Analysis of the ABC Model and Its Application to Treasury Wine Estates

VerifiedAdded on 2021/05/31

|13

|2780

|28

Report

AI Summary

This report provides an analysis of the Activity-Based Costing (ABC) model as a management accounting tool, focusing on its application to Treasury Wine Estates (TWE), an ASX-listed wine company. The report explains the ABC model, its features, and its benefits, highlighting its ability to identify, assign, and describe costs to business processes, offering a more accurate cost management system compared to traditional methods. It examines how the ABC model aligns with TWE's goals and strategies, particularly in improving financial performance and cost optimization. The report recommends the implementation of ABC at TWE to enhance its cost management practices. Additionally, the report suggests the Balanced Scorecard as another suitable management accounting tool for TWE, which could help address performance measurement inadequacies by utilizing both financial and non-financial measures. The conclusion emphasizes that TWE can utilize ABC to replace its current standard costing to achieve key objectives like increasing profitability and improving financial performance.

Managerial Accounting 1

MANAGERIAL ACCOUNTING

Author’s Name

MANAGERIAL ACCOUNTING

Author’s Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 2

Course Title

Professor

City

Date

Course Title

Professor

City

Date

Managerial Accounting 3

Executive Summary

This report presents analysis of ABC model as one of the management costing system and its

relation with Treasury Wine Estates. ABC is one of the most powerful tools used in

measuring an organization’s performance. It is utilized in identifying, assigning and

describing different costs to the agency operations or business processes. ABC is the multi-

level cost allocation technique where different costs are driven in stages; that is, from activity

to activity, and from one stage to the other. It is usually a more detailed technique to

attributing costs, first to their activities and to their cost objects which is said to create some

demand for such indirect costs. Based on the analysis, it was found out that Treasury Wine

Estate can utilize ABC in replacing it current standard costing, since the model could assist

the firm to doing better cost management which would in turn assist it achieve it key

objectives. Basically, increasing profitability or improving financial performance is a

complex thing for any firm, which has numerous aspects require to be considered. Hence, it

was found that ABC could assist Treasury Wine Estate making more profits that could in turn

assist in improving its profitability and sales level.

Executive Summary

This report presents analysis of ABC model as one of the management costing system and its

relation with Treasury Wine Estates. ABC is one of the most powerful tools used in

measuring an organization’s performance. It is utilized in identifying, assigning and

describing different costs to the agency operations or business processes. ABC is the multi-

level cost allocation technique where different costs are driven in stages; that is, from activity

to activity, and from one stage to the other. It is usually a more detailed technique to

attributing costs, first to their activities and to their cost objects which is said to create some

demand for such indirect costs. Based on the analysis, it was found out that Treasury Wine

Estate can utilize ABC in replacing it current standard costing, since the model could assist

the firm to doing better cost management which would in turn assist it achieve it key

objectives. Basically, increasing profitability or improving financial performance is a

complex thing for any firm, which has numerous aspects require to be considered. Hence, it

was found that ABC could assist Treasury Wine Estate making more profits that could in turn

assist in improving its profitability and sales level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 4

Introduction

An increasing number of different forms are using the ABC in gaining some insights

into manufacturing processes and product process. With these, the report aims at

presenting what ABC is all about. It also aims to present its features and how the model

aligns with existing goals as well as strategies of one of the ASX listed company.

Additionally, the report would present some of the recommendations in implementing

ABC explaining how this model could improve management accounting information on

the company’s top management team. Finally, the report would explain other

management accounting tool which would be suitable for the company.

Explanation of ABC Model and Its Features

ABC is one of the management accounting tool indicating how different resources are

utilized by activities in producing products or outputs beneficial to clients (Bufi & Moilanen

2014). Besides, ABC is one of the most powerful tools used in measuring an organization’s

performance. It is utilized in identifying, assigning and describing different costs to the

agency operations or business processes (Innes & Kouhy 2011). The tool is said to offer more

accurate management costing system than the traditional costing accounting in identifying

available opportunities for improvement of the business processes efficiency and

effectiveness through determination of true costs of the services or products. Additionally,

ABC utilizes or employs cost drivers in assigning costs from different activities to the outputs

(Theriou, Theriou & Papadopoulos 2007). In other words, ABC is the multi-level cost

allocation technique where different costs are driven in stages; that is, from activity to

activity, and from one stage to the other. Further, ABC is said to encourages organization’s

management in evaluating cost-effectiveness and efficiency of the program activities. its

Introduction

An increasing number of different forms are using the ABC in gaining some insights

into manufacturing processes and product process. With these, the report aims at

presenting what ABC is all about. It also aims to present its features and how the model

aligns with existing goals as well as strategies of one of the ASX listed company.

Additionally, the report would present some of the recommendations in implementing

ABC explaining how this model could improve management accounting information on

the company’s top management team. Finally, the report would explain other

management accounting tool which would be suitable for the company.

Explanation of ABC Model and Its Features

ABC is one of the management accounting tool indicating how different resources are

utilized by activities in producing products or outputs beneficial to clients (Bufi & Moilanen

2014). Besides, ABC is one of the most powerful tools used in measuring an organization’s

performance. It is utilized in identifying, assigning and describing different costs to the

agency operations or business processes (Innes & Kouhy 2011). The tool is said to offer more

accurate management costing system than the traditional costing accounting in identifying

available opportunities for improvement of the business processes efficiency and

effectiveness through determination of true costs of the services or products. Additionally,

ABC utilizes or employs cost drivers in assigning costs from different activities to the outputs

(Theriou, Theriou & Papadopoulos 2007). In other words, ABC is the multi-level cost

allocation technique where different costs are driven in stages; that is, from activity to

activity, and from one stage to the other. Further, ABC is said to encourages organization’s

management in evaluating cost-effectiveness and efficiency of the program activities. its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 5

main benefits is providing insights on the basis of past computed costs not only spending and

them applying similar information in making better decisions (Venieris & Cohen 2008).

ABC provide more accurate outlook on the reality since it recognizes that some of the costs

do not differ with volume measurement but with other measurements (Bufi & Moilanen

2014). It is usually a more detailed technique to attributing costs, first to their activities and to

their cost objects which is said to create some demand for such indirect costs. ABC offer

correct costing data features of being relevant and efficient. Since ABC focuses mostly on

the activities performed during production, it provides alternatives to traditional means of

accounting. According to Pineno (2002), ABC is a system that assesses different costs and

performance of capitals, costs objects and activities, assigns different resources to their

relevant activities as well as different activities to their cost objects on the basis of their use

as well as recognizes the causal relationships of the cost drivers to the activities. It is also

viewed as a technique of measuring different cost and presentation of cost objects and

activities. It usually assigns costs to different cost objects on the basis of the use of the

activities and assigns different costs to their activities on the basis of the use of different

resources. ABC provides some added advantages of at least reducing or evading alterations in

the product costing which is allocated as the indirect costs (Anand, Sahay & Saha 2005).

Besides, it offer useful information regarding how expenses occur, how cost-effect has been

distributed to different departments as well as how one might accomplish quality

improvements over its rivals.

The ABC comprises of two different stages; first, the ABC take into consideration that each

activity causes some costs, and assigns all the costs to their relevant activities (Velmurugan

2010). Such activities are said to take place in the cost pools or activity centres and are

usually evaluated by the cost drivers. Cost of such activities or resources are referred to as

main benefits is providing insights on the basis of past computed costs not only spending and

them applying similar information in making better decisions (Venieris & Cohen 2008).

ABC provide more accurate outlook on the reality since it recognizes that some of the costs

do not differ with volume measurement but with other measurements (Bufi & Moilanen

2014). It is usually a more detailed technique to attributing costs, first to their activities and to

their cost objects which is said to create some demand for such indirect costs. ABC offer

correct costing data features of being relevant and efficient. Since ABC focuses mostly on

the activities performed during production, it provides alternatives to traditional means of

accounting. According to Pineno (2002), ABC is a system that assesses different costs and

performance of capitals, costs objects and activities, assigns different resources to their

relevant activities as well as different activities to their cost objects on the basis of their use

as well as recognizes the causal relationships of the cost drivers to the activities. It is also

viewed as a technique of measuring different cost and presentation of cost objects and

activities. It usually assigns costs to different cost objects on the basis of the use of the

activities and assigns different costs to their activities on the basis of the use of different

resources. ABC provides some added advantages of at least reducing or evading alterations in

the product costing which is allocated as the indirect costs (Anand, Sahay & Saha 2005).

Besides, it offer useful information regarding how expenses occur, how cost-effect has been

distributed to different departments as well as how one might accomplish quality

improvements over its rivals.

The ABC comprises of two different stages; first, the ABC take into consideration that each

activity causes some costs, and assigns all the costs to their relevant activities (Velmurugan

2010). Such activities are said to take place in the cost pools or activity centres and are

usually evaluated by the cost drivers. Cost of such activities or resources are referred to as

Managerial Accounting 6

cost elements. In the second stage, the ABC take into account that different products consume

different activities and therefore costs incurred at particular cost pools or cost centres are

allotted to products on the basis of products consumptions of every activity as well as level of

these activities to ABC (Israelsen 1994). In order to accomplish such, cost drivers are said to

be closely dedicated to assigning different activity costs to the relevant products. Hence,

ABC captures factual cost bookkeeping by assigning the overhead outlays to different cost

centres as well as onwards to the output services or products. Besides, this model is

significant in refining processes both the logically and in the assessment role (Shane 2005).

This is because it determines activities performed by which organization’s resources and

attribute different costs to their relevant products on the basis of their utilization of these

resources.

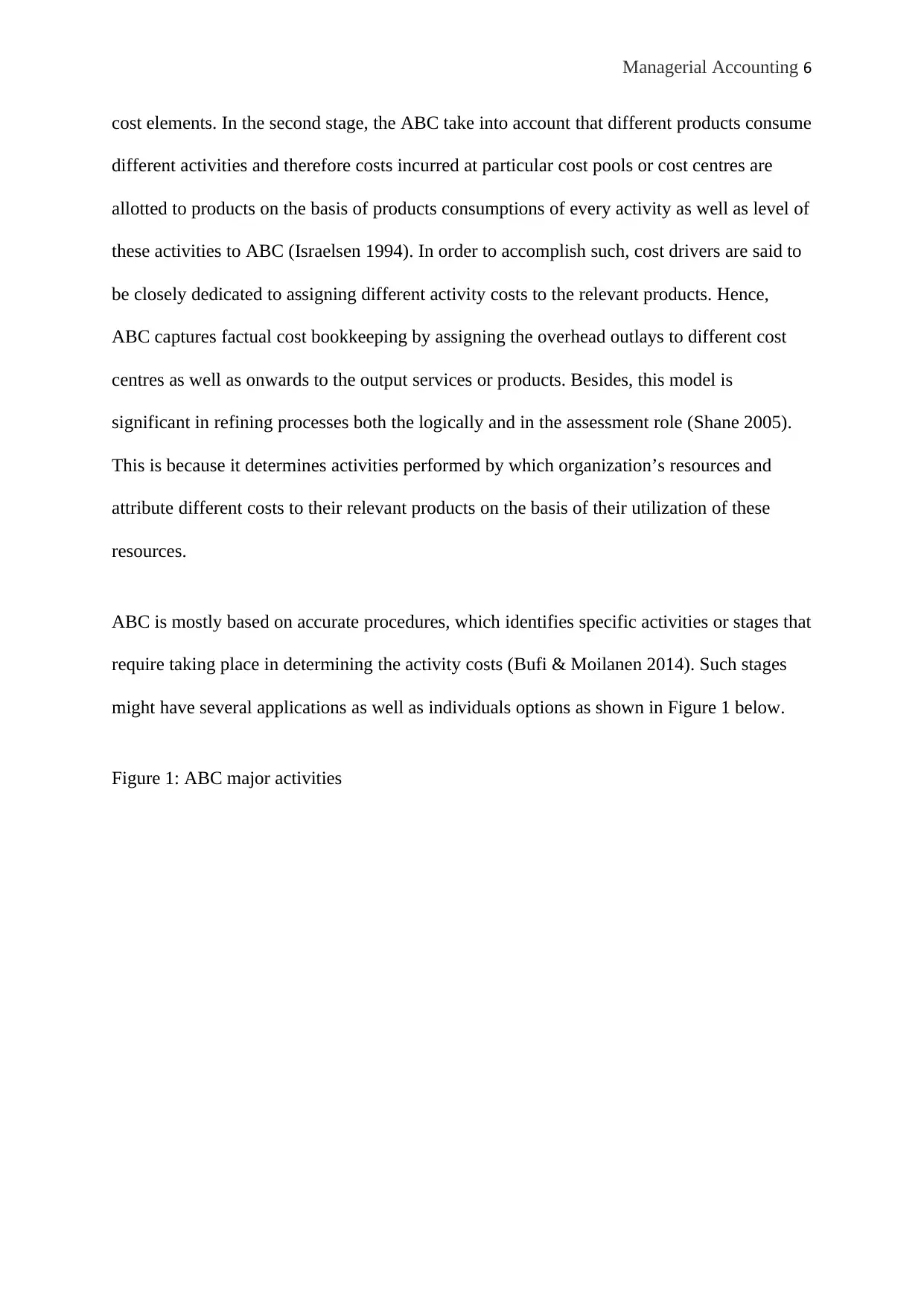

ABC is mostly based on accurate procedures, which identifies specific activities or stages that

require taking place in determining the activity costs (Bufi & Moilanen 2014). Such stages

might have several applications as well as individuals options as shown in Figure 1 below.

Figure 1: ABC major activities

cost elements. In the second stage, the ABC take into account that different products consume

different activities and therefore costs incurred at particular cost pools or cost centres are

allotted to products on the basis of products consumptions of every activity as well as level of

these activities to ABC (Israelsen 1994). In order to accomplish such, cost drivers are said to

be closely dedicated to assigning different activity costs to the relevant products. Hence,

ABC captures factual cost bookkeeping by assigning the overhead outlays to different cost

centres as well as onwards to the output services or products. Besides, this model is

significant in refining processes both the logically and in the assessment role (Shane 2005).

This is because it determines activities performed by which organization’s resources and

attribute different costs to their relevant products on the basis of their utilization of these

resources.

ABC is mostly based on accurate procedures, which identifies specific activities or stages that

require taking place in determining the activity costs (Bufi & Moilanen 2014). Such stages

might have several applications as well as individuals options as shown in Figure 1 below.

Figure 1: ABC major activities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 7

Source: Μυτακίδης (2015).

ABC is said to report more accurate costs and therefore decrease any probability of the

management making poor decision on the basis of the available cost information (Anand,

Sahay & Saha 2005). To be more specific, the ABC improves managerial decision-making

process that is specifically crucial for different organization facing intense competition

(Angelis & Lee 1996). Besides, ABC measure more precisely expenses of different product

process and design involvedness. This implies that it assist product manufacturers to

understand some of the financial inferences of the design selection and therefore sway

conduct by accomplishing the design for the manufacturability (Oseifuah 2018).

Additionally, ABC is said to identify amount of the expenditures incurred on different

activities and therefore outline which particular activities are crucial for manufacturing. Here,

identification of activities which is crucial enhances introduction of the concept of the

continuous improvement. The ABC model recognizes that every client has his or her

Source: Μυτακίδης (2015).

ABC is said to report more accurate costs and therefore decrease any probability of the

management making poor decision on the basis of the available cost information (Anand,

Sahay & Saha 2005). To be more specific, the ABC improves managerial decision-making

process that is specifically crucial for different organization facing intense competition

(Angelis & Lee 1996). Besides, ABC measure more precisely expenses of different product

process and design involvedness. This implies that it assist product manufacturers to

understand some of the financial inferences of the design selection and therefore sway

conduct by accomplishing the design for the manufacturability (Oseifuah 2018).

Additionally, ABC is said to identify amount of the expenditures incurred on different

activities and therefore outline which particular activities are crucial for manufacturing. Here,

identification of activities which is crucial enhances introduction of the concept of the

continuous improvement. The ABC model recognizes that every client has his or her

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 8

character and therefore the firm does not make similar profit from every client (Angelopoulos

& Pollalis 2017).

B) How ABC Model Aligns With the Current Goals and Strategies of Treasury Wine

Estate

i) Treasury Wine Estate’s Mission and Objectives

Treasury Wine Estate is the largest wine firms across the globe which is listed in ASX. The

firms is mostly focused on delivering high quality shareholders’ value vial production of

quality products and selling and marketing quality wine brands to different clients across the

globe. In other words, Treasury Wine Estate is an integrated wine firm focused on

premiumisation which is mostly supported by innovation as well as optimised brand. The

company is also committed to making some positive contributions to local communities

where it operates. Its mission is to be recognized as world’s most celebrated and successful

wine firm.

ii) Treasury Wine Estate’s Corporate Strategies

Treasury Wine Estate corporate strategies include building high performing firm by driving a

supportive, collaborative and inclusive culture. It also comprises of development of long-term

relationship through connecting with its clients, partnering with chief clients in growing its

wine category as well as driving performance for all its stakeholders. Another corporate

strategy by Treasury Wine Estate includes optimizing its capital base. This is to be achieved

by operating safely, responsibly and sustainably, creating supplying chain cost as well as

quality advantages. It is also accomplished by simplifying it processes and addressing high

cost structures. Besides, the company identifies the means it could improve the contributions

character and therefore the firm does not make similar profit from every client (Angelopoulos

& Pollalis 2017).

B) How ABC Model Aligns With the Current Goals and Strategies of Treasury Wine

Estate

i) Treasury Wine Estate’s Mission and Objectives

Treasury Wine Estate is the largest wine firms across the globe which is listed in ASX. The

firms is mostly focused on delivering high quality shareholders’ value vial production of

quality products and selling and marketing quality wine brands to different clients across the

globe. In other words, Treasury Wine Estate is an integrated wine firm focused on

premiumisation which is mostly supported by innovation as well as optimised brand. The

company is also committed to making some positive contributions to local communities

where it operates. Its mission is to be recognized as world’s most celebrated and successful

wine firm.

ii) Treasury Wine Estate’s Corporate Strategies

Treasury Wine Estate corporate strategies include building high performing firm by driving a

supportive, collaborative and inclusive culture. It also comprises of development of long-term

relationship through connecting with its clients, partnering with chief clients in growing its

wine category as well as driving performance for all its stakeholders. Another corporate

strategy by Treasury Wine Estate includes optimizing its capital base. This is to be achieved

by operating safely, responsibly and sustainably, creating supplying chain cost as well as

quality advantages. It is also accomplished by simplifying it processes and addressing high

cost structures. Besides, the company identifies the means it could improve the contributions

Managerial Accounting 9

to local communities by managing social and environmental risks as well as driving

sustainability.

iii) How ABC Model Assist in Achieving Treasury Wine Estate’s Strategies

The main objective and mission of the ABC is mainly to enhance organization’s management

decision-making through development of robust programs across the company with

sustainable data, reports, methodology and analyses. Besides, ABC assist in achievement of

higher quality services and products to the external and internal clients while driving toward a

more effective production of services and goods as well as more efficient performance of the

company’s activities.

C) Recommendations of on Implementation of ABC

Based on the company’s main objectives, it is recommended that Treasury Wine Estate should

make use of the ABC. This is based on the notion that ABC could assist in achievement of

higher quality services and products to the external and internal clients while driving toward a

more effective production of services and goods as well as more efficient performance of the

company’s activities. Furthermore, ABC assigns costs to different cost objects on the basis of

the use of the activities and assigns different costs to their activities on the basis of the use of

different resources.

d) Other Management Accounting Tool That is Suitable for Treasury Wine Estate

Other than the ABC, Treasury Wine Estate should utilize balanced scorecard as one of the

most suitable management accounting tools. This is based on the fact that BSC could assist

the company in addressing inadequacies of the performance measurement (Angelis & Lee

to local communities by managing social and environmental risks as well as driving

sustainability.

iii) How ABC Model Assist in Achieving Treasury Wine Estate’s Strategies

The main objective and mission of the ABC is mainly to enhance organization’s management

decision-making through development of robust programs across the company with

sustainable data, reports, methodology and analyses. Besides, ABC assist in achievement of

higher quality services and products to the external and internal clients while driving toward a

more effective production of services and goods as well as more efficient performance of the

company’s activities.

C) Recommendations of on Implementation of ABC

Based on the company’s main objectives, it is recommended that Treasury Wine Estate should

make use of the ABC. This is based on the notion that ABC could assist in achievement of

higher quality services and products to the external and internal clients while driving toward a

more effective production of services and goods as well as more efficient performance of the

company’s activities. Furthermore, ABC assigns costs to different cost objects on the basis of

the use of the activities and assigns different costs to their activities on the basis of the use of

different resources.

d) Other Management Accounting Tool That is Suitable for Treasury Wine Estate

Other than the ABC, Treasury Wine Estate should utilize balanced scorecard as one of the

most suitable management accounting tools. This is based on the fact that BSC could assist

the company in addressing inadequacies of the performance measurement (Angelis & Lee

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 10

1996). Besides, the BSC could assist Treasury Wine Estate in improving its decision-making

by utilizing both non-financial and financial measures and could also improve its

performance. This is based on the notion that the BSC emphasise needs of giving the

company suitable information in addressing all its applicable areas of the performance in a

manner that is unbiased and objective, to help the management in accomplishing and

formulating the strategic policies (Anand, Sahay & Saha 2005). In essence, employment of

the BSC would help Treasury Wine Estate in improving it strategies, resulting in improved

financial and economic performance. Furthermore, the BSC could assist the company by

offering sustainable information for their decision-making by setting clear objectives and

targets that might in turn assist in improving the company’s financial performance. Besides,

BSC comprises of tools which are significant for the company management since it

increases probability of a successful introduction of the strategy and accomplishment of the

business objectives and goals (Angelis & Lee 1996). BSC would also assist the company in

aligning the non-financial and financial measures which might in turn permit the

organization’s management in overviewing existing situation and then present innovative

perspective which could be utilized in interpreting different strategies for the growth into the

operative terms that the management is in a position to review financial performance in

numerous segments concurrently. It would also assist the company to continue improving

and creating value since it result in learning and innovative perspective where future succeed

today (Anand, Sahay & Saha 2005).

Conclusion

In conclusion, Treasury Wine Estate can utilize ABC in replacing it current standard costing,

since the model could assist the firm achieve it key objectives. Basically, increasing

profitability or improving financial performance is a complex thing for any firm, which has

1996). Besides, the BSC could assist Treasury Wine Estate in improving its decision-making

by utilizing both non-financial and financial measures and could also improve its

performance. This is based on the notion that the BSC emphasise needs of giving the

company suitable information in addressing all its applicable areas of the performance in a

manner that is unbiased and objective, to help the management in accomplishing and

formulating the strategic policies (Anand, Sahay & Saha 2005). In essence, employment of

the BSC would help Treasury Wine Estate in improving it strategies, resulting in improved

financial and economic performance. Furthermore, the BSC could assist the company by

offering sustainable information for their decision-making by setting clear objectives and

targets that might in turn assist in improving the company’s financial performance. Besides,

BSC comprises of tools which are significant for the company management since it

increases probability of a successful introduction of the strategy and accomplishment of the

business objectives and goals (Angelis & Lee 1996). BSC would also assist the company in

aligning the non-financial and financial measures which might in turn permit the

organization’s management in overviewing existing situation and then present innovative

perspective which could be utilized in interpreting different strategies for the growth into the

operative terms that the management is in a position to review financial performance in

numerous segments concurrently. It would also assist the company to continue improving

and creating value since it result in learning and innovative perspective where future succeed

today (Anand, Sahay & Saha 2005).

Conclusion

In conclusion, Treasury Wine Estate can utilize ABC in replacing it current standard costing,

since the model could assist the firm achieve it key objectives. Basically, increasing

profitability or improving financial performance is a complex thing for any firm, which has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 11

numerous aspects require to be considered. The ABC could assist Treasury Wine Estate

making more profits that could in turn assist in improving its profitability and sales level.

Furthermore, given the ABC would be of greater importance to Treasury Wine Estate, there

is need to also implement BSC. This is based on the fact that BSC could assist the company

in addressing inadequacies of the performance measurement. Besides, BSC is said to assist

Treasury Wine Estate in improving its decision-making by utilizing both non-financial and

financial measures and could also improve its performance. Additionally, BSC is also found

to assist the company in aligning the non-financial and financial measures which might in

turn permit the organization’s management in overviewing existing situation.

numerous aspects require to be considered. The ABC could assist Treasury Wine Estate

making more profits that could in turn assist in improving its profitability and sales level.

Furthermore, given the ABC would be of greater importance to Treasury Wine Estate, there

is need to also implement BSC. This is based on the fact that BSC could assist the company

in addressing inadequacies of the performance measurement. Besides, BSC is said to assist

Treasury Wine Estate in improving its decision-making by utilizing both non-financial and

financial measures and could also improve its performance. Additionally, BSC is also found

to assist the company in aligning the non-financial and financial measures which might in

turn permit the organization’s management in overviewing existing situation.

Managerial Accounting 12

References

Anand, M, Sahay, BS & Saha, S 2005, Activity-based cost management practices in India:

An empirical study.

International Journal of Economics and Financial Issues,

7(3), 586-593.

Angelis, DI & Lee, CY 1996, ‘Strategic investment analysis using activity based costing

concepts and analytical hierarchy process techniques,’ International Journal of Production

Research, 34(5), 1331-1345.

Angelopoulos, M & Pollalis, Y 2017, Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Bufi, E & Moilanen, S 2014, ‘Designing An Activity-Based Costing System for A Specialty

Retail Store,’ Unpublished Master‘s Thesis, Oulu Business School Department of

Accounting, Finlandiya.

Innes, J & Kouhy, R 2011, ‘The Activity-Based Approach,’ In Review of Management

Accounting Research (pp. 243-274). Palgrave Macmillan, London.

Israelsen, P 1994, ‘ABC and variability accounting differences and potential benefits of

integration,’ European Accounting Review, 3(1), 15-47.

Pineno, CJ 2002, ‘The balanced scorecard with time-driven activity basedcosting: An

incremental approach model to health care cost management,’ J Health Care Finance, 28(4),

69-80.

Oseifuah, EK 2018, ‘Activity based costing (ABC) in the public sector: benefits and

challenges,’ Management, 12, 4-2.

References

Anand, M, Sahay, BS & Saha, S 2005, Activity-based cost management practices in India:

An empirical study.

International Journal of Economics and Financial Issues,

7(3), 586-593.

Angelis, DI & Lee, CY 1996, ‘Strategic investment analysis using activity based costing

concepts and analytical hierarchy process techniques,’ International Journal of Production

Research, 34(5), 1331-1345.

Angelopoulos, M & Pollalis, Y 2017, Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Bufi, E & Moilanen, S 2014, ‘Designing An Activity-Based Costing System for A Specialty

Retail Store,’ Unpublished Master‘s Thesis, Oulu Business School Department of

Accounting, Finlandiya.

Innes, J & Kouhy, R 2011, ‘The Activity-Based Approach,’ In Review of Management

Accounting Research (pp. 243-274). Palgrave Macmillan, London.

Israelsen, P 1994, ‘ABC and variability accounting differences and potential benefits of

integration,’ European Accounting Review, 3(1), 15-47.

Pineno, CJ 2002, ‘The balanced scorecard with time-driven activity basedcosting: An

incremental approach model to health care cost management,’ J Health Care Finance, 28(4),

69-80.

Oseifuah, EK 2018, ‘Activity based costing (ABC) in the public sector: benefits and

challenges,’ Management, 12, 4-2.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.