BMP5006 Financial Management Presentation: ABC of Rock Widget Ltd

VerifiedAdded on 2023/06/04

|19

|2699

|317

Presentation

AI Summary

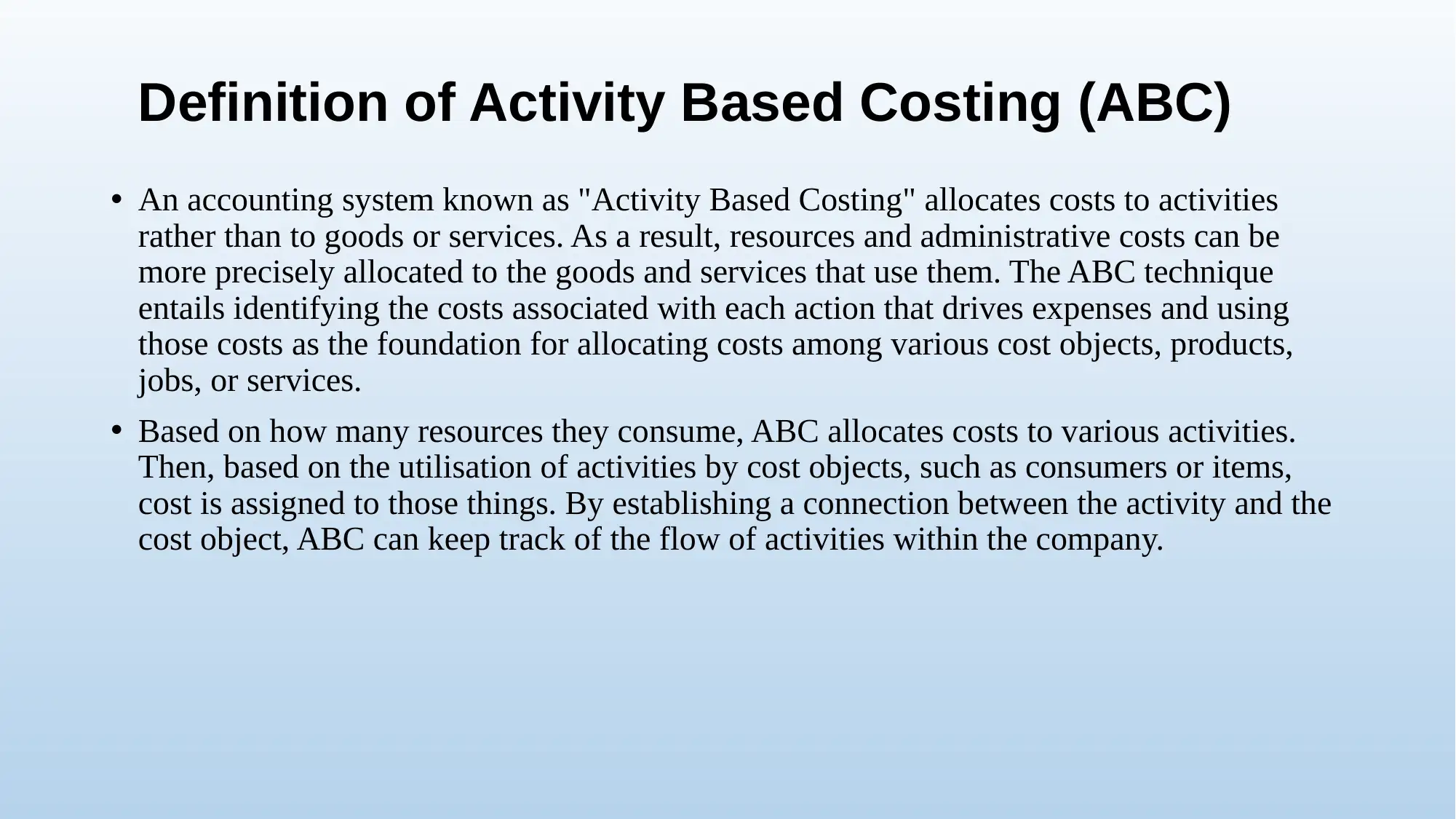

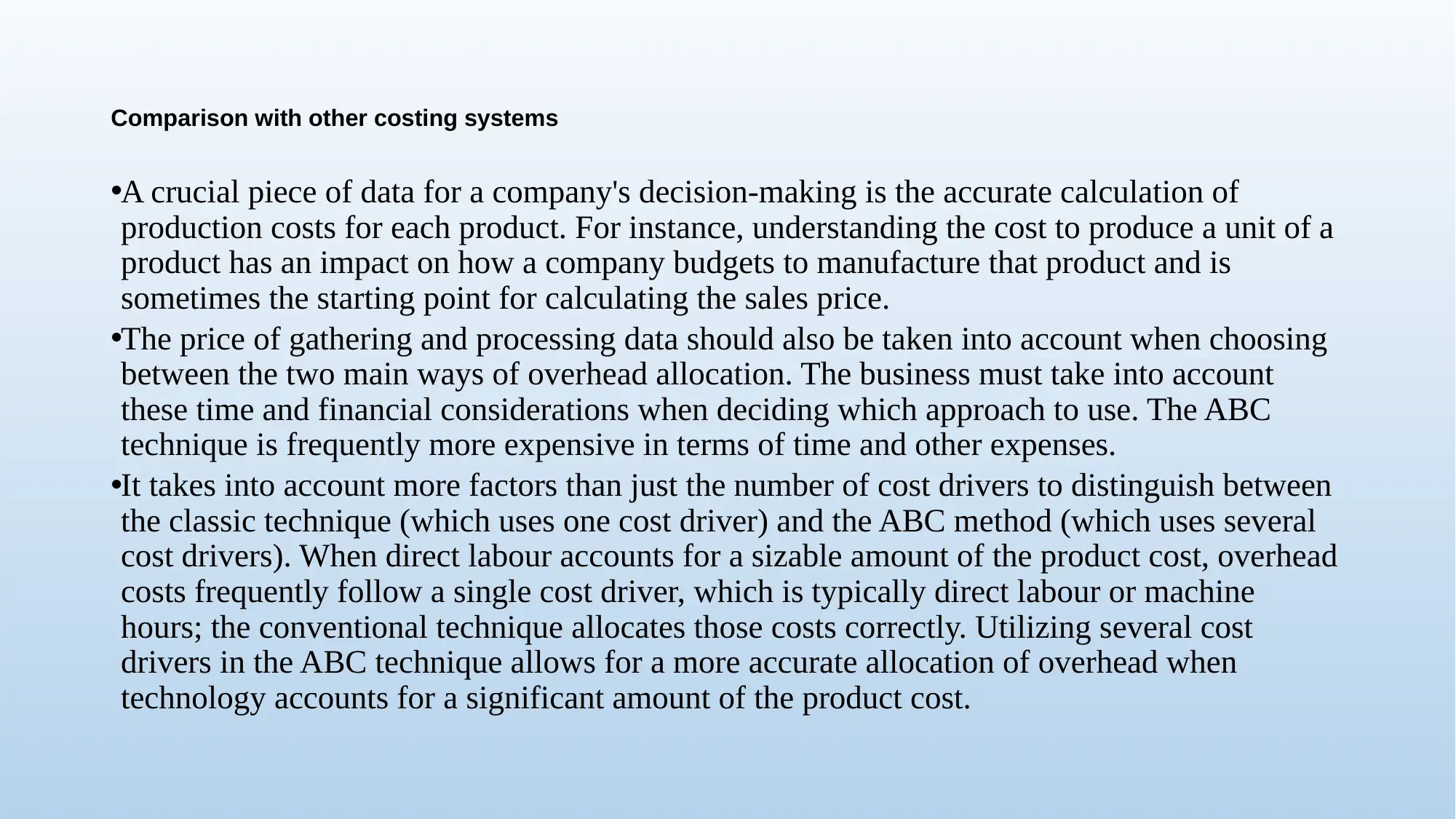

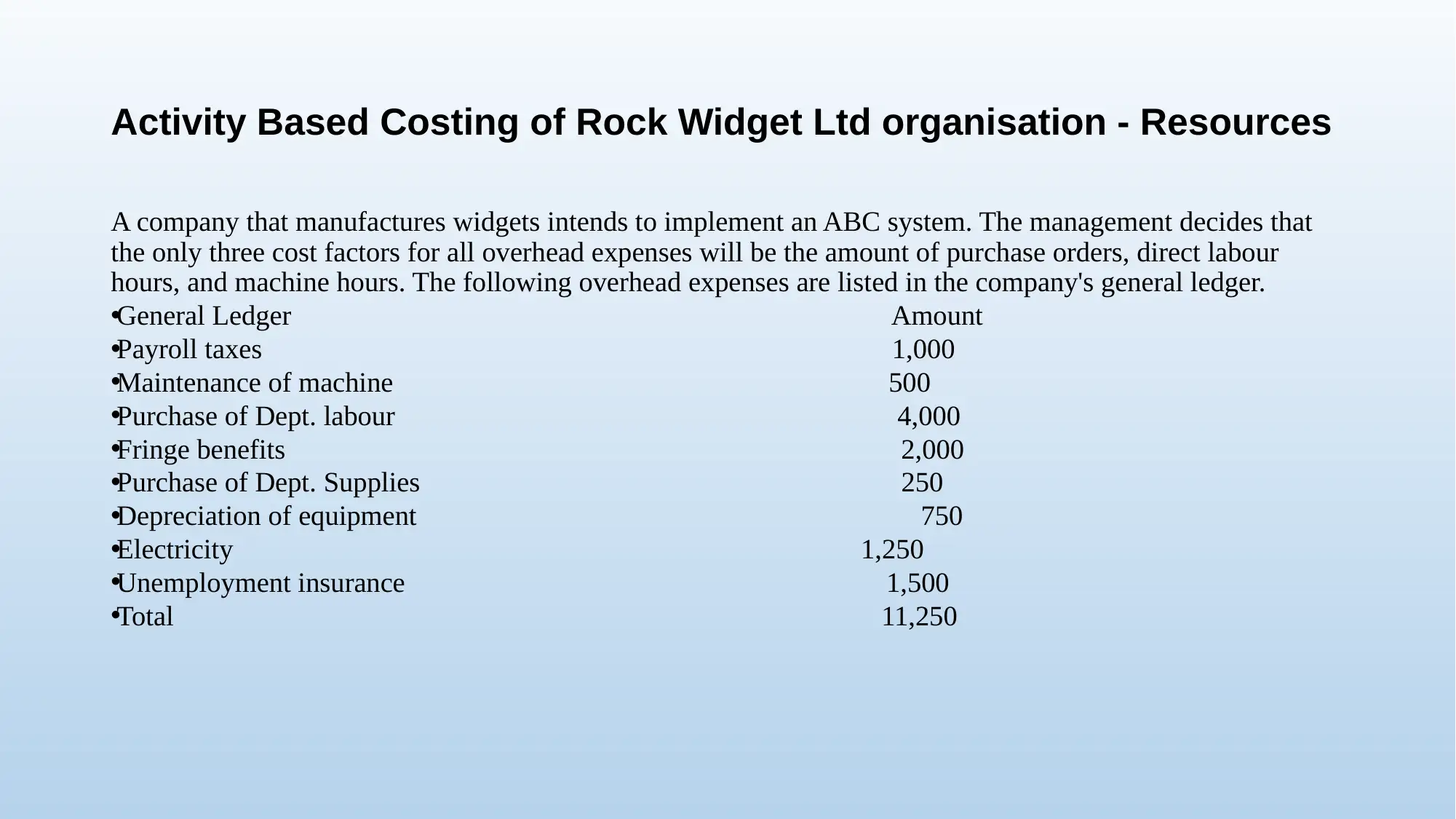

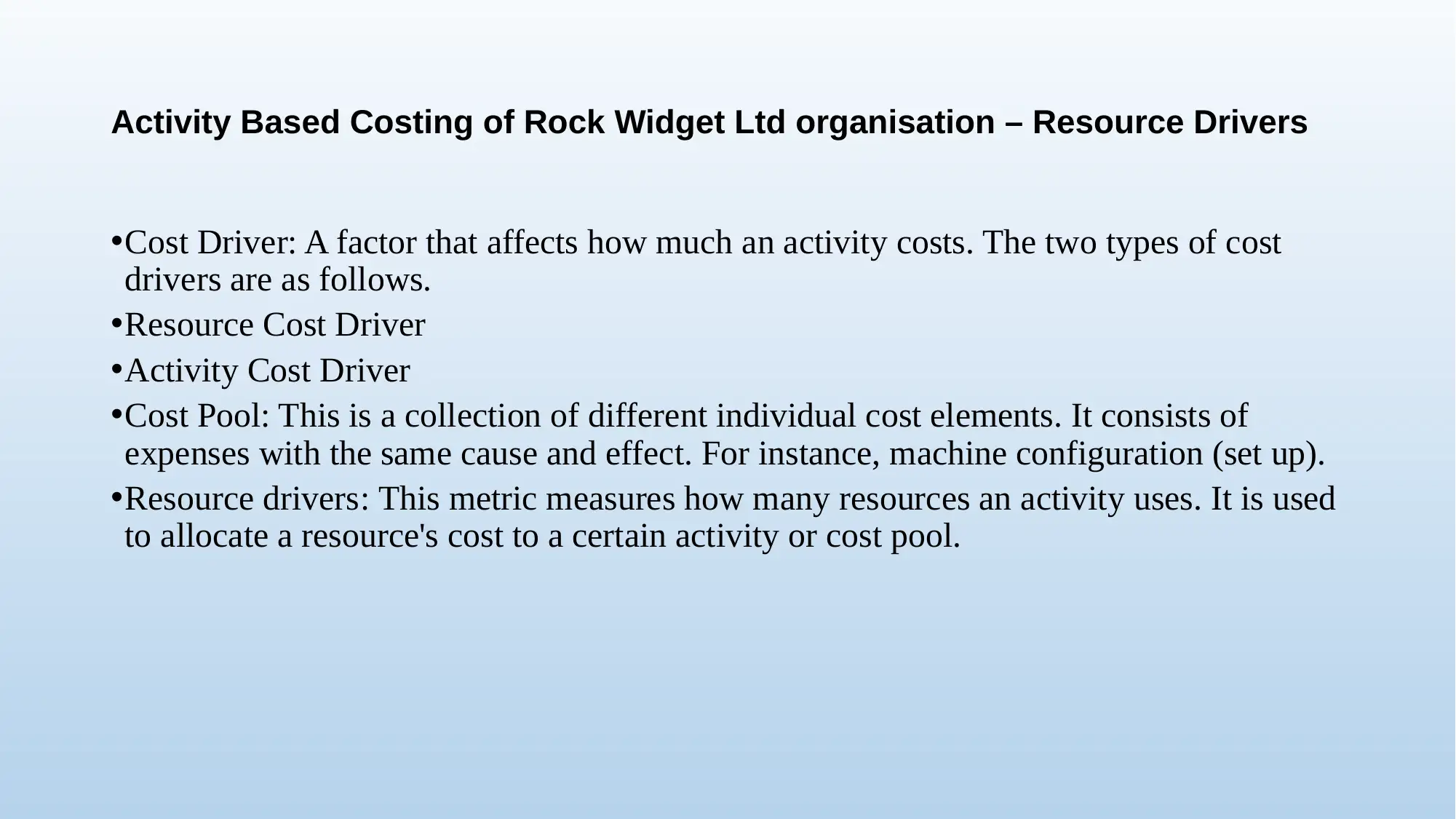

This presentation delves into Activity Based Costing (ABC), a financial management technique that allocates costs to activities rather than products or services, providing a more accurate allocation of resources and administrative costs. It compares ABC with traditional costing systems, highlighting the importance of accurate production cost calculation for decision-making. The presentation analyzes the application of ABC within Rock Widget Ltd, including resources, resource drivers, activities, activity drivers, and cost objects. It also discusses the advantages and disadvantages of ABC, the use of traditional costing techniques, and why ABC might be preferred. The presentation outlines the steps involved in implementing an ABC system, including identifying activities, determining activity cost drivers, and calculating activity cost driver rates to improve overhead allocation. It emphasizes how ABC offers a more precise picture of cost behavior, leading to better financial decisions.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.