ACC09901 Corporate Financial Management: A.G. Barr Plc Analysis

VerifiedAdded on 2023/06/14

|18

|3789

|262

Report

AI Summary

This report provides a comprehensive financial analysis of A.G. Barr Plc, prepared for the Amicable Pension Fund. It assesses the company's strategic direction, key business activities, and financial performance over a five-year period, including growth rates, cash conversion cycles, and financial ratios. The report identifies future business opportunities and risks, such as changing consumer preferences and the impact of sugar tax. It also evaluates A.G. Barr Plc's financial strengths and weaknesses, including its diverse portfolio and risk management framework. The analysis incorporates the Efficient Market Hypothesis and examines stock market pricing efficiency, concluding with investment recommendations based on valuation methods like the dividend discount model and net asset value.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student

Name of the University

Authors Note

Course ID

Corporate Finance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE FINANCE

Table of Contents

Introduction:...............................................................................................................................2

Strategic Direction:....................................................................................................................2

Vital features of business strategies:..........................................................................................3

Five year trend performance:.....................................................................................................3

Yearly percentage growth rates:.................................................................................................4

Cash conversion cycle:...............................................................................................................4

Financial ratios:..........................................................................................................................5

Future business opportunities and risk for A.G. Barr Plc:.........................................................5

Financial performance:...............................................................................................................6

Financial strength and weakness:...............................................................................................6

Efficiency Market Hypothesis:..................................................................................................8

Stock Market Pricing Efficiency in A.G. Barr Plc Share Price:................................................8

Semi strong market form of market efficiency:.........................................................................9

Justification and description of assumptions:..........................................................................10

Usefulness and limitations of valuation methods:...................................................................11

Share price information............................................................................................................11

Conclusion:..............................................................................................................................13

Reference List:.........................................................................................................................15

Table of Contents

Introduction:...............................................................................................................................2

Strategic Direction:....................................................................................................................2

Vital features of business strategies:..........................................................................................3

Five year trend performance:.....................................................................................................3

Yearly percentage growth rates:.................................................................................................4

Cash conversion cycle:...............................................................................................................4

Financial ratios:..........................................................................................................................5

Future business opportunities and risk for A.G. Barr Plc:.........................................................5

Financial performance:...............................................................................................................6

Financial strength and weakness:...............................................................................................6

Efficiency Market Hypothesis:..................................................................................................8

Stock Market Pricing Efficiency in A.G. Barr Plc Share Price:................................................8

Semi strong market form of market efficiency:.........................................................................9

Justification and description of assumptions:..........................................................................10

Usefulness and limitations of valuation methods:...................................................................11

Share price information............................................................................................................11

Conclusion:..............................................................................................................................13

Reference List:.........................................................................................................................15

2CORPORATE FINANCE

Introduction:

A.G. Barr Plc is regarded as the soft drink producer from Scotland that has its

operational base in Cumbernauld. A.G. Barr Plc is known as the popular manufacturer of

Scottish drink (Agbarr.Co.Uk, 2018). The company is listed on the London stock exchange

and it is viewed as the constituent of FTSE 250 Index. The present report is takes into

consideration the determination of strategic decision of A.G. Barr Plc by defining the main

activities carried out by the company together with the necessary features of the strategy

undertaken. The analysis will focus on the business opportunities and risk facing the

company with the emphasis on the operating performance of the firm.

The current report will be addressing the Amicable Pension Fund to take into the

account the details of financial performance over the period of five years. The study will refer

to stock market pricing efficient and efficient market hypothesis would be performed to

determine the market efficiency of A.G. Barr Plc. Additional coverage will made in the share

price performance of the firm to offer brief commentary on the share performance and

suitable recommendations will be provided relating to investment prospect for Amicable

Pension Fund.

Strategic Direction:

The primary business activates of A.G. Barr Plc is associated with the production

capabilities, generating higher quality products all through the well-funded and operative

manufacturing location. The chief business functions of A.G. Barr Plc is related to sourcing

of raw materials throughout the world to create the packaging materials for continuous

improvement. A.G. Barr Plc has its fleet of around hundred vehicles that has long relation

with the vital distribution partners (Agbarr.Co.Uk, 2018). A.G. Barr Plc strives to provide

greater service to all the customers from small to big local outlets. A.G. Barr Plc has its

Introduction:

A.G. Barr Plc is regarded as the soft drink producer from Scotland that has its

operational base in Cumbernauld. A.G. Barr Plc is known as the popular manufacturer of

Scottish drink (Agbarr.Co.Uk, 2018). The company is listed on the London stock exchange

and it is viewed as the constituent of FTSE 250 Index. The present report is takes into

consideration the determination of strategic decision of A.G. Barr Plc by defining the main

activities carried out by the company together with the necessary features of the strategy

undertaken. The analysis will focus on the business opportunities and risk facing the

company with the emphasis on the operating performance of the firm.

The current report will be addressing the Amicable Pension Fund to take into the

account the details of financial performance over the period of five years. The study will refer

to stock market pricing efficient and efficient market hypothesis would be performed to

determine the market efficiency of A.G. Barr Plc. Additional coverage will made in the share

price performance of the firm to offer brief commentary on the share performance and

suitable recommendations will be provided relating to investment prospect for Amicable

Pension Fund.

Strategic Direction:

The primary business activates of A.G. Barr Plc is associated with the production

capabilities, generating higher quality products all through the well-funded and operative

manufacturing location. The chief business functions of A.G. Barr Plc is related to sourcing

of raw materials throughout the world to create the packaging materials for continuous

improvement. A.G. Barr Plc has its fleet of around hundred vehicles that has long relation

with the vital distribution partners (Agbarr.Co.Uk, 2018). A.G. Barr Plc strives to provide

greater service to all the customers from small to big local outlets. A.G. Barr Plc has its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE FINANCE

business operations through numerous roads to market its products. The primary business

activities of company is linked with the operating activities and effective distribution

networks with direct delivery to store channel.

Vital features of business strategies:

Taking account of vital business features of A.G. Barr Plc it provides the clarity of

purpose and reliability approach forms the best outcomes (Agbarr.Co.Uk, 2018). The vital

business features for A.G. Barr Plc are;

a. Flexible and effective business operations

b. Strongly differentiated brands

c. Innovating customer understanding

d. Partnership that promotes growth

e. The company leverages its business strength and commitment of its team.

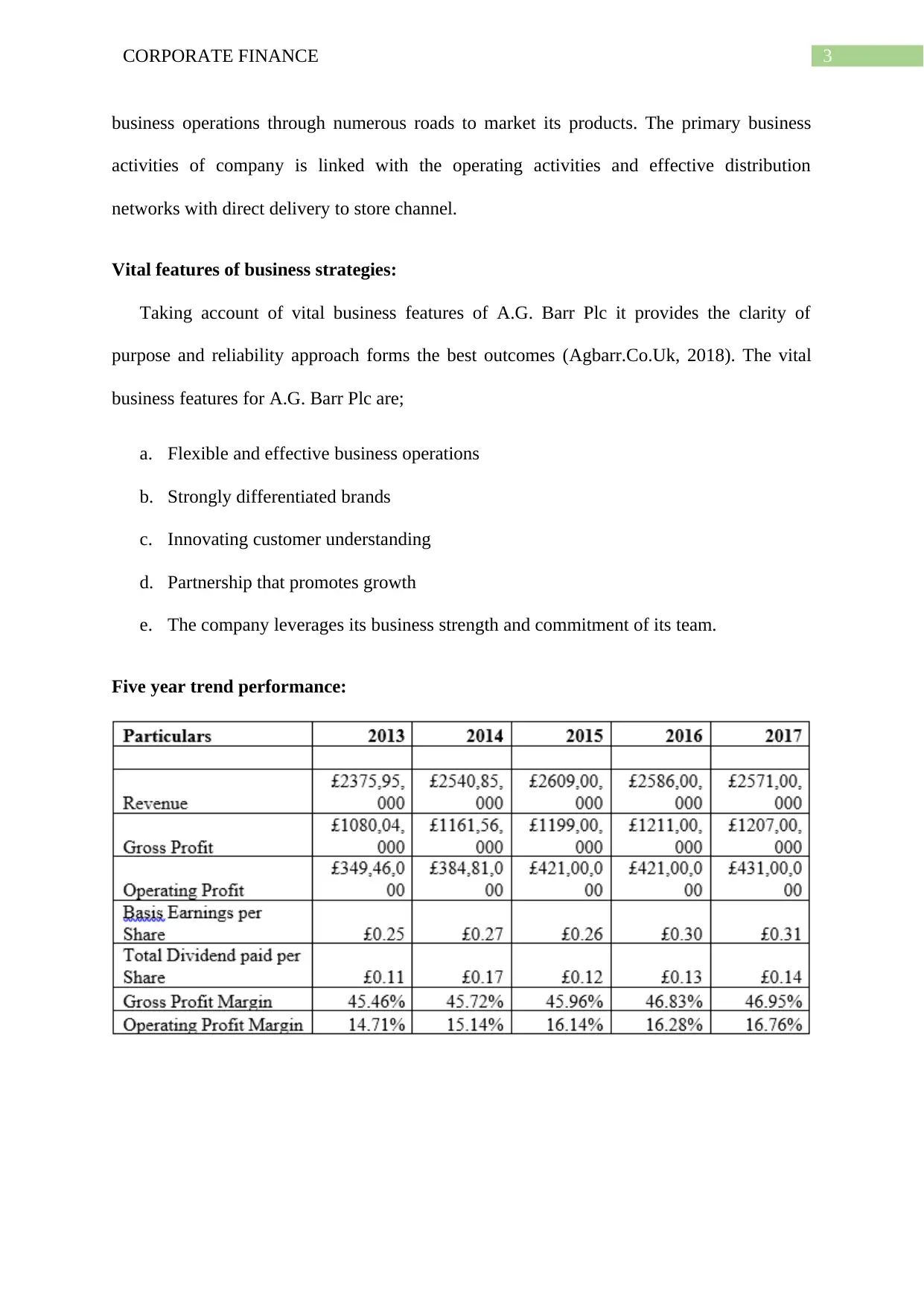

Five year trend performance:

business operations through numerous roads to market its products. The primary business

activities of company is linked with the operating activities and effective distribution

networks with direct delivery to store channel.

Vital features of business strategies:

Taking account of vital business features of A.G. Barr Plc it provides the clarity of

purpose and reliability approach forms the best outcomes (Agbarr.Co.Uk, 2018). The vital

business features for A.G. Barr Plc are;

a. Flexible and effective business operations

b. Strongly differentiated brands

c. Innovating customer understanding

d. Partnership that promotes growth

e. The company leverages its business strength and commitment of its team.

Five year trend performance:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE FINANCE

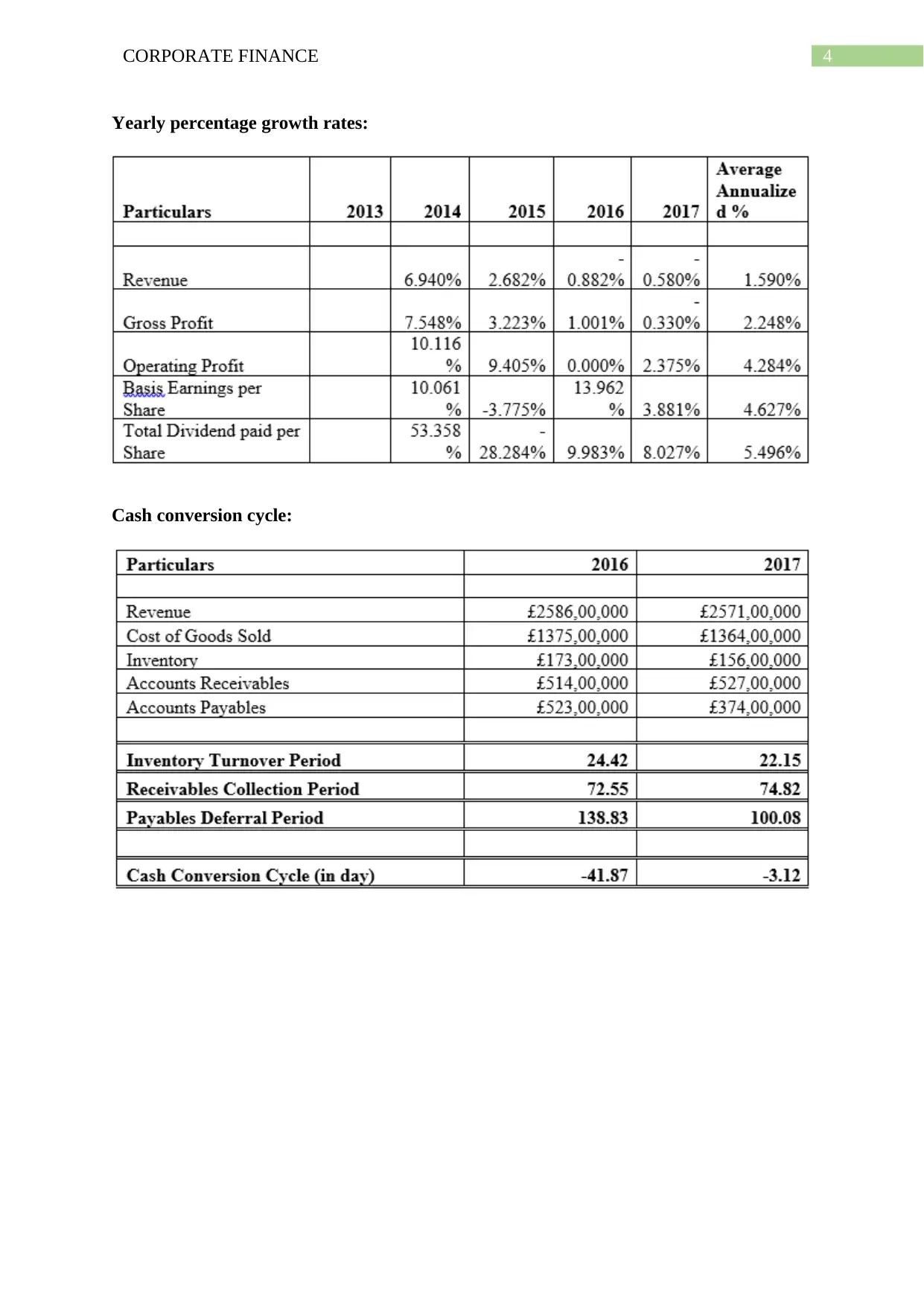

Yearly percentage growth rates:

Cash conversion cycle:

Yearly percentage growth rates:

Cash conversion cycle:

5CORPORATE FINANCE

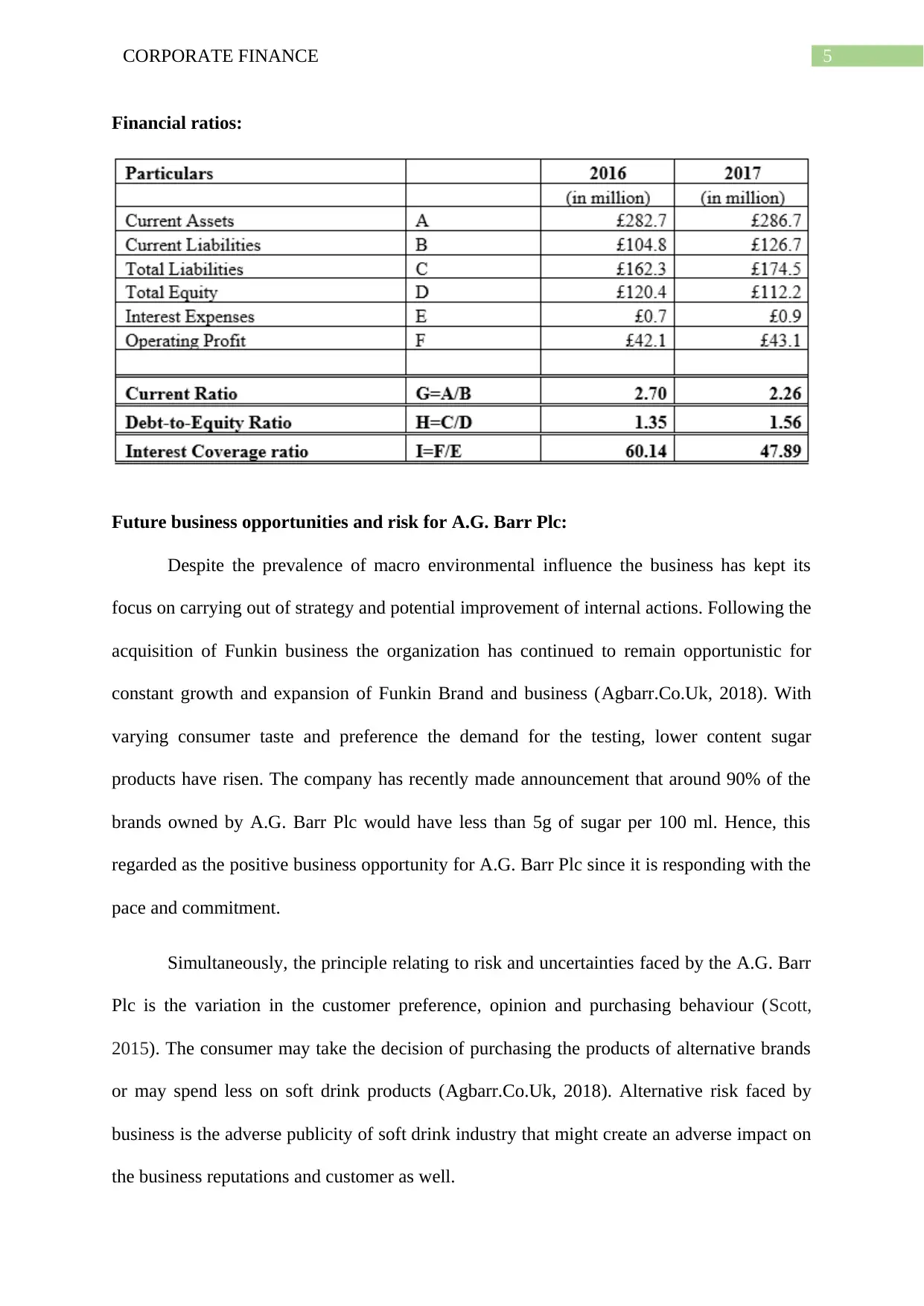

Financial ratios:

Future business opportunities and risk for A.G. Barr Plc:

Despite the prevalence of macro environmental influence the business has kept its

focus on carrying out of strategy and potential improvement of internal actions. Following the

acquisition of Funkin business the organization has continued to remain opportunistic for

constant growth and expansion of Funkin Brand and business (Agbarr.Co.Uk, 2018). With

varying consumer taste and preference the demand for the testing, lower content sugar

products have risen. The company has recently made announcement that around 90% of the

brands owned by A.G. Barr Plc would have less than 5g of sugar per 100 ml. Hence, this

regarded as the positive business opportunity for A.G. Barr Plc since it is responding with the

pace and commitment.

Simultaneously, the principle relating to risk and uncertainties faced by the A.G. Barr

Plc is the variation in the customer preference, opinion and purchasing behaviour (Scott,

2015). The consumer may take the decision of purchasing the products of alternative brands

or may spend less on soft drink products (Agbarr.Co.Uk, 2018). Alternative risk faced by

business is the adverse publicity of soft drink industry that might create an adverse impact on

the business reputations and customer as well.

Financial ratios:

Future business opportunities and risk for A.G. Barr Plc:

Despite the prevalence of macro environmental influence the business has kept its

focus on carrying out of strategy and potential improvement of internal actions. Following the

acquisition of Funkin business the organization has continued to remain opportunistic for

constant growth and expansion of Funkin Brand and business (Agbarr.Co.Uk, 2018). With

varying consumer taste and preference the demand for the testing, lower content sugar

products have risen. The company has recently made announcement that around 90% of the

brands owned by A.G. Barr Plc would have less than 5g of sugar per 100 ml. Hence, this

regarded as the positive business opportunity for A.G. Barr Plc since it is responding with the

pace and commitment.

Simultaneously, the principle relating to risk and uncertainties faced by the A.G. Barr

Plc is the variation in the customer preference, opinion and purchasing behaviour (Scott,

2015). The consumer may take the decision of purchasing the products of alternative brands

or may spend less on soft drink products (Agbarr.Co.Uk, 2018). Alternative risk faced by

business is the adverse publicity of soft drink industry that might create an adverse impact on

the business reputations and customer as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE FINANCE

Financial performance:

Over the last twelve months A.G. Barr Plc has made considerable amount of progress

with strong financial earnings in spite of the volatile and unsuitable market situations. The

profit before exceptional items for A.G. Barr Plc has stood remarkably at £42.4m reflecting

an increase of 2.7% from the figures reported in the previous year (Agbarr.Co.Uk, 2018).

A.G. Barr Plc has experienced better business performance than the Funkin cocktail. The

A.G. Barr Plc operating margin prior to exceptional items stood 16.3% in 2016 which

positively rose to 16.8% during 2017 (Schaltegger & Burritt, 2017). The free cash flow for

A.G. Barr Plc stood £28.3 million during 2016 while in2017 it increased to £43.2 million.

Taking into the consideration the financial performance reported by A.G. Barr Plc the

gross margin for the company was 46.8% in 2016 which marginally increased to 46.9% in

2017. The A.G. Barr Plc profit before tax and exceptional items were £41.3 in 2016 and

increased to £43.1 million in 2017 reflecting a rise of 4.4% from the previous year figures

(Warren & Jones, 2018). A.G. Barr Plc has put behind the challenges related to supply chain

and challenges of system application that helped in serving out the constrained during 2016

(Agbarr.Co.Uk, 2018). In spite of the fall in the reported revenue by 0.6% the underlying

income of business grew by 1.5% resulting a rise in revenue of 1.5% inspired by innovation

across IRN BRU and Rubicon brands.

Financial strength and weakness:

Taking account of the A.G. Barr Plc financial strength and weakness, the same is

based on the diverse and differentiated business portfolio (Macve, 2015). Taking into the

account the strength of A.G. Barr Plc the organization not only places emphasis on the

production but have placed their emphasis on the segment of cocktail mixer which has

increased and strengthen the portfolio under the unquiet and leading market brand in the

growing market of soft drink industry.

Financial performance:

Over the last twelve months A.G. Barr Plc has made considerable amount of progress

with strong financial earnings in spite of the volatile and unsuitable market situations. The

profit before exceptional items for A.G. Barr Plc has stood remarkably at £42.4m reflecting

an increase of 2.7% from the figures reported in the previous year (Agbarr.Co.Uk, 2018).

A.G. Barr Plc has experienced better business performance than the Funkin cocktail. The

A.G. Barr Plc operating margin prior to exceptional items stood 16.3% in 2016 which

positively rose to 16.8% during 2017 (Schaltegger & Burritt, 2017). The free cash flow for

A.G. Barr Plc stood £28.3 million during 2016 while in2017 it increased to £43.2 million.

Taking into the consideration the financial performance reported by A.G. Barr Plc the

gross margin for the company was 46.8% in 2016 which marginally increased to 46.9% in

2017. The A.G. Barr Plc profit before tax and exceptional items were £41.3 in 2016 and

increased to £43.1 million in 2017 reflecting a rise of 4.4% from the previous year figures

(Warren & Jones, 2018). A.G. Barr Plc has put behind the challenges related to supply chain

and challenges of system application that helped in serving out the constrained during 2016

(Agbarr.Co.Uk, 2018). In spite of the fall in the reported revenue by 0.6% the underlying

income of business grew by 1.5% resulting a rise in revenue of 1.5% inspired by innovation

across IRN BRU and Rubicon brands.

Financial strength and weakness:

Taking account of the A.G. Barr Plc financial strength and weakness, the same is

based on the diverse and differentiated business portfolio (Macve, 2015). Taking into the

account the strength of A.G. Barr Plc the organization not only places emphasis on the

production but have placed their emphasis on the segment of cocktail mixer which has

increased and strengthen the portfolio under the unquiet and leading market brand in the

growing market of soft drink industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCE

One more business strength for A.G. Barr Plc is the robust balance sheet and cash

derived by the firm (Agbarr.Co.Uk, 2018). This has resulted the board to undertake the

decision of returning the £30 million to its shareholders with the help of share repurchase

programme. Additionally, A.G. Barr Plc has dedicated set of people which have immensely

contributed to the success of the business.

The increasing growth reported by A.G. Barr Plc in the net asset have led the balance

sheet of the firm to significantly gain strength (Trotman et al., 2015). The strong balance

sheet has empowered the business to gain access of the cost effective and flexible facilities of

debt to make sure that the A.G. Barr Plc possess the agility of benefiting from the

opportunities that is recognized.

A.G. Barr Plc has strong structure of risk management of assessing the risk. The

framework of risk management lay down the systematic approach of managing the risk

(Waegenaere et al., 2015). A.G. Barr Plc strength is bestowed in the re-evaluation of risk by

modifying the range of brands of offered. A.G. Barr Plc offers its consumers with the range

of products from numerous brands across wide variety of business channels and customers.

There are certain weakness and failure recognized in the financial year. A.G. Barr Plc

faces the weakness in maintaining appropriate customer relationships. As a result of this,

A.G. Barr Plc may face the problem of reduced customer base which may create an adverse

impact on the sales with fall in operating profit as well (Carlon et al., 2015). Furthermore,

another weakness that is identified for A.G. Barr Plc is the failure in protecting the

intellectual property rights of the company. The failure of maintaining in appropriate

customer relation and intellectual property rights may result in loss of brand worth.

Evidences from the analysis represents that the company reported a current ratio of

2.70 in 2016 which subsequently declined to 2.36. Furthermore the debt to equity ratio of

One more business strength for A.G. Barr Plc is the robust balance sheet and cash

derived by the firm (Agbarr.Co.Uk, 2018). This has resulted the board to undertake the

decision of returning the £30 million to its shareholders with the help of share repurchase

programme. Additionally, A.G. Barr Plc has dedicated set of people which have immensely

contributed to the success of the business.

The increasing growth reported by A.G. Barr Plc in the net asset have led the balance

sheet of the firm to significantly gain strength (Trotman et al., 2015). The strong balance

sheet has empowered the business to gain access of the cost effective and flexible facilities of

debt to make sure that the A.G. Barr Plc possess the agility of benefiting from the

opportunities that is recognized.

A.G. Barr Plc has strong structure of risk management of assessing the risk. The

framework of risk management lay down the systematic approach of managing the risk

(Waegenaere et al., 2015). A.G. Barr Plc strength is bestowed in the re-evaluation of risk by

modifying the range of brands of offered. A.G. Barr Plc offers its consumers with the range

of products from numerous brands across wide variety of business channels and customers.

There are certain weakness and failure recognized in the financial year. A.G. Barr Plc

faces the weakness in maintaining appropriate customer relationships. As a result of this,

A.G. Barr Plc may face the problem of reduced customer base which may create an adverse

impact on the sales with fall in operating profit as well (Carlon et al., 2015). Furthermore,

another weakness that is identified for A.G. Barr Plc is the failure in protecting the

intellectual property rights of the company. The failure of maintaining in appropriate

customer relation and intellectual property rights may result in loss of brand worth.

Evidences from the analysis represents that the company reported a current ratio of

2.70 in 2016 which subsequently declined to 2.36. Furthermore the debt to equity ratio of

8CORPORATE FINANCE

A.G. Barr Plc has stood 1.35 during 2016 which relatively increased to 1.56 during the year

2017 (Kahng, 2016). The situation defines that A.G. Barr Plc took higher debt and this may

potentially lead to rise in the operational risk of A.G. Barr Plc.

Efficiency Market Hypothesis:

Stock Market Pricing Efficiency in A.G. Barr Plc Share Price:

The efficient market hypothesis is viewed as the investment theory which states that it

is not probable to beat down the market since the stock market efficiency reflects the price of

share to incorporate and reflect the essential information. It is noticed that the recent

application of sugar tax in UK is regarded as the semi-strong information (Damodaran,

2016). Stocks are traded constantly at the fair value on stock exchange which is not possible

for the investors either purchase the undervalued stocks or sell the stocks at higher price. The

government measure of announcing the sugar tax can be considered as the semi-strong

measure since the information derived to forecast the performance of stock might be

highlighted in the stock price.

The information concerning the higher tax on sugar might enable the organizations to

quicken the long awaited sugar soft drink programme. Therefore, this would result the firm in

capitalizing on the price trends of the securities trending in the market. The main reason for

the variation in the share price of A.G. Barr Plc is arrival of new information. As a result of

this, the present prices of shares offers all the required information from the outside sources

and subsequently there are hardly any reason to believe that the share price are very high or

very low (Ang, 2018). Concerning the A.G. Barr Plc, the new information relating to sugar

tax can be viewed as the prevalence of efficient market for the investors to gain profit from

the new information.

A.G. Barr Plc has stood 1.35 during 2016 which relatively increased to 1.56 during the year

2017 (Kahng, 2016). The situation defines that A.G. Barr Plc took higher debt and this may

potentially lead to rise in the operational risk of A.G. Barr Plc.

Efficiency Market Hypothesis:

Stock Market Pricing Efficiency in A.G. Barr Plc Share Price:

The efficient market hypothesis is viewed as the investment theory which states that it

is not probable to beat down the market since the stock market efficiency reflects the price of

share to incorporate and reflect the essential information. It is noticed that the recent

application of sugar tax in UK is regarded as the semi-strong information (Damodaran,

2016). Stocks are traded constantly at the fair value on stock exchange which is not possible

for the investors either purchase the undervalued stocks or sell the stocks at higher price. The

government measure of announcing the sugar tax can be considered as the semi-strong

measure since the information derived to forecast the performance of stock might be

highlighted in the stock price.

The information concerning the higher tax on sugar might enable the organizations to

quicken the long awaited sugar soft drink programme. Therefore, this would result the firm in

capitalizing on the price trends of the securities trending in the market. The main reason for

the variation in the share price of A.G. Barr Plc is arrival of new information. As a result of

this, the present prices of shares offers all the required information from the outside sources

and subsequently there are hardly any reason to believe that the share price are very high or

very low (Ang, 2018). Concerning the A.G. Barr Plc, the new information relating to sugar

tax can be viewed as the prevalence of efficient market for the investors to gain profit from

the new information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE FINANCE

Semi strong market form of market efficiency:

Under the efficient market hypothesis semi strong form of efficiency means that all the

necessary public information has been taken account in determining the current share price.

Therefore, neither the technical nor the fundamental analysis can be implemented to obtain

higher gains (Fracassi, 2016). Under the semi-strong forms of market efficiency information

provided is based on the public available benefits which the investors are looking to earn

from the abnormal returns on investment.

As evident in the circumstances of of A.G.Barr Plc the government action of applying

sugar tax suggest that the information relates to the assistance of the investors to derive

abnormal return on investment (Ehrhardt & Brigham, 2016). The information that is derived

for A.G.Barr Plc is considered in stock price and resulting in semi-strong classification of

stock price as the information that is obtained is through the outside sources. Therefore, the

investors that are looking for abnormal return on their investment can derive benefit from the

stock of of A.G.Barr Plc.

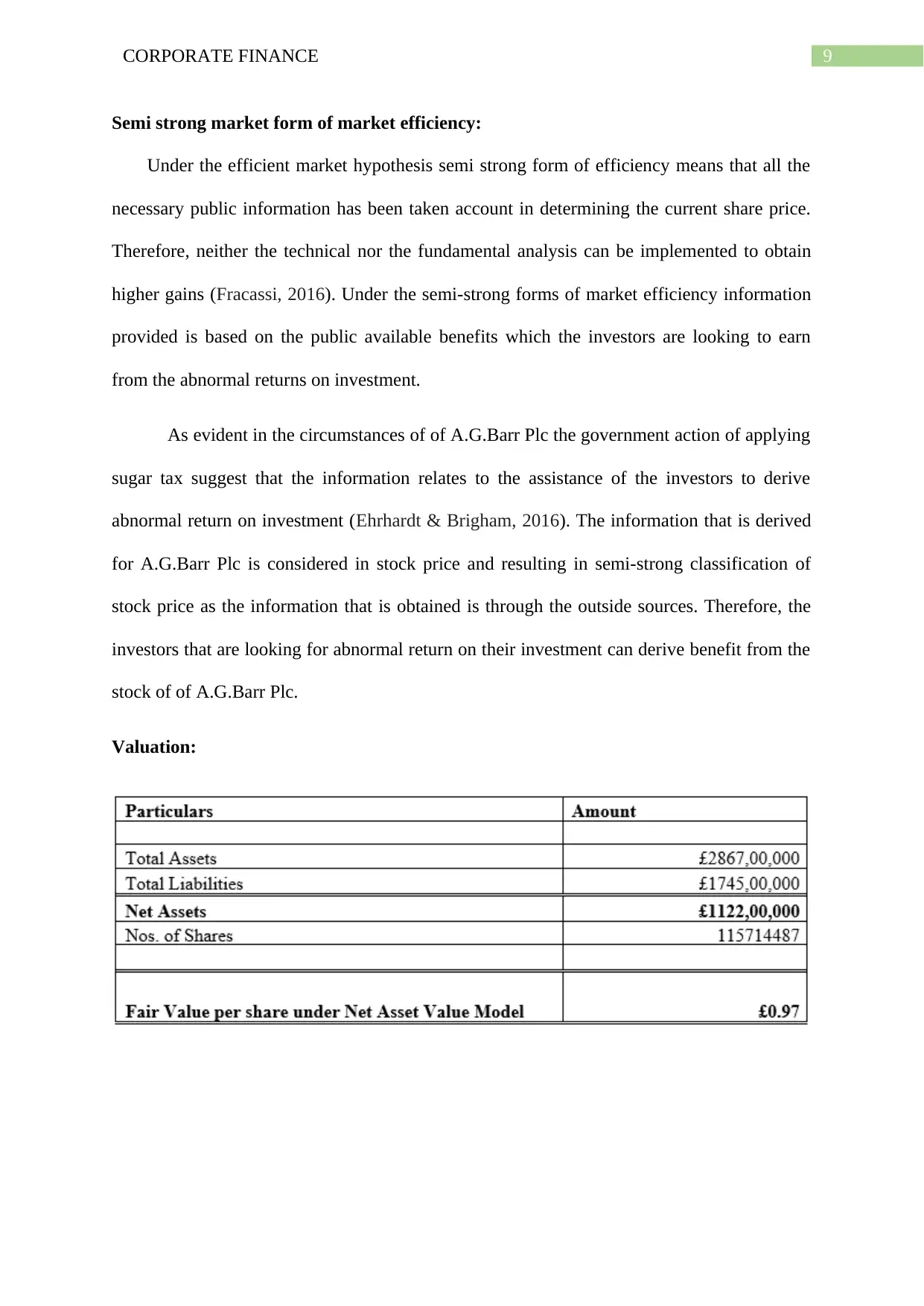

Valuation:

Semi strong market form of market efficiency:

Under the efficient market hypothesis semi strong form of efficiency means that all the

necessary public information has been taken account in determining the current share price.

Therefore, neither the technical nor the fundamental analysis can be implemented to obtain

higher gains (Fracassi, 2016). Under the semi-strong forms of market efficiency information

provided is based on the public available benefits which the investors are looking to earn

from the abnormal returns on investment.

As evident in the circumstances of of A.G.Barr Plc the government action of applying

sugar tax suggest that the information relates to the assistance of the investors to derive

abnormal return on investment (Ehrhardt & Brigham, 2016). The information that is derived

for A.G.Barr Plc is considered in stock price and resulting in semi-strong classification of

stock price as the information that is obtained is through the outside sources. Therefore, the

investors that are looking for abnormal return on their investment can derive benefit from the

stock of of A.G.Barr Plc.

Valuation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE FINANCE

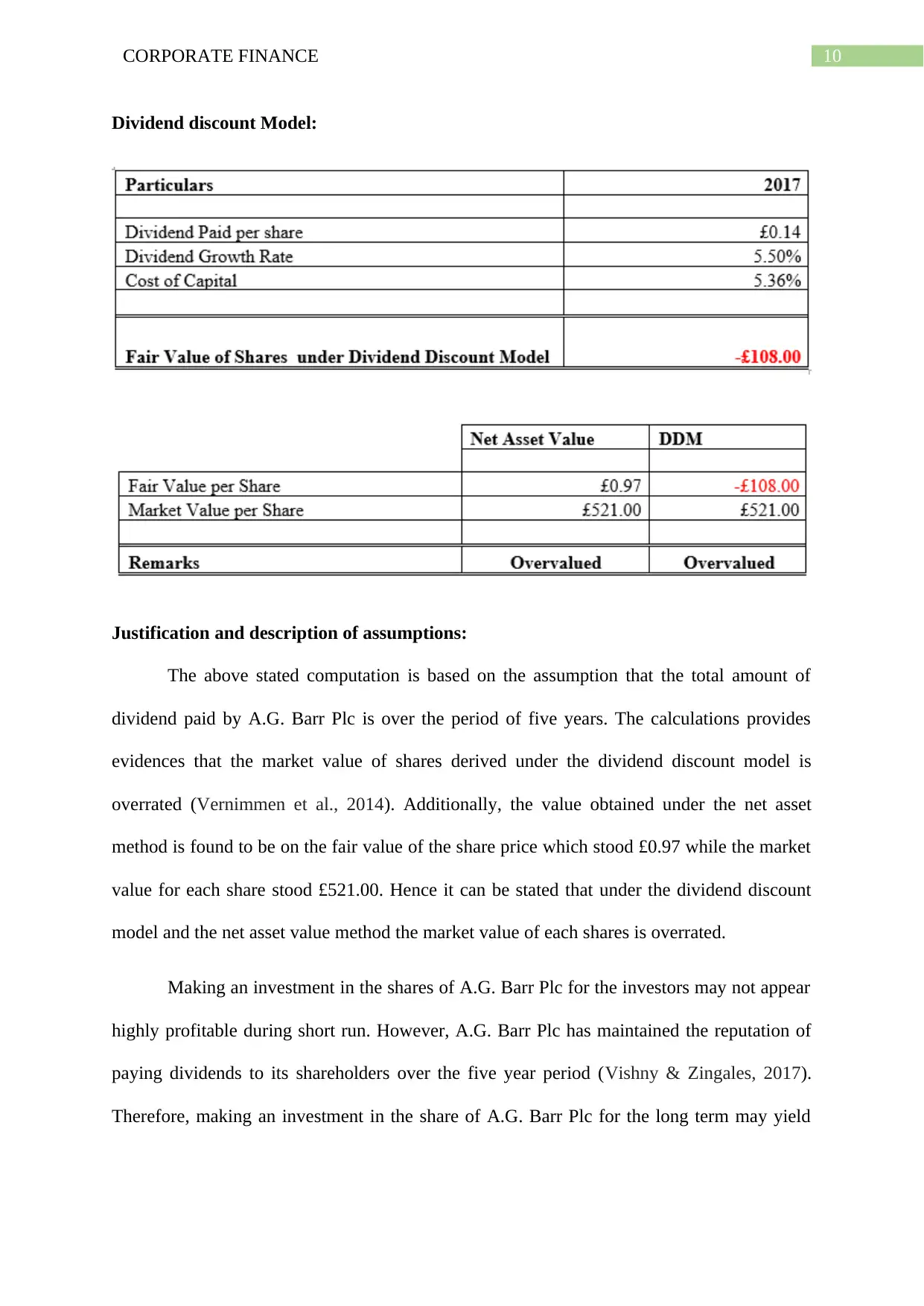

Dividend discount Model:

Justification and description of assumptions:

The above stated computation is based on the assumption that the total amount of

dividend paid by A.G. Barr Plc is over the period of five years. The calculations provides

evidences that the market value of shares derived under the dividend discount model is

overrated (Vernimmen et al., 2014). Additionally, the value obtained under the net asset

method is found to be on the fair value of the share price which stood £0.97 while the market

value for each share stood £521.00. Hence it can be stated that under the dividend discount

model and the net asset value method the market value of each shares is overrated.

Making an investment in the shares of A.G. Barr Plc for the investors may not appear

highly profitable during short run. However, A.G. Barr Plc has maintained the reputation of

paying dividends to its shareholders over the five year period (Vishny & Zingales, 2017).

Therefore, making an investment in the share of A.G. Barr Plc for the long term may yield

Dividend discount Model:

Justification and description of assumptions:

The above stated computation is based on the assumption that the total amount of

dividend paid by A.G. Barr Plc is over the period of five years. The calculations provides

evidences that the market value of shares derived under the dividend discount model is

overrated (Vernimmen et al., 2014). Additionally, the value obtained under the net asset

method is found to be on the fair value of the share price which stood £0.97 while the market

value for each share stood £521.00. Hence it can be stated that under the dividend discount

model and the net asset value method the market value of each shares is overrated.

Making an investment in the shares of A.G. Barr Plc for the investors may not appear

highly profitable during short run. However, A.G. Barr Plc has maintained the reputation of

paying dividends to its shareholders over the five year period (Vishny & Zingales, 2017).

Therefore, making an investment in the share of A.G. Barr Plc for the long term may yield

11CORPORATE FINANCE

sufficient amount of benefit for the shareholders under food and beverage industry while

other market players have paid higher dividends to its shareholders.

Usefulness and limitations of valuation methods:

Valuation of stock under the dividend discount model is viewed as the useful method

based on the notion that stock of the organization holds the worth in respect to all the sum

value of future dividend payments (Titman et al., 2017). To determine the intrinsic value of

stock the dividend discount model is regarded useful since it excludes the present value

conditions. The model is helpful in determining the current value of shares and future

dividend payments.

The net asset value method on the other hand is regarded as the useful tool of business

valuation that places emphasis on the organization net asset or the fair market value of the

total assets following the subtraction of total liabilities (Gitman et al., 2015). The net asset

method is best suited in determining the financial picture of the organization from the

information presented in the balance sheet.

Taking account of the limitation of dividend discount model, the model fails to

account the non-dividend factors namely the brand loyalty and the proportion of the

intangible assets. Since these components increases the value of the organization (Barberis et

al., 2015). Additionally, the model is based on the assumption that rate of growth is constant

and stable. These assumptions hardly exists in the modern world.

The net asset value simultaneously is regarded as the difficult method of determining

the value of intangible assets particularly the property rights (Lazzati & Menichini, 2015).

Additionally, the statement of financial position may prematurely value the assets because of

the existence of depreciation.

sufficient amount of benefit for the shareholders under food and beverage industry while

other market players have paid higher dividends to its shareholders.

Usefulness and limitations of valuation methods:

Valuation of stock under the dividend discount model is viewed as the useful method

based on the notion that stock of the organization holds the worth in respect to all the sum

value of future dividend payments (Titman et al., 2017). To determine the intrinsic value of

stock the dividend discount model is regarded useful since it excludes the present value

conditions. The model is helpful in determining the current value of shares and future

dividend payments.

The net asset value method on the other hand is regarded as the useful tool of business

valuation that places emphasis on the organization net asset or the fair market value of the

total assets following the subtraction of total liabilities (Gitman et al., 2015). The net asset

method is best suited in determining the financial picture of the organization from the

information presented in the balance sheet.

Taking account of the limitation of dividend discount model, the model fails to

account the non-dividend factors namely the brand loyalty and the proportion of the

intangible assets. Since these components increases the value of the organization (Barberis et

al., 2015). Additionally, the model is based on the assumption that rate of growth is constant

and stable. These assumptions hardly exists in the modern world.

The net asset value simultaneously is regarded as the difficult method of determining

the value of intangible assets particularly the property rights (Lazzati & Menichini, 2015).

Additionally, the statement of financial position may prematurely value the assets because of

the existence of depreciation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.