AC4052QA Financial Accounting Report: Ratio Analysis and Ovid Venture

VerifiedAdded on 2023/06/14

|11

|2035

|263

Report

AI Summary

This report provides a comprehensive financial analysis, beginning with an interpretation of financial ratios for ASOS plc, a UK-based online retailer, evaluating its profitability, efficiency, liquidity, and financial structure. The analysis reveals areas needing improvement, such as stock turnover and debtor collection days, and suggests strategies for enhancement. The report then presents the preparation of financial statements for Ovid Venture, including an income statement and balance sheet for the year ended December 31, 2021. Finally, it details the impact of various adjustments on the profit and loss account and balance sheet, along with the cash flow implications of depreciation, disposal of non-current assets, and changes in inventory.

AC4052QA FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A.....................................................................................................................................3

INTRODUCTION...........................................................................................................................3

Interpretation of Ratios................................................................................................................3

CONCLUSION................................................................................................................................5

SECTION B.....................................................................................................................................6

Question 1....................................................................................................................................6

Preparation of Income statement of Ovid Venture......................................................................6

Preparation of balance sheet of Ovid Venture.............................................................................6

Question 2....................................................................................................................................7

1....................................................................................................................................................7

2....................................................................................................................................................8

REFERENCES................................................................................................................................9

SECTION A.....................................................................................................................................3

INTRODUCTION...........................................................................................................................3

Interpretation of Ratios................................................................................................................3

CONCLUSION................................................................................................................................5

SECTION B.....................................................................................................................................6

Question 1....................................................................................................................................6

Preparation of Income statement of Ovid Venture......................................................................6

Preparation of balance sheet of Ovid Venture.............................................................................6

Question 2....................................................................................................................................7

1....................................................................................................................................................7

2....................................................................................................................................................8

REFERENCES................................................................................................................................9

SECTION A

INTRODUCTION

Ratio analysis is a tool with the help of which users of financial statement can analyse the

financial performance of company for their decision-making purpose. ASOS plc is a UK based

online retail company which offer fashion related products to its customers. The report will cover

the interpretation of ratios via evaluating the profitability, efficiency, liquidity and financial

structure of ASOS organization.

Interpretation of Ratios

Evaluating financial performance and position of ASOS Plc using financial ratios are as follows:

Profitability ratios: The profitability ratio state the ability of the company to generate

returns from the business operation and capital. In order to evaluate the profitability position of

ASOS plc, the return on capital employed is used. After analysing the result of return on capital

employed of ASOS organization for the four year, it is identified that profitability performance

of company is getting worst current year as compared to previous year. It is because in the year

2018 the ROCE of company is 22.72%, 2019 it is 6.99%, 2020 it is 12.52% and in the year 2021

it is 9.39%. The reason behind the drastic decrement in the ROCE of ASOS company is a

decrease in the earnings before interest and tax, increase in equity or an increase in non-current

liabilities. Ultimately, the result indicates that the ability of ASOS organization to generate profit

from its invested capital is poor in current year as compared to previous year. In order to improve

the same, the company need to adopt appropriate and suitable strategies. Here, the company

basically need to increase the sales and reduce the cost of sales. To reduce the cost of sales, it is

recommended to the company that they should provide training and development to its

employees (Gouda, El-Hoshy and Hassan, 2018). The impact of which the wastage of resources

will get decrease and ultimately cost of production will decrease.

Thus, in this way, ASOS company can enhance its overall profitability position of the

business in the market and gain competitive advantage.

Efficiency ratios: An efficiency ratio of the company indicates the ability of the

company to appropriately use assets in the business operation in order to generate income. The

three most significant efficiency ratio used to identify efficiency performance of ASOS is stock

INTRODUCTION

Ratio analysis is a tool with the help of which users of financial statement can analyse the

financial performance of company for their decision-making purpose. ASOS plc is a UK based

online retail company which offer fashion related products to its customers. The report will cover

the interpretation of ratios via evaluating the profitability, efficiency, liquidity and financial

structure of ASOS organization.

Interpretation of Ratios

Evaluating financial performance and position of ASOS Plc using financial ratios are as follows:

Profitability ratios: The profitability ratio state the ability of the company to generate

returns from the business operation and capital. In order to evaluate the profitability position of

ASOS plc, the return on capital employed is used. After analysing the result of return on capital

employed of ASOS organization for the four year, it is identified that profitability performance

of company is getting worst current year as compared to previous year. It is because in the year

2018 the ROCE of company is 22.72%, 2019 it is 6.99%, 2020 it is 12.52% and in the year 2021

it is 9.39%. The reason behind the drastic decrement in the ROCE of ASOS company is a

decrease in the earnings before interest and tax, increase in equity or an increase in non-current

liabilities. Ultimately, the result indicates that the ability of ASOS organization to generate profit

from its invested capital is poor in current year as compared to previous year. In order to improve

the same, the company need to adopt appropriate and suitable strategies. Here, the company

basically need to increase the sales and reduce the cost of sales. To reduce the cost of sales, it is

recommended to the company that they should provide training and development to its

employees (Gouda, El-Hoshy and Hassan, 2018). The impact of which the wastage of resources

will get decrease and ultimately cost of production will decrease.

Thus, in this way, ASOS company can enhance its overall profitability position of the

business in the market and gain competitive advantage.

Efficiency ratios: An efficiency ratio of the company indicates the ability of the

company to appropriately use assets in the business operation in order to generate income. The

three most significant efficiency ratio used to identify efficiency performance of ASOS is stock

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

turnover percentage, debtor collection period and creditors payment period. The stock turnover

of company in the current year i.e., 2021 is 4.85% which is lower than the previous year of

6.13%. Not only that, in the year 2019 and 2019, the stock turnover percentage is higher than

current year. This means that the capacity of the company to sell its goods and products quickly

and easily is poor in current year. Further, the debtor’s collection period of ASOS plc in the year

2021 is higher than all the previous three years. This means that company takes more time to

collect its dues from the debtors because of its poor credit policy (Linares-Mustarós, Coenders

and Vives-Mestres, 2018). The creditors' payment period of ASOS organization in the year 2021

i.e., 36.81 is lower than the previous year of 39.5 days. This means the company pay its dues to

its supplier on time in order to improve the credit worthiness of the business.

After analysing the overall efficiency ratio result, it can be interpretable that the credit

policy of ASOS organization is poor along with its selling strategy. In order to improve the same,

it is advisable to ASOS plc that they should promote its products and services over the social

media platform. Not only that, the company’s management also need to decide the discount

policy on sales. It means the company should offer discount to its customers if they purchase the

products on cash rather than credit (Risal and Aqsa, 2020). Also, discount will be offer to

customer on the early payment of dues. Further, it is also advisable to the management of ASOS

that they should prepare A/R aging report in order to determine the current payment status of

each debtors of the organization. Also, being proactive in generating invoices and sending them

to customers is most important part of the internal management of the company.

Liquidity ratios: The liquidity ratio is also one of the significant metrics of financial

ratio which indicate the capability of the company to pay off its current obligation with the use of

cash balance and cash generated from other current assets. The current ratio and quick ratio is

computed and used for identifying the liquidity performance of the company. After analysing the

result of ratio calculations, it is identified that current ratio of ASOS plc in the year 2021 is 1.56

which is higher than all the previous three years. On the other hand, quick ratio of the company

also higher in current year i.e., 0.75 as compared to all the previous three years. This means the

liquidity position of ASOS company is getting better year by year. This might be because of the

good credit worthiness of the business in the market and in the eye of supplier. The company has

the capability to pay its supplier on time from the cash they kept aside or cash collection from

of company in the current year i.e., 2021 is 4.85% which is lower than the previous year of

6.13%. Not only that, in the year 2019 and 2019, the stock turnover percentage is higher than

current year. This means that the capacity of the company to sell its goods and products quickly

and easily is poor in current year. Further, the debtor’s collection period of ASOS plc in the year

2021 is higher than all the previous three years. This means that company takes more time to

collect its dues from the debtors because of its poor credit policy (Linares-Mustarós, Coenders

and Vives-Mestres, 2018). The creditors' payment period of ASOS organization in the year 2021

i.e., 36.81 is lower than the previous year of 39.5 days. This means the company pay its dues to

its supplier on time in order to improve the credit worthiness of the business.

After analysing the overall efficiency ratio result, it can be interpretable that the credit

policy of ASOS organization is poor along with its selling strategy. In order to improve the same,

it is advisable to ASOS plc that they should promote its products and services over the social

media platform. Not only that, the company’s management also need to decide the discount

policy on sales. It means the company should offer discount to its customers if they purchase the

products on cash rather than credit (Risal and Aqsa, 2020). Also, discount will be offer to

customer on the early payment of dues. Further, it is also advisable to the management of ASOS

that they should prepare A/R aging report in order to determine the current payment status of

each debtors of the organization. Also, being proactive in generating invoices and sending them

to customers is most important part of the internal management of the company.

Liquidity ratios: The liquidity ratio is also one of the significant metrics of financial

ratio which indicate the capability of the company to pay off its current obligation with the use of

cash balance and cash generated from other current assets. The current ratio and quick ratio is

computed and used for identifying the liquidity performance of the company. After analysing the

result of ratio calculations, it is identified that current ratio of ASOS plc in the year 2021 is 1.56

which is higher than all the previous three years. On the other hand, quick ratio of the company

also higher in current year i.e., 0.75 as compared to all the previous three years. This means the

liquidity position of ASOS company is getting better year by year. This might be because of the

good credit worthiness of the business in the market and in the eye of supplier. The company has

the capability to pay its supplier on time from the cash they kept aside or cash collection from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

debtors or cash from sale of inventory. However, the current as well as quick ratio of the

company is lower than the ideal or standard ratio of 2:1 and 1:1 respectively. So, in order to

achieve the ideal ratio, the management of ASOS plc should adopt some steps.

It is advisable to company that they should offer an early payment discounts to its credit

customers in order to collect the cash earlier. This further used by company to pay off its

obligations on time (Mongwe and Malan, 2020). Along with this, the company can also sale its

outdated assets into the market in order to generate more cash within the organization. Besides

generating cash, the company also need to build strong relation with the supplier so that any

delay in payment will not affect the liquidity and credit worthiness of the organization.

Financial structure ratios: This is another financial ratio metrics which indicate the

gearing percentage of ASOS organization is higher in current year as compared to previous years

(Coufal, 2020). This indicates better structural and financial position of the company in the

market. ASOS should maintain its financial structure in this way only without increasing

percentage too much. In this way, it can be said that the overall financial performance of ASOS

is good but the company should adopt strategy to improve its more.

CONCLUSION

After summing up the above information, it is concluded that the overall financial

performance and structure of ASOS plc is good in current year except some of the areas such as

stock turnover, return on capital employed, debtor’s collection days. The report has

recommended the various strategies with the application of which the company can enhance its

performance and position of business. Lastly, the report has also concluded the factors which

leads to decrease in ratios in the interpretation of ratio section of report.

company is lower than the ideal or standard ratio of 2:1 and 1:1 respectively. So, in order to

achieve the ideal ratio, the management of ASOS plc should adopt some steps.

It is advisable to company that they should offer an early payment discounts to its credit

customers in order to collect the cash earlier. This further used by company to pay off its

obligations on time (Mongwe and Malan, 2020). Along with this, the company can also sale its

outdated assets into the market in order to generate more cash within the organization. Besides

generating cash, the company also need to build strong relation with the supplier so that any

delay in payment will not affect the liquidity and credit worthiness of the organization.

Financial structure ratios: This is another financial ratio metrics which indicate the

gearing percentage of ASOS organization is higher in current year as compared to previous years

(Coufal, 2020). This indicates better structural and financial position of the company in the

market. ASOS should maintain its financial structure in this way only without increasing

percentage too much. In this way, it can be said that the overall financial performance of ASOS

is good but the company should adopt strategy to improve its more.

CONCLUSION

After summing up the above information, it is concluded that the overall financial

performance and structure of ASOS plc is good in current year except some of the areas such as

stock turnover, return on capital employed, debtor’s collection days. The report has

recommended the various strategies with the application of which the company can enhance its

performance and position of business. Lastly, the report has also concluded the factors which

leads to decrease in ratios in the interpretation of ratio section of report.

SECTION B

Question 1

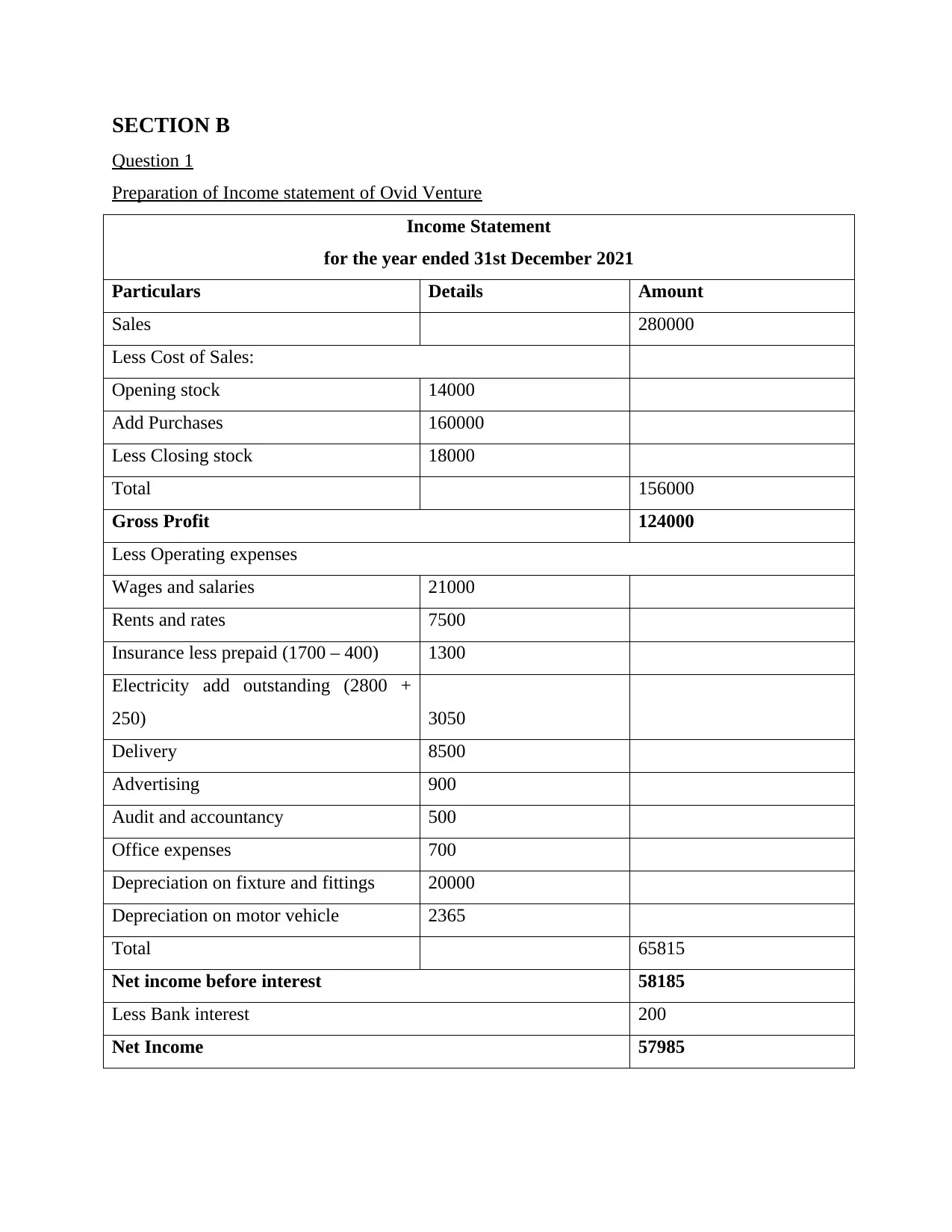

Preparation of Income statement of Ovid Venture

Income Statement

for the year ended 31st December 2021

Particulars Details Amount

Sales 280000

Less Cost of Sales:

Opening stock 14000

Add Purchases 160000

Less Closing stock 18000

Total 156000

Gross Profit 124000

Less Operating expenses

Wages and salaries 21000

Rents and rates 7500

Insurance less prepaid (1700 – 400) 1300

Electricity add outstanding (2800 +

250) 3050

Delivery 8500

Advertising 900

Audit and accountancy 500

Office expenses 700

Depreciation on fixture and fittings 20000

Depreciation on motor vehicle 2365

Total 65815

Net income before interest 58185

Less Bank interest 200

Net Income 57985

Question 1

Preparation of Income statement of Ovid Venture

Income Statement

for the year ended 31st December 2021

Particulars Details Amount

Sales 280000

Less Cost of Sales:

Opening stock 14000

Add Purchases 160000

Less Closing stock 18000

Total 156000

Gross Profit 124000

Less Operating expenses

Wages and salaries 21000

Rents and rates 7500

Insurance less prepaid (1700 – 400) 1300

Electricity add outstanding (2800 +

250) 3050

Delivery 8500

Advertising 900

Audit and accountancy 500

Office expenses 700

Depreciation on fixture and fittings 20000

Depreciation on motor vehicle 2365

Total 65815

Net income before interest 58185

Less Bank interest 200

Net Income 57985

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

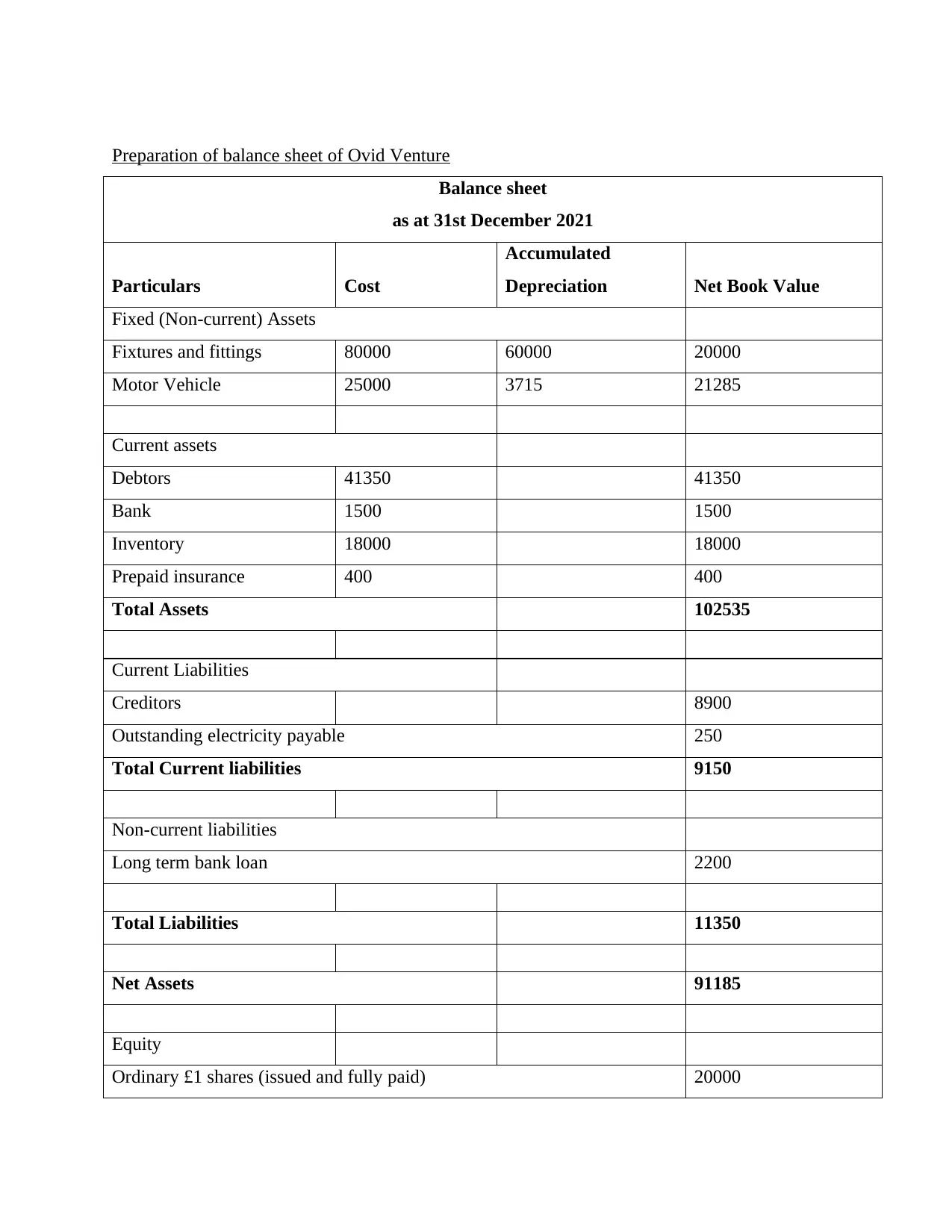

Preparation of balance sheet of Ovid Venture

Balance sheet

as at 31st December 2021

Particulars Cost

Accumulated

Depreciation Net Book Value

Fixed (Non-current) Assets

Fixtures and fittings 80000 60000 20000

Motor Vehicle 25000 3715 21285

Current assets

Debtors 41350 41350

Bank 1500 1500

Inventory 18000 18000

Prepaid insurance 400 400

Total Assets 102535

Current Liabilities

Creditors 8900

Outstanding electricity payable 250

Total Current liabilities 9150

Non-current liabilities

Long term bank loan 2200

Total Liabilities 11350

Net Assets 91185

Equity

Ordinary £1 shares (issued and fully paid) 20000

Balance sheet

as at 31st December 2021

Particulars Cost

Accumulated

Depreciation Net Book Value

Fixed (Non-current) Assets

Fixtures and fittings 80000 60000 20000

Motor Vehicle 25000 3715 21285

Current assets

Debtors 41350 41350

Bank 1500 1500

Inventory 18000 18000

Prepaid insurance 400 400

Total Assets 102535

Current Liabilities

Creditors 8900

Outstanding electricity payable 250

Total Current liabilities 9150

Non-current liabilities

Long term bank loan 2200

Total Liabilities 11350

Net Assets 91185

Equity

Ordinary £1 shares (issued and fully paid) 20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

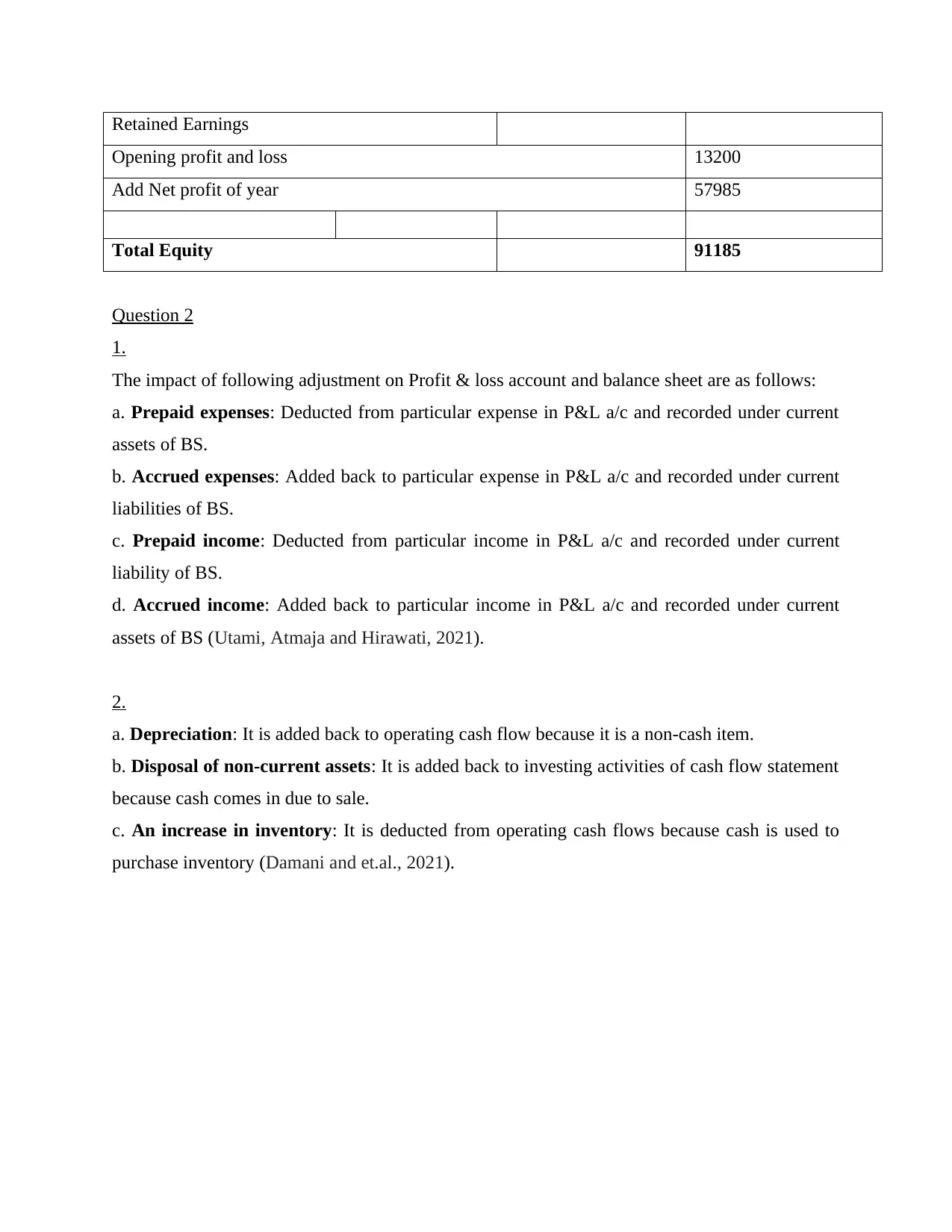

Retained Earnings

Opening profit and loss 13200

Add Net profit of year 57985

Total Equity 91185

Question 2

1.

The impact of following adjustment on Profit & loss account and balance sheet are as follows:

a. Prepaid expenses: Deducted from particular expense in P&L a/c and recorded under current

assets of BS.

b. Accrued expenses: Added back to particular expense in P&L a/c and recorded under current

liabilities of BS.

c. Prepaid income: Deducted from particular income in P&L a/c and recorded under current

liability of BS.

d. Accrued income: Added back to particular income in P&L a/c and recorded under current

assets of BS (Utami, Atmaja and Hirawati, 2021).

2.

a. Depreciation: It is added back to operating cash flow because it is a non-cash item.

b. Disposal of non-current assets: It is added back to investing activities of cash flow statement

because cash comes in due to sale.

c. An increase in inventory: It is deducted from operating cash flows because cash is used to

purchase inventory (Damani and et.al., 2021).

Opening profit and loss 13200

Add Net profit of year 57985

Total Equity 91185

Question 2

1.

The impact of following adjustment on Profit & loss account and balance sheet are as follows:

a. Prepaid expenses: Deducted from particular expense in P&L a/c and recorded under current

assets of BS.

b. Accrued expenses: Added back to particular expense in P&L a/c and recorded under current

liabilities of BS.

c. Prepaid income: Deducted from particular income in P&L a/c and recorded under current

liability of BS.

d. Accrued income: Added back to particular income in P&L a/c and recorded under current

assets of BS (Utami, Atmaja and Hirawati, 2021).

2.

a. Depreciation: It is added back to operating cash flow because it is a non-cash item.

b. Disposal of non-current assets: It is added back to investing activities of cash flow statement

because cash comes in due to sale.

c. An increase in inventory: It is deducted from operating cash flows because cash is used to

purchase inventory (Damani and et.al., 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Gouda, O. E., El-Hoshy, S. H. and Hassan, H. T., 2018. Proposed three ratios technique for the

interpretation of mineral oil transformers based dissolved gas analysis. IET Generation,

Transmission & Distribution. 12(11). pp.2650-2661.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting. 40. pp.1-10.

Risal, M. and Aqsa, M., 2020, October. The Influence of Financial Ratios and Intellectual

Capital on Financial Difficulties in Construction Companies. In International

Conference on Community Development (ICCD 2020) (pp. 303-307). Atlantis Press.

Mongwe, W. T. and Malan, K. M., 2020, December. The efficacy of financial ratios for fraud

detection using self organising maps. In 2020 IEEE Symposium Series on

Computational Intelligence (SSCI) (pp. 1100-1106). IEEE.

Coufal, M., 2020. Significance of different financial ratios in predicting stock returns: NYSE-

cross-industry analysis.

Utami, D. W., Atmaja, H. E. and Hirawati, H., 2021. The Role of Financial Ratios on the

Financial Distress Prediction. KINERJA. 25(2). pp.287-307.

Damani, A. D. and et.al., 2021. An Empirical study of the Financial Ratios of the Indian

Information Technology Sector by applying Factor Analysis and substantiation of the

results using Cluster Analysis.

Books and journals

Gouda, O. E., El-Hoshy, S. H. and Hassan, H. T., 2018. Proposed three ratios technique for the

interpretation of mineral oil transformers based dissolved gas analysis. IET Generation,

Transmission & Distribution. 12(11). pp.2650-2661.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting. 40. pp.1-10.

Risal, M. and Aqsa, M., 2020, October. The Influence of Financial Ratios and Intellectual

Capital on Financial Difficulties in Construction Companies. In International

Conference on Community Development (ICCD 2020) (pp. 303-307). Atlantis Press.

Mongwe, W. T. and Malan, K. M., 2020, December. The efficacy of financial ratios for fraud

detection using self organising maps. In 2020 IEEE Symposium Series on

Computational Intelligence (SSCI) (pp. 1100-1106). IEEE.

Coufal, M., 2020. Significance of different financial ratios in predicting stock returns: NYSE-

cross-industry analysis.

Utami, D. W., Atmaja, H. E. and Hirawati, H., 2021. The Role of Financial Ratios on the

Financial Distress Prediction. KINERJA. 25(2). pp.287-307.

Damani, A. D. and et.al., 2021. An Empirical study of the Financial Ratios of the Indian

Information Technology Sector by applying Factor Analysis and substantiation of the

results using Cluster Analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.