AC4052QA - Financial Accounting: Ratio Analysis, Ovid Ventures

VerifiedAdded on 2023/06/12

|11

|1894

|379

Report

AI Summary

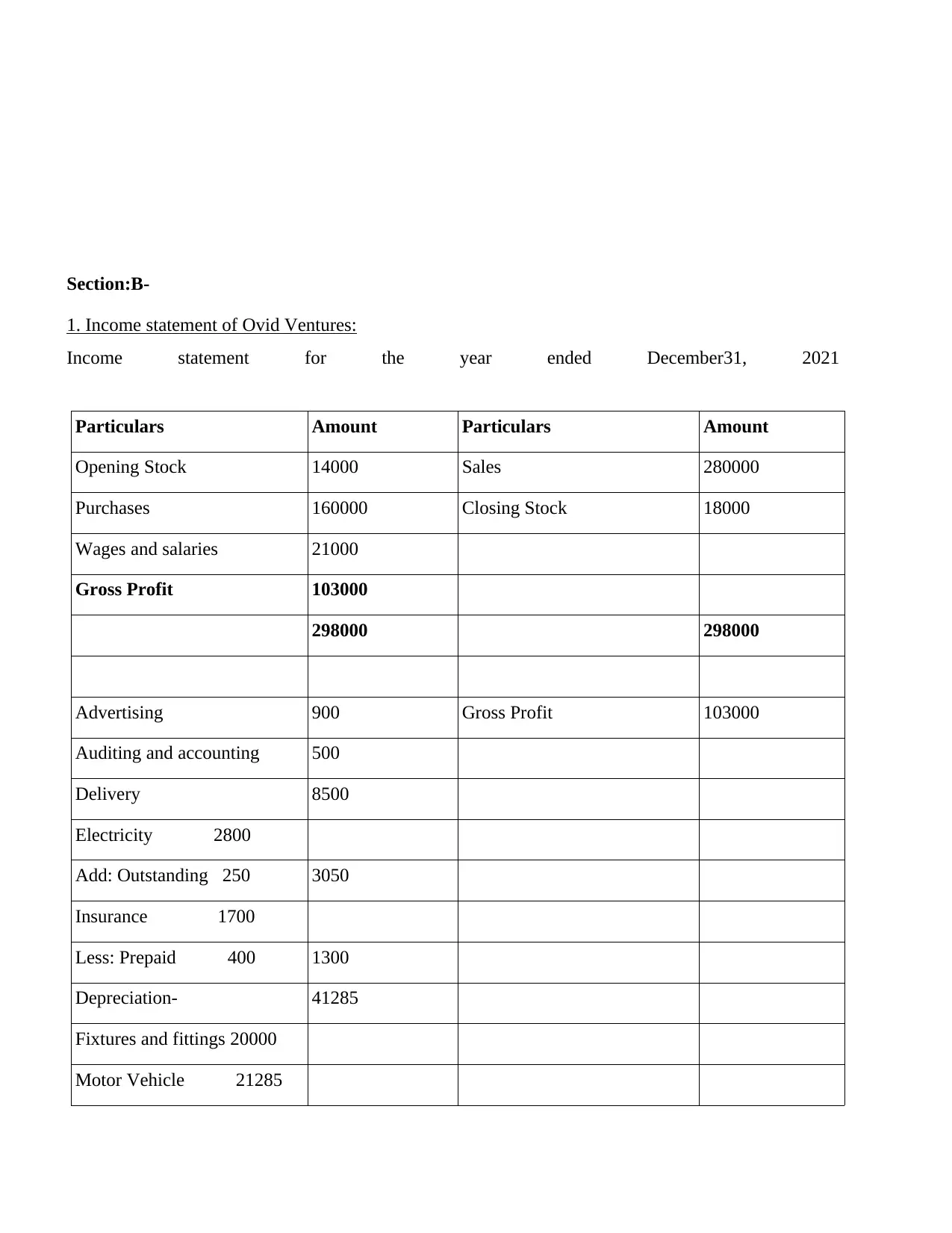

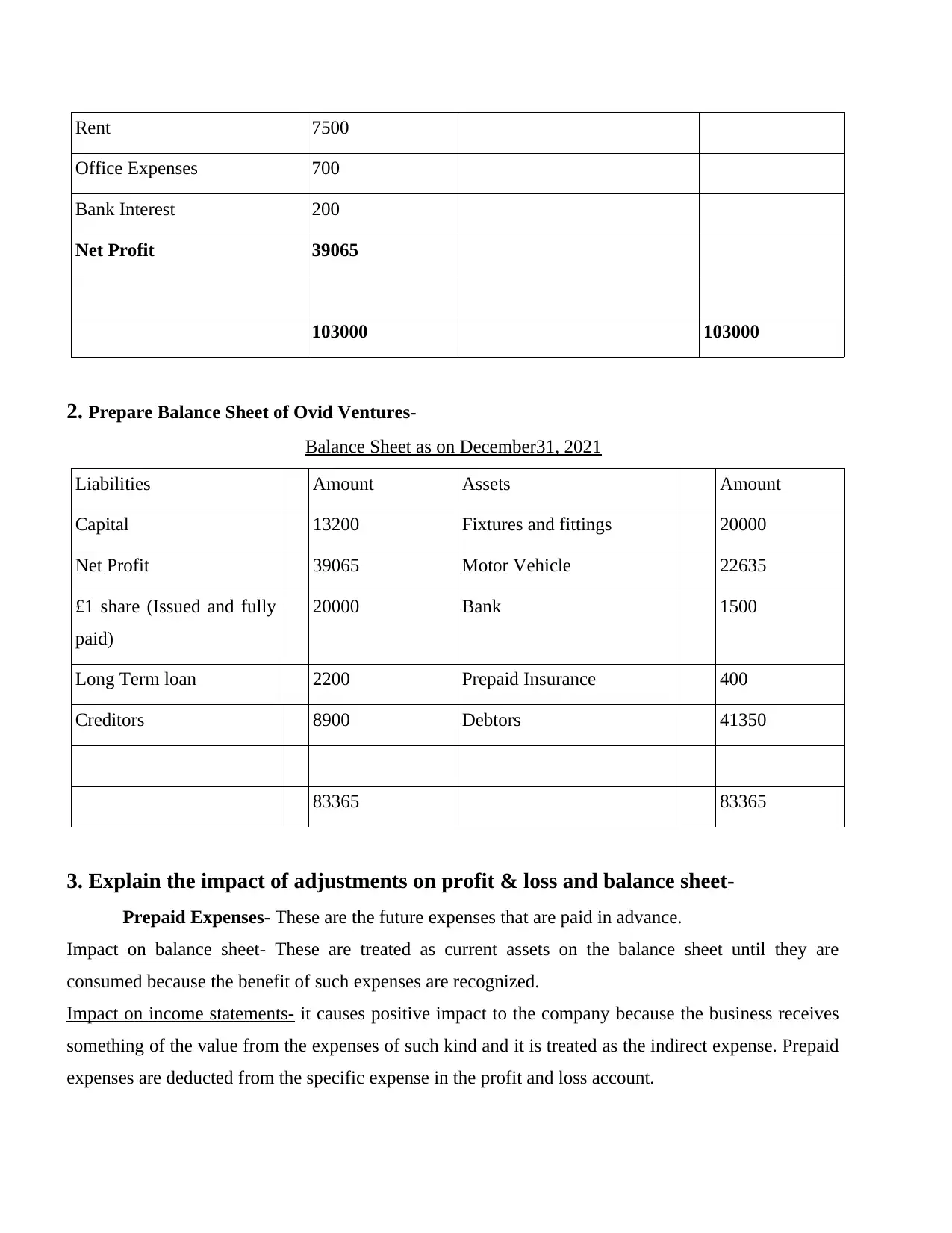

This report provides a detailed analysis of financial accounting principles, focusing on the interpretation of financial ratios for ASOS PLC over four years (2018-2021). It evaluates profitability, efficiency, liquidity, and financial structure using key ratios such as ROCE, stock turnover, debtors collection period, creditors payment period, current ratio, and gearing ratio. The report also includes prepared financial statements for Ovid Ventures, including an income statement and balance sheet, with explanations of the impact of adjustments like prepaid and accrued expenses and income. Additionally, it discusses the reasons for adding and deducting specific items in cash flow statements, such as depreciation and disposal of non-current assets. The analysis concludes with insights into the importance of ratio analysis for organizational comparison and the significance of adjustments in financial statements.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.