Financial Analysis: Present vs. Proposed Machine Investment - Report

VerifiedAdded on 2022/12/29

|9

|907

|43

Report

AI Summary

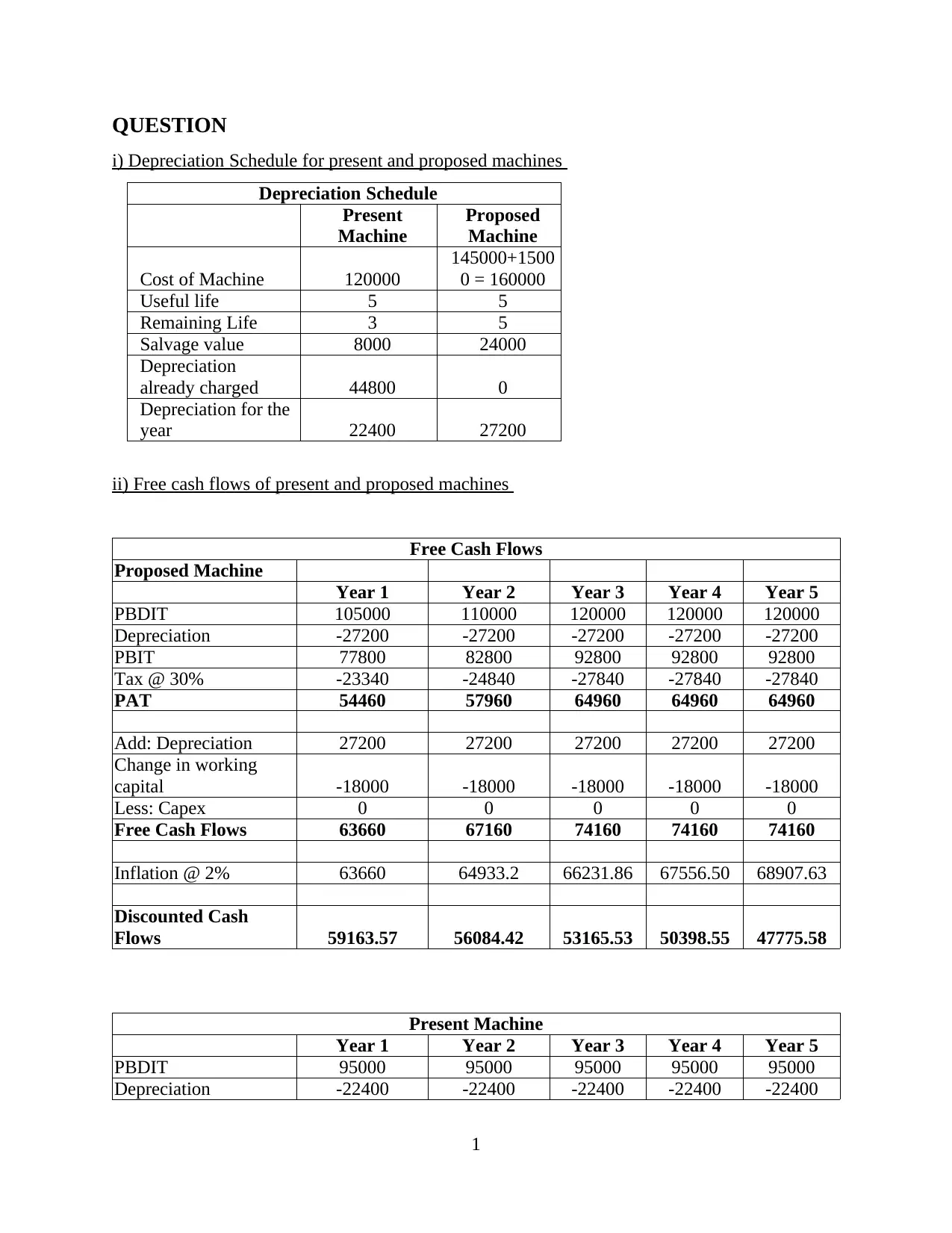

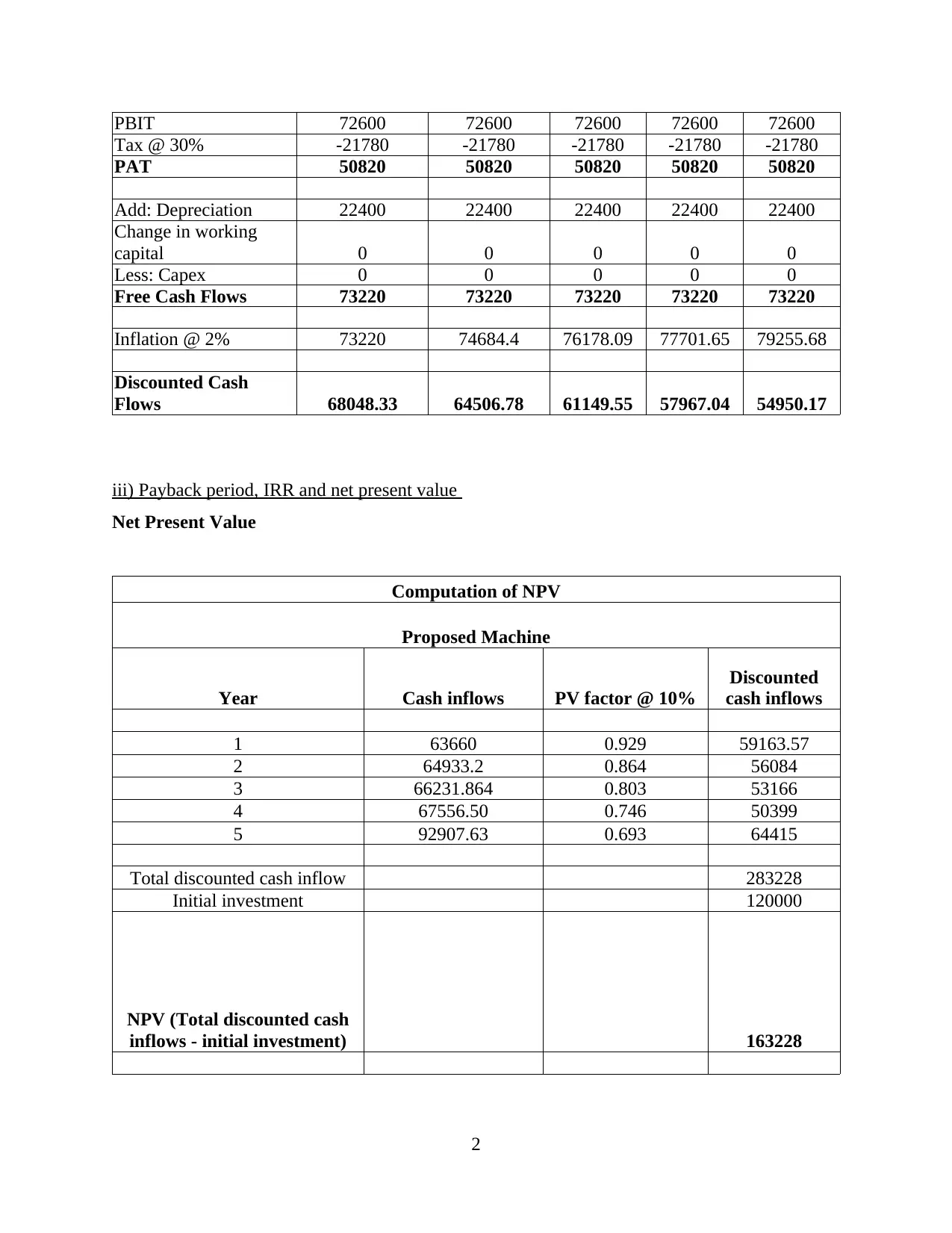

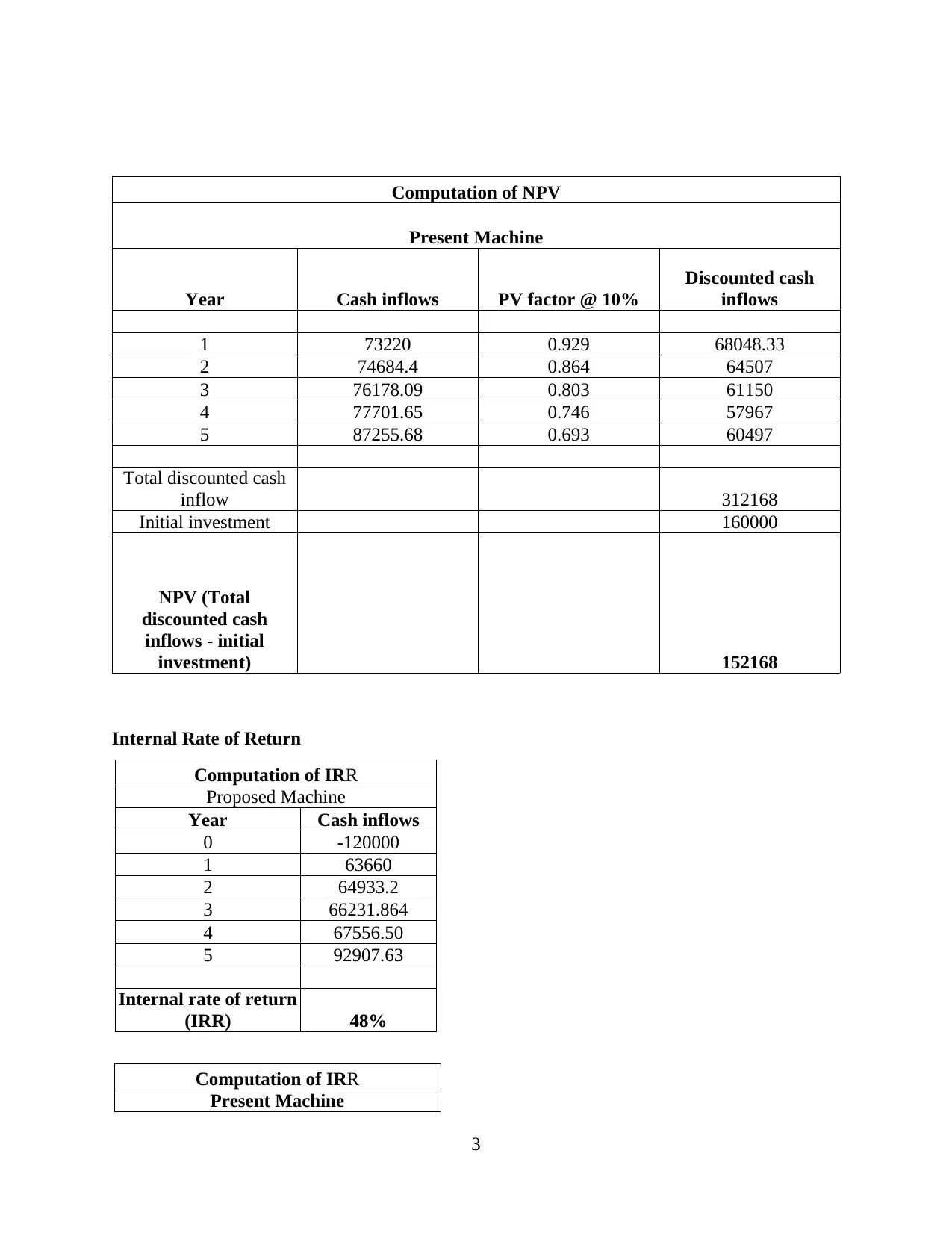

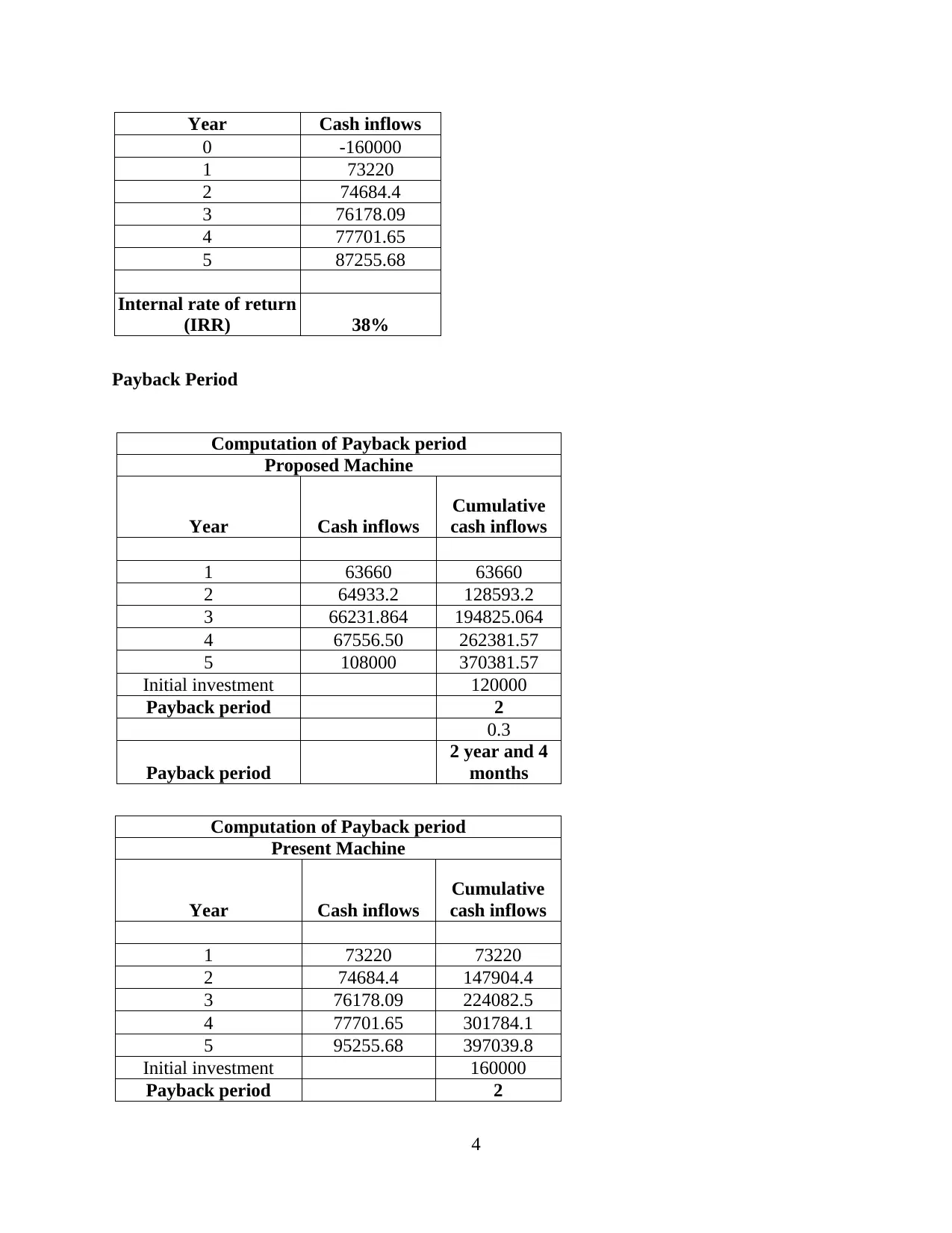

This report presents a detailed financial analysis comparing the present and a proposed machine investment for ABC Manufacturing. It begins with the creation of depreciation schedules for both machines, followed by the calculation of free cash flows over a five-year period, considering factors like depreciation, tax, and changes in working capital. The analysis then proceeds to determine the payback period, Internal Rate of Return (IRR), and Net Present Value (NPV) for each machine. The report computes the NPV for both machines, with the proposed machine yielding a higher NPV, suggesting it would generate greater profits. The IRR is also significantly higher for the proposed machine. Based on the financial metrics, the report recommends that ABC Manufacturing invest in the new machine and sell the old one to maximize returns and reduce initial investment costs. The document concludes with references to relevant academic literature supporting the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.