AC4410 Accounting & Finance: Financial Analysis of BT Group Plc

VerifiedAdded on 2023/04/20

|20

|2535

|81

Report

AI Summary

This report provides a comprehensive financial analysis of BT Group Plc, a multinational telecommunications company headquartered in London. The analysis utilizes key financial ratios, including profitability, liquidity, and efficiency ratios, computed from the company's financial statements over a four-year period (2015-2018). Profitability ratios, such as operating profit ratio and net profit ratio, indicate a fluctuating performance, with a slight decline in net profitability due to rising costs. Return on capital employed (ROCE) shows a moderate return on investments. Liquidity ratios, including current ratio and acid test ratio, suggest an improved but not yet ideal liquidity position. Activity ratios, such as trade receivables collection period and inventory turnover period, highlight areas for improvement in efficiency. The report concludes that while BT Group Plc shows some financial improvements, further cost management and efficiency enhancements are necessary. Desklib offers similar solved assignments and past papers for students.

Running head: ACCOUNTS AND FINANCE

Accounts and Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounts and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTS AND FINANCE

Table of Contents

Overview of the Company...............................................................................................................3

Ratio Analysis..................................................................................................................................3

Application of Ratio Analysis.....................................................................................................3

Merits of Ratio Analysis..............................................................................................................4

Demerits of Ratio Analysis..........................................................................................................4

Profitability Ratios...........................................................................................................................5

Operating Profit Ratios................................................................................................................5

Net Profit Ratio............................................................................................................................6

Return on Capital Employed.......................................................................................................6

Liquidity Ratios...............................................................................................................................7

Current Ratio...............................................................................................................................7

Acid Test Ratio............................................................................................................................8

Activity Ratios.................................................................................................................................9

Trade Receivables Collection Period...........................................................................................9

Trade Payables Payment Period................................................................................................10

Inventories Turnover Period......................................................................................................10

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

Appendix........................................................................................................................................14

ACCOUNTS AND FINANCE

Table of Contents

Overview of the Company...............................................................................................................3

Ratio Analysis..................................................................................................................................3

Application of Ratio Analysis.....................................................................................................3

Merits of Ratio Analysis..............................................................................................................4

Demerits of Ratio Analysis..........................................................................................................4

Profitability Ratios...........................................................................................................................5

Operating Profit Ratios................................................................................................................5

Net Profit Ratio............................................................................................................................6

Return on Capital Employed.......................................................................................................6

Liquidity Ratios...............................................................................................................................7

Current Ratio...............................................................................................................................7

Acid Test Ratio............................................................................................................................8

Activity Ratios.................................................................................................................................9

Trade Receivables Collection Period...........................................................................................9

Trade Payables Payment Period................................................................................................10

Inventories Turnover Period......................................................................................................10

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

Appendix........................................................................................................................................14

2

ACCOUNTS AND FINANCE

ACCOUNTS AND FINANCE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTS AND FINANCE

Overview of the Company

BT Group plc is multinational company which is engaged in telecommunication and the

company has its headquarters in London. The company is engaged in providing

telecommunication services in many countries and this shows that the scale of operation of the

company is high. BT group controls of a large number of subsidiaries. The company controls

telephone, broad bank and subscription television services on Great Britain.

The company is listed in London stock exchanges and the company has developed

reputation in the market. The company serves maximum customers in the market of London. The

origin of the business dates back toto the founding of Electric Telegraph which was established

in 1946. In today’s era the company serves around 30 million customers and is regarded as the

leading supplier of customer broad bank and communication services in UK (Btplc.com. 2018).

The assessment aims to analyze the financial performance of the business with the help of key

ratios which are computed for the business.

Ratio Analysis

Application of Ratio Analysis

The financial ratios of a business are considered to be important financial indicators of

the business and can be used effectively to determine the performance of the business. The ratios

which are computed and analyzed using the technique of ratio analysis are liquidity ratios,

profitability ratios and efficiency ratios (Delen, Kuzey and Uyar 2013). The ratios which are

computed are considered to be important factors which determine the performance of the

business and also are considered to financial indicators for the success of the business. In

addition to this, the financial ratios cover different aspects of performance of a business such as

ACCOUNTS AND FINANCE

Overview of the Company

BT Group plc is multinational company which is engaged in telecommunication and the

company has its headquarters in London. The company is engaged in providing

telecommunication services in many countries and this shows that the scale of operation of the

company is high. BT group controls of a large number of subsidiaries. The company controls

telephone, broad bank and subscription television services on Great Britain.

The company is listed in London stock exchanges and the company has developed

reputation in the market. The company serves maximum customers in the market of London. The

origin of the business dates back toto the founding of Electric Telegraph which was established

in 1946. In today’s era the company serves around 30 million customers and is regarded as the

leading supplier of customer broad bank and communication services in UK (Btplc.com. 2018).

The assessment aims to analyze the financial performance of the business with the help of key

ratios which are computed for the business.

Ratio Analysis

Application of Ratio Analysis

The financial ratios of a business are considered to be important financial indicators of

the business and can be used effectively to determine the performance of the business. The ratios

which are computed and analyzed using the technique of ratio analysis are liquidity ratios,

profitability ratios and efficiency ratios (Delen, Kuzey and Uyar 2013). The ratios which are

computed are considered to be important factors which determine the performance of the

business and also are considered to financial indicators for the success of the business. In

addition to this, the financial ratios cover different aspects of performance of a business such as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTS AND FINANCE

profitability, liquidity, solvency and similar other aspects. Moreover, the financial ratios are also

helpful in decision making process and effectively highlight the strengths of the business.

Merits of Ratio Analysis

The benefits of ratio analysis are listed below in details:

Ratio analysis can effectively used by the management of the company for taking major

decisions in a business which can be related to any aspect of the business.

The technique is very useful in simplifying difficult treatment of the business and also

financial data into simple estimates which can be interpreted easily by the management of

the company.

The key financial ratios which are computed are often considered by the investors before

they take any decision whether to invest in the shares of the business.

Demerits of Ratio Analysis

The limitation which is associated with the technique of ratio analysis are listed below:

The effect and impact of inflation are completely ignored by the technique of ratio

analysis. The changes in the price level of the business is not considered by the

technique.

The qualitative aspects of a company are not considered by ratio analysis of financial

statement of a business.

The different types of accounting principles and treatment which are undertaken by

different company can have an impact on the technique of ratio analysis and therefore the

technique is not reliable.

ACCOUNTS AND FINANCE

profitability, liquidity, solvency and similar other aspects. Moreover, the financial ratios are also

helpful in decision making process and effectively highlight the strengths of the business.

Merits of Ratio Analysis

The benefits of ratio analysis are listed below in details:

Ratio analysis can effectively used by the management of the company for taking major

decisions in a business which can be related to any aspect of the business.

The technique is very useful in simplifying difficult treatment of the business and also

financial data into simple estimates which can be interpreted easily by the management of

the company.

The key financial ratios which are computed are often considered by the investors before

they take any decision whether to invest in the shares of the business.

Demerits of Ratio Analysis

The limitation which is associated with the technique of ratio analysis are listed below:

The effect and impact of inflation are completely ignored by the technique of ratio

analysis. The changes in the price level of the business is not considered by the

technique.

The qualitative aspects of a company are not considered by ratio analysis of financial

statement of a business.

The different types of accounting principles and treatment which are undertaken by

different company can have an impact on the technique of ratio analysis and therefore the

technique is not reliable.

5

ACCOUNTS AND FINANCE

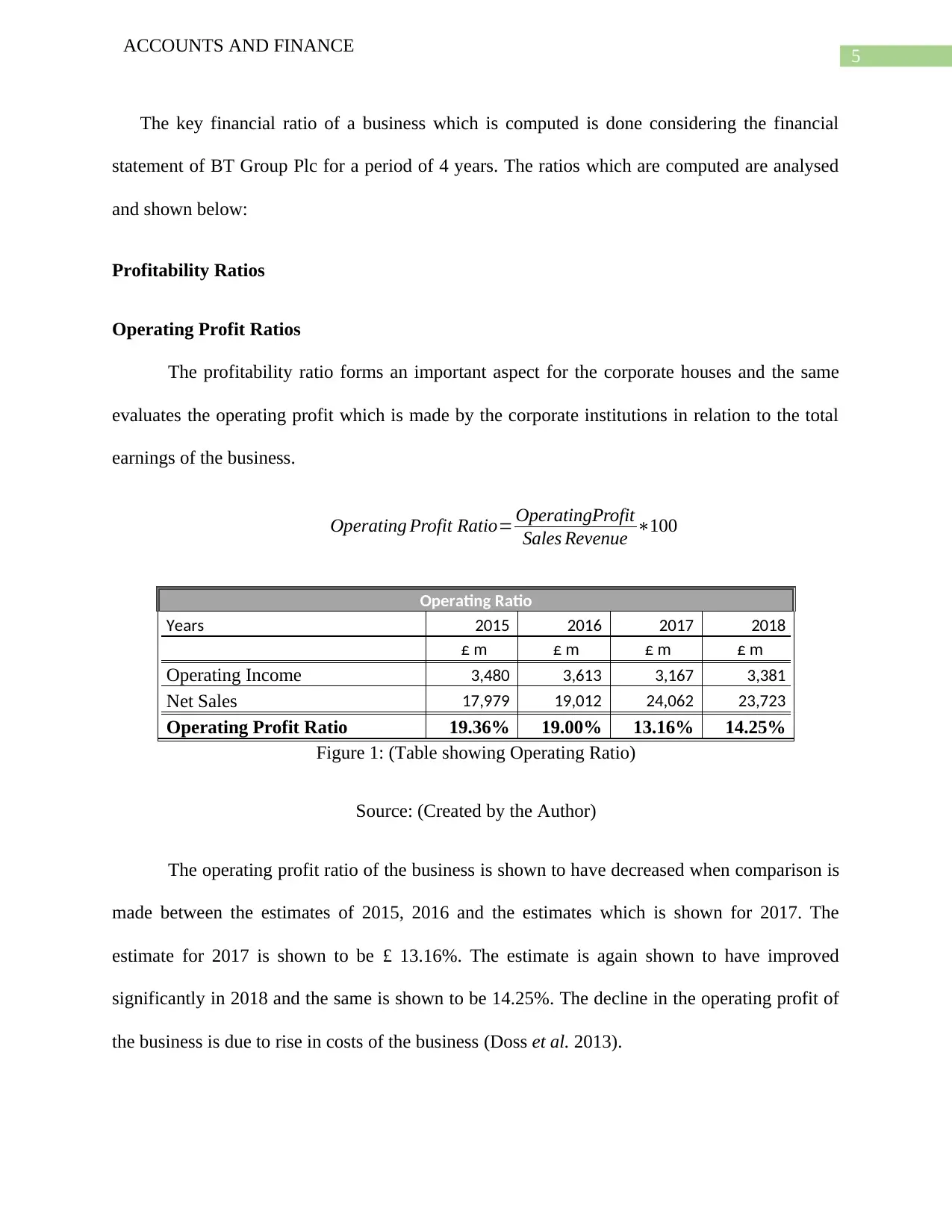

The key financial ratio of a business which is computed is done considering the financial

statement of BT Group Plc for a period of 4 years. The ratios which are computed are analysed

and shown below:

Profitability Ratios

Operating Profit Ratios

The profitability ratio forms an important aspect for the corporate houses and the same

evaluates the operating profit which is made by the corporate institutions in relation to the total

earnings of the business.

Operating Profit Ratio= OperatingProfit

Sales Revenue ∗100

Operating Ratio

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Operating Income 3,480 3,613 3,167 3,381

Net Sales 17,979 19,012 24,062 23,723

Operating Profit Ratio 19.36% 19.00% 13.16% 14.25%

Figure 1: (Table showing Operating Ratio)

Source: (Created by the Author)

The operating profit ratio of the business is shown to have decreased when comparison is

made between the estimates of 2015, 2016 and the estimates which is shown for 2017. The

estimate for 2017 is shown to be £ 13.16%. The estimate is again shown to have improved

significantly in 2018 and the same is shown to be 14.25%. The decline in the operating profit of

the business is due to rise in costs of the business (Doss et al. 2013).

ACCOUNTS AND FINANCE

The key financial ratio of a business which is computed is done considering the financial

statement of BT Group Plc for a period of 4 years. The ratios which are computed are analysed

and shown below:

Profitability Ratios

Operating Profit Ratios

The profitability ratio forms an important aspect for the corporate houses and the same

evaluates the operating profit which is made by the corporate institutions in relation to the total

earnings of the business.

Operating Profit Ratio= OperatingProfit

Sales Revenue ∗100

Operating Ratio

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Operating Income 3,480 3,613 3,167 3,381

Net Sales 17,979 19,012 24,062 23,723

Operating Profit Ratio 19.36% 19.00% 13.16% 14.25%

Figure 1: (Table showing Operating Ratio)

Source: (Created by the Author)

The operating profit ratio of the business is shown to have decreased when comparison is

made between the estimates of 2015, 2016 and the estimates which is shown for 2017. The

estimate for 2017 is shown to be £ 13.16%. The estimate is again shown to have improved

significantly in 2018 and the same is shown to be 14.25%. The decline in the operating profit of

the business is due to rise in costs of the business (Doss et al. 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTS AND FINANCE

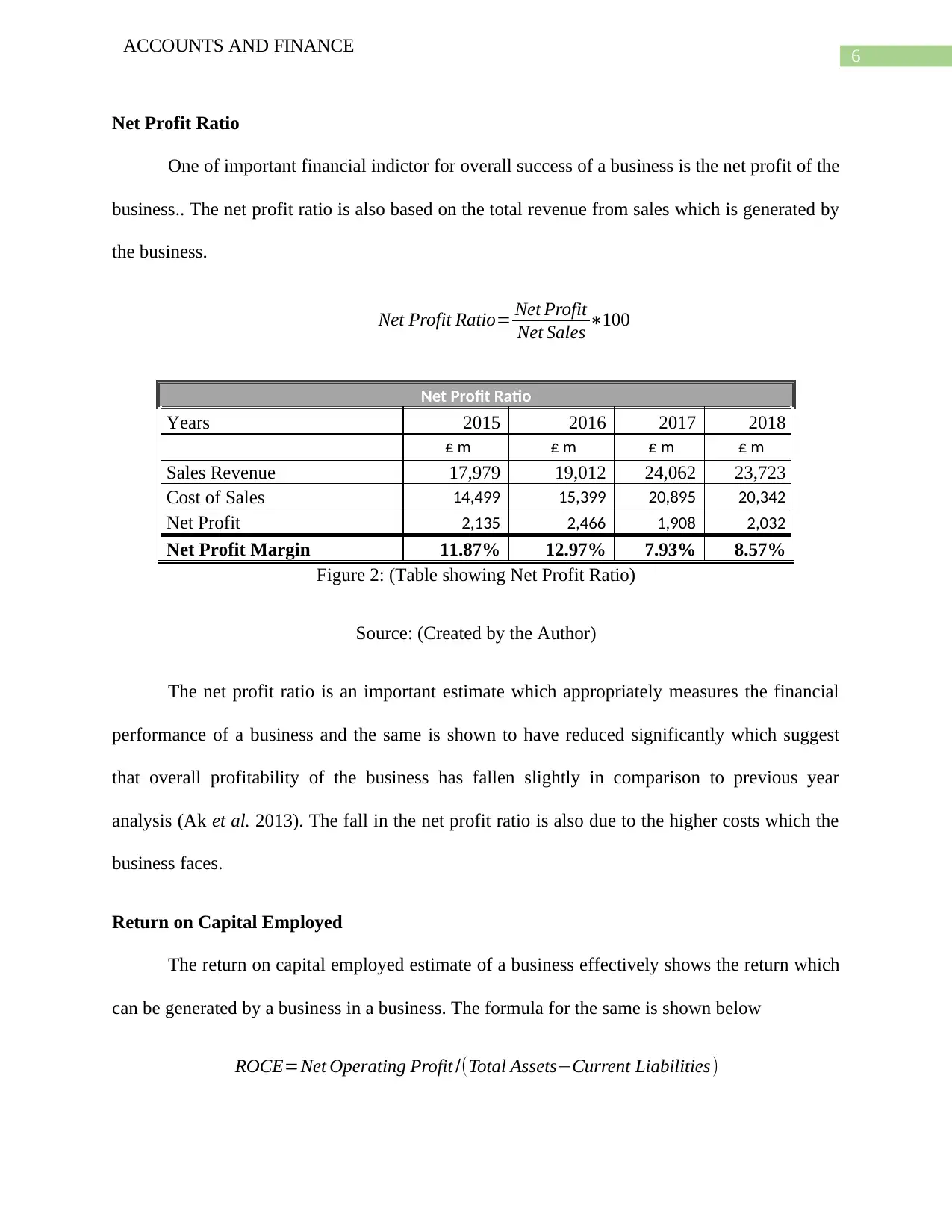

Net Profit Ratio

One of important financial indictor for overall success of a business is the net profit of the

business.. The net profit ratio is also based on the total revenue from sales which is generated by

the business.

Net Profit Ratio= Net Profit

Net Sales ∗100

Net Profit Ratio

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Sales Revenue 17,979 19,012 24,062 23,723

Cost of Sales 14,499 15,399 20,895 20,342

Net Profit 2,135 2,466 1,908 2,032

Net Profit Margin 11.87% 12.97% 7.93% 8.57%

Figure 2: (Table showing Net Profit Ratio)

Source: (Created by the Author)

The net profit ratio is an important estimate which appropriately measures the financial

performance of a business and the same is shown to have reduced significantly which suggest

that overall profitability of the business has fallen slightly in comparison to previous year

analysis (Ak et al. 2013). The fall in the net profit ratio is also due to the higher costs which the

business faces.

Return on Capital Employed

The return on capital employed estimate of a business effectively shows the return which

can be generated by a business in a business. The formula for the same is shown below

ROCE=Net Operating Profit /(Total Assets−Current Liabilities)

ACCOUNTS AND FINANCE

Net Profit Ratio

One of important financial indictor for overall success of a business is the net profit of the

business.. The net profit ratio is also based on the total revenue from sales which is generated by

the business.

Net Profit Ratio= Net Profit

Net Sales ∗100

Net Profit Ratio

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Sales Revenue 17,979 19,012 24,062 23,723

Cost of Sales 14,499 15,399 20,895 20,342

Net Profit 2,135 2,466 1,908 2,032

Net Profit Margin 11.87% 12.97% 7.93% 8.57%

Figure 2: (Table showing Net Profit Ratio)

Source: (Created by the Author)

The net profit ratio is an important estimate which appropriately measures the financial

performance of a business and the same is shown to have reduced significantly which suggest

that overall profitability of the business has fallen slightly in comparison to previous year

analysis (Ak et al. 2013). The fall in the net profit ratio is also due to the higher costs which the

business faces.

Return on Capital Employed

The return on capital employed estimate of a business effectively shows the return which

can be generated by a business in a business. The formula for the same is shown below

ROCE=Net Operating Profit /(Total Assets−Current Liabilities)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTS AND FINANCE

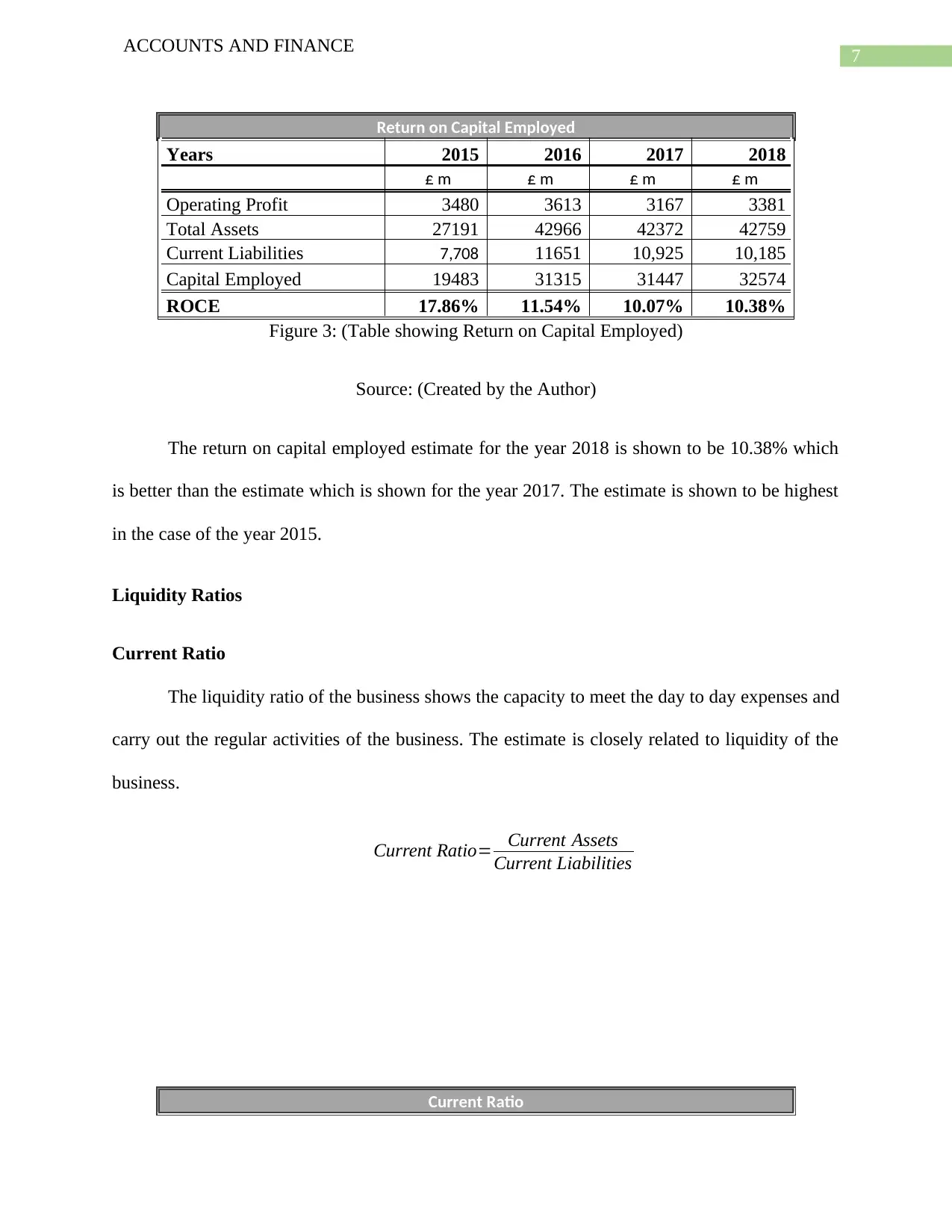

Return on Capital Employed

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Operating Profit 3480 3613 3167 3381

Total Assets 27191 42966 42372 42759

Current Liabilities 7,708 11651 10,925 10,185

Capital Employed 19483 31315 31447 32574

ROCE 17.86% 11.54% 10.07% 10.38%

Figure 3: (Table showing Return on Capital Employed)

Source: (Created by the Author)

The return on capital employed estimate for the year 2018 is shown to be 10.38% which

is better than the estimate which is shown for the year 2017. The estimate is shown to be highest

in the case of the year 2015.

Liquidity Ratios

Current Ratio

The liquidity ratio of the business shows the capacity to meet the day to day expenses and

carry out the regular activities of the business. The estimate is closely related to liquidity of the

business.

Current Ratio= Current Assets

Current Liabilities

Current Ratio

ACCOUNTS AND FINANCE

Return on Capital Employed

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Operating Profit 3480 3613 3167 3381

Total Assets 27191 42966 42372 42759

Current Liabilities 7,708 11651 10,925 10,185

Capital Employed 19483 31315 31447 32574

ROCE 17.86% 11.54% 10.07% 10.38%

Figure 3: (Table showing Return on Capital Employed)

Source: (Created by the Author)

The return on capital employed estimate for the year 2018 is shown to be 10.38% which

is better than the estimate which is shown for the year 2017. The estimate is shown to be highest

in the case of the year 2015.

Liquidity Ratios

Current Ratio

The liquidity ratio of the business shows the capacity to meet the day to day expenses and

carry out the regular activities of the business. The estimate is closely related to liquidity of the

business.

Current Ratio= Current Assets

Current Liabilities

Current Ratio

8

ACCOUNTS AND FINANCE

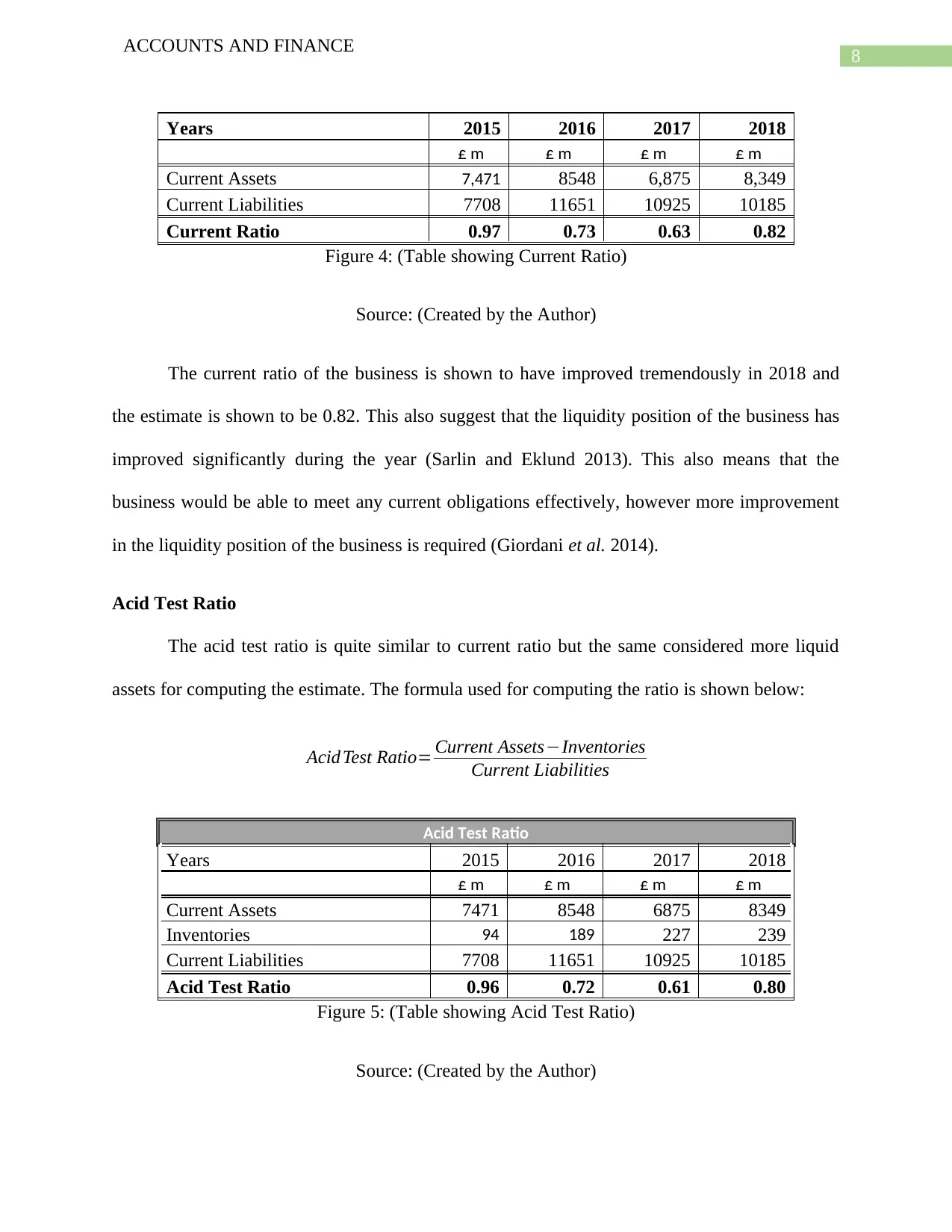

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Current Assets 7,471 8548 6,875 8,349

Current Liabilities 7708 11651 10925 10185

Current Ratio 0.97 0.73 0.63 0.82

Figure 4: (Table showing Current Ratio)

Source: (Created by the Author)

The current ratio of the business is shown to have improved tremendously in 2018 and

the estimate is shown to be 0.82. This also suggest that the liquidity position of the business has

improved significantly during the year (Sarlin and Eklund 2013). This also means that the

business would be able to meet any current obligations effectively, however more improvement

in the liquidity position of the business is required (Giordani et al. 2014).

Acid Test Ratio

The acid test ratio is quite similar to current ratio but the same considered more liquid

assets for computing the estimate. The formula used for computing the ratio is shown below:

Acid Test Ratio= Current Assets−Inventories

Current Liabilities

Acid Test Ratio

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Current Assets 7471 8548 6875 8349

Inventories 94 189 227 239

Current Liabilities 7708 11651 10925 10185

Acid Test Ratio 0.96 0.72 0.61 0.80

Figure 5: (Table showing Acid Test Ratio)

Source: (Created by the Author)

ACCOUNTS AND FINANCE

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Current Assets 7,471 8548 6,875 8,349

Current Liabilities 7708 11651 10925 10185

Current Ratio 0.97 0.73 0.63 0.82

Figure 4: (Table showing Current Ratio)

Source: (Created by the Author)

The current ratio of the business is shown to have improved tremendously in 2018 and

the estimate is shown to be 0.82. This also suggest that the liquidity position of the business has

improved significantly during the year (Sarlin and Eklund 2013). This also means that the

business would be able to meet any current obligations effectively, however more improvement

in the liquidity position of the business is required (Giordani et al. 2014).

Acid Test Ratio

The acid test ratio is quite similar to current ratio but the same considered more liquid

assets for computing the estimate. The formula used for computing the ratio is shown below:

Acid Test Ratio= Current Assets−Inventories

Current Liabilities

Acid Test Ratio

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Current Assets 7471 8548 6875 8349

Inventories 94 189 227 239

Current Liabilities 7708 11651 10925 10185

Acid Test Ratio 0.96 0.72 0.61 0.80

Figure 5: (Table showing Acid Test Ratio)

Source: (Created by the Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTS AND FINANCE

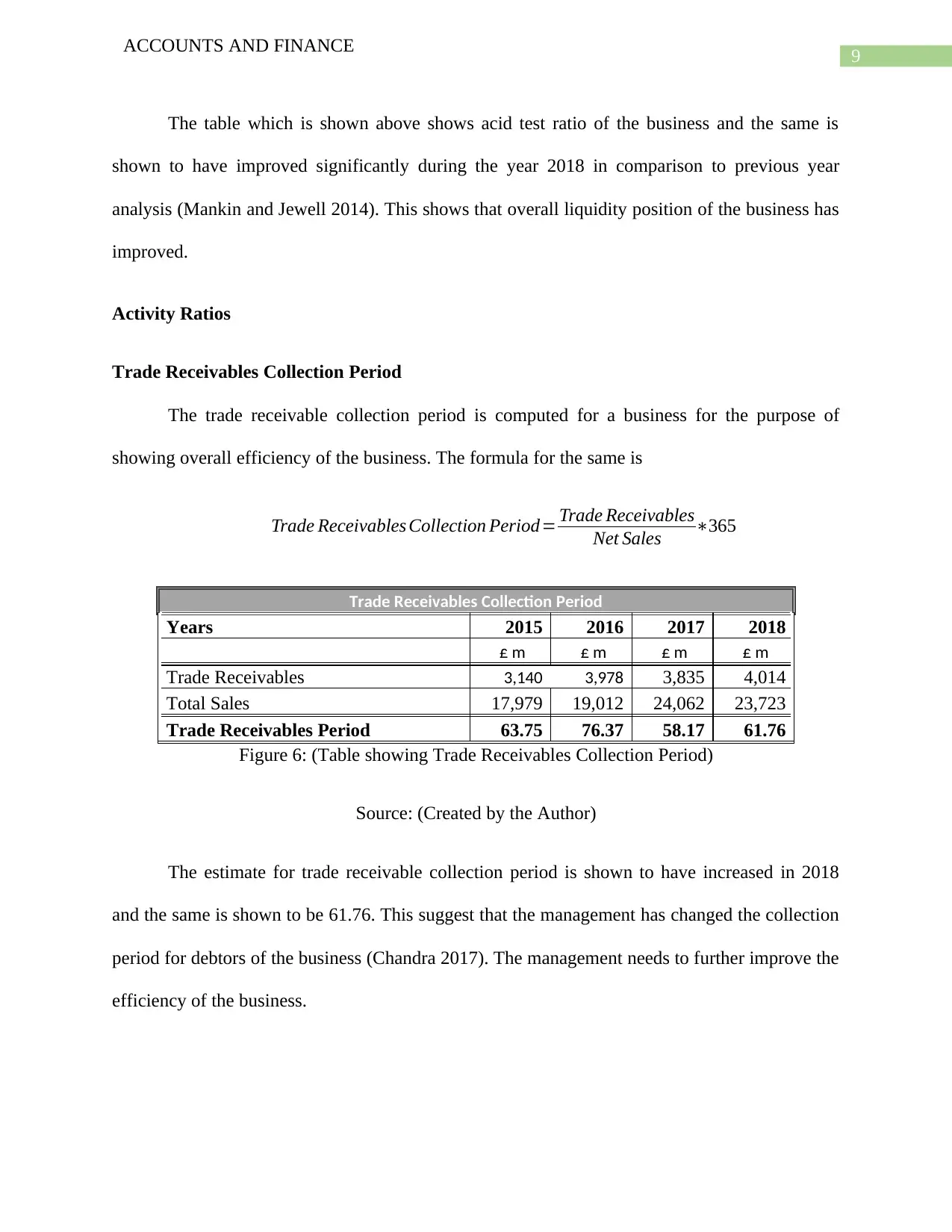

The table which is shown above shows acid test ratio of the business and the same is

shown to have improved significantly during the year 2018 in comparison to previous year

analysis (Mankin and Jewell 2014). This shows that overall liquidity position of the business has

improved.

Activity Ratios

Trade Receivables Collection Period

The trade receivable collection period is computed for a business for the purpose of

showing overall efficiency of the business. The formula for the same is

Trade Receivables Collection Period= Trade Receivables

Net Sales ∗365

Trade Receivables Collection Period

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Trade Receivables 3,140 3,978 3,835 4,014

Total Sales 17,979 19,012 24,062 23,723

Trade Receivables Period 63.75 76.37 58.17 61.76

Figure 6: (Table showing Trade Receivables Collection Period)

Source: (Created by the Author)

The estimate for trade receivable collection period is shown to have increased in 2018

and the same is shown to be 61.76. This suggest that the management has changed the collection

period for debtors of the business (Chandra 2017). The management needs to further improve the

efficiency of the business.

ACCOUNTS AND FINANCE

The table which is shown above shows acid test ratio of the business and the same is

shown to have improved significantly during the year 2018 in comparison to previous year

analysis (Mankin and Jewell 2014). This shows that overall liquidity position of the business has

improved.

Activity Ratios

Trade Receivables Collection Period

The trade receivable collection period is computed for a business for the purpose of

showing overall efficiency of the business. The formula for the same is

Trade Receivables Collection Period= Trade Receivables

Net Sales ∗365

Trade Receivables Collection Period

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Trade Receivables 3,140 3,978 3,835 4,014

Total Sales 17,979 19,012 24,062 23,723

Trade Receivables Period 63.75 76.37 58.17 61.76

Figure 6: (Table showing Trade Receivables Collection Period)

Source: (Created by the Author)

The estimate for trade receivable collection period is shown to have increased in 2018

and the same is shown to be 61.76. This suggest that the management has changed the collection

period for debtors of the business (Chandra 2017). The management needs to further improve the

efficiency of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTS AND FINANCE

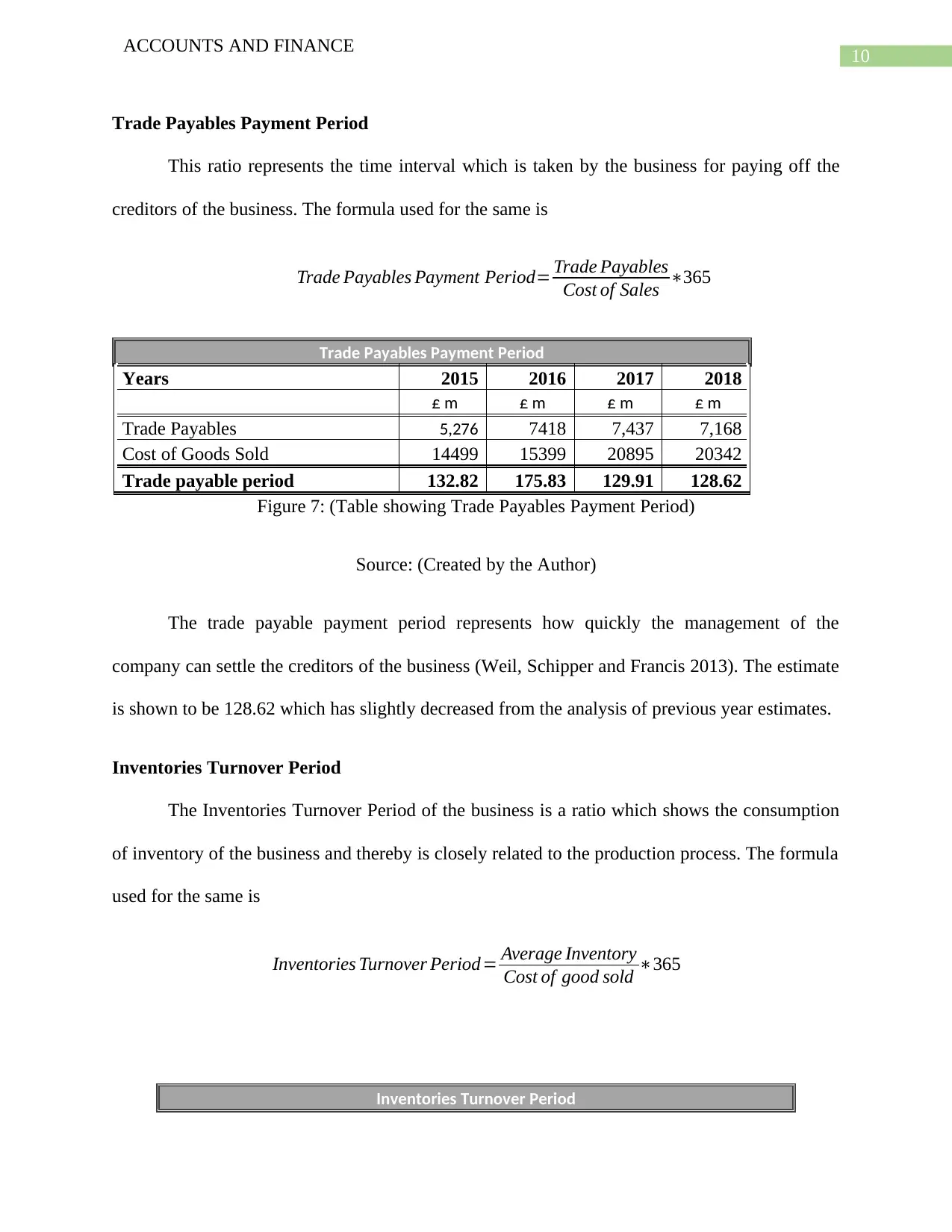

Trade Payables Payment Period

This ratio represents the time interval which is taken by the business for paying off the

creditors of the business. The formula used for the same is

Trade Payables Payment Period= Trade Payables

Cost of Sales ∗365

Trade Payables Payment Period

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Trade Payables 5,276 7418 7,437 7,168

Cost of Goods Sold 14499 15399 20895 20342

Trade payable period 132.82 175.83 129.91 128.62

Figure 7: (Table showing Trade Payables Payment Period)

Source: (Created by the Author)

The trade payable payment period represents how quickly the management of the

company can settle the creditors of the business (Weil, Schipper and Francis 2013). The estimate

is shown to be 128.62 which has slightly decreased from the analysis of previous year estimates.

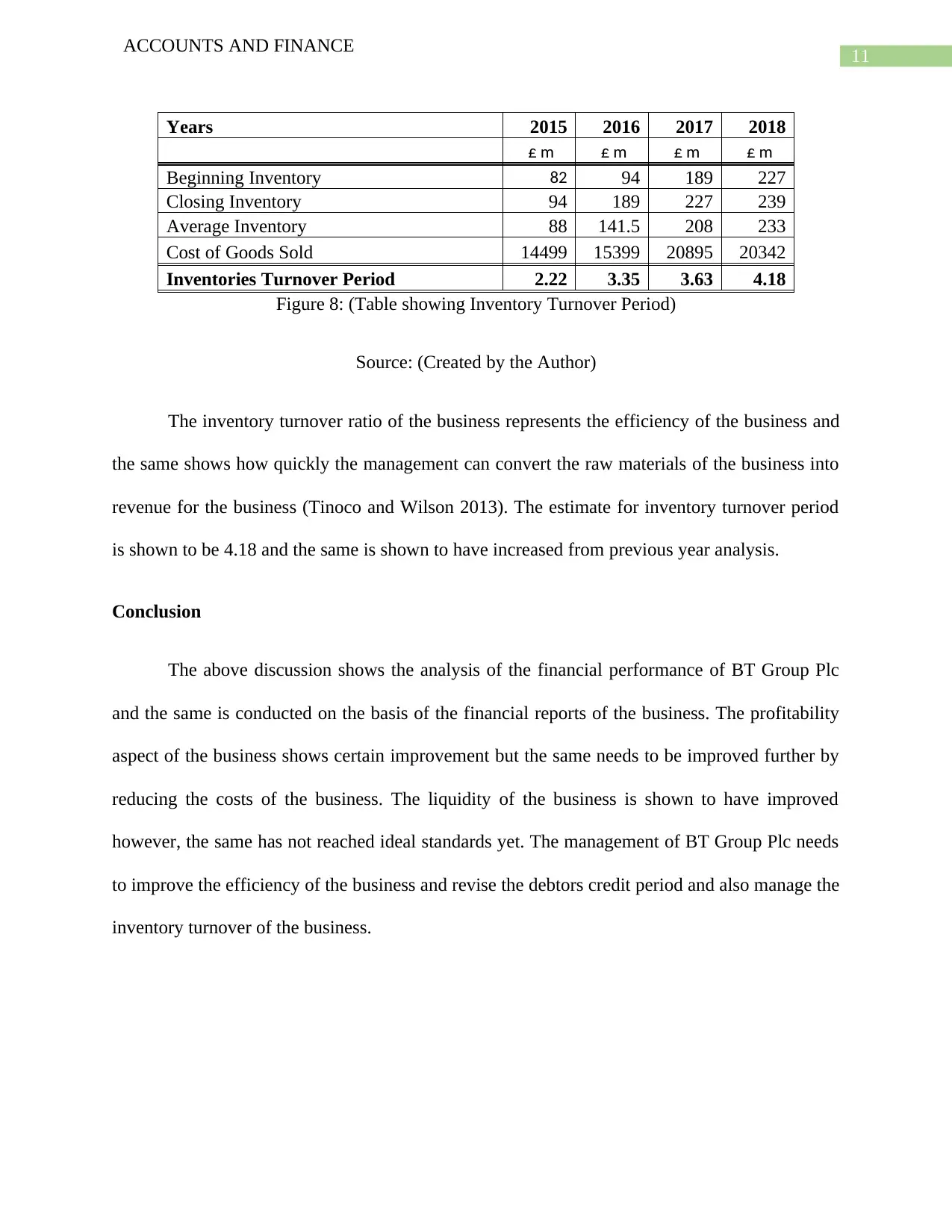

Inventories Turnover Period

The Inventories Turnover Period of the business is a ratio which shows the consumption

of inventory of the business and thereby is closely related to the production process. The formula

used for the same is

Inventories Turnover Period = Average Inventory

Cost of good sold ∗365

Inventories Turnover Period

ACCOUNTS AND FINANCE

Trade Payables Payment Period

This ratio represents the time interval which is taken by the business for paying off the

creditors of the business. The formula used for the same is

Trade Payables Payment Period= Trade Payables

Cost of Sales ∗365

Trade Payables Payment Period

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Trade Payables 5,276 7418 7,437 7,168

Cost of Goods Sold 14499 15399 20895 20342

Trade payable period 132.82 175.83 129.91 128.62

Figure 7: (Table showing Trade Payables Payment Period)

Source: (Created by the Author)

The trade payable payment period represents how quickly the management of the

company can settle the creditors of the business (Weil, Schipper and Francis 2013). The estimate

is shown to be 128.62 which has slightly decreased from the analysis of previous year estimates.

Inventories Turnover Period

The Inventories Turnover Period of the business is a ratio which shows the consumption

of inventory of the business and thereby is closely related to the production process. The formula

used for the same is

Inventories Turnover Period = Average Inventory

Cost of good sold ∗365

Inventories Turnover Period

11

ACCOUNTS AND FINANCE

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Beginning Inventory 82 94 189 227

Closing Inventory 94 189 227 239

Average Inventory 88 141.5 208 233

Cost of Goods Sold 14499 15399 20895 20342

Inventories Turnover Period 2.22 3.35 3.63 4.18

Figure 8: (Table showing Inventory Turnover Period)

Source: (Created by the Author)

The inventory turnover ratio of the business represents the efficiency of the business and

the same shows how quickly the management can convert the raw materials of the business into

revenue for the business (Tinoco and Wilson 2013). The estimate for inventory turnover period

is shown to be 4.18 and the same is shown to have increased from previous year analysis.

Conclusion

The above discussion shows the analysis of the financial performance of BT Group Plc

and the same is conducted on the basis of the financial reports of the business. The profitability

aspect of the business shows certain improvement but the same needs to be improved further by

reducing the costs of the business. The liquidity of the business is shown to have improved

however, the same has not reached ideal standards yet. The management of BT Group Plc needs

to improve the efficiency of the business and revise the debtors credit period and also manage the

inventory turnover of the business.

ACCOUNTS AND FINANCE

Years 2015 2016 2017 2018

£ m £ m £ m £ m

Beginning Inventory 82 94 189 227

Closing Inventory 94 189 227 239

Average Inventory 88 141.5 208 233

Cost of Goods Sold 14499 15399 20895 20342

Inventories Turnover Period 2.22 3.35 3.63 4.18

Figure 8: (Table showing Inventory Turnover Period)

Source: (Created by the Author)

The inventory turnover ratio of the business represents the efficiency of the business and

the same shows how quickly the management can convert the raw materials of the business into

revenue for the business (Tinoco and Wilson 2013). The estimate for inventory turnover period

is shown to be 4.18 and the same is shown to have increased from previous year analysis.

Conclusion

The above discussion shows the analysis of the financial performance of BT Group Plc

and the same is conducted on the basis of the financial reports of the business. The profitability

aspect of the business shows certain improvement but the same needs to be improved further by

reducing the costs of the business. The liquidity of the business is shown to have improved

however, the same has not reached ideal standards yet. The management of BT Group Plc needs

to improve the efficiency of the business and revise the debtors credit period and also manage the

inventory turnover of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.