ACC00712 Business Accounting: AASB Standards and Financial Reporting

VerifiedAdded on 2023/04/03

|13

|2238

|464

Essay

AI Summary

This essay provides an analysis of business accounting principles with reference to the Australian Conceptual Framework for accounting standards. It discusses the qualitative characteristics of financial information and examines the application of Australian Accounting Standards Board (AASB) standards in business practices, specifically focusing on Telstra's land revaluation and Spirit Telecom's compliance with AASB 15 and AASB 102. The essay concludes that compliance with accounting standards enhances the quality and reliability of financial reporting, positively influencing stakeholders and the securities market.

Running head: BUSINESS ACCOUNTING

Business Accounting

Name of the Student:

Name of the University:

Authors Note:

Business Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

BUSINESS ACCOUNTING

Summary:

Every country has conceptual framework for accounting. The accounting in an organization must

be in accordance with the applicable conceptual framework of the country. Companies operating

in Australia are under obligation to comply with the Australian Conceptual Framework for

Accounting. Accounting standards issued by Australian Accounting Standards Board (AASB)

are the standards to be followed by the companies operating in the country to comply with the

conceptual framework for accounting in the country. A clear picture has emerged from this

document that suggests that the conceptual framework of accounting is the prime consideration

to be kept in mind while recording financial transactions in the books of accounts and preparing

financial statements. Accordingly the validity of accounting treatment of two practical entities

namely, Telstra and Spirit Telecom is discussed below with respect to certain aspects of

accounting treatments.

BUSINESS ACCOUNTING

Summary:

Every country has conceptual framework for accounting. The accounting in an organization must

be in accordance with the applicable conceptual framework of the country. Companies operating

in Australia are under obligation to comply with the Australian Conceptual Framework for

Accounting. Accounting standards issued by Australian Accounting Standards Board (AASB)

are the standards to be followed by the companies operating in the country to comply with the

conceptual framework for accounting in the country. A clear picture has emerged from this

document that suggests that the conceptual framework of accounting is the prime consideration

to be kept in mind while recording financial transactions in the books of accounts and preparing

financial statements. Accordingly the validity of accounting treatment of two practical entities

namely, Telstra and Spirit Telecom is discussed below with respect to certain aspects of

accounting treatments.

2

BUSINESS ACCOUNTING

Contents

Summary:.........................................................................................................................................1

Introduction:....................................................................................................................................3

Part 1:...............................................................................................................................................3

Part 2:...............................................................................................................................................4

Part 3:...............................................................................................................................................6

Part 4:...............................................................................................................................................7

Conclusion:......................................................................................................................................9

References:....................................................................................................................................11

BUSINESS ACCOUNTING

Contents

Summary:.........................................................................................................................................1

Introduction:....................................................................................................................................3

Part 1:...............................................................................................................................................3

Part 2:...............................................................................................................................................4

Part 3:...............................................................................................................................................6

Part 4:...............................................................................................................................................7

Conclusion:......................................................................................................................................9

References:....................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

BUSINESS ACCOUNTING

Introduction:

Telstra has purchased a land in 2010 at a cost of $52 million. The market value of the land in

2018 stands at $200 million. As per the accountant of the company it is important to revalue the

land to reflect the economic reality of the asset at the present date. Also the compliance with

conceptual framework of accounting by Spirit Telecom Limited shall be discussed here by taking

examples from its Annual Report 2018.

Part 1:

Australian Accounting Standards Board, here in after to be referred to as AASB in this

document, has issued accounting standards to be followed in recording, summarizing and

maintaining books of accounts of entities operating in the country. The objective behind

introduction and implementation of these standards is to improve the quality of financial

reporting in the country. The fair and true representation of financial performance and position of

an entity in the financial statements is achievable when the financial statements are in

compliance with the accounting standards issued by the country (Barker and Teixeira, 2018).

The accountant of Telstra while suggesting that the land should be revalued to reflect the current

financial value of the asset in the books of accounts stated that this notion is consistent with

qualitative characteristics of faithful presentation (BOYMAL, 2007).

The above statement is correct. The reason for confirming with the statement of the accounting

on the notion of consistency in qualitative characteristics of faithful presentation is because the

objective of financial statements is to state the true and fair financial performance and position of

an organization through financial reports. AASB 13, Fair Value Measurement, issued by the

AASB clearly outlines the importance of fair value accounting in reflecting the actual financial

BUSINESS ACCOUNTING

Introduction:

Telstra has purchased a land in 2010 at a cost of $52 million. The market value of the land in

2018 stands at $200 million. As per the accountant of the company it is important to revalue the

land to reflect the economic reality of the asset at the present date. Also the compliance with

conceptual framework of accounting by Spirit Telecom Limited shall be discussed here by taking

examples from its Annual Report 2018.

Part 1:

Australian Accounting Standards Board, here in after to be referred to as AASB in this

document, has issued accounting standards to be followed in recording, summarizing and

maintaining books of accounts of entities operating in the country. The objective behind

introduction and implementation of these standards is to improve the quality of financial

reporting in the country. The fair and true representation of financial performance and position of

an entity in the financial statements is achievable when the financial statements are in

compliance with the accounting standards issued by the country (Barker and Teixeira, 2018).

The accountant of Telstra while suggesting that the land should be revalued to reflect the current

financial value of the asset in the books of accounts stated that this notion is consistent with

qualitative characteristics of faithful presentation (BOYMAL, 2007).

The above statement is correct. The reason for confirming with the statement of the accounting

on the notion of consistency in qualitative characteristics of faithful presentation is because the

objective of financial statements is to state the true and fair financial performance and position of

an organization through financial reports. AASB 13, Fair Value Measurement, issued by the

AASB clearly outlines the importance of fair value accounting in reflecting the actual financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

BUSINESS ACCOUNTING

state and performance of an organization in its financial statements. The importance of fair value

measurements to reflect the true and fair financial position of an organization is extremely

important to the qualitative characteristics of faithful presentation.

In this case especially, the fact that Telstra acquired the land in 2010 at a cost of $52 million has

significantly higher value in 2018. Thus, to continue to show the land at $52 million despite

knowing that its value at present is $200 million is against the basic principle of true and fair

representation of financial performance and position in financial statements of the company.

Thus, the suggestion of the accountant to revalue the land at current market value is consistent

with fundamental principle of accounting and financial reporting (Craig, Smieliauskas and

Amernic, 2016). By revaluing the land at its current market value of $200 million the actual

economic reality of the asset will be reflected in the financial statements of the company. Thus,

the statement, “This notion is consistent with the qualitative characteristic of faithful

presentation” is correct from the true and fair representation of point of view of financial

statements.

Part 2:

Fundamental characteristics of financial information:

The stakeholders of a business often have no other alternative source of information apart from

financial statements of the business to assess the financial state and performance of an

organization. The financial statements in order to be effective must have certain fundamental

qualitative characteristics. A brief discussion about these fundamental qualitative characteristics

are explained below.

BUSINESS ACCOUNTING

state and performance of an organization in its financial statements. The importance of fair value

measurements to reflect the true and fair financial position of an organization is extremely

important to the qualitative characteristics of faithful presentation.

In this case especially, the fact that Telstra acquired the land in 2010 at a cost of $52 million has

significantly higher value in 2018. Thus, to continue to show the land at $52 million despite

knowing that its value at present is $200 million is against the basic principle of true and fair

representation of financial performance and position in financial statements of the company.

Thus, the suggestion of the accountant to revalue the land at current market value is consistent

with fundamental principle of accounting and financial reporting (Craig, Smieliauskas and

Amernic, 2016). By revaluing the land at its current market value of $200 million the actual

economic reality of the asset will be reflected in the financial statements of the company. Thus,

the statement, “This notion is consistent with the qualitative characteristic of faithful

presentation” is correct from the true and fair representation of point of view of financial

statements.

Part 2:

Fundamental characteristics of financial information:

The stakeholders of a business often have no other alternative source of information apart from

financial statements of the business to assess the financial state and performance of an

organization. The financial statements in order to be effective must have certain fundamental

qualitative characteristics. A brief discussion about these fundamental qualitative characteristics

are explained below.

5

BUSINESS ACCOUNTING

Relevance: The financial statements in order to be useful to the stakeholders of an organization

must provide relevant information to the stakeholders. Thus, relevance of financial information

provided in the financial statements is essential to the overall objective of financial statements.

Only if the information is capable of influencing the decision of users of such information that

it’s relevant.

Faithful presentation: Financial information must be complete, free of error and neutral to

represent the financial performance faithfully. Thus, by not disclosing the correct and present

value of an asset the relevance of financial information of Telstra will be reduced greatly

(Dennis, 2018).

Comparability: The information provided in financial reports must be comparable with an

organizations own information over time as well as with the information of similar organization.

Understandability: The information to be provided in the financial statements by an organization

must be understandable to the users of financial information. Without understandability the

utility of financial information to the stakeholders would be less. Thus, financial information

must be understandable to the users of financial information.

Timeliness: The utility and usefulness of financial information to the users such information will

be dependent on the timeliness of the information. Thus, the information must be provided to the

users on correct time to allow them to take correct decisions using these information.

Verifiability: Information must be verifiable by an audit to assure the users of financial

information about its credibility and reliability.

BUSINESS ACCOUNTING

Relevance: The financial statements in order to be useful to the stakeholders of an organization

must provide relevant information to the stakeholders. Thus, relevance of financial information

provided in the financial statements is essential to the overall objective of financial statements.

Only if the information is capable of influencing the decision of users of such information that

it’s relevant.

Faithful presentation: Financial information must be complete, free of error and neutral to

represent the financial performance faithfully. Thus, by not disclosing the correct and present

value of an asset the relevance of financial information of Telstra will be reduced greatly

(Dennis, 2018).

Comparability: The information provided in financial reports must be comparable with an

organizations own information over time as well as with the information of similar organization.

Understandability: The information to be provided in the financial statements by an organization

must be understandable to the users of financial information. Without understandability the

utility of financial information to the stakeholders would be less. Thus, financial information

must be understandable to the users of financial information.

Timeliness: The utility and usefulness of financial information to the users such information will

be dependent on the timeliness of the information. Thus, the information must be provided to the

users on correct time to allow them to take correct decisions using these information.

Verifiability: Information must be verifiable by an audit to assure the users of financial

information about its credibility and reliability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

BUSINESS ACCOUNTING

AASB conceptual framework is very much established on the above fundamental qualitative

characteristics of financial information. The entire process of issuing accounting standards and

ensuring these are followed is mainly to ensure that the financial information has the above

qualitative characteristics as mentioned (Dragomir, 2011). AASB 1 first time adoption of

accounting standards has specifically mentioned the reason to comply with the accounting

standards in preparing and presenting the financial statements is to ensure that the financial

information has the fundamental qualitative characteristics required to ensure the usefulness of

the information to the stakeholders of an organization.

Part 3:

The annual report of an entity is prepared to provide the stakeholders of the entity with all

information about its operations and performance in the last financial year. Spirit Telecom

Limited has prepared and issued its annual report 2018 containing all the information about the

company and its performance including financial statements and audit report of the company.

The company has mentioned in its annual report about the method and standards issued in

preparing and presenting the financial statements of the company.

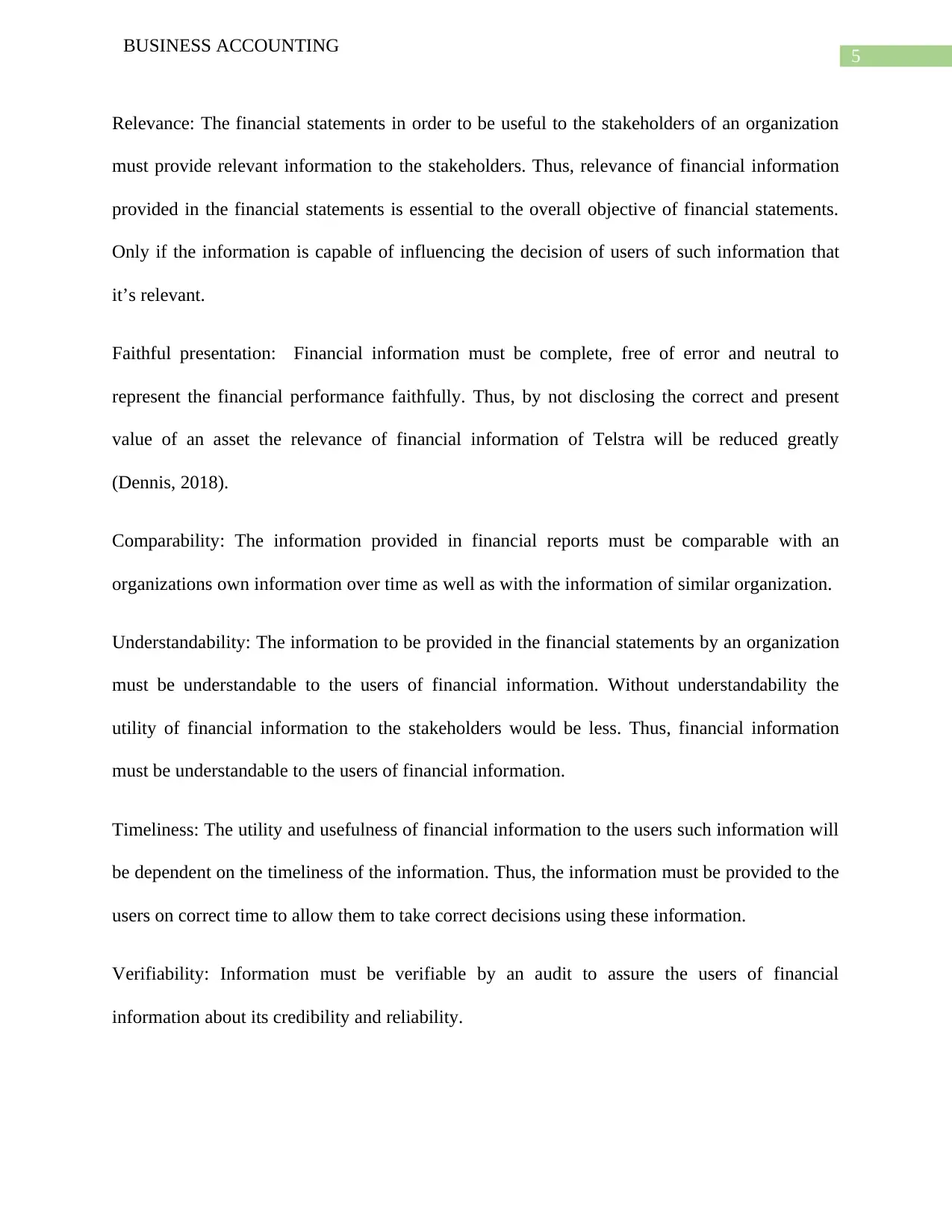

Firstly, it is important to state that the company has prepared complete set of financial statements

as per the accounting conceptual framework in the country including notes to accounts. As per

notes the company has followed AASB 15 to recognize and measure revenue in the books of

accounts of the company. As per the notes revenue has been recognized and measured at the

expected fair value received or receivable in the future. One of the important characteristics of

financial information is faithful presentation. By measuring the revenue in fair value received or

receivable the company has ensured that the qualitative characteristic of faithful representation is

upheld. The screen shot from the annual report of the company attached below shows that the

BUSINESS ACCOUNTING

AASB conceptual framework is very much established on the above fundamental qualitative

characteristics of financial information. The entire process of issuing accounting standards and

ensuring these are followed is mainly to ensure that the financial information has the above

qualitative characteristics as mentioned (Dragomir, 2011). AASB 1 first time adoption of

accounting standards has specifically mentioned the reason to comply with the accounting

standards in preparing and presenting the financial statements is to ensure that the financial

information has the fundamental qualitative characteristics required to ensure the usefulness of

the information to the stakeholders of an organization.

Part 3:

The annual report of an entity is prepared to provide the stakeholders of the entity with all

information about its operations and performance in the last financial year. Spirit Telecom

Limited has prepared and issued its annual report 2018 containing all the information about the

company and its performance including financial statements and audit report of the company.

The company has mentioned in its annual report about the method and standards issued in

preparing and presenting the financial statements of the company.

Firstly, it is important to state that the company has prepared complete set of financial statements

as per the accounting conceptual framework in the country including notes to accounts. As per

notes the company has followed AASB 15 to recognize and measure revenue in the books of

accounts of the company. As per the notes revenue has been recognized and measured at the

expected fair value received or receivable in the future. One of the important characteristics of

financial information is faithful presentation. By measuring the revenue in fair value received or

receivable the company has ensured that the qualitative characteristic of faithful representation is

upheld. The screen shot from the annual report of the company attached below shows that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BUSINESS ACCOUNTING

company has complied with AASB 15 (Financial Accounting and Reporting Standards for

Private Entities, 2006).

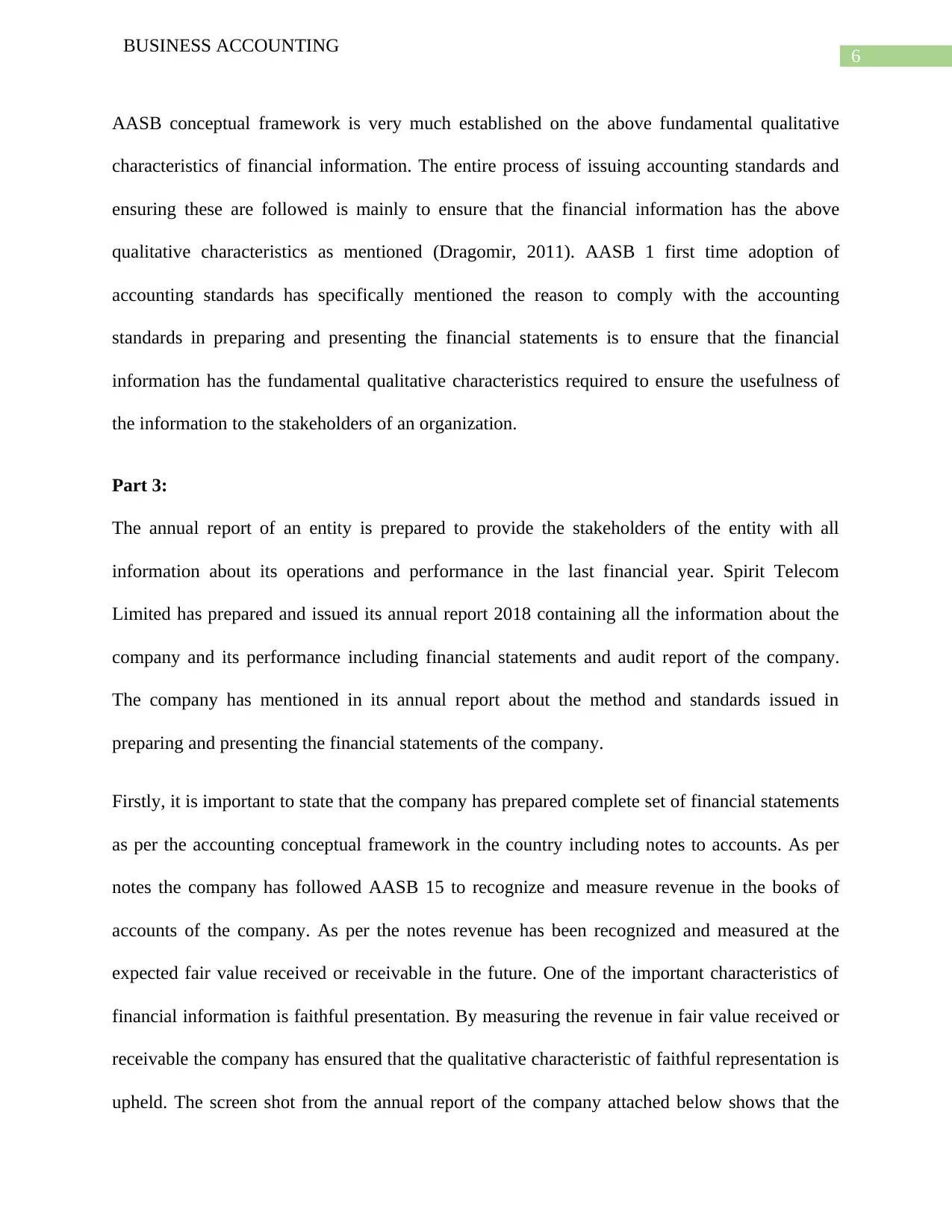

Inventory is one of the most important elements of financial information and must be properly

accounted for in the books of accounts of an organization. Inventories must be valued properly as

incorrect valuation of inventories could lead to misrepresentation of financial performance as

well as position of an organization as at the end of a financial year. AASB 102 provides that an

entity must value its inventory at the lower of cost or net realizable value. As a result any entity

if not comply with the requirements of AASB 102 to value the closing inventories would not

comply with the concept of maintaining qualitative characteristics of financial information

(Samuel, 2018). As per the annual report 2018 of Spirit Telecom, the inventories of the company

has been valued at lower of cost and net realizable value to comply with the requirements of

AASB 102. Hence, two of the most important elements of financial statements have been

recorded as per the applicable accounting standards to improve the qualitative characteristics of

financial information. Using snipping tools the extract of annual report of the company is

attached below to assess the compliance with AASB in this regard.

BUSINESS ACCOUNTING

company has complied with AASB 15 (Financial Accounting and Reporting Standards for

Private Entities, 2006).

Inventory is one of the most important elements of financial information and must be properly

accounted for in the books of accounts of an organization. Inventories must be valued properly as

incorrect valuation of inventories could lead to misrepresentation of financial performance as

well as position of an organization as at the end of a financial year. AASB 102 provides that an

entity must value its inventory at the lower of cost or net realizable value. As a result any entity

if not comply with the requirements of AASB 102 to value the closing inventories would not

comply with the concept of maintaining qualitative characteristics of financial information

(Samuel, 2018). As per the annual report 2018 of Spirit Telecom, the inventories of the company

has been valued at lower of cost and net realizable value to comply with the requirements of

AASB 102. Hence, two of the most important elements of financial statements have been

recorded as per the applicable accounting standards to improve the qualitative characteristics of

financial information. Using snipping tools the extract of annual report of the company is

attached below to assess the compliance with AASB in this regard.

8

BUSINESS ACCOUNTING

Hence, it is clear from the verification of revenue and inventories stated in the financial

statements of the company that the company has followed AASB to ensure these the financial

information has all the qualitative characteristics necessary to be useful to the stakeholders of the

company.

Part 4:

The investors and securities market are external stakeholders of an organization they have very

limited sources available to gather credible financial information about a company. One of the

main sources to get financial information about an organization for these external stakeholders is

the annual report of the company. These stakeholders take important decisions affecting their

interests in the company by using the financial information provided in the annual report. In case

of Spirit Telecom Limited let’s analyze the reaction of the securities market investors to the

information provided in the annual report of the company (Spraakman and Jackling, 2014).

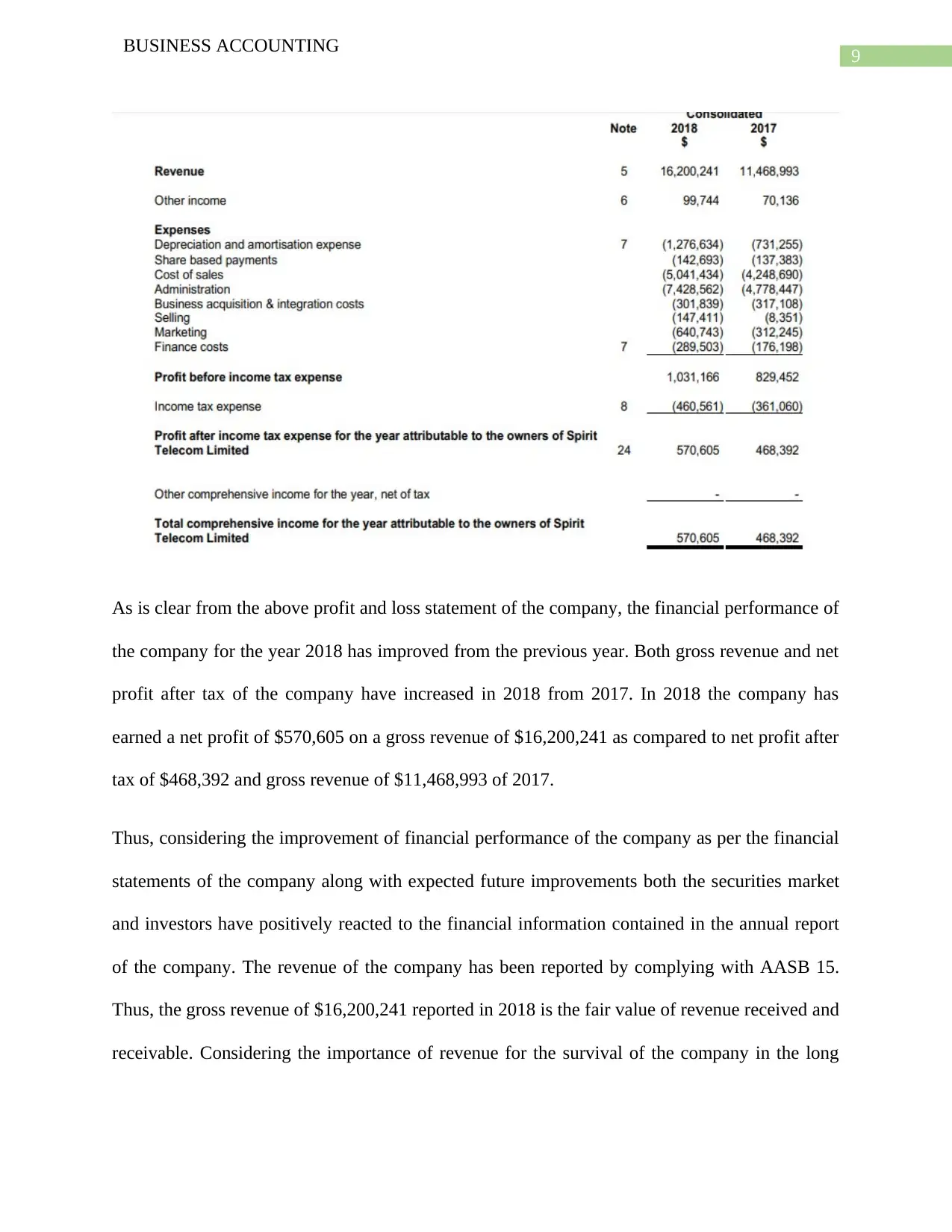

Extract below shows the statement of profit and loss of the company as at the end of the financial

year 2018 along with comparative figures of preceding year 2017.

BUSINESS ACCOUNTING

Hence, it is clear from the verification of revenue and inventories stated in the financial

statements of the company that the company has followed AASB to ensure these the financial

information has all the qualitative characteristics necessary to be useful to the stakeholders of the

company.

Part 4:

The investors and securities market are external stakeholders of an organization they have very

limited sources available to gather credible financial information about a company. One of the

main sources to get financial information about an organization for these external stakeholders is

the annual report of the company. These stakeholders take important decisions affecting their

interests in the company by using the financial information provided in the annual report. In case

of Spirit Telecom Limited let’s analyze the reaction of the securities market investors to the

information provided in the annual report of the company (Spraakman and Jackling, 2014).

Extract below shows the statement of profit and loss of the company as at the end of the financial

year 2018 along with comparative figures of preceding year 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

BUSINESS ACCOUNTING

As is clear from the above profit and loss statement of the company, the financial performance of

the company for the year 2018 has improved from the previous year. Both gross revenue and net

profit after tax of the company have increased in 2018 from 2017. In 2018 the company has

earned a net profit of $570,605 on a gross revenue of $16,200,241 as compared to net profit after

tax of $468,392 and gross revenue of $11,468,993 of 2017.

Thus, considering the improvement of financial performance of the company as per the financial

statements of the company along with expected future improvements both the securities market

and investors have positively reacted to the financial information contained in the annual report

of the company. The revenue of the company has been reported by complying with AASB 15.

Thus, the gross revenue of $16,200,241 reported in 2018 is the fair value of revenue received and

receivable. Considering the importance of revenue for the survival of the company in the long

BUSINESS ACCOUNTING

As is clear from the above profit and loss statement of the company, the financial performance of

the company for the year 2018 has improved from the previous year. Both gross revenue and net

profit after tax of the company have increased in 2018 from 2017. In 2018 the company has

earned a net profit of $570,605 on a gross revenue of $16,200,241 as compared to net profit after

tax of $468,392 and gross revenue of $11,468,993 of 2017.

Thus, considering the improvement of financial performance of the company as per the financial

statements of the company along with expected future improvements both the securities market

and investors have positively reacted to the financial information contained in the annual report

of the company. The revenue of the company has been reported by complying with AASB 15.

Thus, the gross revenue of $16,200,241 reported in 2018 is the fair value of revenue received and

receivable. Considering the importance of revenue for the survival of the company in the long

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BUSINESS ACCOUNTING

run the increase in revenue has certainly motivated the investors to invest in the shares of the

company. This has certainly influenced the securities market positively (Stevenson, 2012).

Similarly, the fact that the company has valued its inventories at lower of cost and net realizable

value as per AASB 102 is a matter that has certainly influenced the net profit of the company as

reported in the statement of profit and loss. The profit after tax for the company in 2018 is

$570,605 has also positively influenced the behavior of the investors as well as that of the

securities market. Thus, complying with accounting standards to improve the quality of financial

reporting is certainly essential to the proper disclosure of financial performance and position as

on a particular date (Walton, 2018).

Conclusion:

Discussion in this document shows the importance of financial information to have necessary

qualitative characteristics to be useful to the users of financial information. The accounting

standards issued in the country is in line with the conceptual framework of accounting and must

be followed to improve the quality of financial reporting. In case of Spirit Telecom Limited the

annual report of the company confirms that the financial statements of the company have been

complied with the accounting standards in the country.

BUSINESS ACCOUNTING

run the increase in revenue has certainly motivated the investors to invest in the shares of the

company. This has certainly influenced the securities market positively (Stevenson, 2012).

Similarly, the fact that the company has valued its inventories at lower of cost and net realizable

value as per AASB 102 is a matter that has certainly influenced the net profit of the company as

reported in the statement of profit and loss. The profit after tax for the company in 2018 is

$570,605 has also positively influenced the behavior of the investors as well as that of the

securities market. Thus, complying with accounting standards to improve the quality of financial

reporting is certainly essential to the proper disclosure of financial performance and position as

on a particular date (Walton, 2018).

Conclusion:

Discussion in this document shows the importance of financial information to have necessary

qualitative characteristics to be useful to the users of financial information. The accounting

standards issued in the country is in line with the conceptual framework of accounting and must

be followed to improve the quality of financial reporting. In case of Spirit Telecom Limited the

annual report of the company confirms that the financial statements of the company have been

complied with the accounting standards in the country.

11

BUSINESS ACCOUNTING

References:

Barker, R. and Teixeira, A. (2018). Gaps in the IFRS Conceptual Framework. Accounting in

Europe, 15(2), pp.153-166.

BOYMAL, D. (2007). The Work Program and Priorities of the AASB. Australian Accounting

Review, 17(42), pp.3-7.

Craig, R., Smieliauskas, W. and Amernic, J. (2016). Estimation Uncertainty and the IASB's

Proposed Conceptual Framework. Australian Accounting Review, 27(1), pp.112-114.

Dennis, I. (2018). What is a Conceptual Framework for Financial Reporting?. Accounting in

Europe, 15(3), pp.374-401.

Dragomir, V. (2011). Accounting for sustainability: the quest for a conceptual

framework. International Journal of Critical Accounting, 3(4), p.384.

Financial Accounting and Reporting Standards for Private Entities. (2006). Accounting Horizons,

20(2), pp.179-194.

Samuel, S. (2018). A conceptual framework for teaching management accounting. Journal of

Accounting Education, 44(54), pp.25-34.

Spraakman, G. and Jackling, B. (2014). A Conceptual Framework for Learning Management

Accounting. Accounting Perspectives, 13(1), pp.61-81.

Stevenson, K. (2012). The Changing IASB and AASB Relationship. Australian Accounting

Review, 22(3), pp.239-243.

BUSINESS ACCOUNTING

References:

Barker, R. and Teixeira, A. (2018). Gaps in the IFRS Conceptual Framework. Accounting in

Europe, 15(2), pp.153-166.

BOYMAL, D. (2007). The Work Program and Priorities of the AASB. Australian Accounting

Review, 17(42), pp.3-7.

Craig, R., Smieliauskas, W. and Amernic, J. (2016). Estimation Uncertainty and the IASB's

Proposed Conceptual Framework. Australian Accounting Review, 27(1), pp.112-114.

Dennis, I. (2018). What is a Conceptual Framework for Financial Reporting?. Accounting in

Europe, 15(3), pp.374-401.

Dragomir, V. (2011). Accounting for sustainability: the quest for a conceptual

framework. International Journal of Critical Accounting, 3(4), p.384.

Financial Accounting and Reporting Standards for Private Entities. (2006). Accounting Horizons,

20(2), pp.179-194.

Samuel, S. (2018). A conceptual framework for teaching management accounting. Journal of

Accounting Education, 44(54), pp.25-34.

Spraakman, G. and Jackling, B. (2014). A Conceptual Framework for Learning Management

Accounting. Accounting Perspectives, 13(1), pp.61-81.

Stevenson, K. (2012). The Changing IASB and AASB Relationship. Australian Accounting

Review, 22(3), pp.239-243.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.