ACC200: Investigating Costing Methods for Sewing Easy Ltd, 2018

VerifiedAdded on 2023/06/12

|7

|928

|459

Report

AI Summary

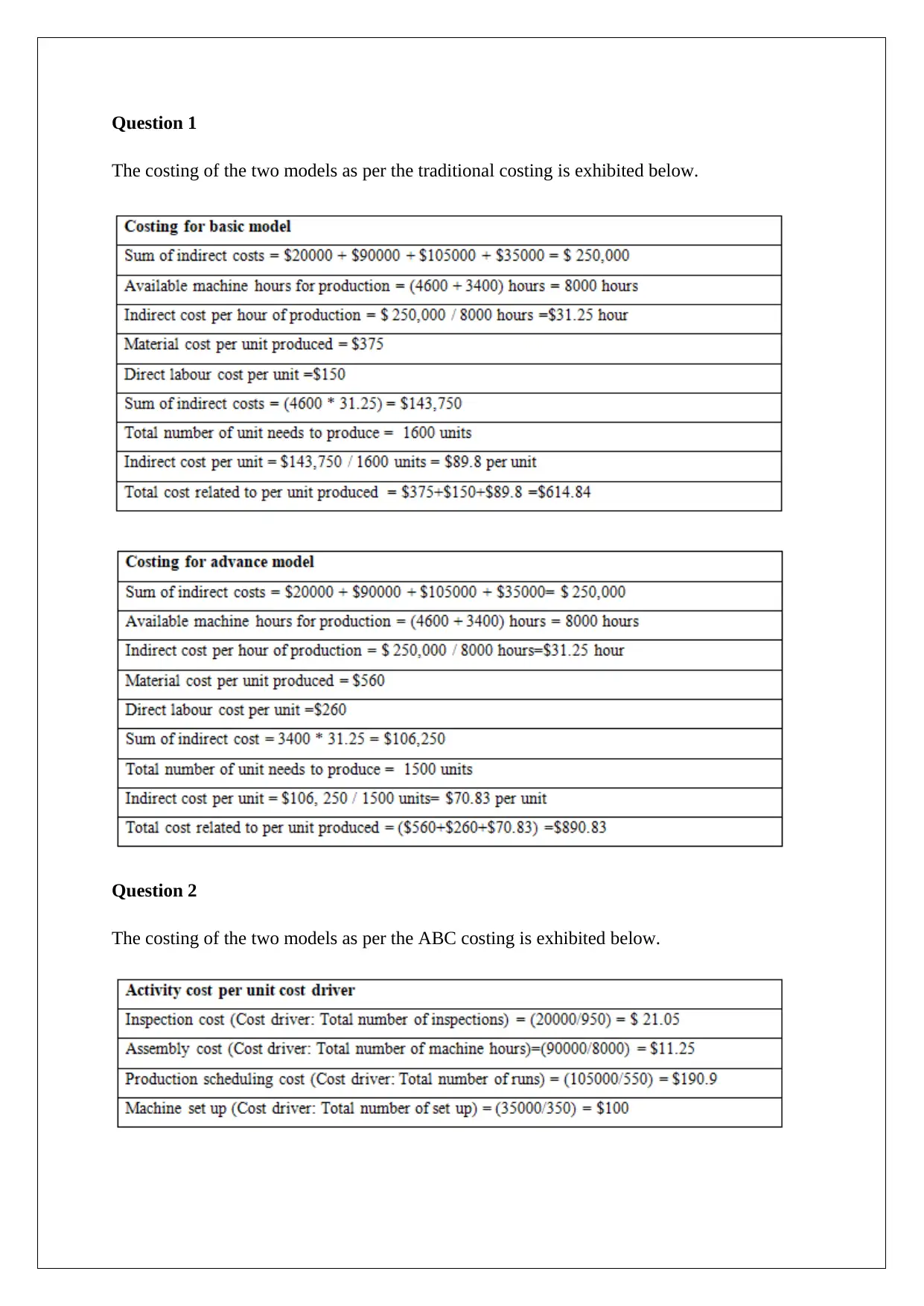

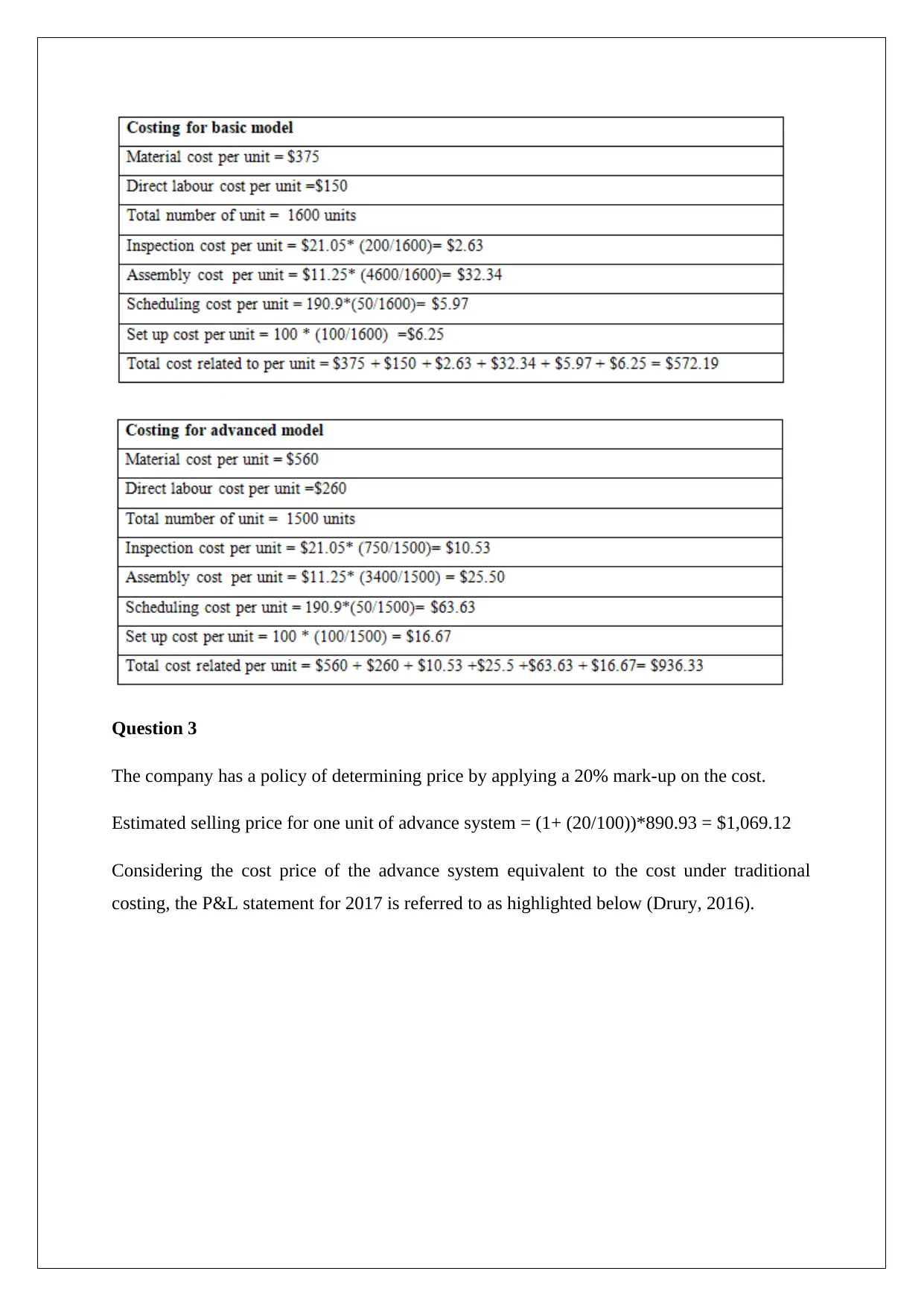

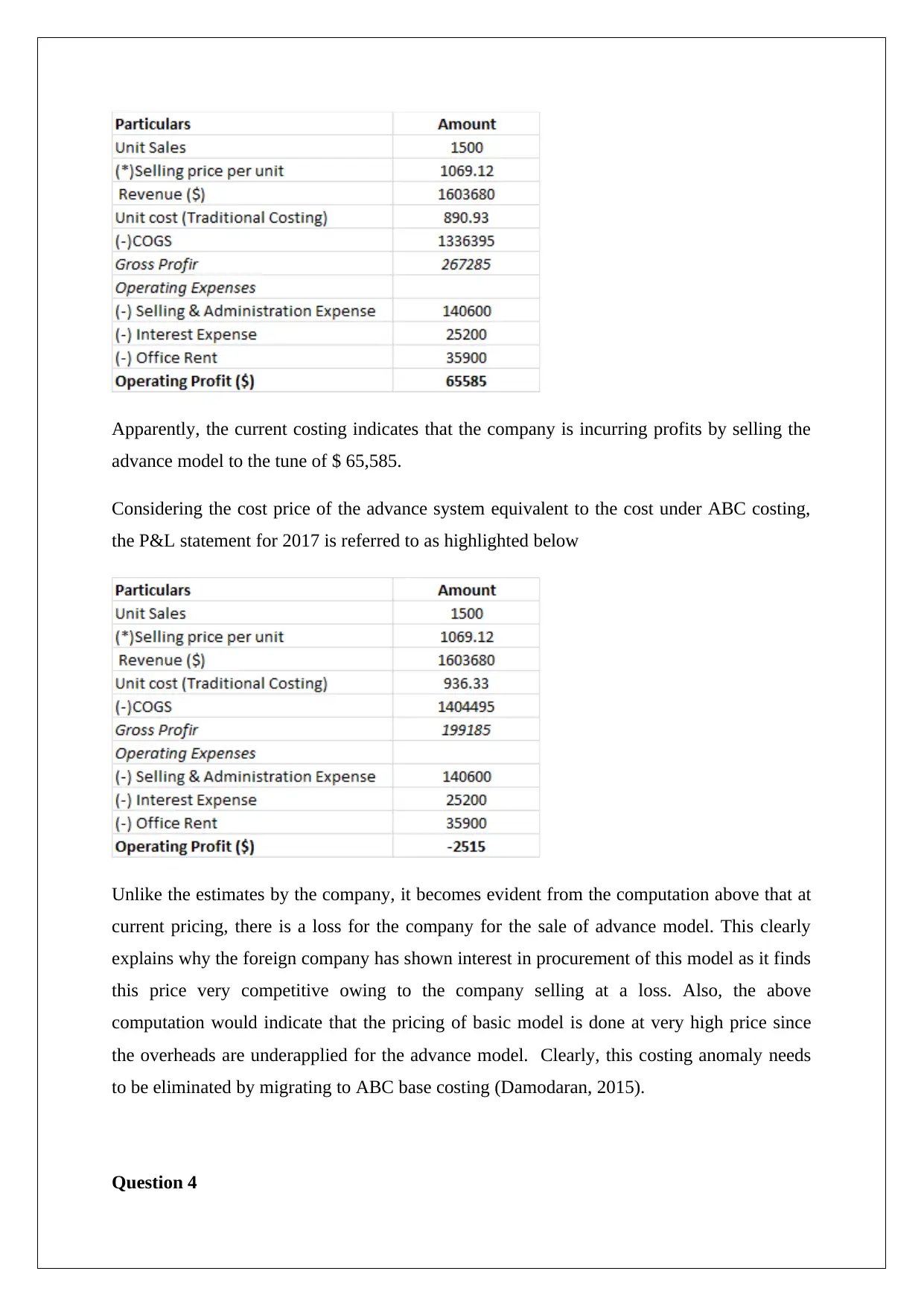

This report analyzes the costing methods employed by Sewing Easy Ltd, focusing on traditional costing versus activity-based costing (ABC) for their basic and advanced sewing machine models. The assignment examines why an overseas buyer is exclusively interested in the advanced model, highlighting potential issues with the company's current traditional costing system. It explores the discrepancies between actual and applied overheads, suggesting a shift towards ABC costing for more accurate cost allocation and pricing strategies. The report also discusses the benefits and challenges of implementing ABC costing, emphasizing its potential to improve management decision-making related to production, outsourcing, and special orders. The analysis reveals that the advanced model may be sold at a loss under the traditional costing method, explaining the buyer's interest and indicating a need for pricing adjustments based on a more accurate costing system.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.