ACC00152 Business Finance: Evaluating SSF's Product Launch Options

VerifiedAdded on 2023/04/25

|9

|1304

|252

Report

AI Summary

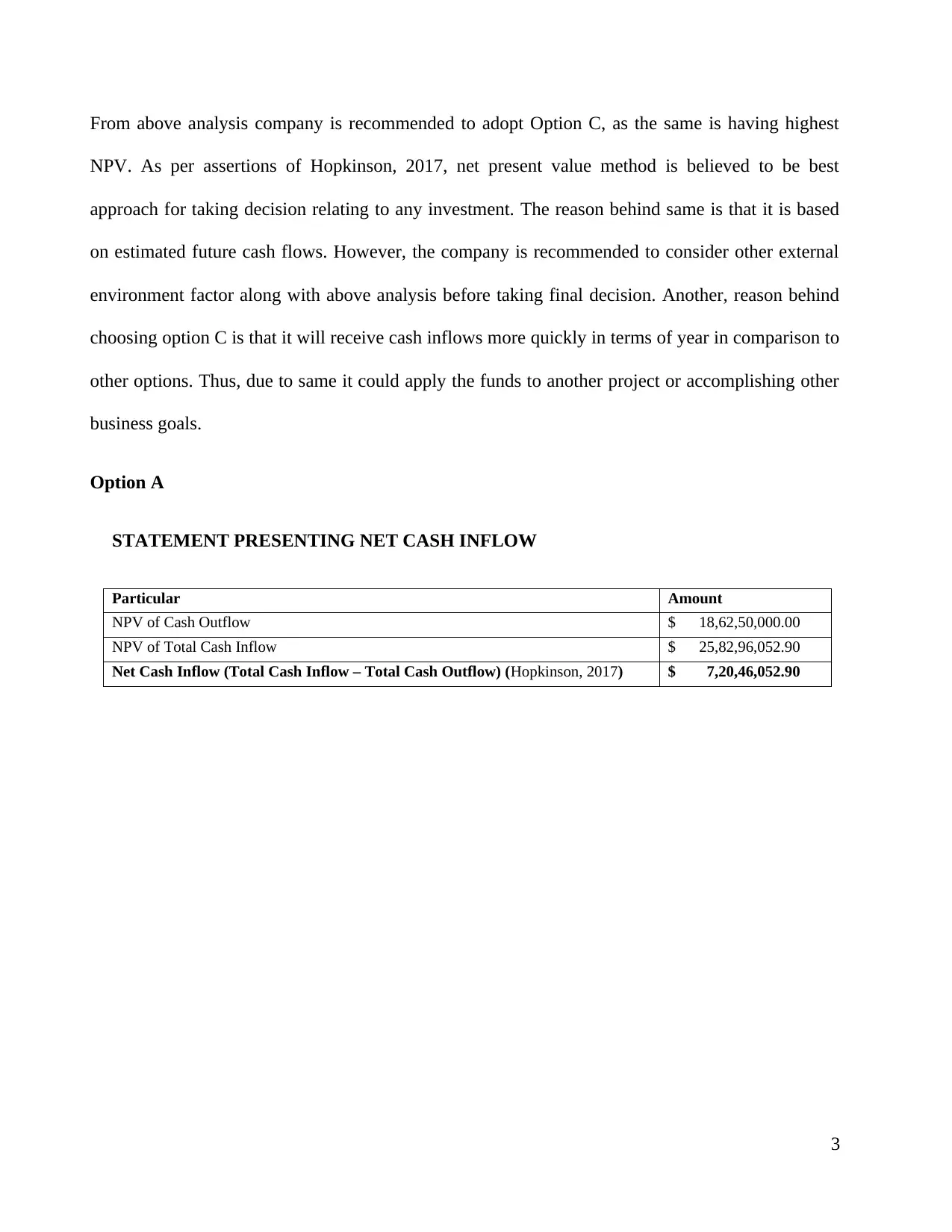

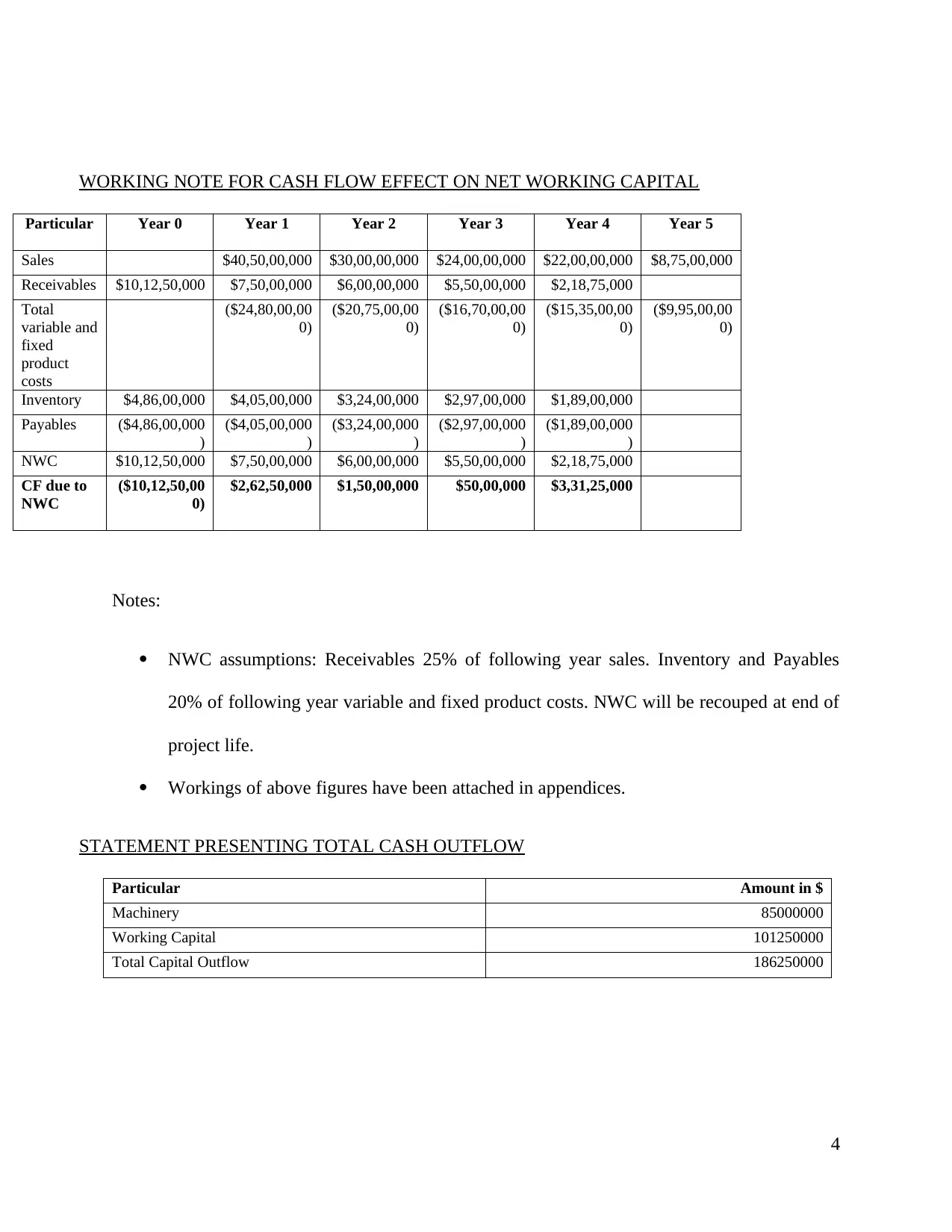

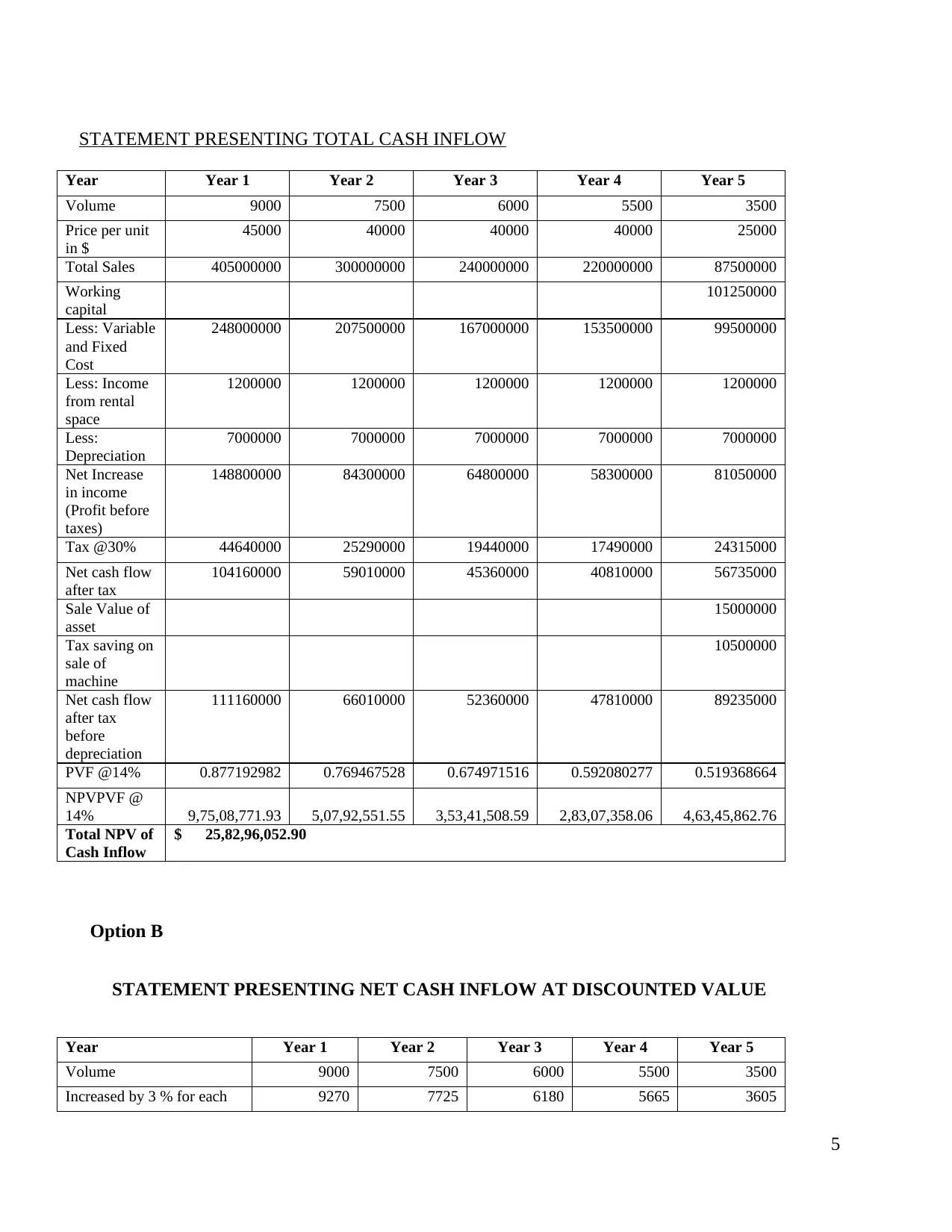

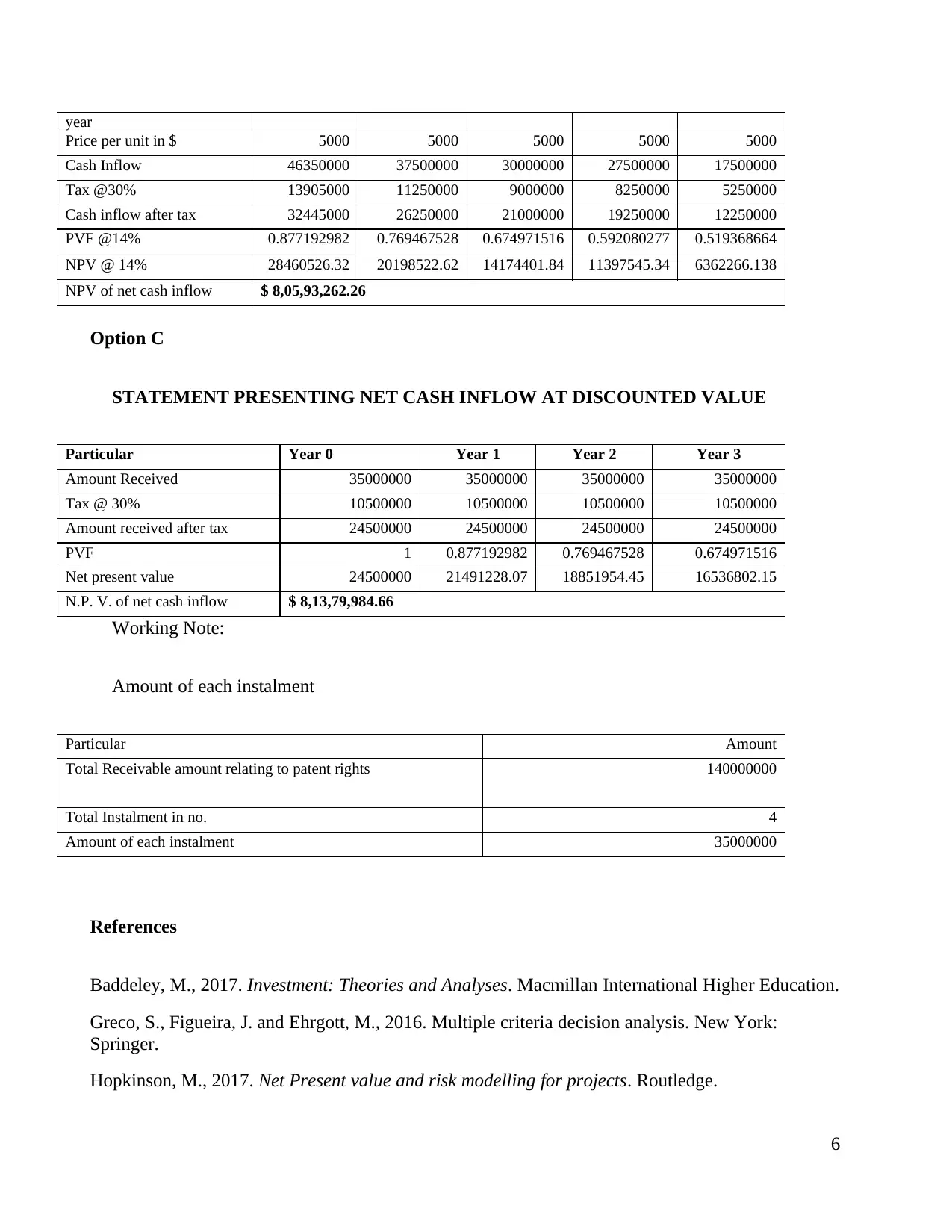

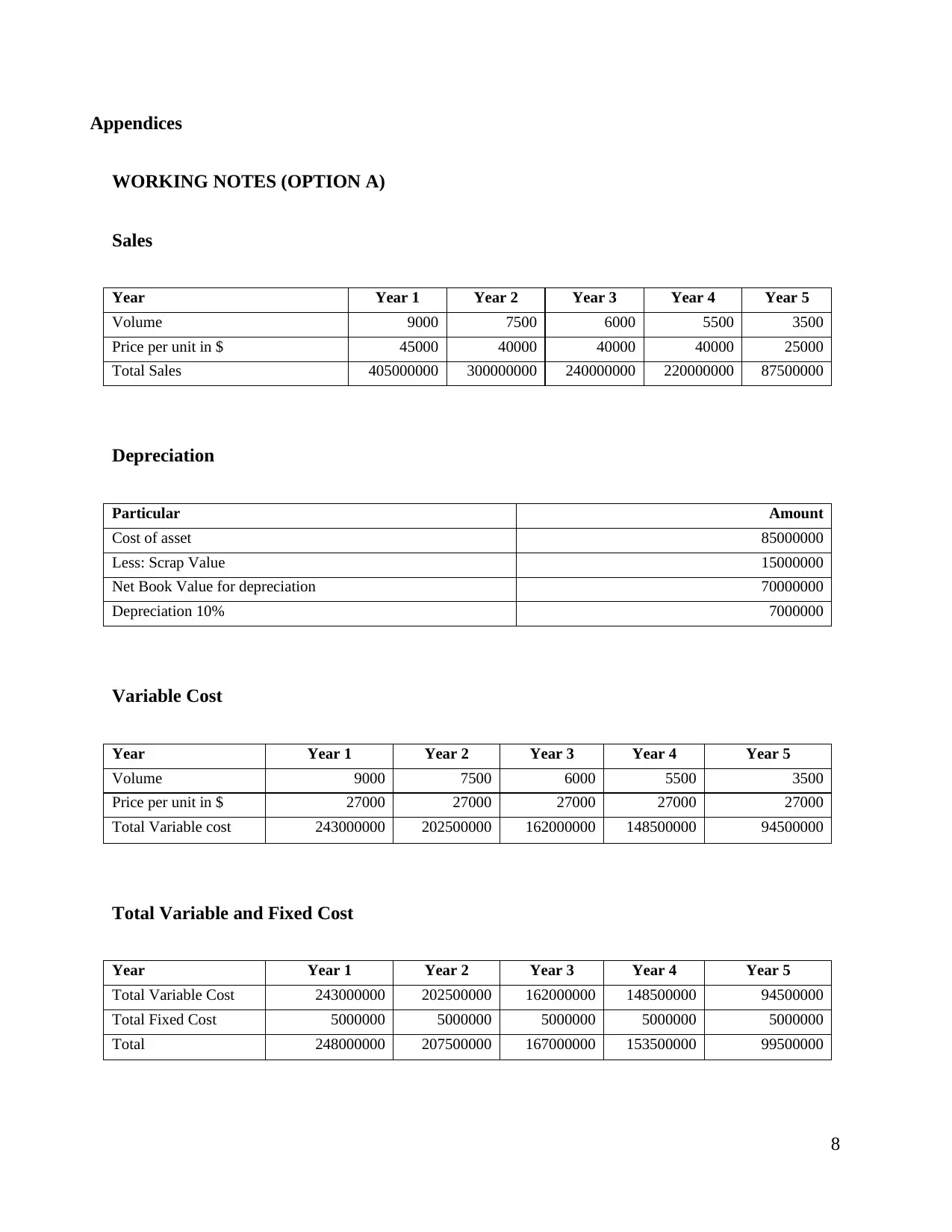

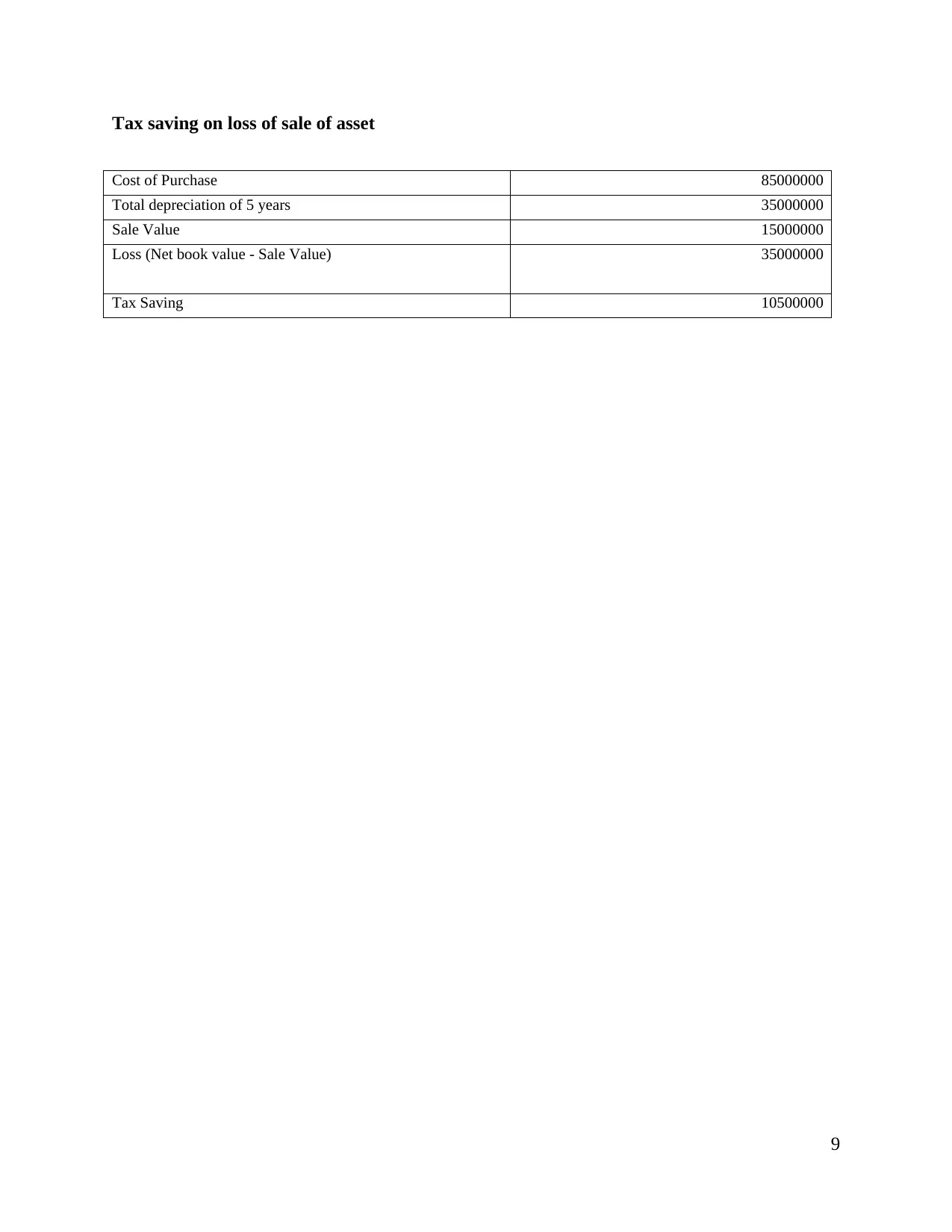

This report provides a critical evaluation and analysis of three options available to Space Sky Flight Ltd for launching their product. The analysis utilizes the Net Present Value (NPV) method to determine the most suitable option. Option A involves in-house manufacturing and direct sales, requiring significant initial cash outflow but potentially yielding higher profits and brand control. Option B considers licensing the product for royalties, emphasizing the importance of licensing agreement terms. Option C focuses on selling the patent rights, highlighting the potential for quick cash inflows but also the complexities of patenting. The report recommends Option C based on its highest NPV, while also advising the company to consider external environmental factors. Detailed financial statements and working notes are included for each option, outlining cash flows, sales projections, cost analysis, and NPV calculations. The appendices provide further details on sales, depreciation, variable costs, and tax savings. Desklib provides students with access to similar solved assignments and past papers.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.