Job Costing Analysis: Simple vs. ABC Costing for ACCG200 Case Study

VerifiedAdded on 2023/02/01

|3

|507

|81

Case Study

AI Summary

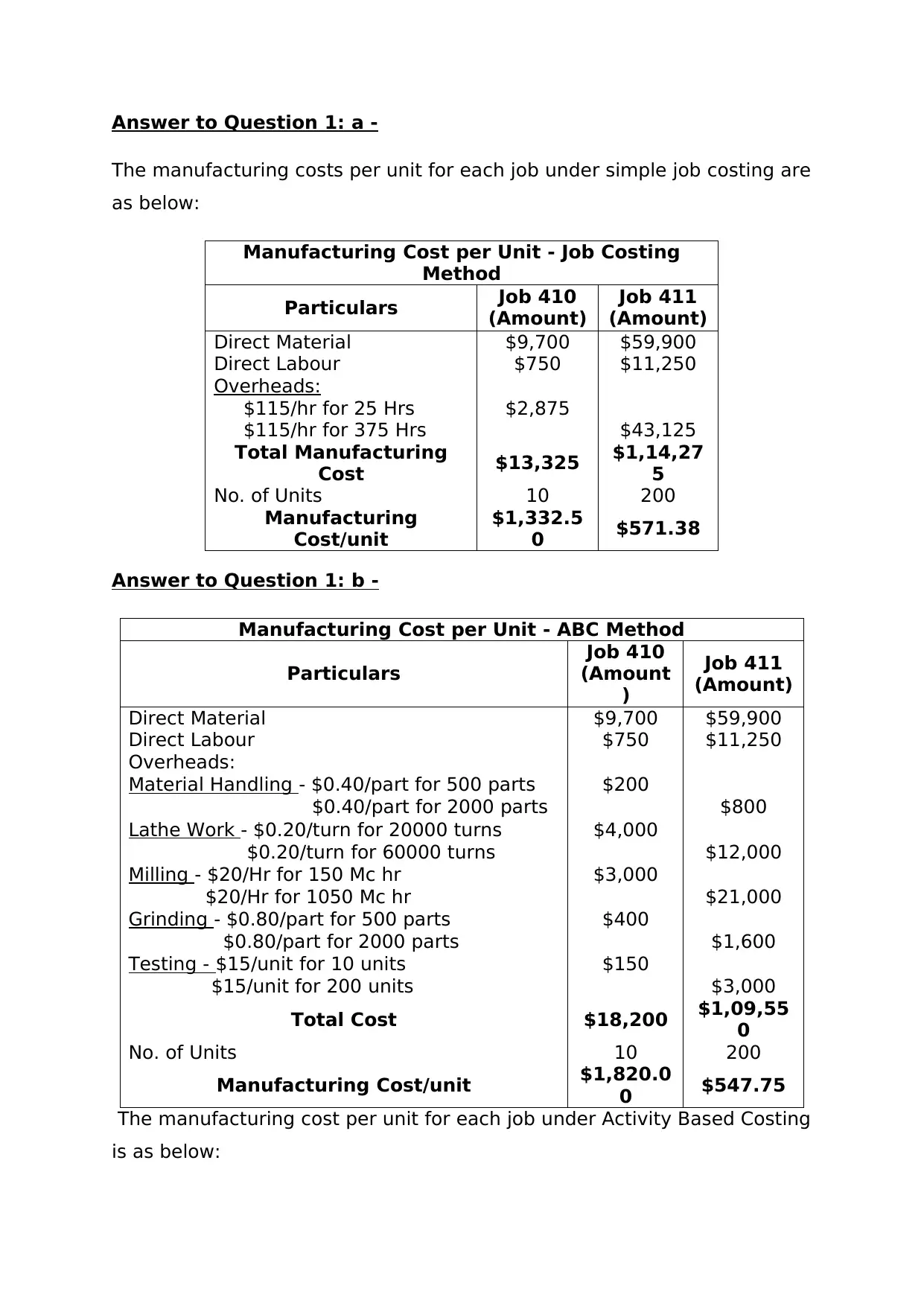

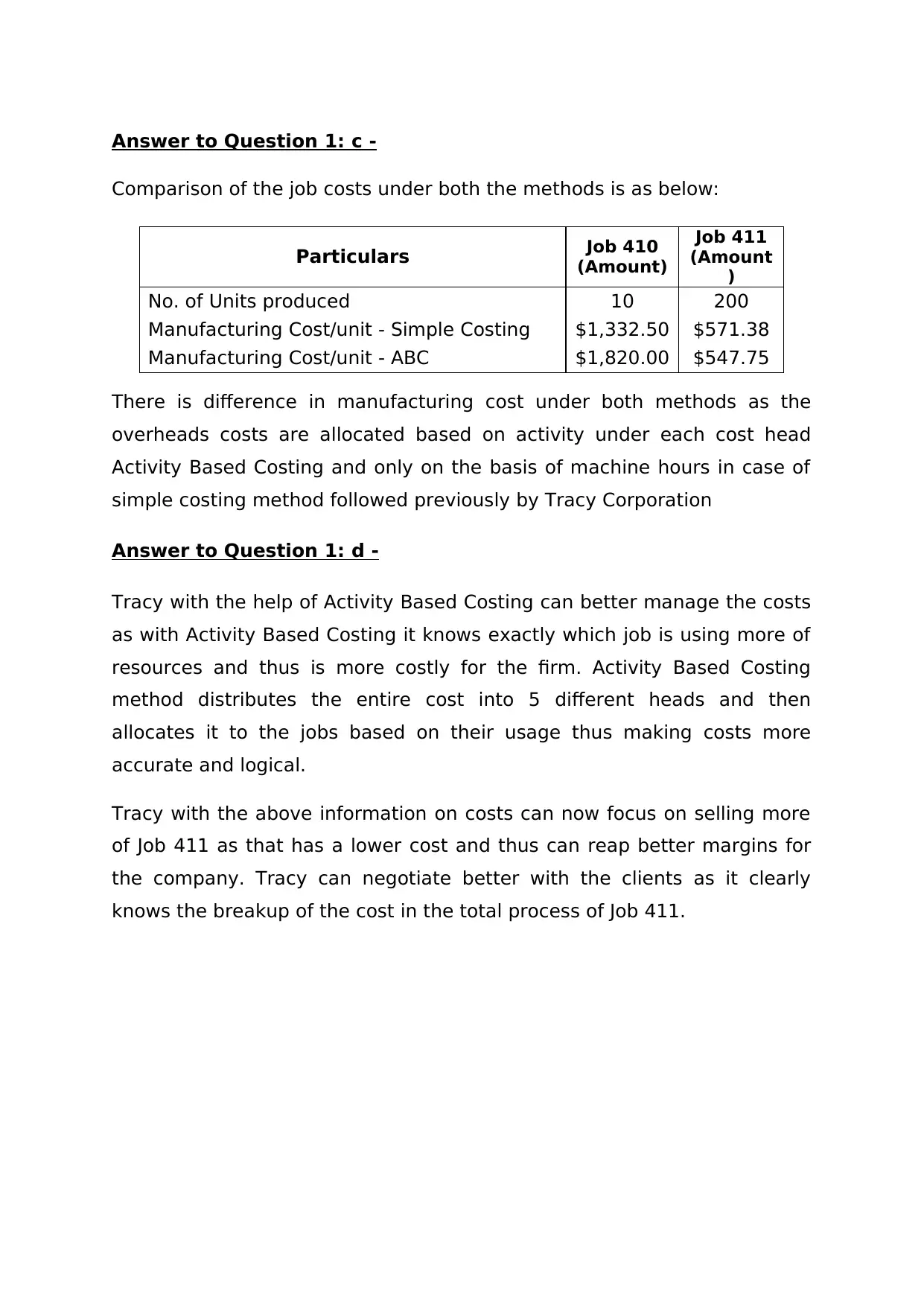

This document provides a detailed solution to a case study focusing on job costing methods. The analysis compares two primary approaches: simple job costing and activity-based costing (ABC). The solution calculates manufacturing costs per unit for two jobs (410 and 411) under both methods, considering direct materials, direct labor, and overheads. A key aspect of the solution involves a comprehensive breakdown of overhead allocation, highlighting the differences between the two methods. Simple costing uses a single overhead rate based on machine hours, while ABC allocates overhead costs across multiple activity cost drivers, such as material handling, lathe work, milling, grinding, and testing. The document then compares the manufacturing costs per unit under both methods, revealing how ABC provides a more accurate and logical cost distribution. The case study concludes by discussing how Tracy Corporation can leverage ABC to better manage costs, make informed decisions about product pricing and sales strategies, and improve client negotiations. The solution references relevant accounting literature to support the analysis.

1 out of 3

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.