ACC00724: Report on Profitability Improvement Proposals Analysis

VerifiedAdded on 2023/04/22

|7

|1796

|369

Report

AI Summary

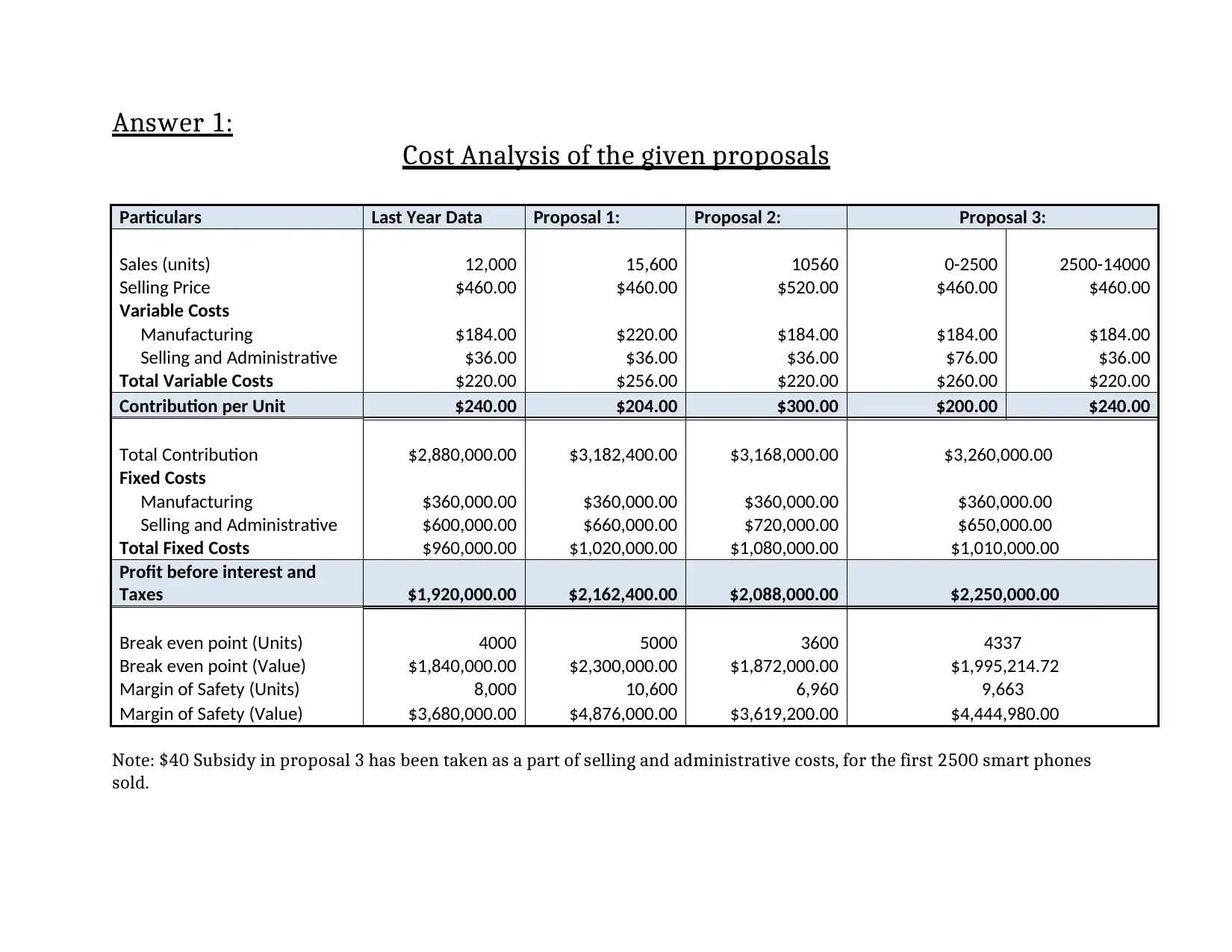

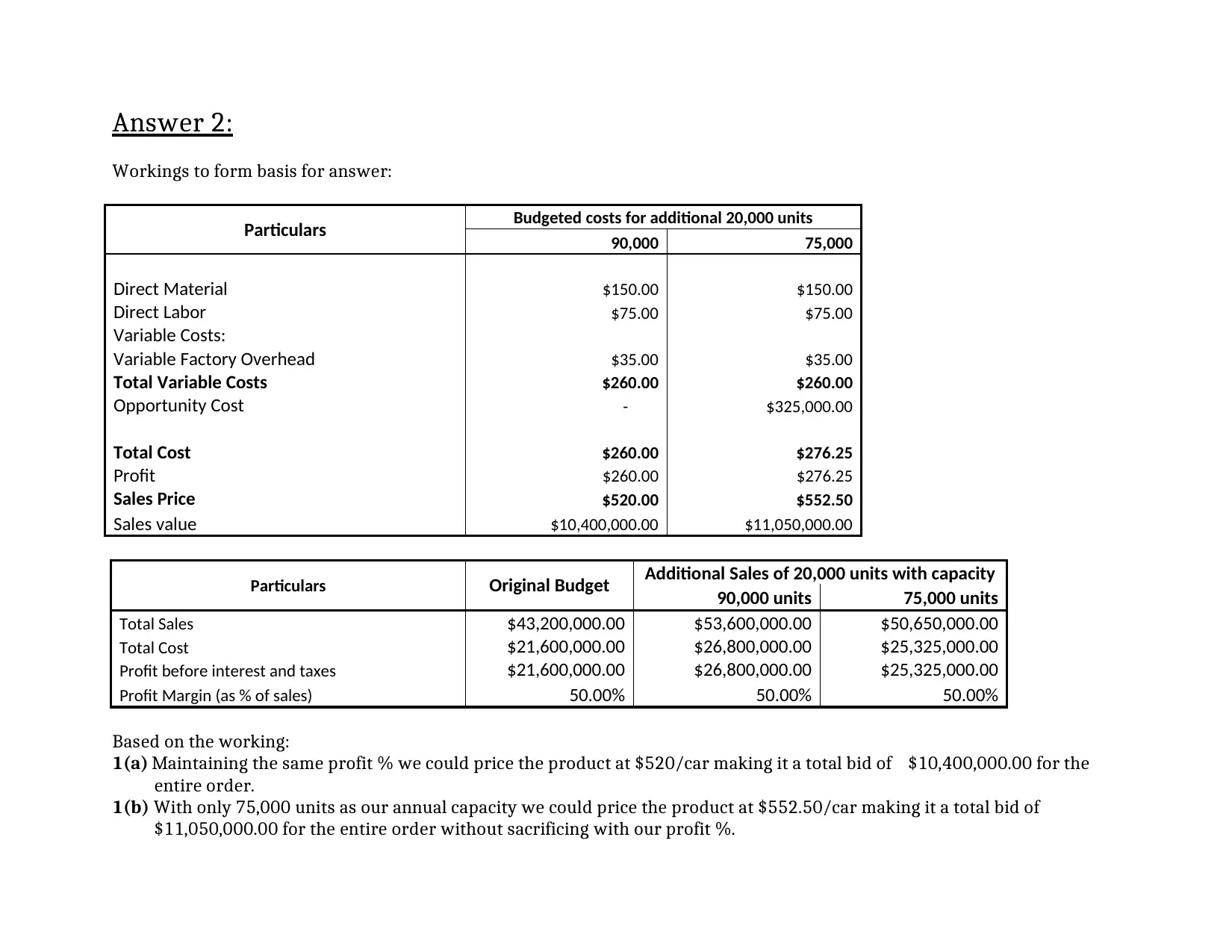

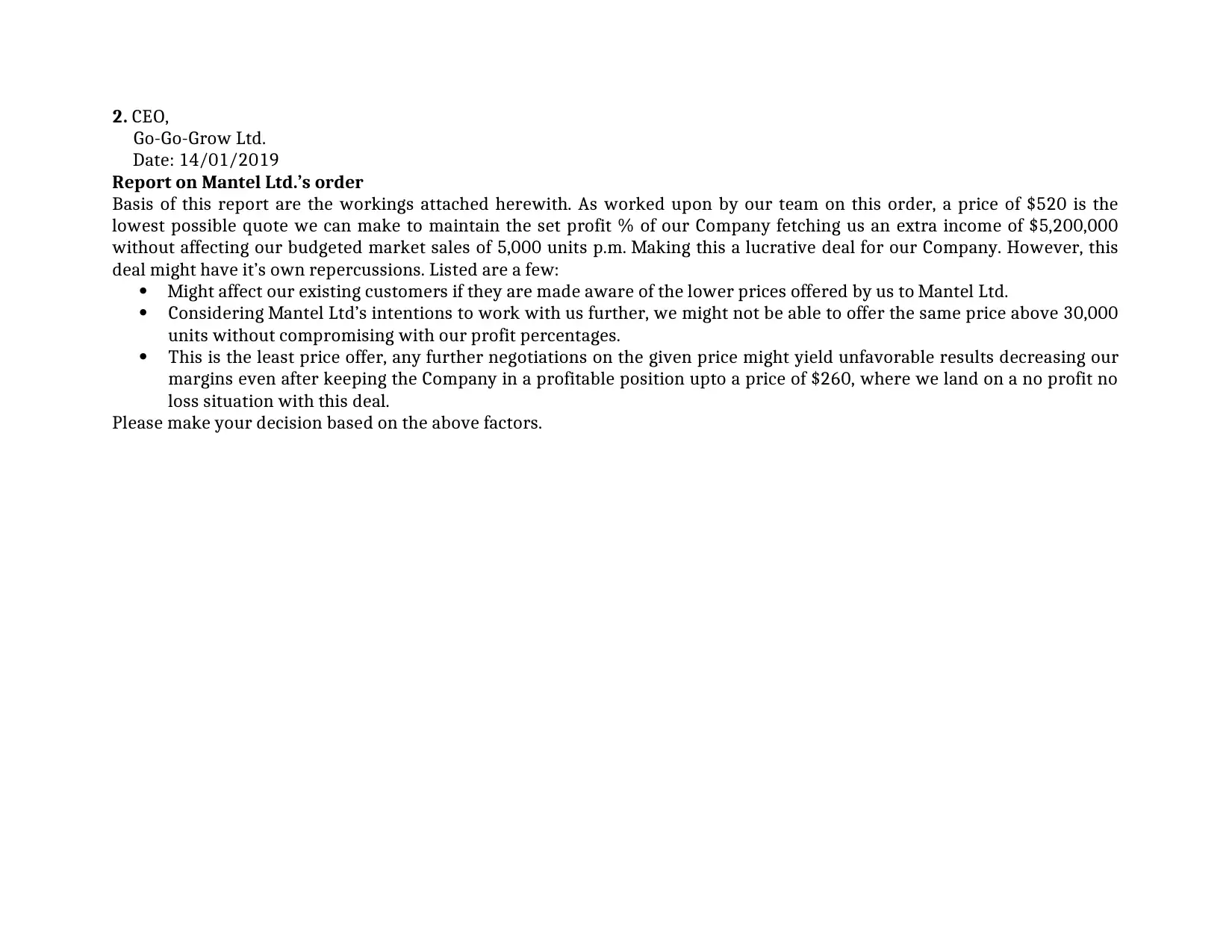

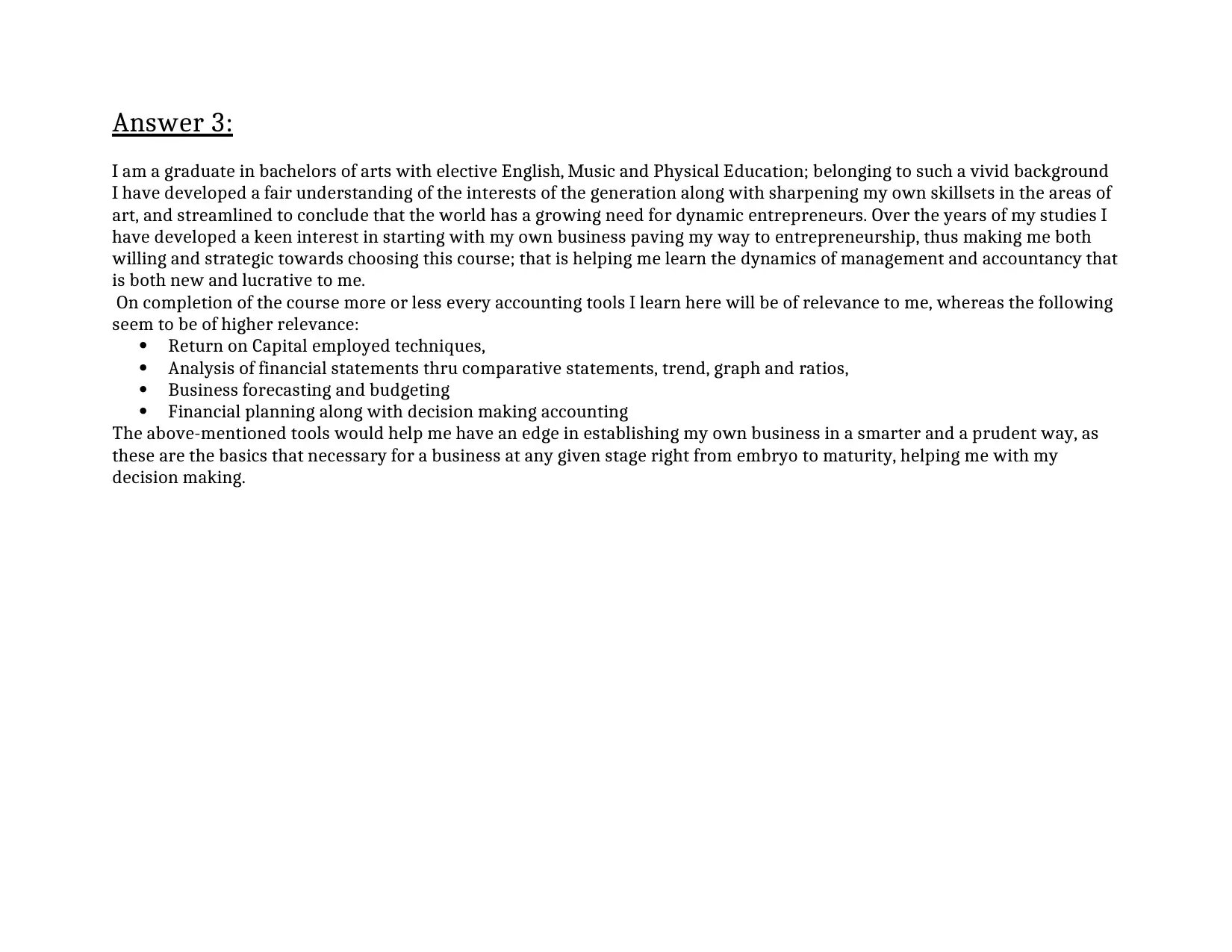

This assignment is a report evaluating several proposals aimed at improving the profitability of Pacific Telemet Ltd.'s smartphone business. It includes a detailed cost analysis of three different proposals, examining their impact on sales, variable costs, fixed costs, contribution margins, break-even points, and margin of safety. The analysis considers both quantitative data and qualitative factors, such as the potential impact of product quality improvements, the adoption of a skimming strategy, and the effects of promotional discounting. The report also includes a discussion on pricing strategies for a potential bulk order, considering capacity constraints and profit margin targets. Finally, the assignment reflects on the relevance of accounting tools learned in a management course to the student's entrepreneurial aspirations, highlighting the importance of financial analysis, budgeting, and forecasting for business decision-making. This document is available on Desklib, a platform offering a wide range of study resources including past papers and solved assignments.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.