Cost Accounting Report: Job, Process, ABC Costing, Overhead Analysis

VerifiedAdded on 2023/06/08

|11

|1740

|109

Report

AI Summary

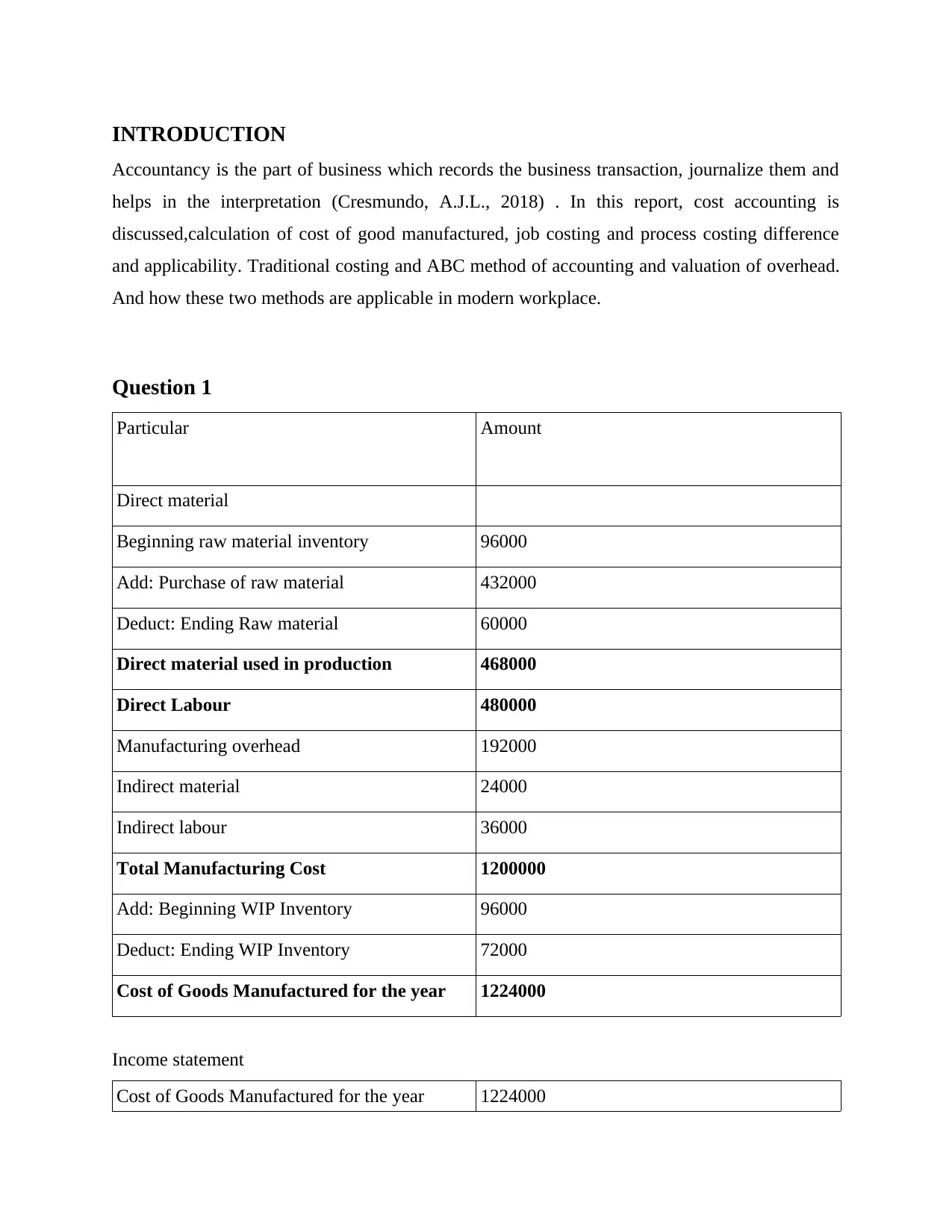

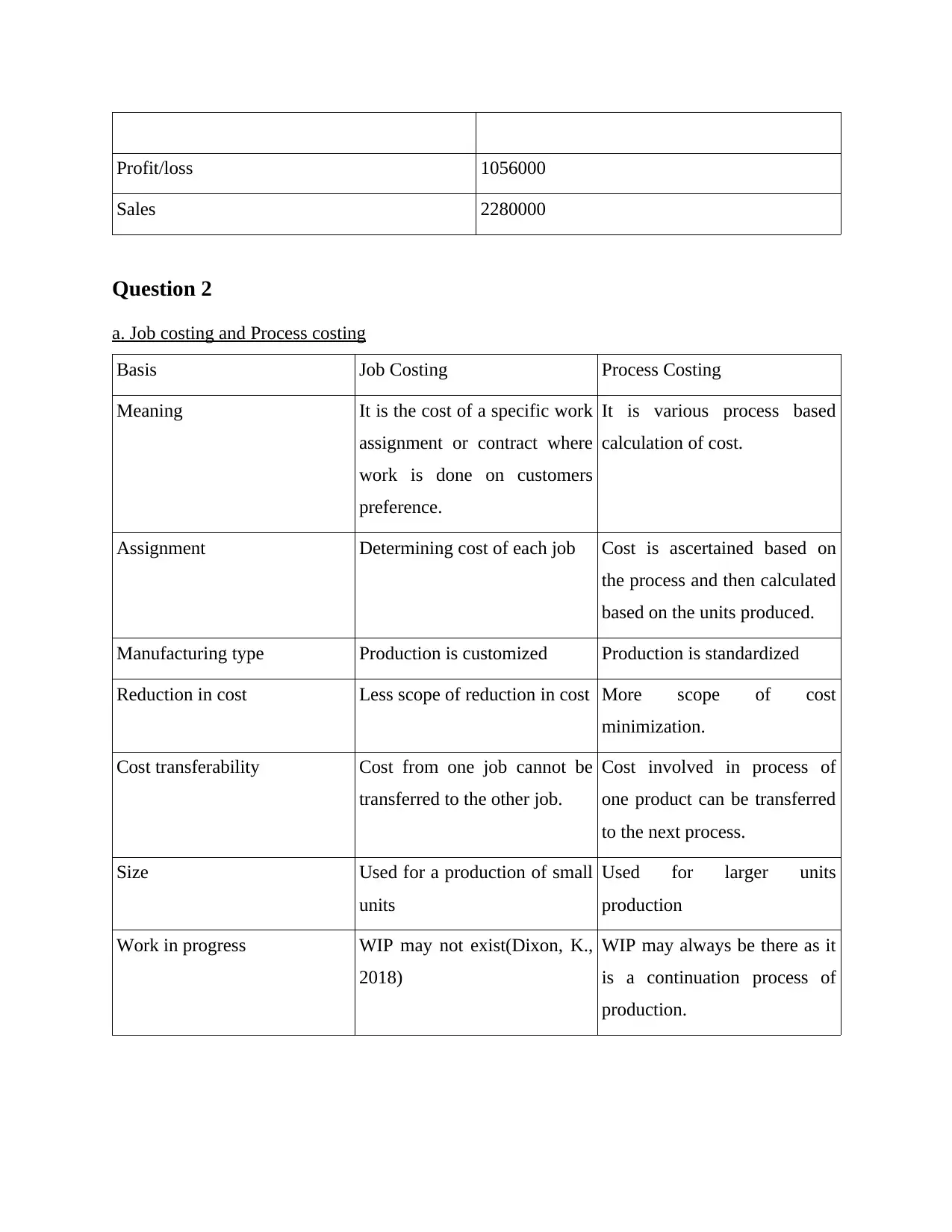

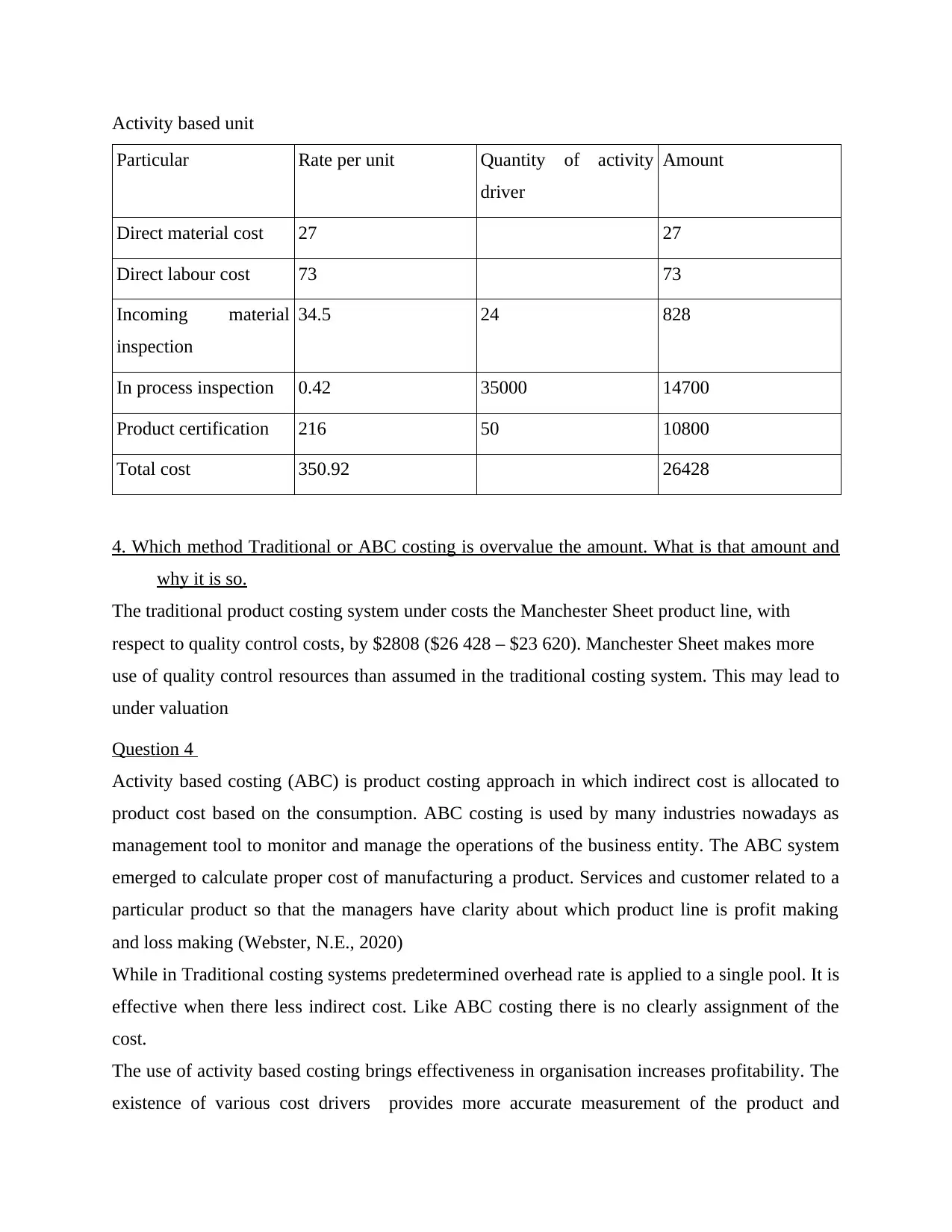

This report delves into the core concepts of cost accounting, providing a comprehensive overview of various costing methods. It begins by defining accountancy and its role in business, then explores the differences between job costing and process costing, illustrating their applicability through real-world examples like architect firms and oil refineries. The report then calculates the cost of goods manufactured, including direct materials, direct labor, and manufacturing overhead. It proceeds to analyze traditional costing versus ABC costing, calculating overhead rates and cost per unit under both methods, and determining which method overvalues the amount and why. The report includes journal entries for various transactions, such as material purchases, labor costs, and depreciation. Finally, it discusses the application of ABC and traditional costing, highlighting the benefits of ABC in improving operational efficiency and profitability, and concludes by summarizing the key findings and emphasizing the importance of accurate cost allocation in modern business environments. The report utilizes formulas, calculations, and real-world examples to illustrate the concepts, providing a clear understanding of cost accounting principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.