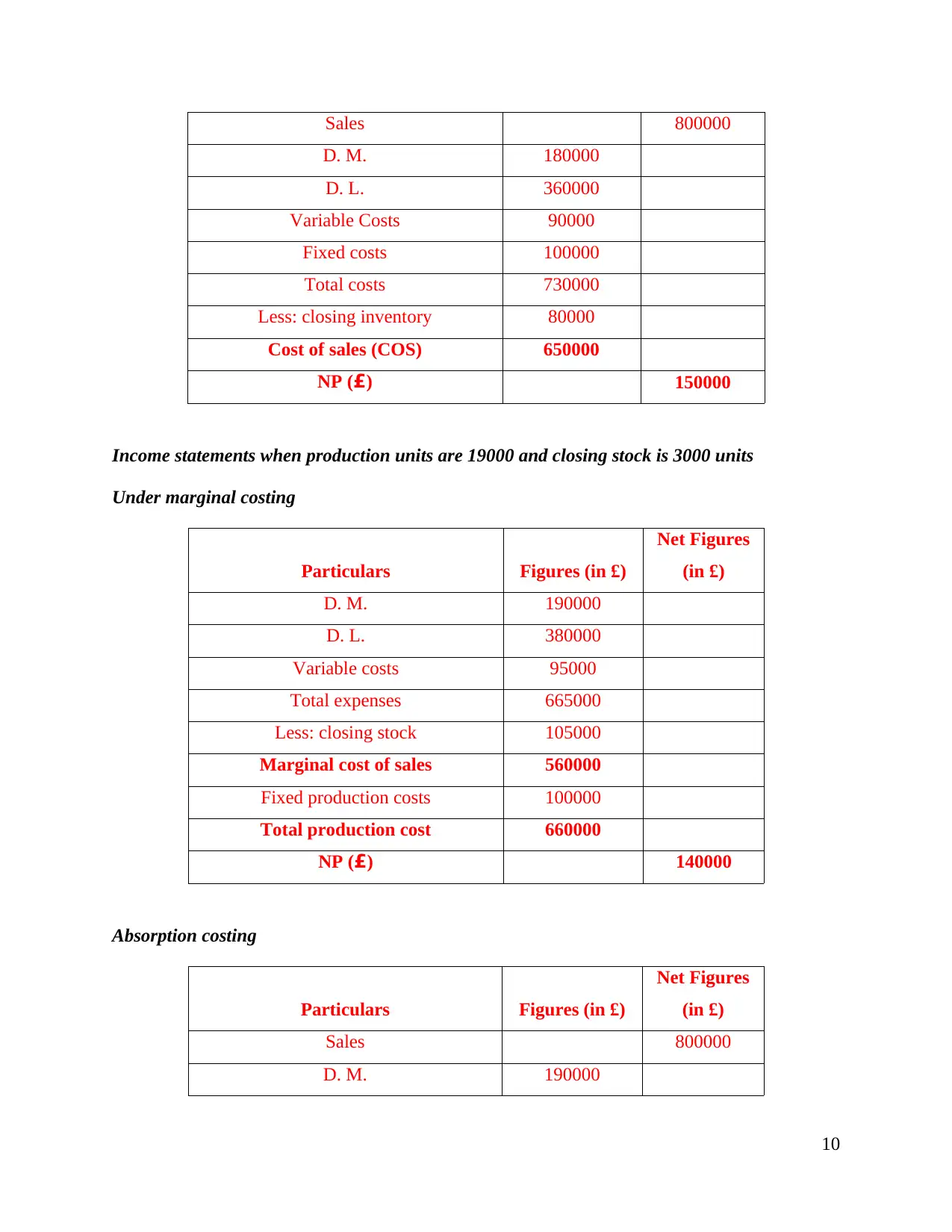

Sales 800000

D. M. 180000

D. L. 360000

Variable Costs 90000

Fixed costs 100000

Total costs 730000

Less: closing inventory 80000

Cost of sales (COS) 650000

NP (£) 150000

Income statements when production units are 19000 and closing stock is 3000 units

Under marginal costing

Particulars Figures (in £)

Net Figures

(in £)

D. M. 190000

D. L. 380000

Variable costs 95000

Total expenses 665000

Less: closing stock 105000

Marginal cost of sales 560000

Fixed production costs 100000

Total production cost 660000

NP (£) 140000

Absorption costing

Particulars Figures (in £)

Net Figures

(in £)

Sales 800000

D. M. 190000

10

D. M. 180000

D. L. 360000

Variable Costs 90000

Fixed costs 100000

Total costs 730000

Less: closing inventory 80000

Cost of sales (COS) 650000

NP (£) 150000

Income statements when production units are 19000 and closing stock is 3000 units

Under marginal costing

Particulars Figures (in £)

Net Figures

(in £)

D. M. 190000

D. L. 380000

Variable costs 95000

Total expenses 665000

Less: closing stock 105000

Marginal cost of sales 560000

Fixed production costs 100000

Total production cost 660000

NP (£) 140000

Absorption costing

Particulars Figures (in £)

Net Figures

(in £)

Sales 800000

D. M. 190000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

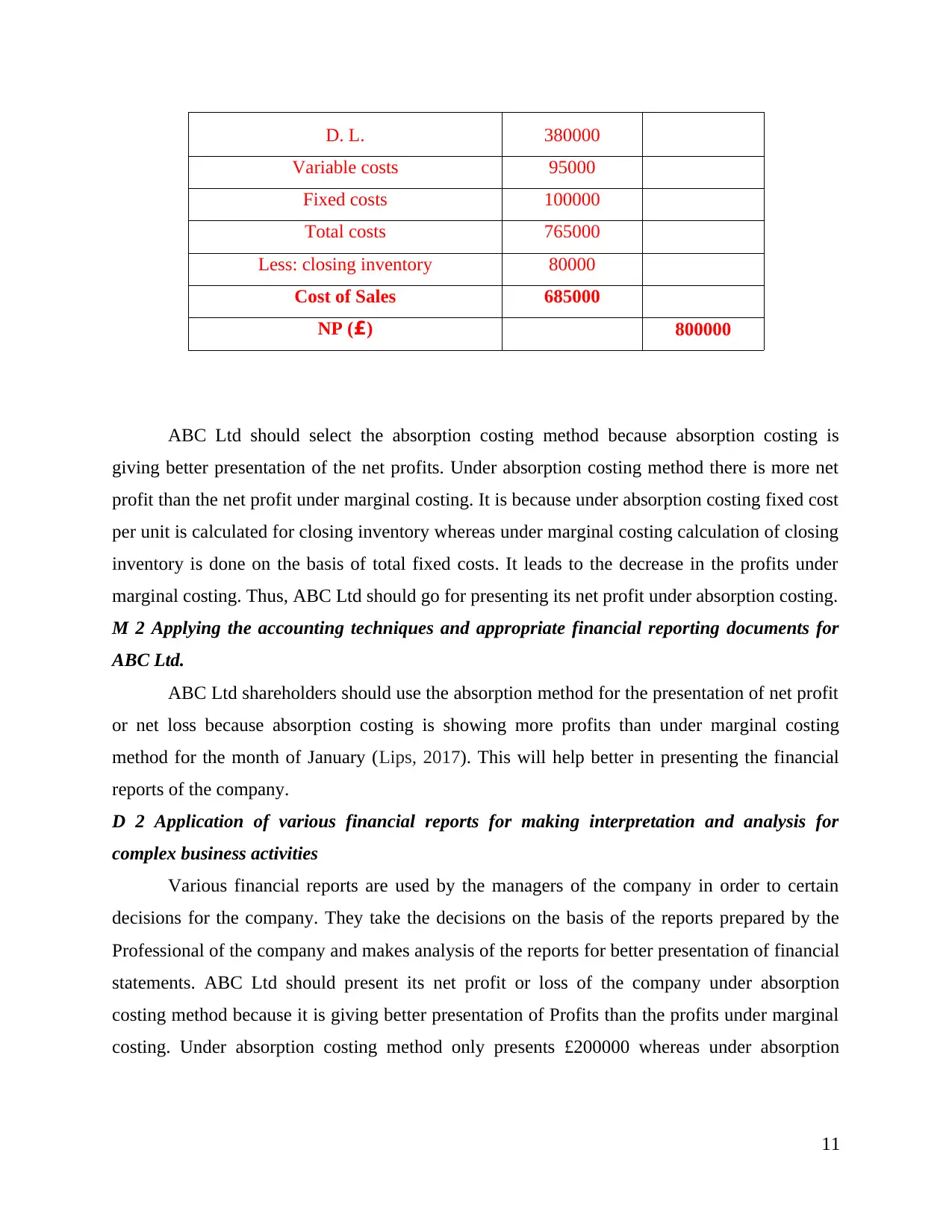

D. L. 380000

Variable costs 95000

Fixed costs 100000

Total costs 765000

Less: closing inventory 80000

Cost of Sales 685000

NP (£) 800000

ABC Ltd should select the absorption costing method because absorption costing is

giving better presentation of the net profits. Under absorption costing method there is more net

profit than the net profit under marginal costing. It is because under absorption costing fixed cost

per unit is calculated for closing inventory whereas under marginal costing calculation of closing

inventory is done on the basis of total fixed costs. It leads to the decrease in the profits under

marginal costing. Thus, ABC Ltd should go for presenting its net profit under absorption costing.

M 2 Applying the accounting techniques and appropriate financial reporting documents for

ABC Ltd.

ABC Ltd shareholders should use the absorption method for the presentation of net profit

or net loss because absorption costing is showing more profits than under marginal costing

method for the month of January (Lips, 2017). This will help better in presenting the financial

reports of the company.

D 2 Application of various financial reports for making interpretation and analysis for

complex business activities

Various financial reports are used by the managers of the company in order to certain

decisions for the company. They take the decisions on the basis of the reports prepared by the

Professional of the company and makes analysis of the reports for better presentation of financial

statements. ABC Ltd should present its net profit or loss of the company under absorption

costing method because it is giving better presentation of Profits than the profits under marginal

costing. Under absorption costing method only presents £200000 whereas under absorption

11

Variable costs 95000

Fixed costs 100000

Total costs 765000

Less: closing inventory 80000

Cost of Sales 685000

NP (£) 800000

ABC Ltd should select the absorption costing method because absorption costing is

giving better presentation of the net profits. Under absorption costing method there is more net

profit than the net profit under marginal costing. It is because under absorption costing fixed cost

per unit is calculated for closing inventory whereas under marginal costing calculation of closing

inventory is done on the basis of total fixed costs. It leads to the decrease in the profits under

marginal costing. Thus, ABC Ltd should go for presenting its net profit under absorption costing.

M 2 Applying the accounting techniques and appropriate financial reporting documents for

ABC Ltd.

ABC Ltd shareholders should use the absorption method for the presentation of net profit

or net loss because absorption costing is showing more profits than under marginal costing

method for the month of January (Lips, 2017). This will help better in presenting the financial

reports of the company.

D 2 Application of various financial reports for making interpretation and analysis for

complex business activities

Various financial reports are used by the managers of the company in order to certain

decisions for the company. They take the decisions on the basis of the reports prepared by the

Professional of the company and makes analysis of the reports for better presentation of financial

statements. ABC Ltd should present its net profit or loss of the company under absorption

costing method because it is giving better presentation of Profits than the profits under marginal

costing. Under absorption costing method only presents £200000 whereas under absorption

11

costing it is showing £218000. So, company should go present its income statement under

absorption costing method.

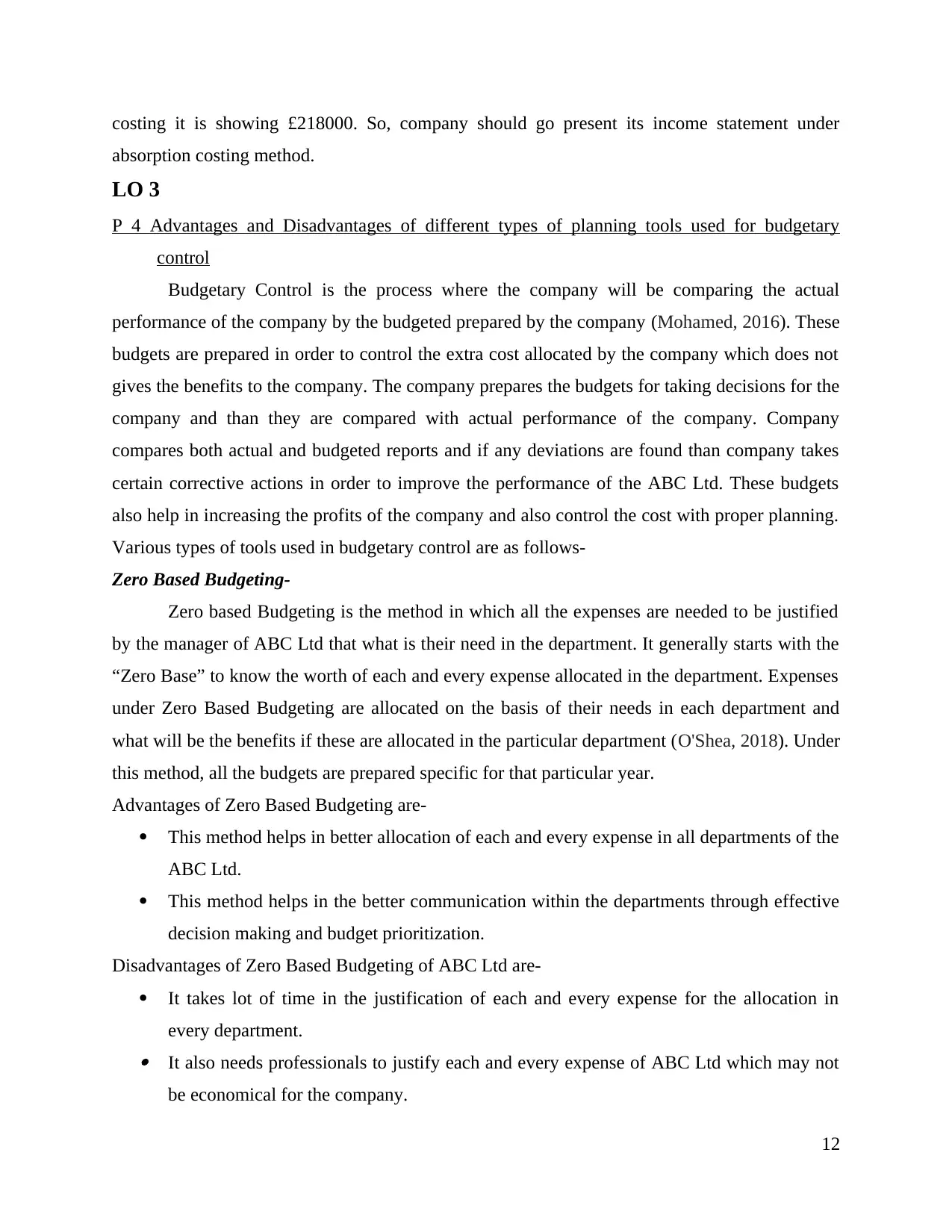

LO 3

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary

control

Budgetary Control is the process where the company will be comparing the actual

performance of the company by the budgeted prepared by the company (Mohamed, 2016). These

budgets are prepared in order to control the extra cost allocated by the company which does not

gives the benefits to the company. The company prepares the budgets for taking decisions for the

company and than they are compared with actual performance of the company. Company

compares both actual and budgeted reports and if any deviations are found than company takes

certain corrective actions in order to improve the performance of the ABC Ltd. These budgets

also help in increasing the profits of the company and also control the cost with proper planning.

Various types of tools used in budgetary control are as follows-

Zero Based Budgeting-

Zero based Budgeting is the method in which all the expenses are needed to be justified

by the manager of ABC Ltd that what is their need in the department. It generally starts with the

“Zero Base” to know the worth of each and every expense allocated in the department. Expenses

under Zero Based Budgeting are allocated on the basis of their needs in each department and

what will be the benefits if these are allocated in the particular department (O'Shea, 2018). Under

this method, all the budgets are prepared specific for that particular year.

Advantages of Zero Based Budgeting are-

This method helps in better allocation of each and every expense in all departments of the

ABC Ltd.

This method helps in the better communication within the departments through effective

decision making and budget prioritization.

Disadvantages of Zero Based Budgeting of ABC Ltd are-

It takes lot of time in the justification of each and every expense for the allocation in

every department. It also needs professionals to justify each and every expense of ABC Ltd which may not

be economical for the company.

12

absorption costing method.

LO 3

P 4 Advantages and Disadvantages of different types of planning tools used for budgetary

control

Budgetary Control is the process where the company will be comparing the actual

performance of the company by the budgeted prepared by the company (Mohamed, 2016). These

budgets are prepared in order to control the extra cost allocated by the company which does not

gives the benefits to the company. The company prepares the budgets for taking decisions for the

company and than they are compared with actual performance of the company. Company

compares both actual and budgeted reports and if any deviations are found than company takes

certain corrective actions in order to improve the performance of the ABC Ltd. These budgets

also help in increasing the profits of the company and also control the cost with proper planning.

Various types of tools used in budgetary control are as follows-

Zero Based Budgeting-

Zero based Budgeting is the method in which all the expenses are needed to be justified

by the manager of ABC Ltd that what is their need in the department. It generally starts with the

“Zero Base” to know the worth of each and every expense allocated in the department. Expenses

under Zero Based Budgeting are allocated on the basis of their needs in each department and

what will be the benefits if these are allocated in the particular department (O'Shea, 2018). Under

this method, all the budgets are prepared specific for that particular year.

Advantages of Zero Based Budgeting are-

This method helps in better allocation of each and every expense in all departments of the

ABC Ltd.

This method helps in the better communication within the departments through effective

decision making and budget prioritization.

Disadvantages of Zero Based Budgeting of ABC Ltd are-

It takes lot of time in the justification of each and every expense for the allocation in

every department. It also needs professionals to justify each and every expense of ABC Ltd which may not

be economical for the company.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.