ACC200 - Evaluating Costing Methods for Fantori Ltd Sewing Machines

VerifiedAdded on 2023/04/21

|12

|2572

|72

Report

AI Summary

This report analyzes Fantori Ltd's current traditional costing method and compares it with activity-based costing (ABC) to understand why a foreign buyer is only interested in the advanced sewing machine model. The analysis includes detailed computations of unit costs for both basic and advanced models under both costing methods. The report also constructs income statements under each costing approach to highlight the impact on profitability. It discusses the importance of accurate product pricing, the reasons for under-application or over-application of overheads, and provides recommendations for managing these issues. The report concludes that the traditional costing method under-prices the advanced model and over-prices the basic model, leading to skewed sales patterns and profit loss. Switching to ABC is recommended for better decision-making and profitability.

MANAGEMENT ACCOUNTING

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................2

Analysis......................................................................................................................................2

Traditional Costing.................................................................................................................2

Activity Based Costing...........................................................................................................4

Income Statement.......................................................................................................................6

Under-application and over-application of overheads...............................................................8

Under-applied/Over-applied Overhead......................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

1

Introduction................................................................................................................................2

Analysis......................................................................................................................................2

Traditional Costing.................................................................................................................2

Activity Based Costing...........................................................................................................4

Income Statement.......................................................................................................................6

Under-application and over-application of overheads...............................................................8

Under-applied/Over-applied Overhead......................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

1

Introduction

Fantori Ltd is a company that manufactures sewing machine in two models namely the basic

model and advanced model. The traditional costing method is used by the company for

product costing where the overhead cost is allocated between the two models on the basis of a

direct cost. The company is about to enter into a new phase as a foreign buyer has shown

interest. However, this buyer has shown interest only in the advanced model and not in the

basic model which is rather surprising. Tony Mans suspects that the primary reason for the

strange pattern of interest by the foreign buyer may be linked to the use of traditional costing

system which might be providing inaccurate cost estimate thus making the prices of the

model skewed. In this background, the objective is to report is to carry out the costing of the

two models of sewing machine using both traditional and Activity Based costing (ABC) so as

to advice if there has been an under-application or over-application of overhead to the two

models. Also, the importance of accurate product costing and pricing would also be dealt by

the given report.

Analysis

This section presents the analysis of the data provided in the context of the problem at hand

and the objective at hand.

Traditional Costing

The various details pertaining to the costing of the two models has been offered and using the

same the unit price of each model would be determined as per the traditional costing. A key

feature of the traditional costing method is that the indirect cost allocation is linked to one of

the direct costs (Damodaran, 2015). As per the company practice, machine hour is used as the

measure to drive the indirect cost allocation between the two models.

Step 1: Computation of direct costs per unit

Model 1: Basic Model

Unit material cost = $ 350

Unit direct labour cost = $ 175

Total direct cost per unit = 350 +175 = $ 525

Model 2: Advance Model

2

Fantori Ltd is a company that manufactures sewing machine in two models namely the basic

model and advanced model. The traditional costing method is used by the company for

product costing where the overhead cost is allocated between the two models on the basis of a

direct cost. The company is about to enter into a new phase as a foreign buyer has shown

interest. However, this buyer has shown interest only in the advanced model and not in the

basic model which is rather surprising. Tony Mans suspects that the primary reason for the

strange pattern of interest by the foreign buyer may be linked to the use of traditional costing

system which might be providing inaccurate cost estimate thus making the prices of the

model skewed. In this background, the objective is to report is to carry out the costing of the

two models of sewing machine using both traditional and Activity Based costing (ABC) so as

to advice if there has been an under-application or over-application of overhead to the two

models. Also, the importance of accurate product costing and pricing would also be dealt by

the given report.

Analysis

This section presents the analysis of the data provided in the context of the problem at hand

and the objective at hand.

Traditional Costing

The various details pertaining to the costing of the two models has been offered and using the

same the unit price of each model would be determined as per the traditional costing. A key

feature of the traditional costing method is that the indirect cost allocation is linked to one of

the direct costs (Damodaran, 2015). As per the company practice, machine hour is used as the

measure to drive the indirect cost allocation between the two models.

Step 1: Computation of direct costs per unit

Model 1: Basic Model

Unit material cost = $ 350

Unit direct labour cost = $ 175

Total direct cost per unit = 350 +175 = $ 525

Model 2: Advance Model

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unit material cost = $ 580

Unit direct labour cost = $ 280

Total direct cost per unit = 580 +280 = $ 860

Step 2: Allocation of indirect costs per unit

The basis of allocation of indirect costs would be on the basis of the total machine used for

the production of two models.

Total indirect cost = Inspection ($30,000) + Assembly ($ 100,000) + Production Scheduling

($110,000) + Machine Set up ($40,000) = $ 280,000

Total machine hours used for the production of the two products = 4700 + 3500 = 8,200

hours

Indirect cost per unit machine hour = (280000/8200) = $ 34.146

Indirect cost allocated to the production of the basic model = 4700*34.146 = $ 160.488

Indirect cost allocated to the production of the advance model = 3500*34.146 = $ 119.512

Based on the given information, units of production of basic model = 1700

Unit indirect cost allocated to basic model = (160488/1700) = $ 94.40

Based on the given information, units of production of advance model = 1600

Unit indirect cost allocated to advance model = (119512/1600) = $ 74.70

Step 3: Unit cost as per traditional costing

Unit cost of a model = Unit direct cost + Unit indirect cost

Unit cost of basic model = 525 + 94.40 = $619.40

Unit cost of advance model = 860 + 74.70 = $934.70

3

Unit direct labour cost = $ 280

Total direct cost per unit = 580 +280 = $ 860

Step 2: Allocation of indirect costs per unit

The basis of allocation of indirect costs would be on the basis of the total machine used for

the production of two models.

Total indirect cost = Inspection ($30,000) + Assembly ($ 100,000) + Production Scheduling

($110,000) + Machine Set up ($40,000) = $ 280,000

Total machine hours used for the production of the two products = 4700 + 3500 = 8,200

hours

Indirect cost per unit machine hour = (280000/8200) = $ 34.146

Indirect cost allocated to the production of the basic model = 4700*34.146 = $ 160.488

Indirect cost allocated to the production of the advance model = 3500*34.146 = $ 119.512

Based on the given information, units of production of basic model = 1700

Unit indirect cost allocated to basic model = (160488/1700) = $ 94.40

Based on the given information, units of production of advance model = 1600

Unit indirect cost allocated to advance model = (119512/1600) = $ 74.70

Step 3: Unit cost as per traditional costing

Unit cost of a model = Unit direct cost + Unit indirect cost

Unit cost of basic model = 525 + 94.40 = $619.40

Unit cost of advance model = 860 + 74.70 = $934.70

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above computations, it can be inferred that unit cost for basic model and advance

model as per traditional costing is $ 619.40 and $ 934.70 respectively.

Activity Based Costing

Unlike traditional costing, the indirect cost allocation is not based on any direct cost driver

but is based on the respective cost drivers of the various activities involved in the overhead

costs. As a result, it is expected to be a more accurate method for estimation of the costs

especially when the underlying firm produces more than one variant of a particular product

(Brealey, Myers and Allen, 2014).

Step 1: Computation of direct costs per unit

For the Basic Model, unit direct cost is $ 525 as has been shown in the traditional costing. For

the Advance Model, unit direct cost is $ 860 as has been shown in the traditional costing.

Step 2: Allocation of indirect costs per unit

The computation of the indirect costs can be carried on as shown below.

1) Indirect Cost – Inspection Cost

Cost driver – Number of Inspections

Total inspection cost = $30,000

Total number of inspections = 210+760 = 970

Inspection cost per inspection = (30000/970) = $ 30.93

2) Indirect Cost – Assembly Cost

Cost driver – Number of machine hours

Total assembly cost = $ 100,000

Total number of machine hours = 4700 + 3500 = 8,200 hours

Assembly cost per machine hour = 100000/8200 = $ 12.20

3) Indirect Cost – Production Scheduling

Cost driver – Number of production runs

4

model as per traditional costing is $ 619.40 and $ 934.70 respectively.

Activity Based Costing

Unlike traditional costing, the indirect cost allocation is not based on any direct cost driver

but is based on the respective cost drivers of the various activities involved in the overhead

costs. As a result, it is expected to be a more accurate method for estimation of the costs

especially when the underlying firm produces more than one variant of a particular product

(Brealey, Myers and Allen, 2014).

Step 1: Computation of direct costs per unit

For the Basic Model, unit direct cost is $ 525 as has been shown in the traditional costing. For

the Advance Model, unit direct cost is $ 860 as has been shown in the traditional costing.

Step 2: Allocation of indirect costs per unit

The computation of the indirect costs can be carried on as shown below.

1) Indirect Cost – Inspection Cost

Cost driver – Number of Inspections

Total inspection cost = $30,000

Total number of inspections = 210+760 = 970

Inspection cost per inspection = (30000/970) = $ 30.93

2) Indirect Cost – Assembly Cost

Cost driver – Number of machine hours

Total assembly cost = $ 100,000

Total number of machine hours = 4700 + 3500 = 8,200 hours

Assembly cost per machine hour = 100000/8200 = $ 12.20

3) Indirect Cost – Production Scheduling

Cost driver – Number of production runs

4

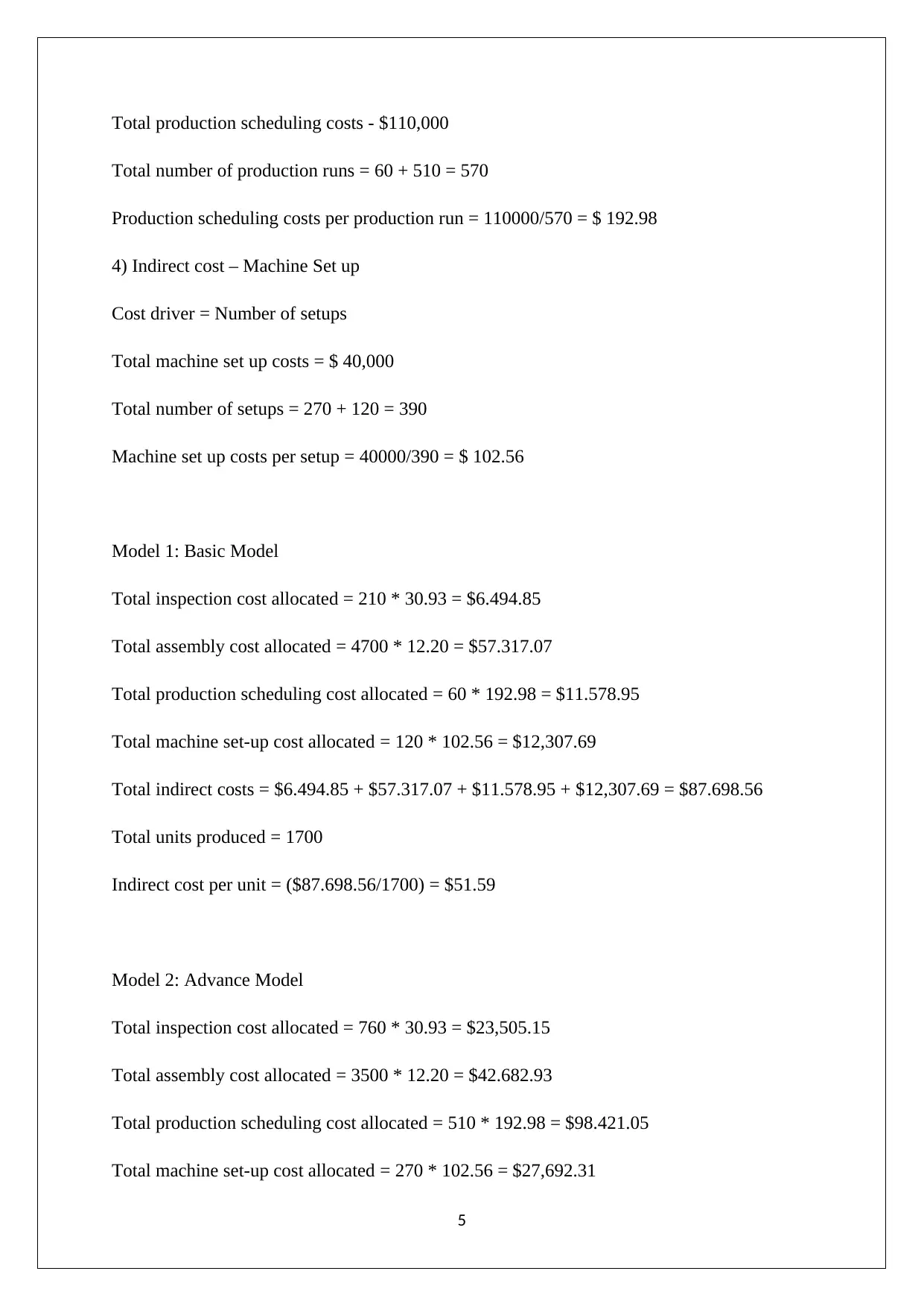

Total production scheduling costs - $110,000

Total number of production runs = 60 + 510 = 570

Production scheduling costs per production run = 110000/570 = $ 192.98

4) Indirect cost – Machine Set up

Cost driver = Number of setups

Total machine set up costs = $ 40,000

Total number of setups = 270 + 120 = 390

Machine set up costs per setup = 40000/390 = $ 102.56

Model 1: Basic Model

Total inspection cost allocated = 210 * 30.93 = $6.494.85

Total assembly cost allocated = 4700 * 12.20 = $57.317.07

Total production scheduling cost allocated = 60 * 192.98 = $11.578.95

Total machine set-up cost allocated = 120 * 102.56 = $12,307.69

Total indirect costs = $6.494.85 + $57.317.07 + $11.578.95 + $12,307.69 = $87.698.56

Total units produced = 1700

Indirect cost per unit = ($87.698.56/1700) = $51.59

Model 2: Advance Model

Total inspection cost allocated = 760 * 30.93 = $23,505.15

Total assembly cost allocated = 3500 * 12.20 = $42.682.93

Total production scheduling cost allocated = 510 * 192.98 = $98.421.05

Total machine set-up cost allocated = 270 * 102.56 = $27,692.31

5

Total number of production runs = 60 + 510 = 570

Production scheduling costs per production run = 110000/570 = $ 192.98

4) Indirect cost – Machine Set up

Cost driver = Number of setups

Total machine set up costs = $ 40,000

Total number of setups = 270 + 120 = 390

Machine set up costs per setup = 40000/390 = $ 102.56

Model 1: Basic Model

Total inspection cost allocated = 210 * 30.93 = $6.494.85

Total assembly cost allocated = 4700 * 12.20 = $57.317.07

Total production scheduling cost allocated = 60 * 192.98 = $11.578.95

Total machine set-up cost allocated = 120 * 102.56 = $12,307.69

Total indirect costs = $6.494.85 + $57.317.07 + $11.578.95 + $12,307.69 = $87.698.56

Total units produced = 1700

Indirect cost per unit = ($87.698.56/1700) = $51.59

Model 2: Advance Model

Total inspection cost allocated = 760 * 30.93 = $23,505.15

Total assembly cost allocated = 3500 * 12.20 = $42.682.93

Total production scheduling cost allocated = 510 * 192.98 = $98.421.05

Total machine set-up cost allocated = 270 * 102.56 = $27,692.31

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

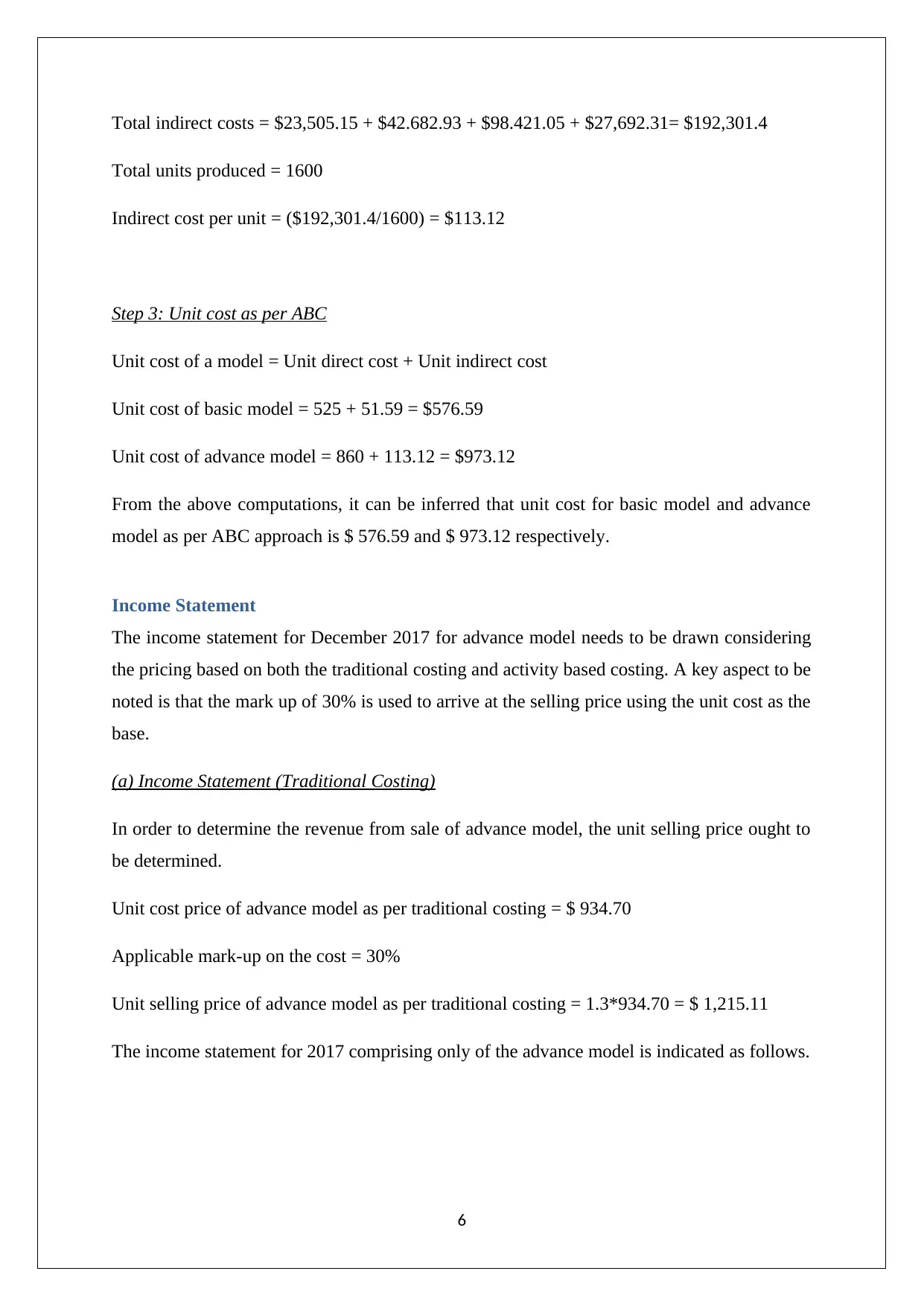

Total indirect costs = $23,505.15 + $42.682.93 + $98.421.05 + $27,692.31= $192,301.4

Total units produced = 1600

Indirect cost per unit = ($192,301.4/1600) = $113.12

Step 3: Unit cost as per ABC

Unit cost of a model = Unit direct cost + Unit indirect cost

Unit cost of basic model = 525 + 51.59 = $576.59

Unit cost of advance model = 860 + 113.12 = $973.12

From the above computations, it can be inferred that unit cost for basic model and advance

model as per ABC approach is $ 576.59 and $ 973.12 respectively.

Income Statement

The income statement for December 2017 for advance model needs to be drawn considering

the pricing based on both the traditional costing and activity based costing. A key aspect to be

noted is that the mark up of 30% is used to arrive at the selling price using the unit cost as the

base.

(a) Income Statement (Traditional Costing)

In order to determine the revenue from sale of advance model, the unit selling price ought to

be determined.

Unit cost price of advance model as per traditional costing = $ 934.70

Applicable mark-up on the cost = 30%

Unit selling price of advance model as per traditional costing = 1.3*934.70 = $ 1,215.11

The income statement for 2017 comprising only of the advance model is indicated as follows.

6

Total units produced = 1600

Indirect cost per unit = ($192,301.4/1600) = $113.12

Step 3: Unit cost as per ABC

Unit cost of a model = Unit direct cost + Unit indirect cost

Unit cost of basic model = 525 + 51.59 = $576.59

Unit cost of advance model = 860 + 113.12 = $973.12

From the above computations, it can be inferred that unit cost for basic model and advance

model as per ABC approach is $ 576.59 and $ 973.12 respectively.

Income Statement

The income statement for December 2017 for advance model needs to be drawn considering

the pricing based on both the traditional costing and activity based costing. A key aspect to be

noted is that the mark up of 30% is used to arrive at the selling price using the unit cost as the

base.

(a) Income Statement (Traditional Costing)

In order to determine the revenue from sale of advance model, the unit selling price ought to

be determined.

Unit cost price of advance model as per traditional costing = $ 934.70

Applicable mark-up on the cost = 30%

Unit selling price of advance model as per traditional costing = 1.3*934.70 = $ 1,215.11

The income statement for 2017 comprising only of the advance model is indicated as follows.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

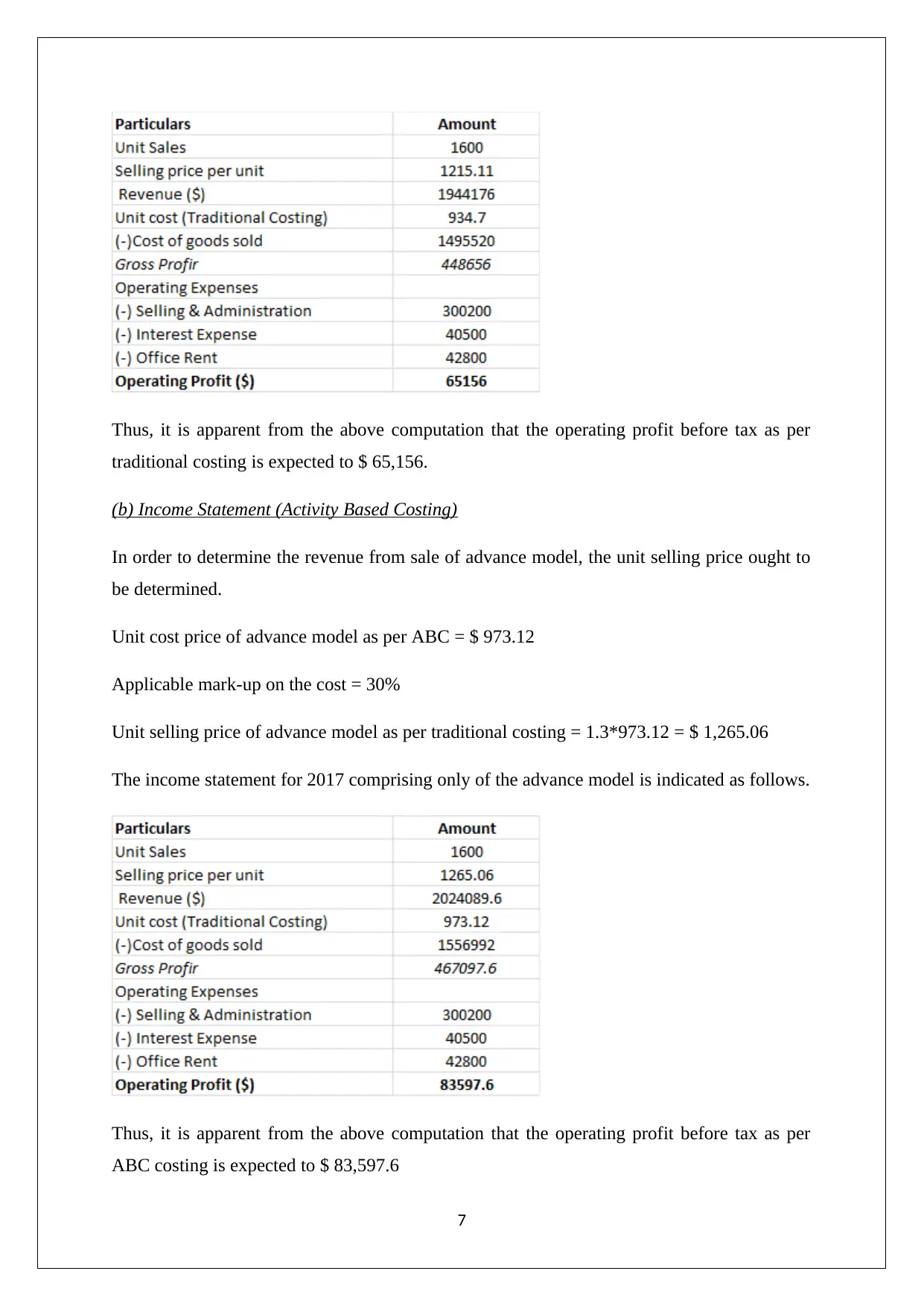

Thus, it is apparent from the above computation that the operating profit before tax as per

traditional costing is expected to $ 65,156.

(b) Income Statement (Activity Based Costing)

In order to determine the revenue from sale of advance model, the unit selling price ought to

be determined.

Unit cost price of advance model as per ABC = $ 973.12

Applicable mark-up on the cost = 30%

Unit selling price of advance model as per traditional costing = 1.3*973.12 = $ 1,265.06

The income statement for 2017 comprising only of the advance model is indicated as follows.

Thus, it is apparent from the above computation that the operating profit before tax as per

ABC costing is expected to $ 83,597.6

7

traditional costing is expected to $ 65,156.

(b) Income Statement (Activity Based Costing)

In order to determine the revenue from sale of advance model, the unit selling price ought to

be determined.

Unit cost price of advance model as per ABC = $ 973.12

Applicable mark-up on the cost = 30%

Unit selling price of advance model as per traditional costing = 1.3*973.12 = $ 1,265.06

The income statement for 2017 comprising only of the advance model is indicated as follows.

Thus, it is apparent from the above computation that the operating profit before tax as per

ABC costing is expected to $ 83,597.6

7

Importance of Product Pricing

From the above computation, it becomes evident that the advance model is priced cheaper

under the traditional costing when compared to ABC approach. This is because the overhead

cost is under-applied to advance model while over-applied to basic model under traditional

costing. As a result, the foreign buyer finds the advance model comparatively cheaper from

other competitors and hence interested in purchasing for the same. The basic model pricing

by the company would be on the higher end owing to which the foreign buyer would procure

the same from competitors at lower cost (Drury, 2016).

The importance of product pricing becomes evident from the comparison of the two income

statements whereby the company is currently losing on profits from the advance model as the

actual margin is lesser than 30%. On the other hand, it is also losing sales on the basic model

as it is priced higher which would render it less competitive against comparable products.

Migrating the activity based costing would ensure that the company is able to derive a higher

profits from the sale of advance model. Also, the sales of the basic model would be higher

owing to the price being more competitive. The accurate product costing also is helpful in

making various decisions such as make or outsource, providing quote for special orders and

hence it makes sense for the company to shift to activity based costing from traditional

costing (Petty et. al., 2015).

Under-application and over-application of overheads

It is very uncommon to find matching applied overhead and actual overhead. A critical

reason for this is that there are some businesses which have not migrated to activity based

costing owing to which there is inaccuracy in overhead costs allocation leading to problem of

overhead being over-applied or under-applied. Yet another reason for the mismatch is that

even when activity based costing is applied, the sub-division of activities into smaller

activities does not continue indefinitely but only to the extent when the errors are not

material. As a result, there is likely to be some mismatch between actual overhead incurred

and overhead applied (Parrino and Kidwell, 2014).

The issue of overhead being over-applied or under-applied can be managed through the

measures underlined below (Petty et.al, 2015).

8

From the above computation, it becomes evident that the advance model is priced cheaper

under the traditional costing when compared to ABC approach. This is because the overhead

cost is under-applied to advance model while over-applied to basic model under traditional

costing. As a result, the foreign buyer finds the advance model comparatively cheaper from

other competitors and hence interested in purchasing for the same. The basic model pricing

by the company would be on the higher end owing to which the foreign buyer would procure

the same from competitors at lower cost (Drury, 2016).

The importance of product pricing becomes evident from the comparison of the two income

statements whereby the company is currently losing on profits from the advance model as the

actual margin is lesser than 30%. On the other hand, it is also losing sales on the basic model

as it is priced higher which would render it less competitive against comparable products.

Migrating the activity based costing would ensure that the company is able to derive a higher

profits from the sale of advance model. Also, the sales of the basic model would be higher

owing to the price being more competitive. The accurate product costing also is helpful in

making various decisions such as make or outsource, providing quote for special orders and

hence it makes sense for the company to shift to activity based costing from traditional

costing (Petty et. al., 2015).

Under-application and over-application of overheads

It is very uncommon to find matching applied overhead and actual overhead. A critical

reason for this is that there are some businesses which have not migrated to activity based

costing owing to which there is inaccuracy in overhead costs allocation leading to problem of

overhead being over-applied or under-applied. Yet another reason for the mismatch is that

even when activity based costing is applied, the sub-division of activities into smaller

activities does not continue indefinitely but only to the extent when the errors are not

material. As a result, there is likely to be some mismatch between actual overhead incurred

and overhead applied (Parrino and Kidwell, 2014).

The issue of overhead being over-applied or under-applied can be managed through the

measures underlined below (Petty et.al, 2015).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is imperative that allocation of overheads in case of multiple products or multiple

variant of a single product must be carried out through ABC approach and not

traditional costing which is inaccurate.

There must be linking of the product price to the cost incurred (ABC based) and

additionally, the selling price ought to be compared with the prevalent market price to

determine the variations and if these have valid reasons or not.

In products with multiple variants, a particular variant may be having unexpectedly

high sales while other variant may be reporting poor sales. In such instances, it makes

sense to ensure that application of overheads to highlight the underlying cost of the

two variants is correct or not.

Under-applied/Over-applied Overhead

Actual overhead = $ 300,000

Applied overhead = $ 210,000

It is apparent that the applied overhead is lower than the actual overhead incurred and hence

it would to correct to conclude that there has been an under application of overhead in the

given scenario.

Under applied overhead = 300,000-210,000 = $ 90,000

This $ 90,000 would be written off in the three accounts namely work in process, finished

goods and cost of goods sold based on their ending balances.

Overhead written back to work in process = (60500/(60500+90000+1850000))*90000 =

$2,721.82

Overhead written back to inventory= (90000/(60500+90000+1850000))*90000 = $4,049

Overhead written back to cost of goods sold = (1850000/(60500+90000+1850000))*90000 =

$83,229.18

Thus, based on the above computation, the revised closing balances for the three accounts are

highlighted as follows.

Work in process = 60,500 + 2,721.82 = $ 63,221

Inventory = 90,000 + 4049 = $ 94,049

9

variant of a single product must be carried out through ABC approach and not

traditional costing which is inaccurate.

There must be linking of the product price to the cost incurred (ABC based) and

additionally, the selling price ought to be compared with the prevalent market price to

determine the variations and if these have valid reasons or not.

In products with multiple variants, a particular variant may be having unexpectedly

high sales while other variant may be reporting poor sales. In such instances, it makes

sense to ensure that application of overheads to highlight the underlying cost of the

two variants is correct or not.

Under-applied/Over-applied Overhead

Actual overhead = $ 300,000

Applied overhead = $ 210,000

It is apparent that the applied overhead is lower than the actual overhead incurred and hence

it would to correct to conclude that there has been an under application of overhead in the

given scenario.

Under applied overhead = 300,000-210,000 = $ 90,000

This $ 90,000 would be written off in the three accounts namely work in process, finished

goods and cost of goods sold based on their ending balances.

Overhead written back to work in process = (60500/(60500+90000+1850000))*90000 =

$2,721.82

Overhead written back to inventory= (90000/(60500+90000+1850000))*90000 = $4,049

Overhead written back to cost of goods sold = (1850000/(60500+90000+1850000))*90000 =

$83,229.18

Thus, based on the above computation, the revised closing balances for the three accounts are

highlighted as follows.

Work in process = 60,500 + 2,721.82 = $ 63,221

Inventory = 90,000 + 4049 = $ 94,049

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of goods sold = 1,850,000 + 83,229 = $1,933, 229

Conclusion

Based on the above discussion, it is apparent that the activity based costing model is more

accurate with regards to allocation to overheads between the basic and advanced model of

sewing machine. Under the current traditional costing method, there is under-application of

overheads to the advance model and over-application of overheads to the basic model. As a

result, the foreign buyer is interested in advance model which is cheaper but not interested in

the basic model which is expensive. Further, there is realistic chance of mismatch between

actual overhead and applied overhead. As a result, it makes sense that prudent measures

ought to be taken to avoid the same.

10

Conclusion

Based on the above discussion, it is apparent that the activity based costing model is more

accurate with regards to allocation to overheads between the basic and advanced model of

sewing machine. Under the current traditional costing method, there is under-application of

overheads to the advance model and over-application of overheads to the basic model. As a

result, the foreign buyer is interested in advance model which is cheaper but not interested in

the basic model which is expensive. Further, there is realistic chance of mismatch between

actual overhead and applied overhead. As a result, it makes sense that prudent measures

ought to be taken to avoid the same.

10

References

Brealey, R. A., Myers, S. C., & Allen, F. (2014) Principles of corporate finance, 2nd ed. New

York: McGraw-Hill Inc, pp. 78-79

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons, pp. 130-131

Drury, C. (2016) Cost and Management Accounting: An Introduction. 6th ed. New York:

Cengage Learning, pp.67

Parrino, R. and Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publication, pp. 78-79

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education, French

Forest Australia, pp. 79-80, 118-119

11

Brealey, R. A., Myers, S. C., & Allen, F. (2014) Principles of corporate finance, 2nd ed. New

York: McGraw-Hill Inc, pp. 78-79

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons, pp. 130-131

Drury, C. (2016) Cost and Management Accounting: An Introduction. 6th ed. New York:

Cengage Learning, pp.67

Parrino, R. and Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publication, pp. 78-79

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education, French

Forest Australia, pp. 79-80, 118-119

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.