ACC00724 S2 2018 - Cash Flow, Profitability Analysis: Managers

VerifiedAdded on 2023/06/09

|11

|1350

|317

Report

AI Summary

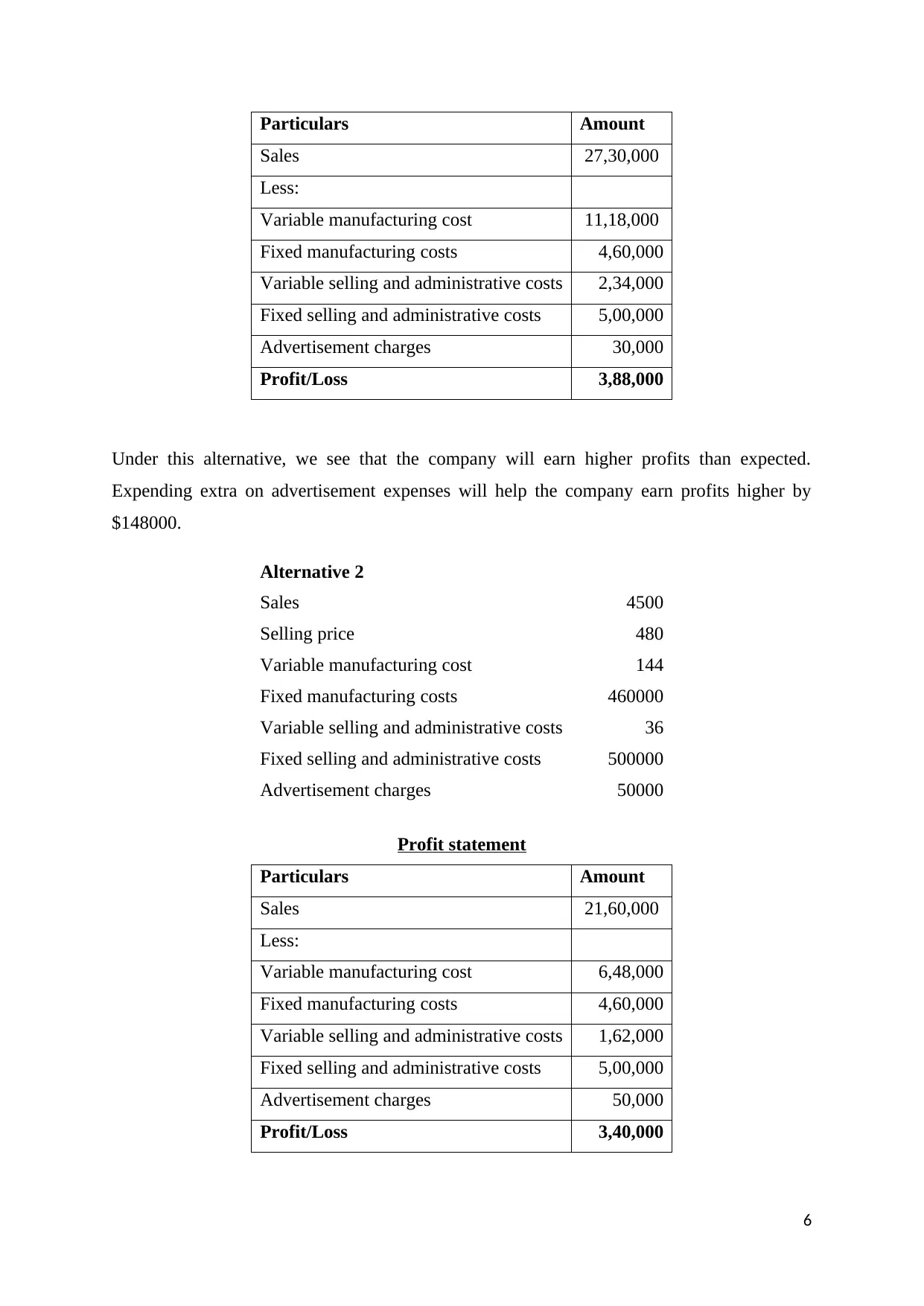

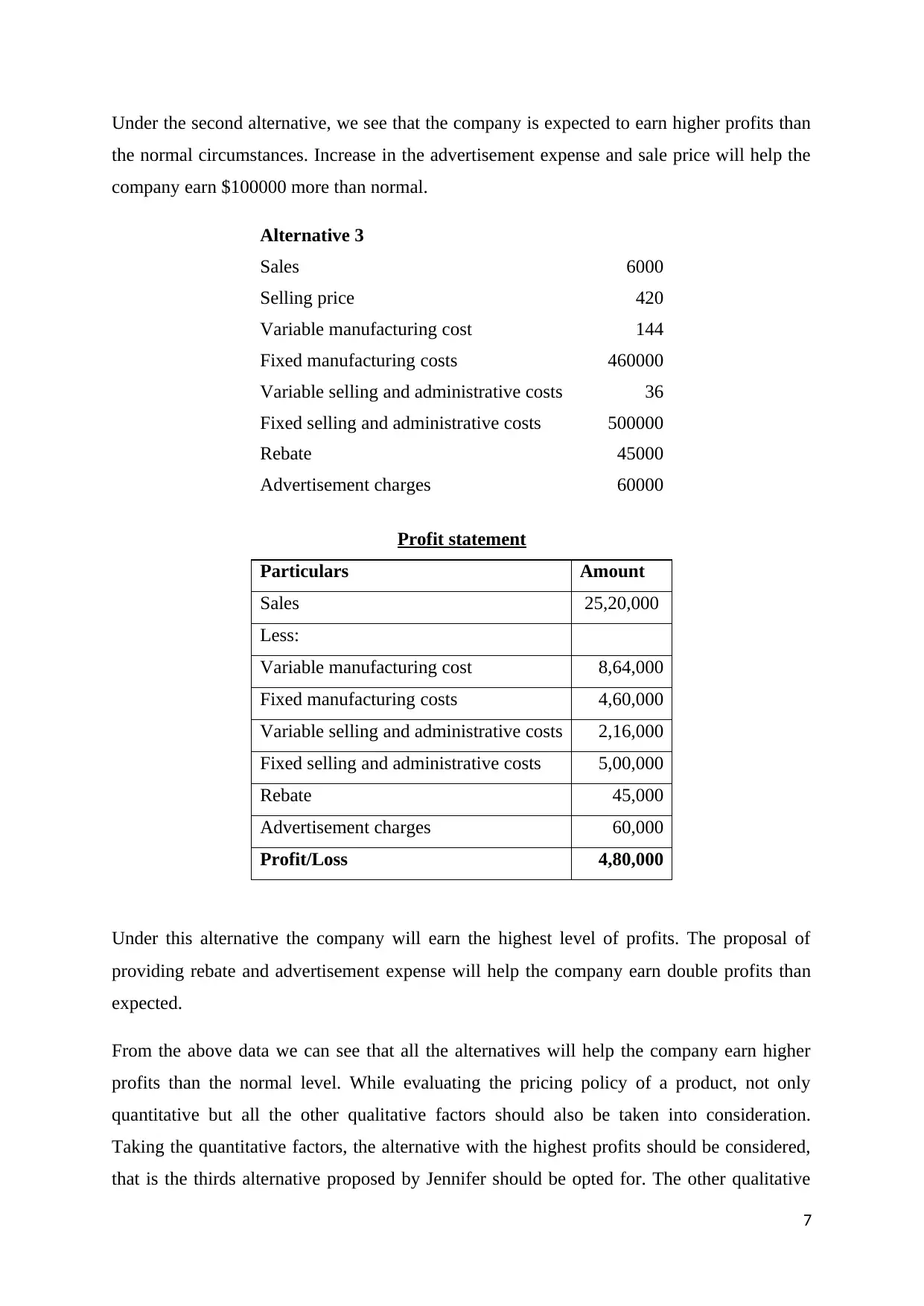

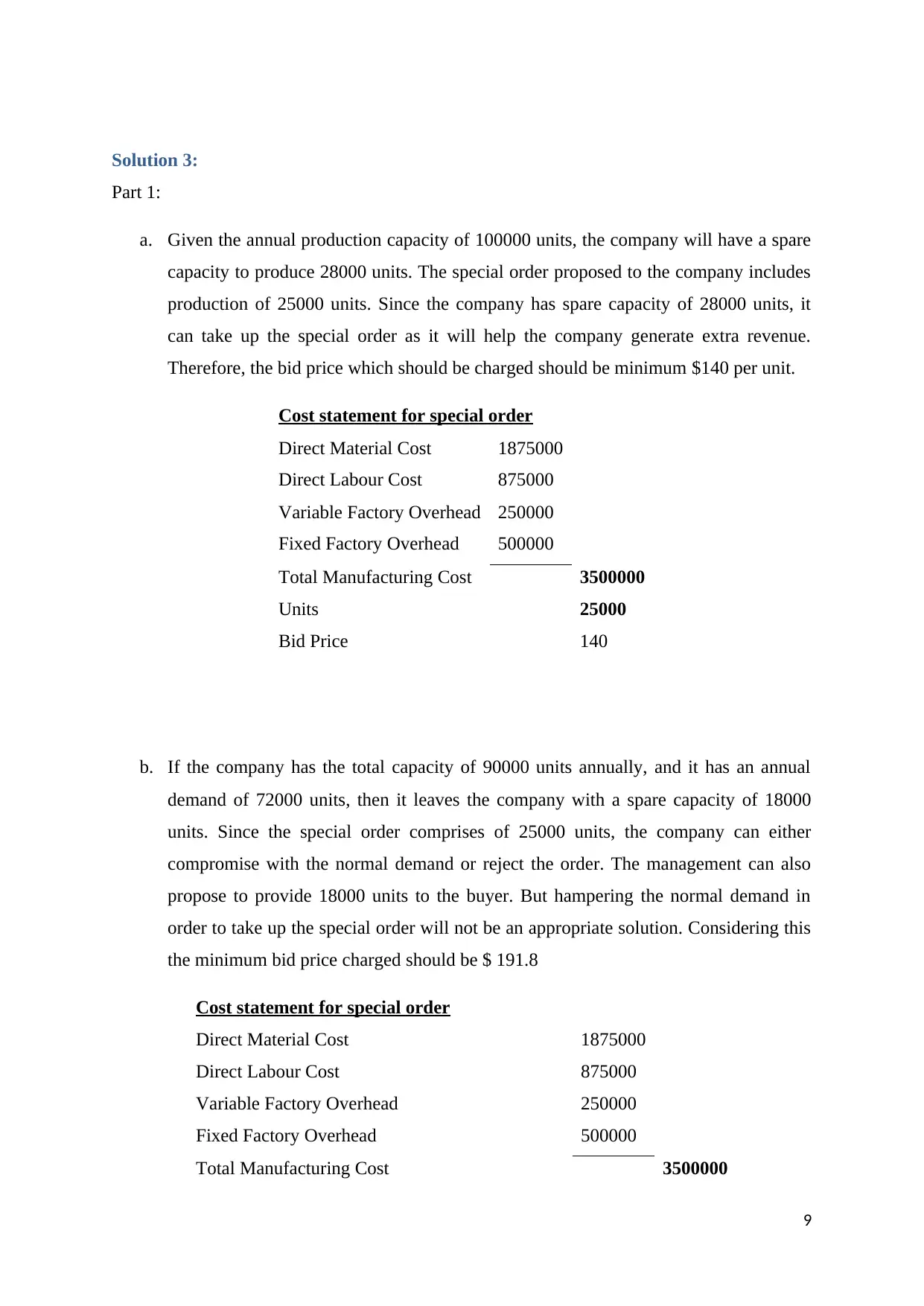

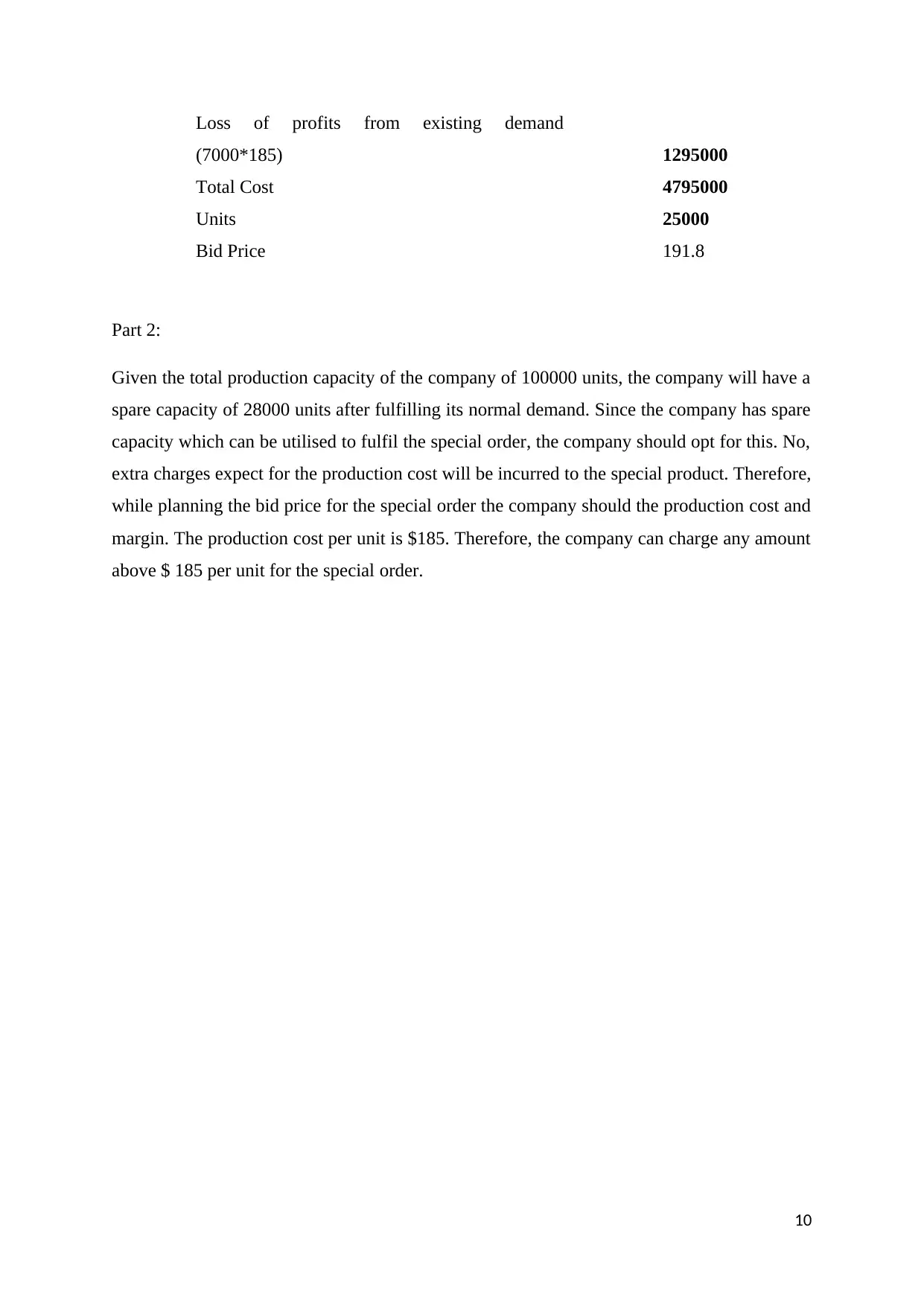

This report provides a detailed analysis of cash flow and profitability for a company, utilizing data from its annual reports and financial statements. It includes a calculation of the company's cash cycle over five years, an evaluation of cash flow trends, and an assessment of different strategies to enhance profitability. The analysis covers various scenarios, including changes in sales volume, pricing, and advertising expenses, to determine the most effective approach for maximizing profits. Furthermore, the report examines a special order scenario, considering factors such as production capacity and potential impact on existing demand, to determine an appropriate bid price. The report concludes with recommendations based on both quantitative and qualitative factors, emphasizing the importance of balancing profitability with product quality and effective promotional campaigns. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.