Advanced Management Accounting Report: ABC Ltd Business Expansion

VerifiedAdded on 2021/02/21

|18

|5694

|176

Report

AI Summary

This report delves into the realm of advanced management accounting, focusing on the application of these principles within ABC Ltd, a company planning global expansion. The report begins by exploring the purpose and presentation of financial information for various stakeholders, emphasizing the significance of clear and transparent reporting. It then moves on to analyze the application of different accounting microeconomic techniques, such as cost analysis, cost-volume-profit analysis, and variance analysis, assessing their value and importance in decision-making. The concept of variance analysis is discussed in detail, including actual and standard costs, along with the advantages and disadvantages of different variance types. Finally, the report considers the impact of external and internal factors on the business environment, evaluating the impact of changes on ABC Ltd. The report uses examples and analysis to explain the practical implications of these accounting methods.

Advanced Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Purpose and presentation of financial information for various stakeholder. ...................1

M1. Need of presenting financial information.......................................................................3

D1. Evaluation of financial information.................................................................................3

TASK 2............................................................................................................................................4

P2. Use of different accounting microeconomic techniques..................................................4

M2. Value and importance of a wide range of accounting techniques.................................6

D2. Evaluate the application of different accounting techniques...........................................6

TASK 3............................................................................................................................................7

P3. Concept of variance analysis in its importance................................................................7

P4. Actual and standard costs to control and correct variances.............................................8

M3. Advantages and disadvantages of different types of variances....................................10

TASK 4..........................................................................................................................................10

P5. External and internal factors changing the business......................................................10

M4. Impact of different types of change..............................................................................12

D3. Critically evaluate the impact of changes.....................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Purpose and presentation of financial information for various stakeholder. ...................1

M1. Need of presenting financial information.......................................................................3

D1. Evaluation of financial information.................................................................................3

TASK 2............................................................................................................................................4

P2. Use of different accounting microeconomic techniques..................................................4

M2. Value and importance of a wide range of accounting techniques.................................6

D2. Evaluate the application of different accounting techniques...........................................6

TASK 3............................................................................................................................................7

P3. Concept of variance analysis in its importance................................................................7

P4. Actual and standard costs to control and correct variances.............................................8

M3. Advantages and disadvantages of different types of variances....................................10

TASK 4..........................................................................................................................................10

P5. External and internal factors changing the business......................................................10

M4. Impact of different types of change..............................................................................12

D3. Critically evaluate the impact of changes.....................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

In today's era every organization wants to decrease costs while preserving product quality

in the current competitive situation, but for organisation it is very hard in the practical term to

attain the desired results (Andriof and Waddock, 2017). Advance management accounting is

indeed a fundamental reporting specialist element that fits with the company's management

structure so that formulating of valuable strategic and policies can be prepared as it’s easy to

make any future decision. It helps company to make effective procedures and potential decision-

making requirements by accounting of information more vibrantly as well as sincerely. In order

to better understand the concept of advance management accounting ABC Ltd has been selected

that is planning to expand its business in different part of world thus its manager requires deep

knowledge about management accounting systems, processes, principles, fundamental tools and

techniques.

In this report, purpose and presentation of financial information, use of different

accounting techniques, concept of variance analysis and its importance to control budget, actual

and standard costs to control and correct variances are discussed. In addition, external and

internal factors changing the business environment impact are being defined in this project

report.

TASK 1

P1. Purpose and presentation of financial information for various stakeholder.

Financial information are the company's financial statements such as profit and loss,

balance sheets and cash flow that aid management and shareholder to make different decisions

according to their requirement (Bhimani, 2019). This information is extremely seen as a

constitutional necessity by the legislative body of the corresponding company that need to

comply with reporting norms. There are number of stakeholder that have interest within the

business of ABC Ltd, some of these are defined below:

Internal stakeholder: The stakeholder those are part of internal management of ABC

Ltd and are the one to whom information is directly delivered. They have the right to get the

detail information so that fair and transparent statements which support in creating policies and

strategies to conduct the business and making sure that any uncertain activity must not be

1

In today's era every organization wants to decrease costs while preserving product quality

in the current competitive situation, but for organisation it is very hard in the practical term to

attain the desired results (Andriof and Waddock, 2017). Advance management accounting is

indeed a fundamental reporting specialist element that fits with the company's management

structure so that formulating of valuable strategic and policies can be prepared as it’s easy to

make any future decision. It helps company to make effective procedures and potential decision-

making requirements by accounting of information more vibrantly as well as sincerely. In order

to better understand the concept of advance management accounting ABC Ltd has been selected

that is planning to expand its business in different part of world thus its manager requires deep

knowledge about management accounting systems, processes, principles, fundamental tools and

techniques.

In this report, purpose and presentation of financial information, use of different

accounting techniques, concept of variance analysis and its importance to control budget, actual

and standard costs to control and correct variances are discussed. In addition, external and

internal factors changing the business environment impact are being defined in this project

report.

TASK 1

P1. Purpose and presentation of financial information for various stakeholder.

Financial information are the company's financial statements such as profit and loss,

balance sheets and cash flow that aid management and shareholder to make different decisions

according to their requirement (Bhimani, 2019). This information is extremely seen as a

constitutional necessity by the legislative body of the corresponding company that need to

comply with reporting norms. There are number of stakeholder that have interest within the

business of ABC Ltd, some of these are defined below:

Internal stakeholder: The stakeholder those are part of internal management of ABC

Ltd and are the one to whom information is directly delivered. They have the right to get the

detail information so that fair and transparent statements which support in creating policies and

strategies to conduct the business and making sure that any uncertain activity must not be

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

included that may lead to wrong interpretation of crucial statements. Some of these are discussed

below:

Employees: They seem to be the most significant business component, because they are

the elements that assist a business to grow significantly. The aim of financial information for

employees is to guarantee that the entities have a good continued financial health because

company's health is linked directly to its employee and mutual compensation, bonuses, job

security, development and learning interests. For example, income statements give detail

information about salary deduction, fringe and other additional benefits so that they can ensure

about their future growth in respective firm.

Manager: These are the people who are able to manage and control all tasks and

operation of a company. For them, financial data is really essential and they can schedule to

improve the company's financial output. Each and every document is important for manager as

they require detail information for making policies and strategies that will be beneficial for ABC

to expand their business and attain competitive advantage (Burns and Vaivio, 2011). They make

use of financial information in order to determine any weak areas of operation in ABC Ltd and

accomplish managerial task effectively.

External stakeholder: All outside individuals investing their cash, providing credit and

buying goods or services are regarded as external stakeholders. They are indirectly related with

the different internal decision of company. Financial information like paid-up capital, and

proposed capital, interest on debenture and return on investment are several important data

submitted throughout balance sheet to external stakeholders.

Investors: The investor requires financial data of the enterprise because it provides

money to the enterprise for the development of its activities and wants to earn a return, that can

be obtained when company is performing well in capital markets. With the support of financial

information, they ensure to have best earning on equity, bonus share, interest on debt capital.

Their aim in searching for economic information so that they can evaluate the company

investment opportunity. The financial report presents earnings per share, rate of growth and

patterns to expound quality data for lenders.

Creditors: Banks, financial organizations, investors and loan services from corporate that

provide loans and financing progress are some important creditors. The aim of creditors from

financial data is to determine that company performs well, ensuring both repayment ability and

2

below:

Employees: They seem to be the most significant business component, because they are

the elements that assist a business to grow significantly. The aim of financial information for

employees is to guarantee that the entities have a good continued financial health because

company's health is linked directly to its employee and mutual compensation, bonuses, job

security, development and learning interests. For example, income statements give detail

information about salary deduction, fringe and other additional benefits so that they can ensure

about their future growth in respective firm.

Manager: These are the people who are able to manage and control all tasks and

operation of a company. For them, financial data is really essential and they can schedule to

improve the company's financial output. Each and every document is important for manager as

they require detail information for making policies and strategies that will be beneficial for ABC

to expand their business and attain competitive advantage (Burns and Vaivio, 2011). They make

use of financial information in order to determine any weak areas of operation in ABC Ltd and

accomplish managerial task effectively.

External stakeholder: All outside individuals investing their cash, providing credit and

buying goods or services are regarded as external stakeholders. They are indirectly related with

the different internal decision of company. Financial information like paid-up capital, and

proposed capital, interest on debenture and return on investment are several important data

submitted throughout balance sheet to external stakeholders.

Investors: The investor requires financial data of the enterprise because it provides

money to the enterprise for the development of its activities and wants to earn a return, that can

be obtained when company is performing well in capital markets. With the support of financial

information, they ensure to have best earning on equity, bonus share, interest on debt capital.

Their aim in searching for economic information so that they can evaluate the company

investment opportunity. The financial report presents earnings per share, rate of growth and

patterns to expound quality data for lenders.

Creditors: Banks, financial organizations, investors and loan services from corporate that

provide loans and financing progress are some important creditors. The aim of creditors from

financial data is to determine that company performs well, ensuring both repayment ability and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest amount. Some of the crucial document that are presented to reliable creditors within

annual report of respective company can be credit policy, credit note and possible modification

in charges and rates.

Customer: All the individuals purchasing the organization's goods are regarded as clients

(Carraher and Van Auken, 2013). For them, financial statements are very essential as they can

analyse that either they are purchasing or not profitable business products with the assistance of

such information.

M1. Need of presenting financial information.

In companies, managers are needed to make meaningful decision on the basis of current trends

and last year data, thus they needed to record each and every business transaction within correct

financial statement. These statements give a good positive information collection that enables

analyse the company's profitability and liquidity situation and gain knowledge into how the

money invested has done over a number of years. There are basically three types of statements

that are prepared and presented for a specific purpose such as balance sheet, income statements

and cash flow. Some basic purpose is discussed below:

Act as a source of decision making: Financial statement reveals the liabilities, asset,

revenue and business loss information. It enables users of economic data such as creditors to

obtain data from financial statements and use it to create effective decisions that support them in

making future decision.

Assist potential investors: Usually, financial statements are developed according to

International Financial Reporting Standard thus it holds descriptive and authentic information.

Investors take use of the data obtained from specified business and afterwards decide whether to

invest or withdraw their equity portion from the particular business.

D1. Evaluation of financial information.

Financial information circulated through financial statements gives a brief overview of a

company's fiscal health. It helps administrators as a supporting component which help in the

development of financial planning and plan for the criterion of long term investment decision

making. These statements offer a broad variety of leadership opportunities to determine the

reasoning behind the imbalance and gaps in information that assist in the implementation of

strategies.

3

annual report of respective company can be credit policy, credit note and possible modification

in charges and rates.

Customer: All the individuals purchasing the organization's goods are regarded as clients

(Carraher and Van Auken, 2013). For them, financial statements are very essential as they can

analyse that either they are purchasing or not profitable business products with the assistance of

such information.

M1. Need of presenting financial information.

In companies, managers are needed to make meaningful decision on the basis of current trends

and last year data, thus they needed to record each and every business transaction within correct

financial statement. These statements give a good positive information collection that enables

analyse the company's profitability and liquidity situation and gain knowledge into how the

money invested has done over a number of years. There are basically three types of statements

that are prepared and presented for a specific purpose such as balance sheet, income statements

and cash flow. Some basic purpose is discussed below:

Act as a source of decision making: Financial statement reveals the liabilities, asset,

revenue and business loss information. It enables users of economic data such as creditors to

obtain data from financial statements and use it to create effective decisions that support them in

making future decision.

Assist potential investors: Usually, financial statements are developed according to

International Financial Reporting Standard thus it holds descriptive and authentic information.

Investors take use of the data obtained from specified business and afterwards decide whether to

invest or withdraw their equity portion from the particular business.

D1. Evaluation of financial information.

Financial information circulated through financial statements gives a brief overview of a

company's fiscal health. It helps administrators as a supporting component which help in the

development of financial planning and plan for the criterion of long term investment decision

making. These statements offer a broad variety of leadership opportunities to determine the

reasoning behind the imbalance and gaps in information that assist in the implementation of

strategies.

3

TASK 2

P2. Use of different accounting microeconomic techniques.

Microeconomics is an individual factor analysis that includes quantitative approach

which aid to determine the behaviour of people and their role on different macro economic

elements (Chenhall and Moers, 2015). Microeconomic methods perform a vital part in evaluating

the company's profit margin metrics in contemporary management accounting theory. Most

microeconomic instruments are addressed below:

Cost analysis: The connection among input costs and yield proportion is studied as cost

analysis. Cost managers of ABC Ltd are studying the interdependence between the input factor

expenses involved in the manufacturing and the comparative performance resulting from such

assessment.

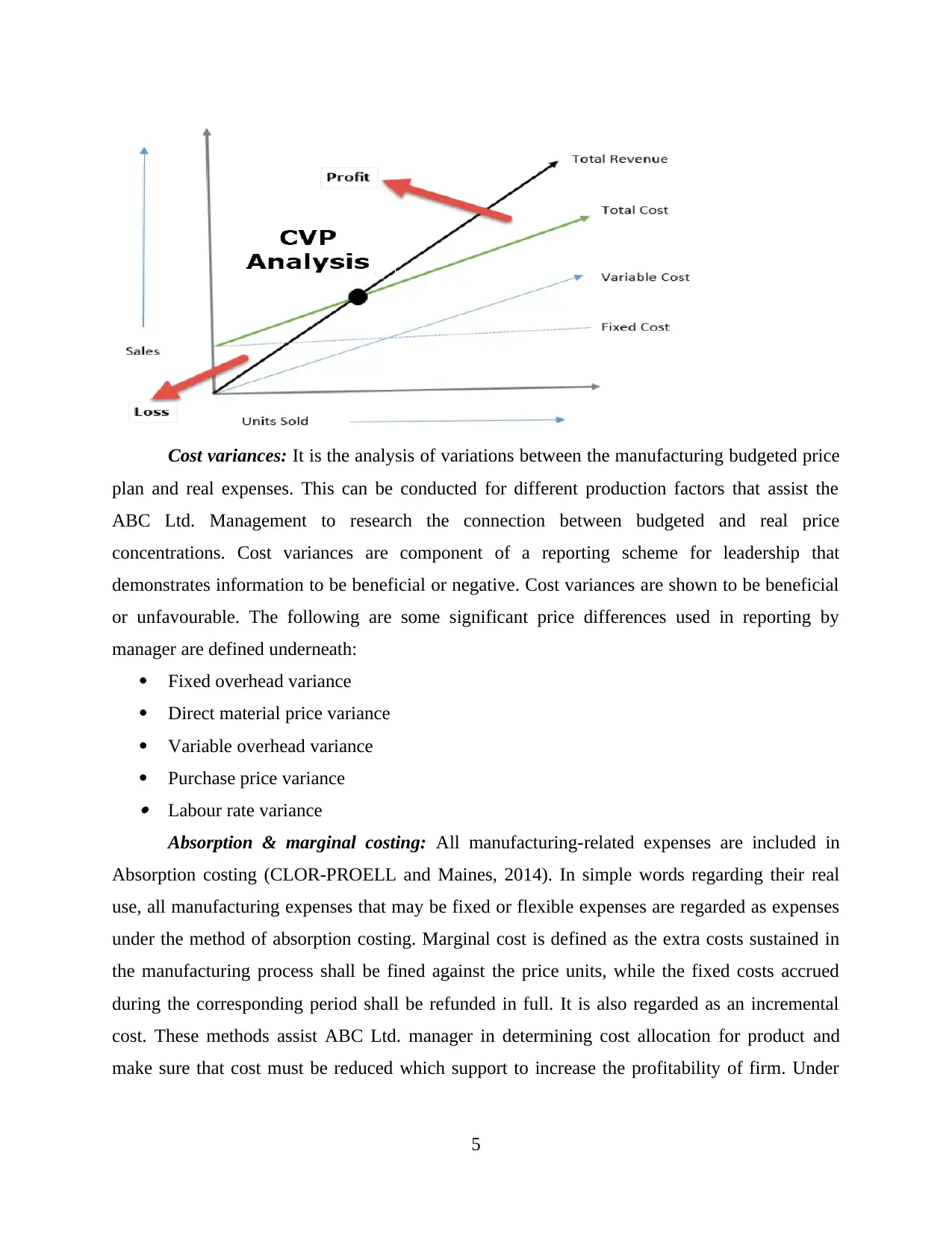

Cost-volume profit analysis: This methodology helps to determines the effect of

operating profit due to differences in cost-to-volume profit. This is often considered as a break-

even analysis that is used by ABC Ltd management so that income is equal to expenses and sales

would be equal to cost during a specific year. This analysis is related with sales price, fixed and

variable costs per unit are expected to be permanent and multiple comparisons are created using

graph for price, cost as well as other factors. This evaluation assists manager in finding the

highest annual sales volume to minimize losses and the volume of sales at which predefined

goals are accomplished. This also support in finding the most favourable and dependable

combination of cost and volume. Mangers in an organization utilizes CVP assessment to predict

and verify the impacts of its choices on fixed costs, marginal costs, quantity of revenues and

value revenues for its profit schemes (Chenhall, 2012).

4

P2. Use of different accounting microeconomic techniques.

Microeconomics is an individual factor analysis that includes quantitative approach

which aid to determine the behaviour of people and their role on different macro economic

elements (Chenhall and Moers, 2015). Microeconomic methods perform a vital part in evaluating

the company's profit margin metrics in contemporary management accounting theory. Most

microeconomic instruments are addressed below:

Cost analysis: The connection among input costs and yield proportion is studied as cost

analysis. Cost managers of ABC Ltd are studying the interdependence between the input factor

expenses involved in the manufacturing and the comparative performance resulting from such

assessment.

Cost-volume profit analysis: This methodology helps to determines the effect of

operating profit due to differences in cost-to-volume profit. This is often considered as a break-

even analysis that is used by ABC Ltd management so that income is equal to expenses and sales

would be equal to cost during a specific year. This analysis is related with sales price, fixed and

variable costs per unit are expected to be permanent and multiple comparisons are created using

graph for price, cost as well as other factors. This evaluation assists manager in finding the

highest annual sales volume to minimize losses and the volume of sales at which predefined

goals are accomplished. This also support in finding the most favourable and dependable

combination of cost and volume. Mangers in an organization utilizes CVP assessment to predict

and verify the impacts of its choices on fixed costs, marginal costs, quantity of revenues and

value revenues for its profit schemes (Chenhall, 2012).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost variances: It is the analysis of variations between the manufacturing budgeted price

plan and real expenses. This can be conducted for different production factors that assist the

ABC Ltd. Management to research the connection between budgeted and real price

concentrations. Cost variances are component of a reporting scheme for leadership that

demonstrates information to be beneficial or negative. Cost variances are shown to be beneficial

or unfavourable. The following are some significant price differences used in reporting by

manager are defined underneath:

Fixed overhead variance

Direct material price variance

Variable overhead variance

Purchase price variance Labour rate variance

Absorption & marginal costing: All manufacturing-related expenses are included in

Absorption costing (CLOR‐PROELL and Maines, 2014). In simple words regarding their real

use, all manufacturing expenses that may be fixed or flexible expenses are regarded as expenses

under the method of absorption costing. Marginal cost is defined as the extra costs sustained in

the manufacturing process shall be fined against the price units, while the fixed costs accrued

during the corresponding period shall be refunded in full. It is also regarded as an incremental

cost. These methods assist ABC Ltd. manager in determining cost allocation for product and

make sure that cost must be reduced which support to increase the profitability of firm. Under

5

plan and real expenses. This can be conducted for different production factors that assist the

ABC Ltd. Management to research the connection between budgeted and real price

concentrations. Cost variances are component of a reporting scheme for leadership that

demonstrates information to be beneficial or negative. Cost variances are shown to be beneficial

or unfavourable. The following are some significant price differences used in reporting by

manager are defined underneath:

Fixed overhead variance

Direct material price variance

Variable overhead variance

Purchase price variance Labour rate variance

Absorption & marginal costing: All manufacturing-related expenses are included in

Absorption costing (CLOR‐PROELL and Maines, 2014). In simple words regarding their real

use, all manufacturing expenses that may be fixed or flexible expenses are regarded as expenses

under the method of absorption costing. Marginal cost is defined as the extra costs sustained in

the manufacturing process shall be fined against the price units, while the fixed costs accrued

during the corresponding period shall be refunded in full. It is also regarded as an incremental

cost. These methods assist ABC Ltd. manager in determining cost allocation for product and

make sure that cost must be reduced which support to increase the profitability of firm. Under

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this method, the comparison of expenses becomes very important since fixed costs were not

taken forward for consecutive years as a compulsory norm.

M2. Value and importance of a wide range of accounting techniques.

All microeconomic techniques are important to a major within ABC Ltd as it support in

determining the different crucial aspect of business and it includes each and every segment of

these activities. Advantage and disadvantage are discussed below:

Marginal costing:

Advantages

This valuation technique is really simple for ABC Ltd managers to understand and use as

it removes the component of fixed expenses and their distribution. This costing method is helpful in assessing and appreciating the impact of additional

sales or manufacturers process that support to make decision regarding more production

resulting into more return to company.

Disadvantages

Developing this technique sometimes becomes irrelevant since fixed costs are the

component of goods and manufacturing anyway, thus their removal does not describe the

degree of variation.

This method sometime becomes complex in the term of separation of fixed and variable

cost due to which the results are inaccurate. The major drawback of this method is that it results into under valuation of inventories

because of exclusion of fixed cost from the existing value of inventories. In addition the

implementation of marginal costing while calculating net profit is not accepted for tax

intent.

Break even analysis

Advantages It offers a variety of technical variables that have impacted marketing variations that have

worsened earnings and potential alternatives to solve them.

Disadvantages

It implies that both manufacturing and revenues are constantly equivalent, which is

inefficient and a mistake in an extensive company framework (Cowell, 2018).

6

taken forward for consecutive years as a compulsory norm.

M2. Value and importance of a wide range of accounting techniques.

All microeconomic techniques are important to a major within ABC Ltd as it support in

determining the different crucial aspect of business and it includes each and every segment of

these activities. Advantage and disadvantage are discussed below:

Marginal costing:

Advantages

This valuation technique is really simple for ABC Ltd managers to understand and use as

it removes the component of fixed expenses and their distribution. This costing method is helpful in assessing and appreciating the impact of additional

sales or manufacturers process that support to make decision regarding more production

resulting into more return to company.

Disadvantages

Developing this technique sometimes becomes irrelevant since fixed costs are the

component of goods and manufacturing anyway, thus their removal does not describe the

degree of variation.

This method sometime becomes complex in the term of separation of fixed and variable

cost due to which the results are inaccurate. The major drawback of this method is that it results into under valuation of inventories

because of exclusion of fixed cost from the existing value of inventories. In addition the

implementation of marginal costing while calculating net profit is not accepted for tax

intent.

Break even analysis

Advantages It offers a variety of technical variables that have impacted marketing variations that have

worsened earnings and potential alternatives to solve them.

Disadvantages

It implies that both manufacturing and revenues are constantly equivalent, which is

inefficient and a mistake in an extensive company framework (Cowell, 2018).

6

This analysis mainly includes unrealistic assumptions such as goods are not sold on the

exact price at various production level, thus fixed cost do not change with the alteration

in output level.

In almost every large companies to get more profit more than one product are sold

therefore it is not easy to calculate break even.

D2. Evaluate the application of different accounting techniques.

Application of accounting practices in ABC Ltd. is really the consequence of huge

accounting and knowledge of leadership methods that have spread systematic order within the

organization. Methods such as Cost analysis, Cost-volume profit analysis and Absorption &

marginal costing internal that have been very important in helping manager of company with

practical business solutions to number of problems they faced within controlling business at

different country. Techniques and variances have assisted business people to predicted, create

plans and strategies and supervise development via ongoing vision, mission and plans evaluation

with the help of above-mentioned accounting techniques. It has been also evaluated that marginal

costing is not beneficial for company in some context, such as it only consist of closing stock

where variable cost is consider and all fixed cost are ignored which result into more twisted

image of total revenue to respective shareholder. Absorption costing have a major disadvantage

as it do not support in management decision making such as choosing of appropriate item

combination, whether to purchase or produce, to choose alternative options, minimum cost to

resolve the phase of depression. While Cost-volume profit analysis has some disadvantage to

ABC Ltd like it is hard to separate complete expenses into their fixed and variable parts by this

analysis and Other aspects such as inflation, effectiveness, ability and technology that may

influence expenses of company. Cost analysis is also not helpful many time such as, it require

more time and cost in order to implement authentic standard costing.

TASK 3

P3. Concept of variance analysis in its importance.

In accounting, the term variance is related with the difference among the real amount and

the budgeted or planned amount. Management always wants to have a proper record of each past

transaction of business so that they can easily analyse the record and make better plan in order to

reduce variance between the actual and estimated or planned amount. It is defined as the

7

exact price at various production level, thus fixed cost do not change with the alteration

in output level.

In almost every large companies to get more profit more than one product are sold

therefore it is not easy to calculate break even.

D2. Evaluate the application of different accounting techniques.

Application of accounting practices in ABC Ltd. is really the consequence of huge

accounting and knowledge of leadership methods that have spread systematic order within the

organization. Methods such as Cost analysis, Cost-volume profit analysis and Absorption &

marginal costing internal that have been very important in helping manager of company with

practical business solutions to number of problems they faced within controlling business at

different country. Techniques and variances have assisted business people to predicted, create

plans and strategies and supervise development via ongoing vision, mission and plans evaluation

with the help of above-mentioned accounting techniques. It has been also evaluated that marginal

costing is not beneficial for company in some context, such as it only consist of closing stock

where variable cost is consider and all fixed cost are ignored which result into more twisted

image of total revenue to respective shareholder. Absorption costing have a major disadvantage

as it do not support in management decision making such as choosing of appropriate item

combination, whether to purchase or produce, to choose alternative options, minimum cost to

resolve the phase of depression. While Cost-volume profit analysis has some disadvantage to

ABC Ltd like it is hard to separate complete expenses into their fixed and variable parts by this

analysis and Other aspects such as inflation, effectiveness, ability and technology that may

influence expenses of company. Cost analysis is also not helpful many time such as, it require

more time and cost in order to implement authentic standard costing.

TASK 3

P3. Concept of variance analysis in its importance.

In accounting, the term variance is related with the difference among the real amount and

the budgeted or planned amount. Management always wants to have a proper record of each past

transaction of business so that they can easily analyse the record and make better plan in order to

reduce variance between the actual and estimated or planned amount. It is defined as the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quantitative investigation which help manager of different department to figure out the difference

among the estimated and actual behaviour in budgeting and management accounting. This

analysis is mainly concerned with the gap in real and scheduled practices as it shows company

performance is affected. In simple words, administrators look at the real cost and sales statistics

after a specific period is over and make comparisons with what has been budgeted for that

period. For instance, in ABC Ltd if manager have a sales budget around $10,000 and actual sales

figures were $8,000 in that period, thus the variance analysis yields a difference of $2,000.

There are two steps relevant to variance analysis these are:

Calculation and recording of individual variances (Cravens and Piercy, 2016).

Understanding the reason of to each one variance.

Some of the major reason for arising variance are as follows:

Shift in market circumstances that have made conventional budgeting methods

unreasonable, e.g. shortage of raw materials leading to higher prices for sellers. Supported budgeting norms could be too idealistic in origin, e.g. machine production may

be wrongly thought.

Importance of variance analysis for controlling budget

It has been observed that Evaluation of variance allows budgeters gain an even more

practical picture to make the budget for all the coming year more reliable. As it supports

effective budgeting because management wants to reduced differences from the scheduled

budgets. to make descriptive and advance looking budgetary decisions. Evaluation of fluctuation

behaves as a method of control. Analysis of big differentiation on important products enables the

business to understand the effects and motivates the management explore possible methods to

avoid such deviation. It aid in managing annual budgets by reviewing the estimated budgets and

comparing the same with real income. For instance, the month-end report of ABC Ltd will only

provide statistical data on income and expenditures or levels of inventory. However, the

assessment of variance will assist to recognize the explanations behind the differences between

scheduled and real revenue that could lead to changes in corporate strategy and end goals.

P4. Actual and standard costs to control and correct variances.

Standard costing seems to be the setting of price norms and their regular evaluation of

operations to ascertain the causes for every variance of company during a specific period. It is

essentially used to evaluate the price of direct material, direct labour and overhead costs that are

8

among the estimated and actual behaviour in budgeting and management accounting. This

analysis is mainly concerned with the gap in real and scheduled practices as it shows company

performance is affected. In simple words, administrators look at the real cost and sales statistics

after a specific period is over and make comparisons with what has been budgeted for that

period. For instance, in ABC Ltd if manager have a sales budget around $10,000 and actual sales

figures were $8,000 in that period, thus the variance analysis yields a difference of $2,000.

There are two steps relevant to variance analysis these are:

Calculation and recording of individual variances (Cravens and Piercy, 2016).

Understanding the reason of to each one variance.

Some of the major reason for arising variance are as follows:

Shift in market circumstances that have made conventional budgeting methods

unreasonable, e.g. shortage of raw materials leading to higher prices for sellers. Supported budgeting norms could be too idealistic in origin, e.g. machine production may

be wrongly thought.

Importance of variance analysis for controlling budget

It has been observed that Evaluation of variance allows budgeters gain an even more

practical picture to make the budget for all the coming year more reliable. As it supports

effective budgeting because management wants to reduced differences from the scheduled

budgets. to make descriptive and advance looking budgetary decisions. Evaluation of fluctuation

behaves as a method of control. Analysis of big differentiation on important products enables the

business to understand the effects and motivates the management explore possible methods to

avoid such deviation. It aid in managing annual budgets by reviewing the estimated budgets and

comparing the same with real income. For instance, the month-end report of ABC Ltd will only

provide statistical data on income and expenditures or levels of inventory. However, the

assessment of variance will assist to recognize the explanations behind the differences between

scheduled and real revenue that could lead to changes in corporate strategy and end goals.

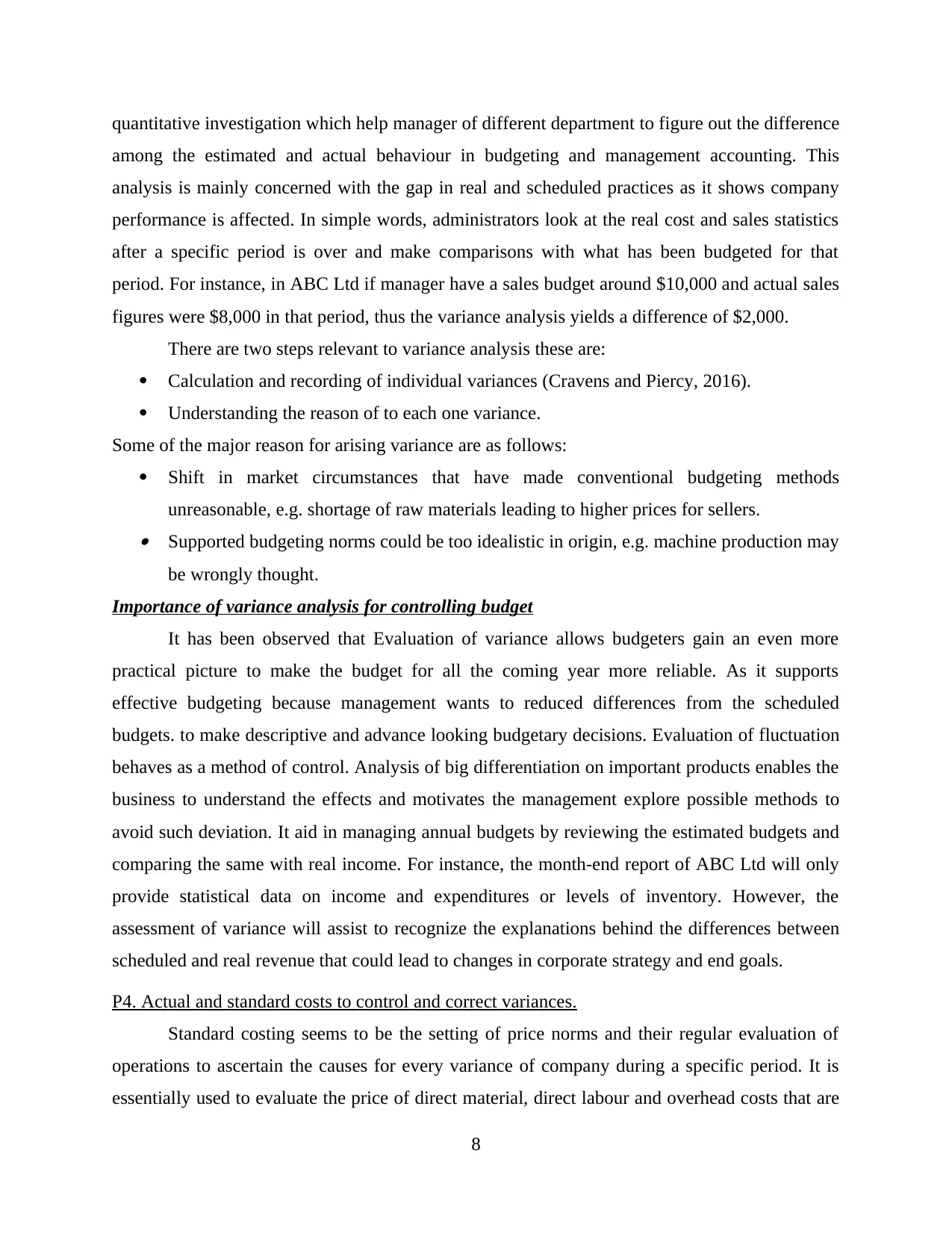

P4. Actual and standard costs to control and correct variances.

Standard costing seems to be the setting of price norms and their regular evaluation of

operations to ascertain the causes for every variance of company during a specific period. It is

essentially used to evaluate the price of direct material, direct labour and overhead costs that are

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the three product elements (De Baerdemaeker and Bruggeman, 2015). Standard goods and

service costs are calculated in advance and compared to the real cost which help to evaluate the

difference and decide for future business situations. This method is used to control variance as it

uses cost estimates to figure all three production cost component such as direct materials, direct

labour and overhead. This support manager to plan for budgets development, product pricing and

costing and distribution to different places for increasing the overall profitability. Hence, when

the standard product cost is calculated in advance and so the difference is compared to the actual

cost.

It actually refers to the real expense of acquiring assets such as direct material, direct

labour and overhead caused by the company. The difference among real costs and normal costs

is therefore referred to as variance. It simply says the actual quantity paid for the purchase of

specific good and by the respective company. For example:

Product

Standard

Time Per

Unit

Budgeted

Units

Total

Standard Hour

Actual

Production

Units Total Production Hour

A 3 3000 9000 1800 5400

B 4 2000 8000 800 3200

Q 5 500 2500 400 2000

Budgeted Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 9,000 8,000 2,500

Direct Labour $2.00 18,000 16,000 5,000

Variable

Overhead $4.00 36,000 32,000 10,000

Total Variable

Costs $6.00 $54,000 $48,000 $15,000

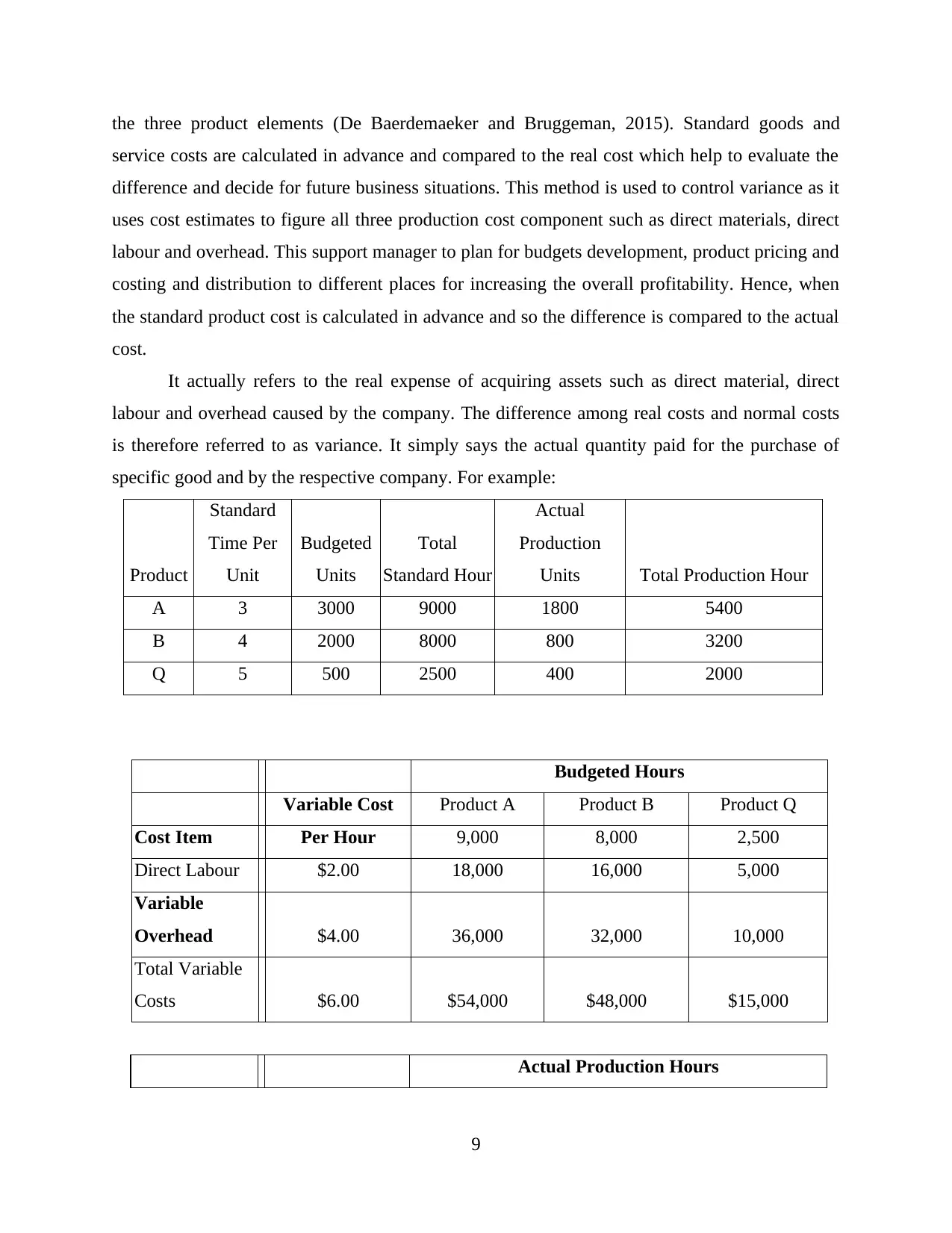

Actual Production Hours

9

service costs are calculated in advance and compared to the real cost which help to evaluate the

difference and decide for future business situations. This method is used to control variance as it

uses cost estimates to figure all three production cost component such as direct materials, direct

labour and overhead. This support manager to plan for budgets development, product pricing and

costing and distribution to different places for increasing the overall profitability. Hence, when

the standard product cost is calculated in advance and so the difference is compared to the actual

cost.

It actually refers to the real expense of acquiring assets such as direct material, direct

labour and overhead caused by the company. The difference among real costs and normal costs

is therefore referred to as variance. It simply says the actual quantity paid for the purchase of

specific good and by the respective company. For example:

Product

Standard

Time Per

Unit

Budgeted

Units

Total

Standard Hour

Actual

Production

Units Total Production Hour

A 3 3000 9000 1800 5400

B 4 2000 8000 800 3200

Q 5 500 2500 400 2000

Budgeted Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 9,000 8,000 2,500

Direct Labour $2.00 18,000 16,000 5,000

Variable

Overhead $4.00 36,000 32,000 10,000

Total Variable

Costs $6.00 $54,000 $48,000 $15,000

Actual Production Hours

9

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour $2.00 10,800 6,400 4,000

Variable

Overhead $4.00 21,600 12,800 8,000

Total Variable

Costs $6.00 $32,400 $19,200 $12,000

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour $2.17 11,700 6,933 4,333

Variable

Overhead $3.33 18,000 10,667 6,667

Total Variable

Costs $5.50 $29,700 $17,600 $11,000

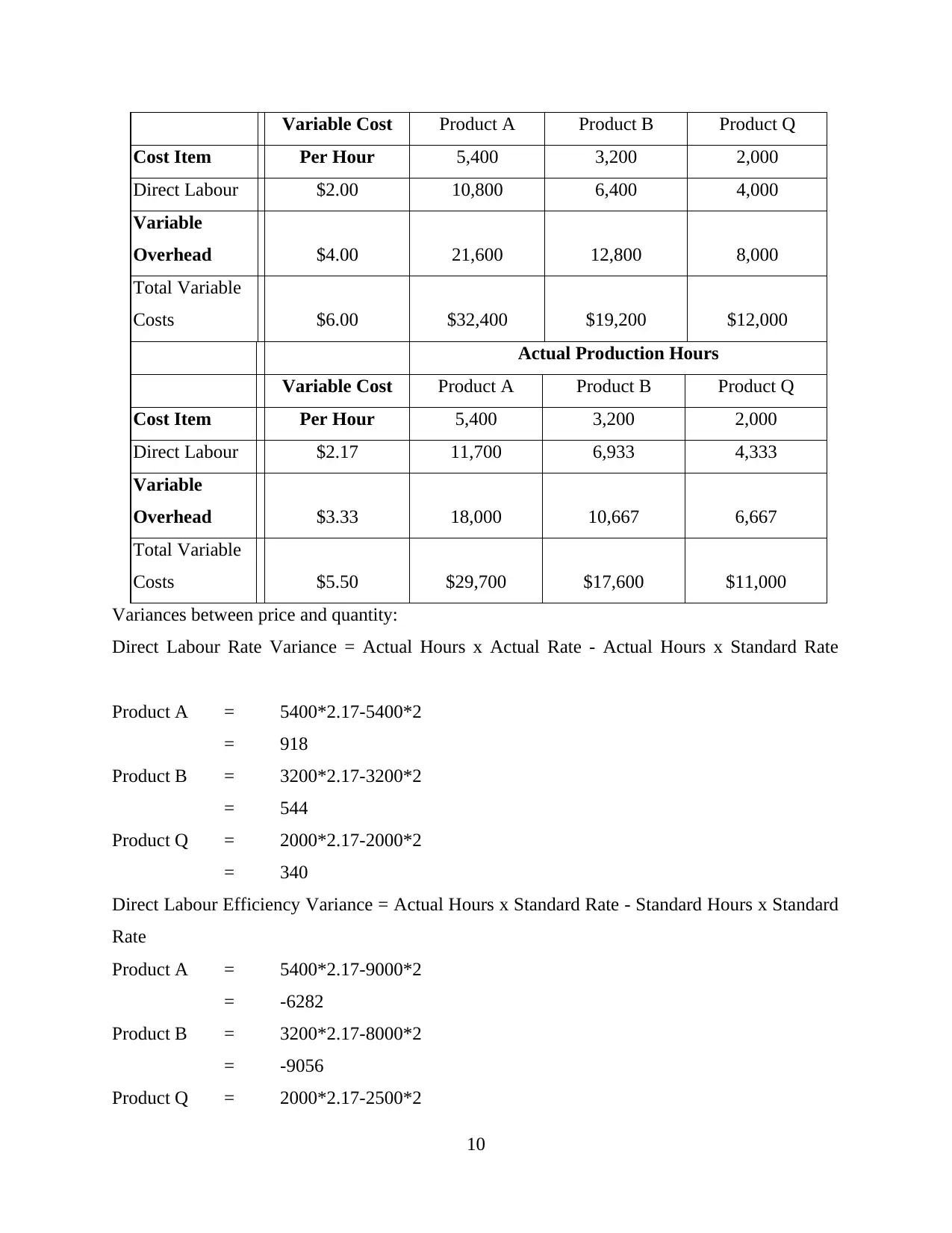

Variances between price and quantity:

Direct Labour Rate Variance = Actual Hours x Actual Rate - Actual Hours x Standard Rate

Product A = 5400*2.17-5400*2

= 918

Product B = 3200*2.17-3200*2

= 544

Product Q = 2000*2.17-2000*2

= 340

Direct Labour Efficiency Variance = Actual Hours x Standard Rate - Standard Hours x Standard

Rate

Product A = 5400*2.17-9000*2

= -6282

Product B = 3200*2.17-8000*2

= -9056

Product Q = 2000*2.17-2500*2

10

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour $2.00 10,800 6,400 4,000

Variable

Overhead $4.00 21,600 12,800 8,000

Total Variable

Costs $6.00 $32,400 $19,200 $12,000

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labour $2.17 11,700 6,933 4,333

Variable

Overhead $3.33 18,000 10,667 6,667

Total Variable

Costs $5.50 $29,700 $17,600 $11,000

Variances between price and quantity:

Direct Labour Rate Variance = Actual Hours x Actual Rate - Actual Hours x Standard Rate

Product A = 5400*2.17-5400*2

= 918

Product B = 3200*2.17-3200*2

= 544

Product Q = 2000*2.17-2000*2

= 340

Direct Labour Efficiency Variance = Actual Hours x Standard Rate - Standard Hours x Standard

Rate

Product A = 5400*2.17-9000*2

= -6282

Product B = 3200*2.17-8000*2

= -9056

Product Q = 2000*2.17-2500*2

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.