Comparative Analysis of Absorption and Marginal Costing for JJB Sports

VerifiedAdded on 2020/12/09

|5

|1141

|330

Report

AI Summary

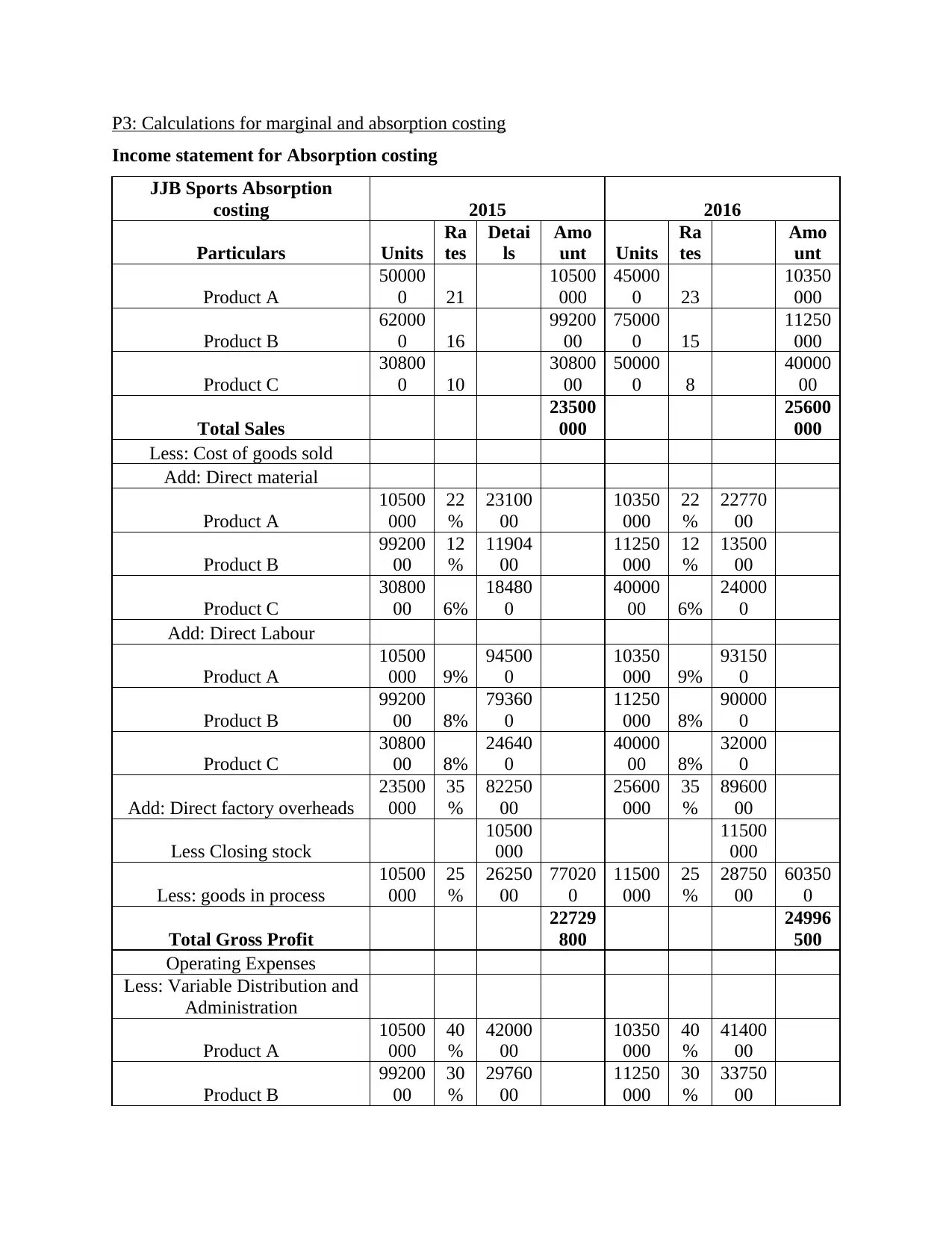

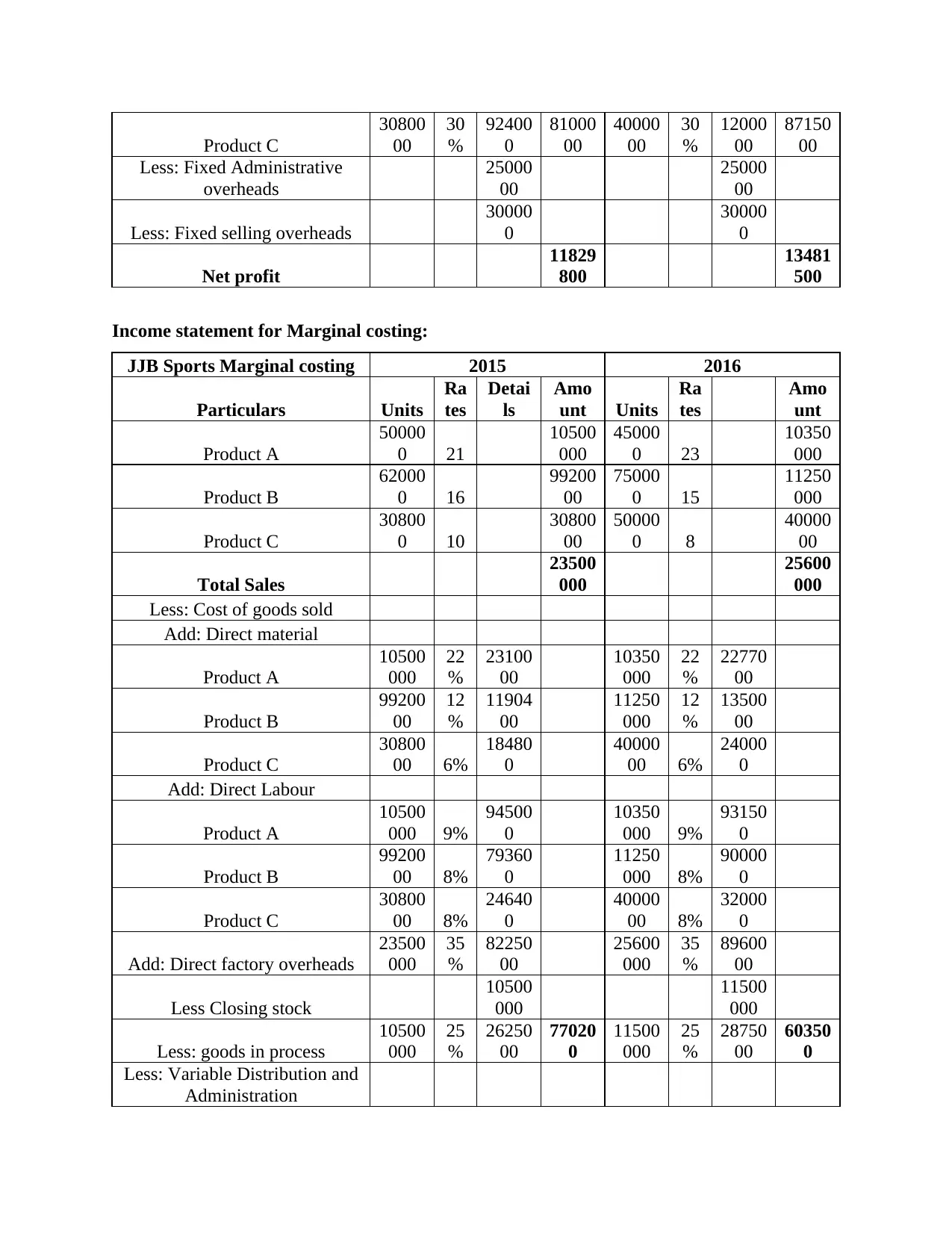

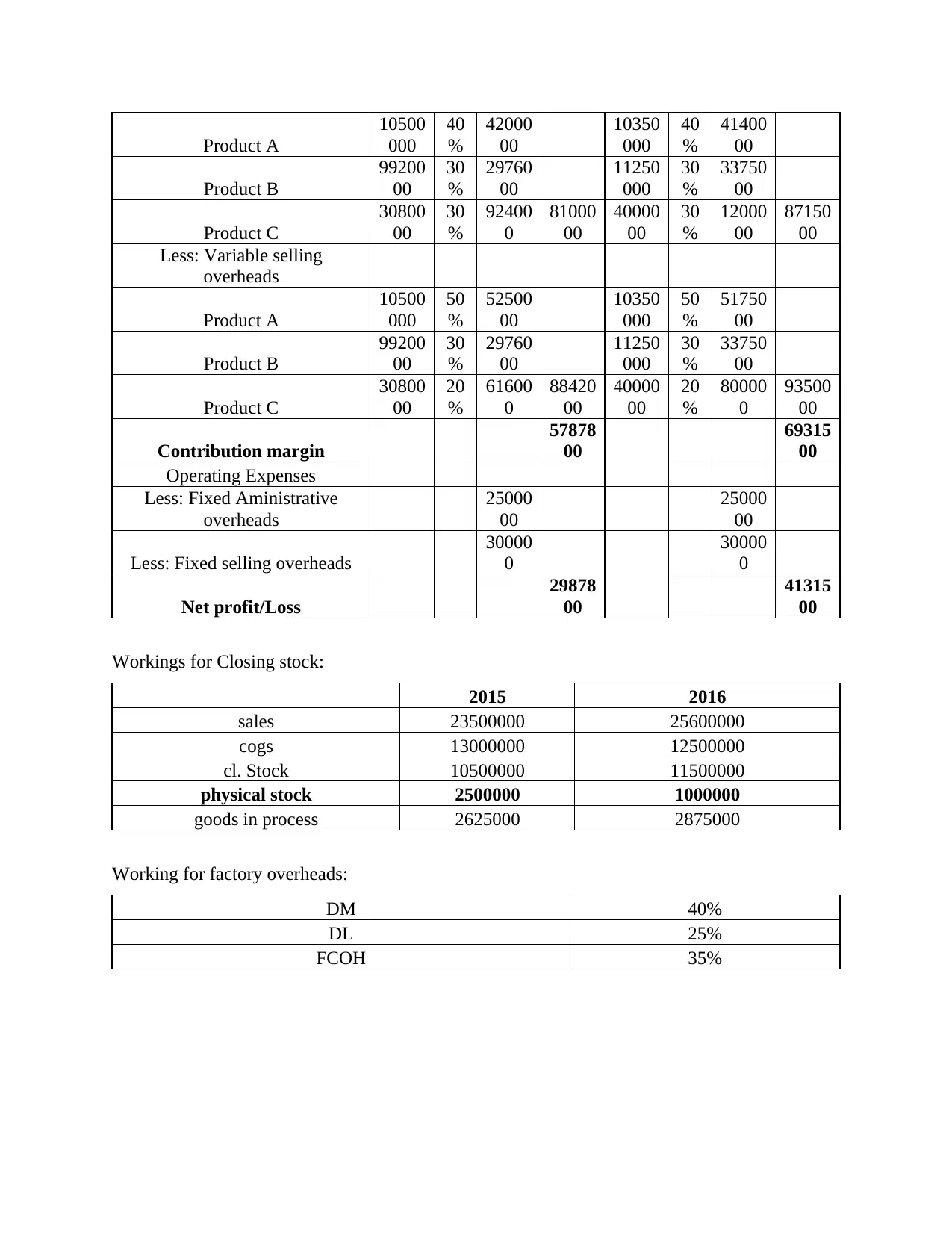

This report presents a comparative analysis of absorption and marginal costing methods, utilizing the financial data of JJB Sports for the years 2015 and 2016. The report begins with income statements prepared under both costing methods, detailing sales, cost of goods sold, direct materials, direct labor, factory overheads, and operating expenses. The analysis further breaks down the calculation of gross profit, contribution margin, and net profit under each method. The document includes detailed workings for closing stock and factory overheads. The report highlights the differences in profit calculation arising from the treatment of fixed manufacturing overheads, offering insights into how each method impacts financial reporting and decision-making. The report covers variable and fixed costs, and explains the differences in the presentation of financial results.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.