Project 1: Absorption Costing, Activity-Based Costing, and BEP

VerifiedAdded on 2023/01/11

|11

|3596

|69

Project

AI Summary

This project delves into the core concepts of financial analysis, focusing on costing methods and break-even analysis. Part A of the project begins with an examination of absorption costing, detailing its calculation and application in determining product costs. It then transitions to activity-based costing, illustrating its method for assigning overhead and indirect costs based on activities. The project includes a critical discussion comparing the advantages and disadvantages of both costing methods. Part B centers on the break-even point (BEP), explaining its significance in business operations. The project outlines the BEP formula, explores its variable aspects (fixed costs, variable costs, contribution margin, and revenue), and highlights its importance for business planning, performance monitoring, and strategic decision-making. The project concludes by emphasizing the critical significance of BEP in identifying the number of products to be sold to cover costs and achieve profitability.

PROJECT

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of absorption costing...........................................................................................3

Calculation of activity based cost...........................................................................................4

Critical discussion of methods of costing...............................................................................4

PART B...........................................................................................................................................5

Break Even Point and its Significance...................................................................................5

CONCLUSION...............................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of absorption costing...........................................................................................3

Calculation of activity based cost...........................................................................................4

Critical discussion of methods of costing...............................................................................4

PART B...........................................................................................................................................5

Break Even Point and its Significance...................................................................................5

CONCLUSION...............................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION

Break even point is the point which used to define a point where total cost incurred by the

company and total sales are equal. Break even analysis is also define as a business tool which

used to help the different industry to explain business operation in terms of the cost. This report

used to highlights the absorption cost for each type of stove in the organization. After that the

report highlights activity based cost for each type of stove in the organization. In the end the

report highlights the discussion about the above method of the costing in the organization. After

that the report highlights importance of BEP for the organization and different critical

significance of BEP for the organization.

PART A

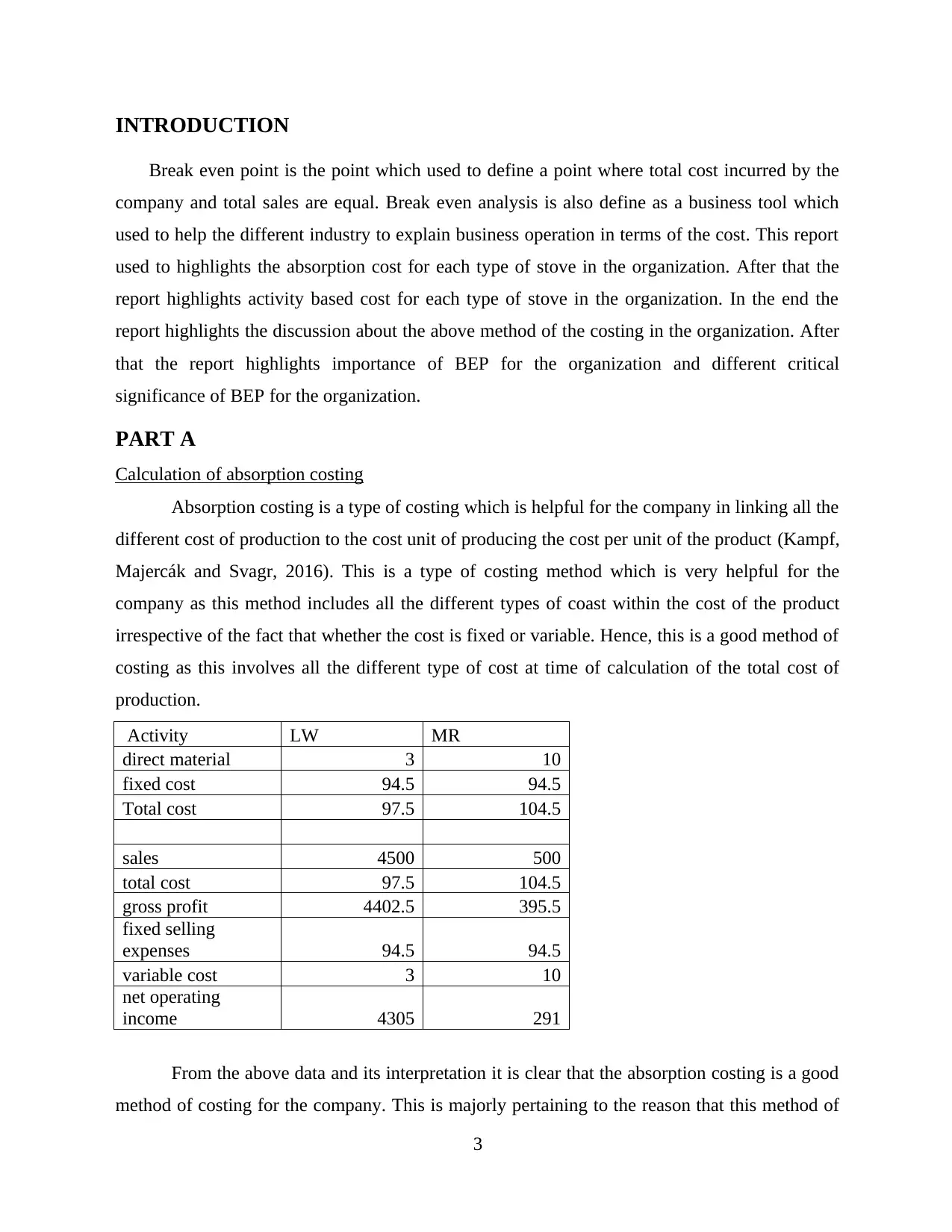

Calculation of absorption costing

Absorption costing is a type of costing which is helpful for the company in linking all the

different cost of production to the cost unit of producing the cost per unit of the product (Kampf,

Majercák and Svagr, 2016). This is a type of costing method which is very helpful for the

company as this method includes all the different types of coast within the cost of the product

irrespective of the fact that whether the cost is fixed or variable. Hence, this is a good method of

costing as this involves all the different type of cost at time of calculation of the total cost of

production.

Activity LW MR

direct material 3 10

fixed cost 94.5 94.5

Total cost 97.5 104.5

sales 4500 500

total cost 97.5 104.5

gross profit 4402.5 395.5

fixed selling

expenses 94.5 94.5

variable cost 3 10

net operating

income 4305 291

From the above data and its interpretation it is clear that the absorption costing is a good

method of costing for the company. This is majorly pertaining to the reason that this method of

3

Break even point is the point which used to define a point where total cost incurred by the

company and total sales are equal. Break even analysis is also define as a business tool which

used to help the different industry to explain business operation in terms of the cost. This report

used to highlights the absorption cost for each type of stove in the organization. After that the

report highlights activity based cost for each type of stove in the organization. In the end the

report highlights the discussion about the above method of the costing in the organization. After

that the report highlights importance of BEP for the organization and different critical

significance of BEP for the organization.

PART A

Calculation of absorption costing

Absorption costing is a type of costing which is helpful for the company in linking all the

different cost of production to the cost unit of producing the cost per unit of the product (Kampf,

Majercák and Svagr, 2016). This is a type of costing method which is very helpful for the

company as this method includes all the different types of coast within the cost of the product

irrespective of the fact that whether the cost is fixed or variable. Hence, this is a good method of

costing as this involves all the different type of cost at time of calculation of the total cost of

production.

Activity LW MR

direct material 3 10

fixed cost 94.5 94.5

Total cost 97.5 104.5

sales 4500 500

total cost 97.5 104.5

gross profit 4402.5 395.5

fixed selling

expenses 94.5 94.5

variable cost 3 10

net operating

income 4305 291

From the above data and its interpretation it is clear that the absorption costing is a good

method of costing for the company. This is majorly pertaining to the reason that this method of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing involves all the cost whether be it fixed cost or the variable cost. This involves all the

cost and because of this no cost is being left unturned and is included in the calculation of the

total cost of production. Thus, this includes all the cost and here the income is calculated by

totalling all the cost and then deducting it from the total sales of the company. Thus, if the total

sales are more than the total cost then this is called the profit for the company.

On the other hand if the total cost is more than the total sales then this is called the loss

for the company and this is necessary to know for the company (Gersil and Kayal, 2016). This is

majorly pertaining to the fact that if the company is suffering from losses then the company will

have to make the strategies in order to improve the performance and sales of the company. On

the flip side if the company is earning good amount of profit then the company have to make

strategies in order to sustain and maintain that level of profitability always and other strategies in

increasing the level of profit to more high.

Calculation of activity based cost

The activity based costing is a type of method which includes the assigning of the

overhead and the indirect cost over the cost of the product or the services. This is a system of

cost accounting which includes the costing done on basis of different activities which are

involved in the production process. Under this system the cost is assigned to every activity

involved in the whole production process.

Activity LW MR

Purchasing 55.56 500

Training 50 33.33

Setting up

machines 37.5 75

Running machines 0.21 1.9

From the above discussion it is clear that the activity based costing is very helpful as this

help the company in assessing that in each of the activity of production how much cost is being

incurred. With the help of this method it was clear that in purchasing activity the total cost is

55.56 in case of LW and 500 in case of MR. In the same way for training in LW 50 and in MR

33.33 but in setting up machines the cost in LW is 37.5 and in MR it is 75. In the end in case of

running the machines the cost is 0.21 in case of LW and 1.9 in case of MR.

4

cost and because of this no cost is being left unturned and is included in the calculation of the

total cost of production. Thus, this includes all the cost and here the income is calculated by

totalling all the cost and then deducting it from the total sales of the company. Thus, if the total

sales are more than the total cost then this is called the profit for the company.

On the other hand if the total cost is more than the total sales then this is called the loss

for the company and this is necessary to know for the company (Gersil and Kayal, 2016). This is

majorly pertaining to the fact that if the company is suffering from losses then the company will

have to make the strategies in order to improve the performance and sales of the company. On

the flip side if the company is earning good amount of profit then the company have to make

strategies in order to sustain and maintain that level of profitability always and other strategies in

increasing the level of profit to more high.

Calculation of activity based cost

The activity based costing is a type of method which includes the assigning of the

overhead and the indirect cost over the cost of the product or the services. This is a system of

cost accounting which includes the costing done on basis of different activities which are

involved in the production process. Under this system the cost is assigned to every activity

involved in the whole production process.

Activity LW MR

Purchasing 55.56 500

Training 50 33.33

Setting up

machines 37.5 75

Running machines 0.21 1.9

From the above discussion it is clear that the activity based costing is very helpful as this

help the company in assessing that in each of the activity of production how much cost is being

incurred. With the help of this method it was clear that in purchasing activity the total cost is

55.56 in case of LW and 500 in case of MR. In the same way for training in LW 50 and in MR

33.33 but in setting up machines the cost in LW is 37.5 and in MR it is 75. In the end in case of

running the machines the cost is 0.21 in case of LW and 1.9 in case of MR.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Critical discussion of methods of costing

In the words of Nasution and Pramana, (2019) the major advantage of using the

absorption costing is that this method includes the fixed expenses and fixed cost as well which is

not done in other costing methods. The price which is being set on the basis of the absorption

costing makes sure that all the different cost are being added within the price which is being

charged to the consumers. But the major difficulty in this type of method of costing is that this is

not much helpful in managing and taking decision relating to the management of the company.

This is necessary because of the fact that this method of costing does not involves the selection

of different types of the product mix or the decision that which manufacturer must be used for

taking the supplies for the company.

On the other hand the other method of costing that is activity based casting is also a very

good method calculating the cost for the company. This is majorly pertaining to the major

advantage of this method which is that this method allocates the cost to each and every activity

of the company which is included in the manufacturing process of the company. Thus, this

involves the calculation of all the activities of the business and not a single activity is left.

On the other side the major disadvantage of the company is that this type of costing is

very time consuming. This is majorly pertaining to the fact that assigning activities to each of

the business activity is that this includes a lot of time in first analysing and evaluating all the

activities involved within the business (Hazra, Pandey and Manzana, 2020). Further after that

each of this activity is analysed and in accordance to the requirement the cost is being allocated

to all the activities. Thus, all these steps involves a lot of time and this increases the process of

calculating the cost on basis of the activity based costing method.

PART B

Break Even Point and its Significance

Break even point is the point which used to define a point where total cost incurred by the

company and total sales are equal. Break even analysis is also define as a business tool which

used to help the different industry to explain business operation in terms of the cost. This is the

point which is generally known as no profit and no loss point (Kim and et.al., 2017). One of the

economist in his published paper used to define used to published that Break even point is the

method which used to define the relationship between the cost, revenue and profit of the

business at different level of the output in the nation. It generally help in determining the point in

5

In the words of Nasution and Pramana, (2019) the major advantage of using the

absorption costing is that this method includes the fixed expenses and fixed cost as well which is

not done in other costing methods. The price which is being set on the basis of the absorption

costing makes sure that all the different cost are being added within the price which is being

charged to the consumers. But the major difficulty in this type of method of costing is that this is

not much helpful in managing and taking decision relating to the management of the company.

This is necessary because of the fact that this method of costing does not involves the selection

of different types of the product mix or the decision that which manufacturer must be used for

taking the supplies for the company.

On the other hand the other method of costing that is activity based casting is also a very

good method calculating the cost for the company. This is majorly pertaining to the major

advantage of this method which is that this method allocates the cost to each and every activity

of the company which is included in the manufacturing process of the company. Thus, this

involves the calculation of all the activities of the business and not a single activity is left.

On the other side the major disadvantage of the company is that this type of costing is

very time consuming. This is majorly pertaining to the fact that assigning activities to each of

the business activity is that this includes a lot of time in first analysing and evaluating all the

activities involved within the business (Hazra, Pandey and Manzana, 2020). Further after that

each of this activity is analysed and in accordance to the requirement the cost is being allocated

to all the activities. Thus, all these steps involves a lot of time and this increases the process of

calculating the cost on basis of the activity based costing method.

PART B

Break Even Point and its Significance

Break even point is the point which used to define a point where total cost incurred by the

company and total sales are equal. Break even analysis is also define as a business tool which

used to help the different industry to explain business operation in terms of the cost. This is the

point which is generally known as no profit and no loss point (Kim and et.al., 2017). One of the

economist in his published paper used to define used to published that Break even point is the

method which used to define the relationship between the cost, revenue and profit of the

business at different level of the output in the nation. It generally help in determining the point in

5

the operation where revenue of the business equals to the cost of the business in the long run. As

break even point used to consider the both type of the cost in the organization.

Formula of Break Even Analysis

To calculate the Break even point of the business, organization generally used to use the

common formula that is Break-Even point(units) = Fixed Costs ÷ (Sales price per unit –

Variable costs per unit) or in sales dollars using the formula: Break-Even point (sales dollars)

= Fixed Costs ÷ Contribution Margin (Vadrale and Katti, 2018).

Different variable aspect of BEP is as follows:

Fixed cost is the cost which is fixed in the nature; this is the costs which do not used to change

with the change in the output of the organization. Variable cost is the cost which used to change

with change in the number of the output in the organization. Contribution margin is generally

calculated in the organization on the basis of the subtracting the variable expenses from the

revenue. Contributing margin generally shows that how much of this contribution will be used in

the organization to cover the fixed cost of the company in the long run. It is generally calculated

on the basis of percentage as well as on net sales basis in the organization. Revenue is the money

that business actually receive from the customer at the time for providing the service and

product to the customer in the market (Kim and et.al., 2017).

It is very important for all the business to calculate Breakeven point in the 21st century as

well, as it has been find out that Break even point used to bring the variety of the significance for

the organization in the real worlds. There are many different importances which are brought by

break even analysis for the business. There are many draw back of the same also for the

organization but before that it will be better to understand the requirement of Break even

analysis in the organization. Some of the requirements are as follows:

Business Plan making: Business Plan making is the first requirement of Break even

analysis in the organization. As Break even Analysis in the organization used to determine the

cost structure of the company and also help the company in understanding number of unit which

needs to be sold by the company to earn good amount of the profit from the market. As a result

it is require in the organization to conduct and build good business plan to see how practical is

the business idea and on the basis of the same it has been analyzed that whether or not

6

break even point used to consider the both type of the cost in the organization.

Formula of Break Even Analysis

To calculate the Break even point of the business, organization generally used to use the

common formula that is Break-Even point(units) = Fixed Costs ÷ (Sales price per unit –

Variable costs per unit) or in sales dollars using the formula: Break-Even point (sales dollars)

= Fixed Costs ÷ Contribution Margin (Vadrale and Katti, 2018).

Different variable aspect of BEP is as follows:

Fixed cost is the cost which is fixed in the nature; this is the costs which do not used to change

with the change in the output of the organization. Variable cost is the cost which used to change

with change in the number of the output in the organization. Contribution margin is generally

calculated in the organization on the basis of the subtracting the variable expenses from the

revenue. Contributing margin generally shows that how much of this contribution will be used in

the organization to cover the fixed cost of the company in the long run. It is generally calculated

on the basis of percentage as well as on net sales basis in the organization. Revenue is the money

that business actually receive from the customer at the time for providing the service and

product to the customer in the market (Kim and et.al., 2017).

It is very important for all the business to calculate Breakeven point in the 21st century as

well, as it has been find out that Break even point used to bring the variety of the significance for

the organization in the real worlds. There are many different importances which are brought by

break even analysis for the business. There are many draw back of the same also for the

organization but before that it will be better to understand the requirement of Break even

analysis in the organization. Some of the requirements are as follows:

Business Plan making: Business Plan making is the first requirement of Break even

analysis in the organization. As Break even Analysis in the organization used to determine the

cost structure of the company and also help the company in understanding number of unit which

needs to be sold by the company to earn good amount of the profit from the market. As a result

it is require in the organization to conduct and build good business plan to see how practical is

the business idea and on the basis of the same it has been analyzed that whether or not

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization should follow the plan in the organization. As All the organization always look for

the idea which used to give as low as break even point to be achieved by the organization.

Performance Monitoring and Analysis: Break even analysis in the organization also

require to analysis to monitor the different performance in the organization. Break even analysis

used to help the organization in setting up different backyard stick to compare the performance

of the business in the market. As organization used to compare the original performance of the

business with the backyard which is set up by the organization in the market, this eventually

help them in determining the future performance of the business in the market, as with the help

of analysing and monitoring the performance of the business in the market, organization used to

make different policy in the organization to carry out. So it can be said that BEP is require in the

organization to analysis the performance of the business in long run.

Critical significance of Break even Analysis

Breakeven analysis helps in identify the number of products to be sold to cover the cost

of different raw material which are being invested in the organization. It help the business in

collecting information regarding the number of unit to be sold which help in collecting the

minimum profits. For evaluate breakeven analysis, variable price and selling price are required.

As having information of minimum unit to be sold organization generally finds it easy to plan

the different activity to be done in the organization. At the same time it has been analysed that

Calculating Break even point in the organization does not grantee the success for the business, as

it has been seen that it require a good amount of the efforts to be invested by the organization to

find out the break even point of the business but it does not grantee the success for the

organization, as it is just a base (Kampf, Majerčák and Švagr, 2016). On the basis of the same

different activity are planned in the organization so it can be said that Break even point is just a

basis; it does not grantee the success in the organization.

Breakeven analysis helps manager in fixing the selling target and accordingly provide

budget to each organizational departments as they known how many product should be sold

cover the cost. In simple words it can be said that BEP in the organization used to help the

company in maintaining the cost structure of the company. At the same time it has been also find

out that BEP only includes the quantitative data, it does not used to consider the qualitative

aspect in the organization. As it has been find out that factor like customer building and good

7

the idea which used to give as low as break even point to be achieved by the organization.

Performance Monitoring and Analysis: Break even analysis in the organization also

require to analysis to monitor the different performance in the organization. Break even analysis

used to help the organization in setting up different backyard stick to compare the performance

of the business in the market. As organization used to compare the original performance of the

business with the backyard which is set up by the organization in the market, this eventually

help them in determining the future performance of the business in the market, as with the help

of analysing and monitoring the performance of the business in the market, organization used to

make different policy in the organization to carry out. So it can be said that BEP is require in the

organization to analysis the performance of the business in long run.

Critical significance of Break even Analysis

Breakeven analysis helps in identify the number of products to be sold to cover the cost

of different raw material which are being invested in the organization. It help the business in

collecting information regarding the number of unit to be sold which help in collecting the

minimum profits. For evaluate breakeven analysis, variable price and selling price are required.

As having information of minimum unit to be sold organization generally finds it easy to plan

the different activity to be done in the organization. At the same time it has been analysed that

Calculating Break even point in the organization does not grantee the success for the business, as

it has been seen that it require a good amount of the efforts to be invested by the organization to

find out the break even point of the business but it does not grantee the success for the

organization, as it is just a base (Kampf, Majerčák and Švagr, 2016). On the basis of the same

different activity are planned in the organization so it can be said that Break even point is just a

basis; it does not grantee the success in the organization.

Breakeven analysis helps manager in fixing the selling target and accordingly provide

budget to each organizational departments as they known how many product should be sold

cover the cost. In simple words it can be said that BEP in the organization used to help the

company in maintaining the cost structure of the company. At the same time it has been also find

out that BEP only includes the quantitative data, it does not used to consider the qualitative

aspect in the organization. As it has been find out that factor like customer building and good

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will which are not seen by break even analysis in the organization this eventually used to create

the variety of the issue for the organization to overcome.

Breakeven analysis help in determining the margin of safety as manager already known

the number of unit to be sold to generate minimum profit which made it easier for them to take

appropriate decisions and strategies to cover cost (Batkovskiy and et.al., 2017). This eventually

used to help the company in increasing the efficiency of the business in the long run as duplicity

of work is generally reduced in the organization. At the same it has been analysed that any

wrong calculation of BEP in the organization lead to very bad impact on the performance of the

business in the long run. As it has been analysis that wrong interpretation of BEP in the

organization leads to wrong formulation of variety of the strategy as well. This used to impact

the performance of the business in the long run.

Break even analysis made it easier for managers to identify the reason behind any

decrease in profit or increase in any type of cost as it analysis both variables and fixed cost. This

eventually used to help the manager in managing the different activity very easily and planning

different activity in organization in a way that future outcome can be predicted that easily in the

market. At the same it has been analysed that BEP in the organization used to help the company

in knowing the decrease in the profit but it used to not show the way to rectify the same in the

organization. So it can be said that it is incomplete analysis as compare to the another (Lee and

et.al., 2018).

Pricing strategies change according to change in breakeven point. For example fewer

units will be sold if selling price increases and more units will sold if selling price reduces to

attain breakeven analysis. This is majorly because of the reason that if the selling price of the

goods and services will be low then the consumers will try to purchase more of the units. This

will not be in the case when the prices are high. Hence the low selling price will increase the

units to be sold by the company in case of the higher selling price. But if the company will lower

the prices to a great extent then this might also be a losing situation for the company. This is due

to the fact that if the selling price will be much low then it might be possible that the consumer

think that the goods and services are of low quality and this might reduce the sales of the

company. Thus, it is very essential for company to charge the selling price in such a manner that

this must return at least what is levied that the product or services must at least attain that much

of the amount which is incurred in producing the goods and services. Thus, the company has to

8

the variety of the issue for the organization to overcome.

Breakeven analysis help in determining the margin of safety as manager already known

the number of unit to be sold to generate minimum profit which made it easier for them to take

appropriate decisions and strategies to cover cost (Batkovskiy and et.al., 2017). This eventually

used to help the company in increasing the efficiency of the business in the long run as duplicity

of work is generally reduced in the organization. At the same it has been analysed that any

wrong calculation of BEP in the organization lead to very bad impact on the performance of the

business in the long run. As it has been analysis that wrong interpretation of BEP in the

organization leads to wrong formulation of variety of the strategy as well. This used to impact

the performance of the business in the long run.

Break even analysis made it easier for managers to identify the reason behind any

decrease in profit or increase in any type of cost as it analysis both variables and fixed cost. This

eventually used to help the manager in managing the different activity very easily and planning

different activity in organization in a way that future outcome can be predicted that easily in the

market. At the same it has been analysed that BEP in the organization used to help the company

in knowing the decrease in the profit but it used to not show the way to rectify the same in the

organization. So it can be said that it is incomplete analysis as compare to the another (Lee and

et.al., 2018).

Pricing strategies change according to change in breakeven point. For example fewer

units will be sold if selling price increases and more units will sold if selling price reduces to

attain breakeven analysis. This is majorly because of the reason that if the selling price of the

goods and services will be low then the consumers will try to purchase more of the units. This

will not be in the case when the prices are high. Hence the low selling price will increase the

units to be sold by the company in case of the higher selling price. But if the company will lower

the prices to a great extent then this might also be a losing situation for the company. This is due

to the fact that if the selling price will be much low then it might be possible that the consumer

think that the goods and services are of low quality and this might reduce the sales of the

company. Thus, it is very essential for company to charge the selling price in such a manner that

this must return at least what is levied that the product or services must at least attain that much

of the amount which is incurred in producing the goods and services. Thus, the company has to

8

charge the price in such a way that the company is in a situation where the company is in no

profit and no loss situation.

Also, it is said that the break even analysis help the company in managing and analysing

the relation between the changes taking place in the relationship between the fixed and variable

cost. This is majorly because of the reason that this relationship has a direct impact over the total

cost of the company. The major reason underlying this fact is that the fixed cost is same

throughout the whole process of production of the company but the variable cost is the one

which varies from the level of production. Thus, the variable cost is the one which is has a major

impact over the working of the total cost. It is so because of the fact that if the production will be

high then the variable cost will also be high and this will increase the total cost. On the other

side if the production is low then the variable cost will also be low and this will not incur high

cost of production for the company. But in both the cases the fixed cost is the same whether the

level of production is high or low it does not matter over the total cost.

CONCLUSION

In the end it is analysed and evaluated that managing the cost of the company is the most

important thing for the success of the company. This is majorly because of the fact that if the

cost will not be apportioned in proper manner then the company will not be able to earn good

amount of profit. Hence, it is necessary for company to manage all the different cost in effective

and efficient manner. In the present case this was earlier done with help of absorption costing

and further it was done with help of activity based costing. Further the report stated the

discussion on the break- even analysis and the critical evaluation of it. With the help of the

discussion and the critical evaluation it was clear that the break- even point is the one where the

company is in no profit and no loss situation.

9

profit and no loss situation.

Also, it is said that the break even analysis help the company in managing and analysing

the relation between the changes taking place in the relationship between the fixed and variable

cost. This is majorly because of the reason that this relationship has a direct impact over the total

cost of the company. The major reason underlying this fact is that the fixed cost is same

throughout the whole process of production of the company but the variable cost is the one

which varies from the level of production. Thus, the variable cost is the one which is has a major

impact over the working of the total cost. It is so because of the fact that if the production will be

high then the variable cost will also be high and this will increase the total cost. On the other

side if the production is low then the variable cost will also be low and this will not incur high

cost of production for the company. But in both the cases the fixed cost is the same whether the

level of production is high or low it does not matter over the total cost.

CONCLUSION

In the end it is analysed and evaluated that managing the cost of the company is the most

important thing for the success of the company. This is majorly because of the fact that if the

cost will not be apportioned in proper manner then the company will not be able to earn good

amount of profit. Hence, it is necessary for company to manage all the different cost in effective

and efficient manner. In the present case this was earlier done with help of absorption costing

and further it was done with help of activity based costing. Further the report stated the

discussion on the break- even analysis and the critical evaluation of it. With the help of the

discussion and the critical evaluation it was clear that the break- even point is the one where the

company is in no profit and no loss situation.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Kim, E. K and et.al., 2017. Retrospective analysis of the financial break-even point for

intrathecal morphine pump use in Korea. The Korean journal of pain. 30(4). p.272.

Vadrale, K. S. and Katti, V. P., 2018. Break-Even Point Analysis of Public and Private Banking

Business. Wealth: International Journal of Money, Banking & Finance. 7(3).

Kim, S. and et.al., 2017. Break-Even Point Analysis of Sodium-Cooled Fast Reactor Capital

Investment Cost Comparing the Direct Disposal Option and Pyro-Sodium-Cooled Fast

Reactor Nuclear Fuel Cycle Option in Korea. Sustainability. 9(9). p.1518.

Kampf, R., Majerčák, P. and Švagr, P., 2016. Application of break-even point analysis. NAŠE

MORE: znanstveno-stručni časopis za more i pomorstvo. 63(3 Special Issue), pp.126-

128.

Batkovskiy, A. M and et.al., 2017. Statistical simulation of the break-even point in the margin

analysis of the company. Journal of Applied Economic Sciences, Romania: European

Research Centre of Managerial Studies in Business Administration. 12(2). p.558.

Lee, M. and et.al., 2018. A break-even analysis and impact analysis of residential solar

photovoltaic systems considering state solar incentives. Technological and Economic

Development of Economy. 24(2). pp.358-382.

Kampf, R., Majercák, P. and Svagr, P., 2016. Application of Break-Even Point

Analysis/Primjena Break-Even Point analize. Nase More, 63(3), p.126.

Nasution, M. R. E. and Pramana, D., 2019. ALGORITHM DEVELOPMENT FOR BREAK-

EVEN ANALYSIS OF UNMANNED AERIAL VEHICLE. Angkasa: Jurnal Ilmiah

Bidang Teknologi. 11(2). pp.90-99.

Gersil, A. and Kayal, C., 2016. A Comparative Analysis of Normal Costing Method with Full

Costing and Variable Costing in Internal Reporting. International Journal of

Management. 7(3).

Hazra, I., Pandey, M.D. and Manzana, N., 2020. Approximate Bayesian computation (ABC)

method for estimating parameters of the gamma process using noisy data. Reliability

Engineering & System Safety. 198. p.106780.

10

Books and Journals

Kim, E. K and et.al., 2017. Retrospective analysis of the financial break-even point for

intrathecal morphine pump use in Korea. The Korean journal of pain. 30(4). p.272.

Vadrale, K. S. and Katti, V. P., 2018. Break-Even Point Analysis of Public and Private Banking

Business. Wealth: International Journal of Money, Banking & Finance. 7(3).

Kim, S. and et.al., 2017. Break-Even Point Analysis of Sodium-Cooled Fast Reactor Capital

Investment Cost Comparing the Direct Disposal Option and Pyro-Sodium-Cooled Fast

Reactor Nuclear Fuel Cycle Option in Korea. Sustainability. 9(9). p.1518.

Kampf, R., Majerčák, P. and Švagr, P., 2016. Application of break-even point analysis. NAŠE

MORE: znanstveno-stručni časopis za more i pomorstvo. 63(3 Special Issue), pp.126-

128.

Batkovskiy, A. M and et.al., 2017. Statistical simulation of the break-even point in the margin

analysis of the company. Journal of Applied Economic Sciences, Romania: European

Research Centre of Managerial Studies in Business Administration. 12(2). p.558.

Lee, M. and et.al., 2018. A break-even analysis and impact analysis of residential solar

photovoltaic systems considering state solar incentives. Technological and Economic

Development of Economy. 24(2). pp.358-382.

Kampf, R., Majercák, P. and Svagr, P., 2016. Application of Break-Even Point

Analysis/Primjena Break-Even Point analize. Nase More, 63(3), p.126.

Nasution, M. R. E. and Pramana, D., 2019. ALGORITHM DEVELOPMENT FOR BREAK-

EVEN ANALYSIS OF UNMANNED AERIAL VEHICLE. Angkasa: Jurnal Ilmiah

Bidang Teknologi. 11(2). pp.90-99.

Gersil, A. and Kayal, C., 2016. A Comparative Analysis of Normal Costing Method with Full

Costing and Variable Costing in Internal Reporting. International Journal of

Management. 7(3).

Hazra, I., Pandey, M.D. and Manzana, N., 2020. Approximate Bayesian computation (ABC)

method for estimating parameters of the gamma process using noisy data. Reliability

Engineering & System Safety. 198. p.106780.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.