ACC00724 Accounting for Managers: Cash Cycle, Decisions & Analysis

VerifiedAdded on 2023/06/07

|12

|1664

|426

Report

AI Summary

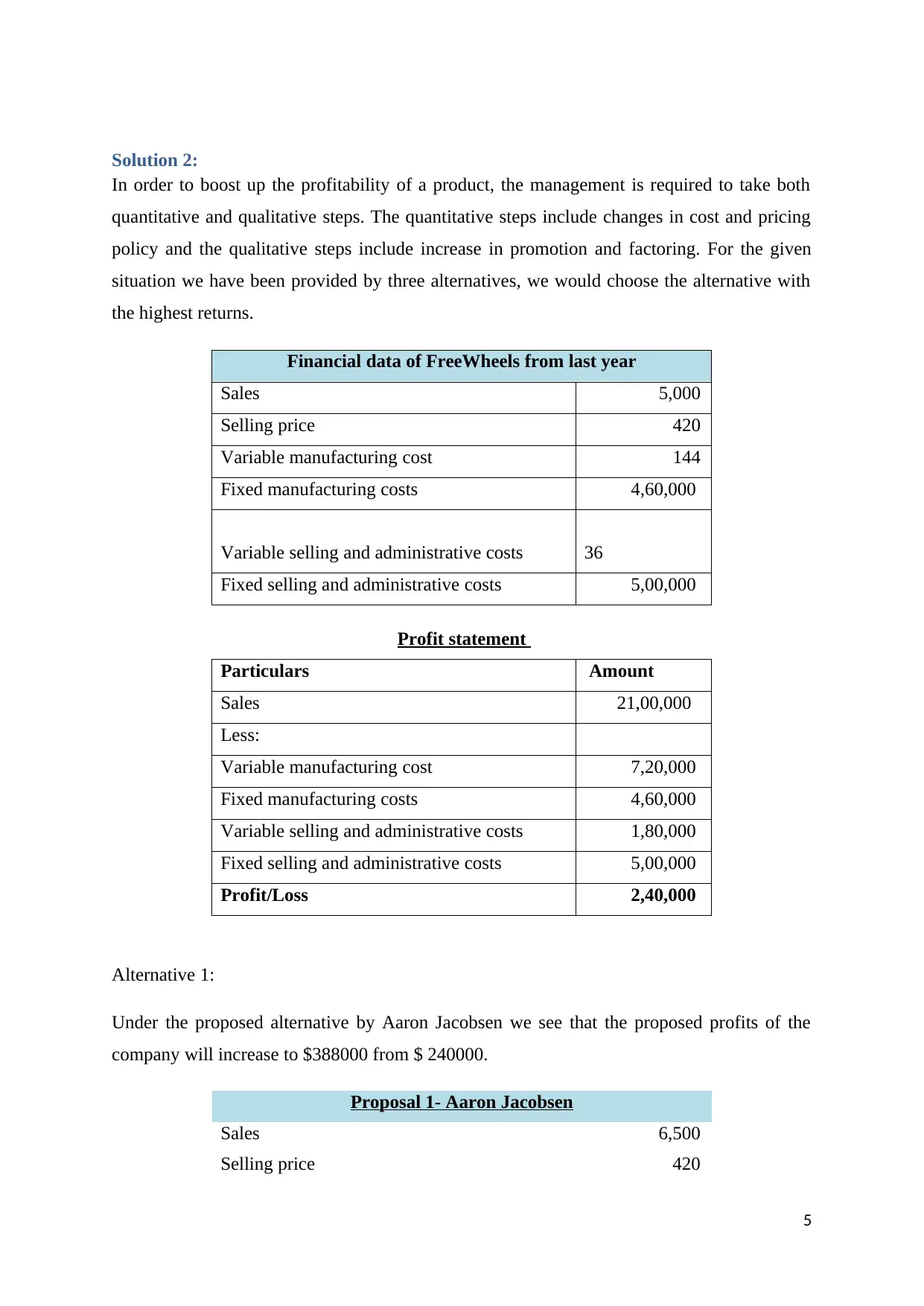

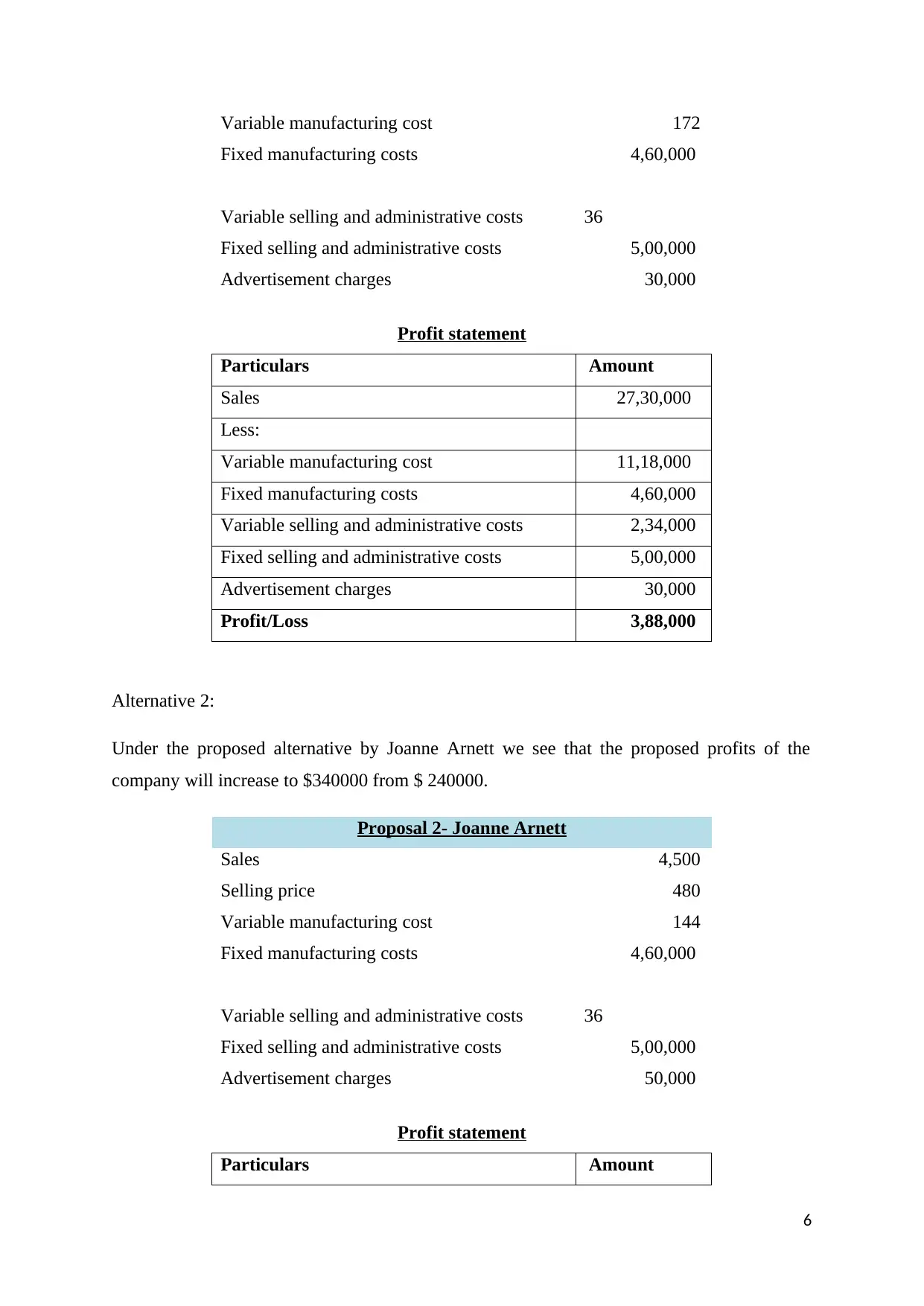

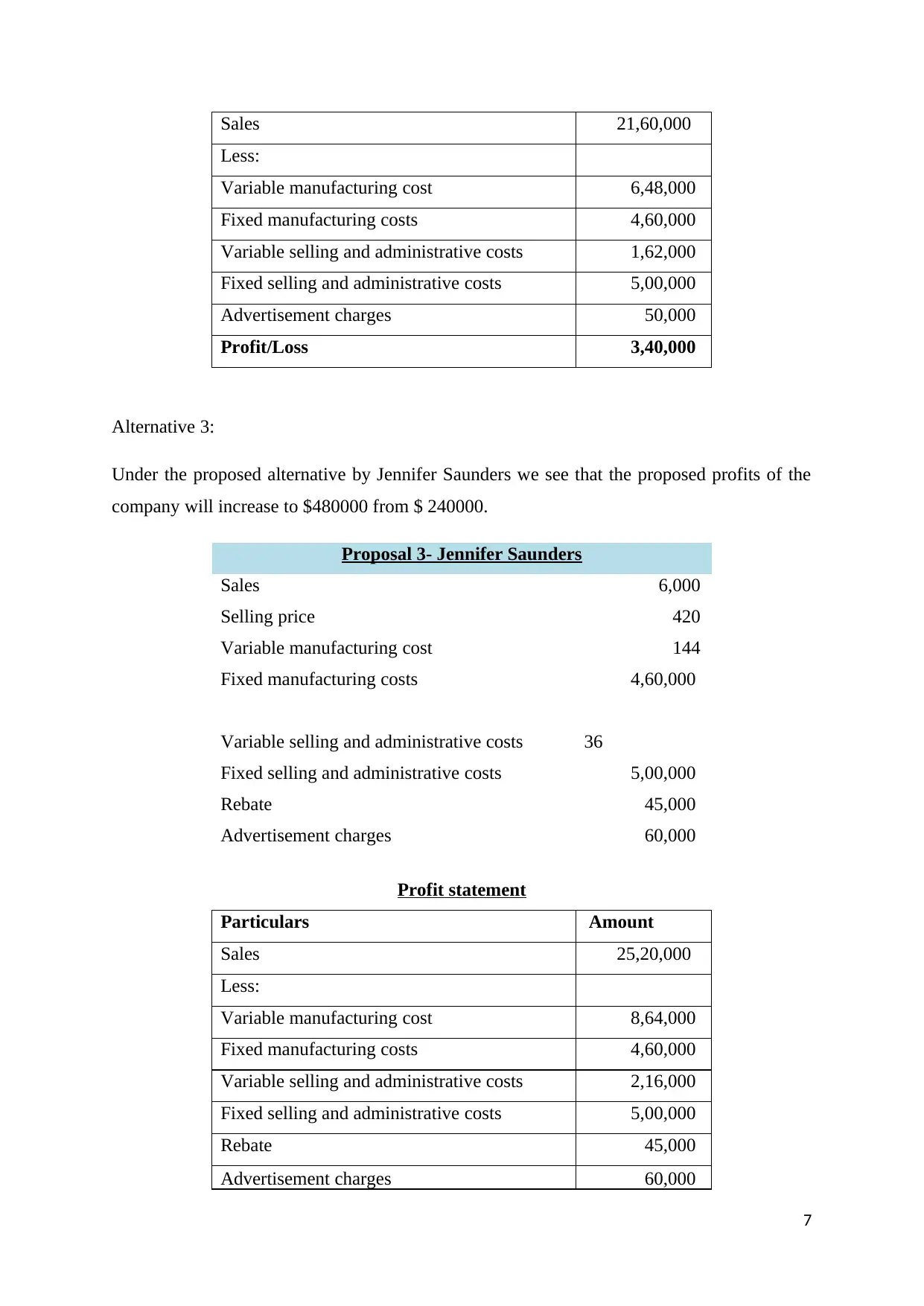

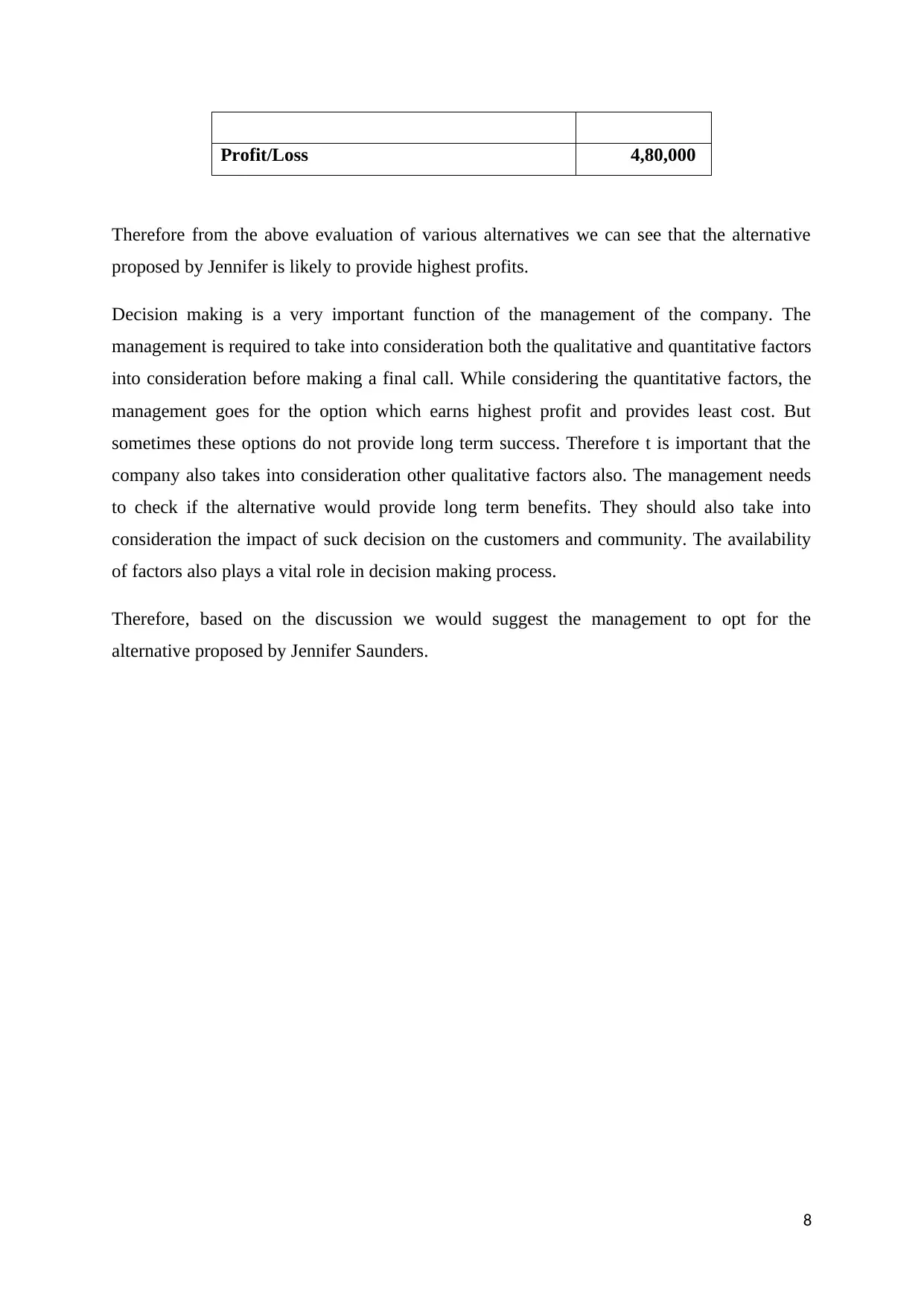

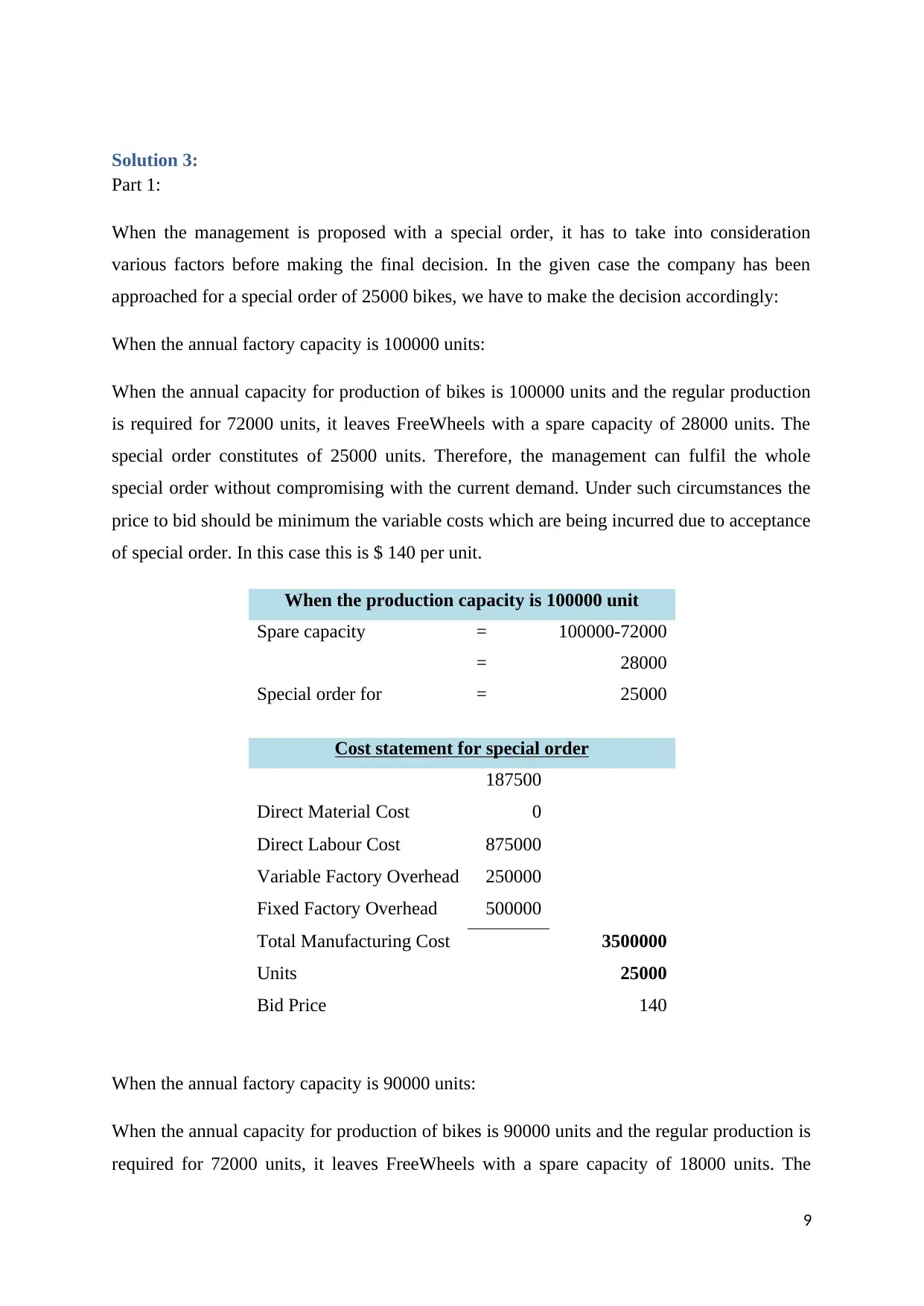

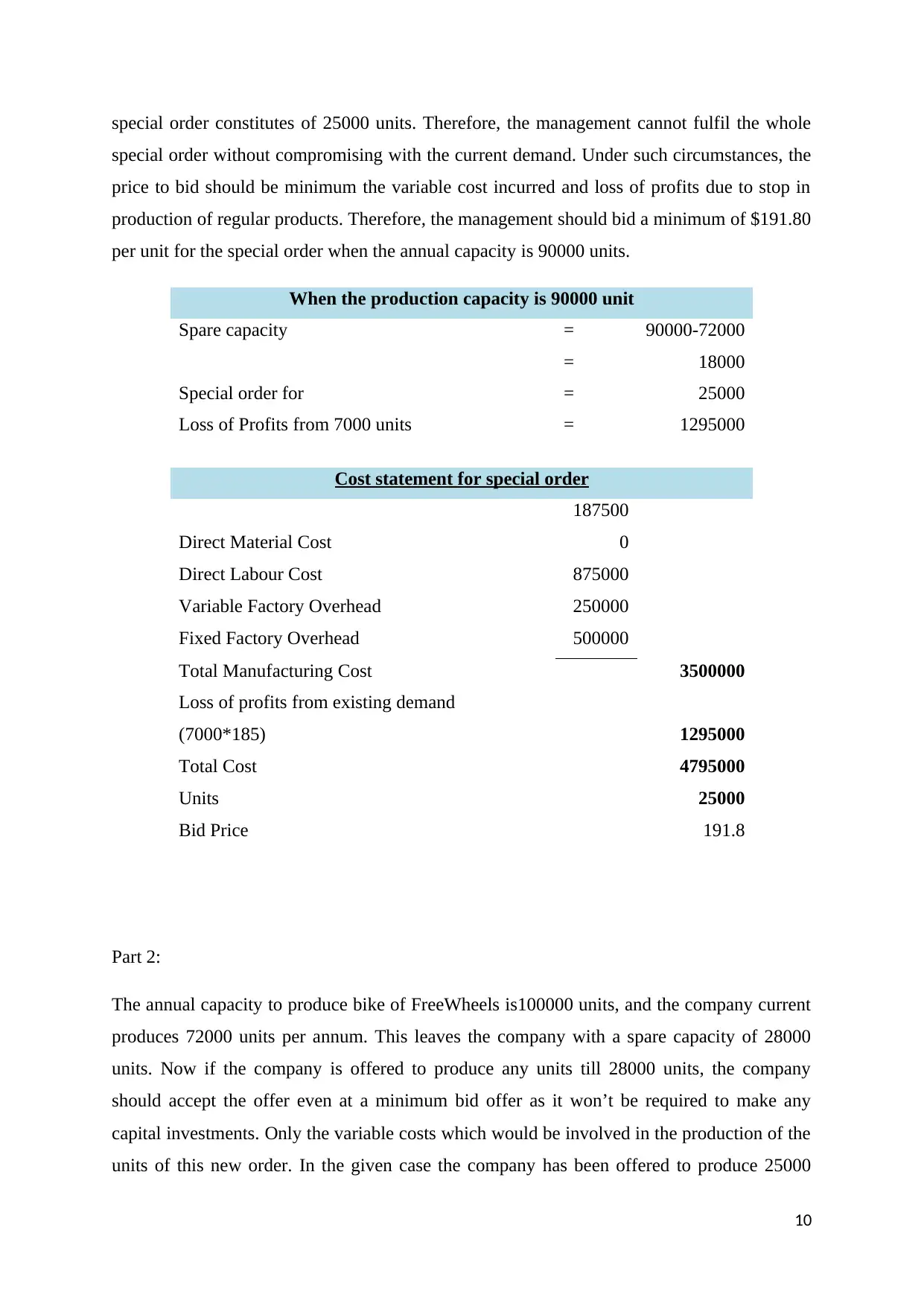

This report provides solutions to accounting problems related to cash cycle analysis, profitability improvement, and special order decisions. The cash cycle of Cash Convertors International Limited is calculated for five years, and the trends in cash flows are evaluated. The report also analyzes three alternative proposals to boost the profitability of Telesmart Ltd, recommending Jennifer Saunders' proposal. Furthermore, it assesses a special order for FreeWheels, determining the minimum bid price under different production capacities. The analysis considers both quantitative and qualitative factors for decision-making. Desklib offers a variety of solved assignments and past papers to aid students in their studies.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.