ACC200 - Costing Analysis: Traditional and ABC Costing Methods

VerifiedAdded on 2023/04/23

|13

|2617

|112

Report

AI Summary

This report provides a detailed costing analysis for Fantori Ltd, comparing traditional costing methods with activity-based costing (ABC) to understand why an overseas buyer is only interested in the advanced sewing machine model. The analysis includes calculations of cost per unit under both costing methods, income statements, and a discussion on the importance of accurate product costing. The report also covers the differences between actual and applied overhead, along with proration techniques for overhead costs, offering a comprehensive overview of costing strategies and their implications for business decisions. Desklib provides access to this report and other study resources for students.

Running Head: COSTING ANALYSIS

0

Costing Analysis

Traditional and ABC Costing

0

Costing Analysis

Traditional and ABC Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

1

Table of Contents

Answer to Question-1................................................................................................................2

Answer to Question-2................................................................................................................4

Answer to Question-3................................................................................................................7

Analysis................................................................................................................................10

Importance of accurate product costing...............................................................................10

Answer to Question 4...............................................................................................................11

Answer to Question 5...............................................................................................................12

Bibliography.............................................................................................................................14

1

Table of Contents

Answer to Question-1................................................................................................................2

Answer to Question-2................................................................................................................4

Answer to Question-3................................................................................................................7

Analysis................................................................................................................................10

Importance of accurate product costing...............................................................................10

Answer to Question 4...............................................................................................................11

Answer to Question 5...............................................................................................................12

Bibliography.............................................................................................................................14

COSTING ANALYSIS

2

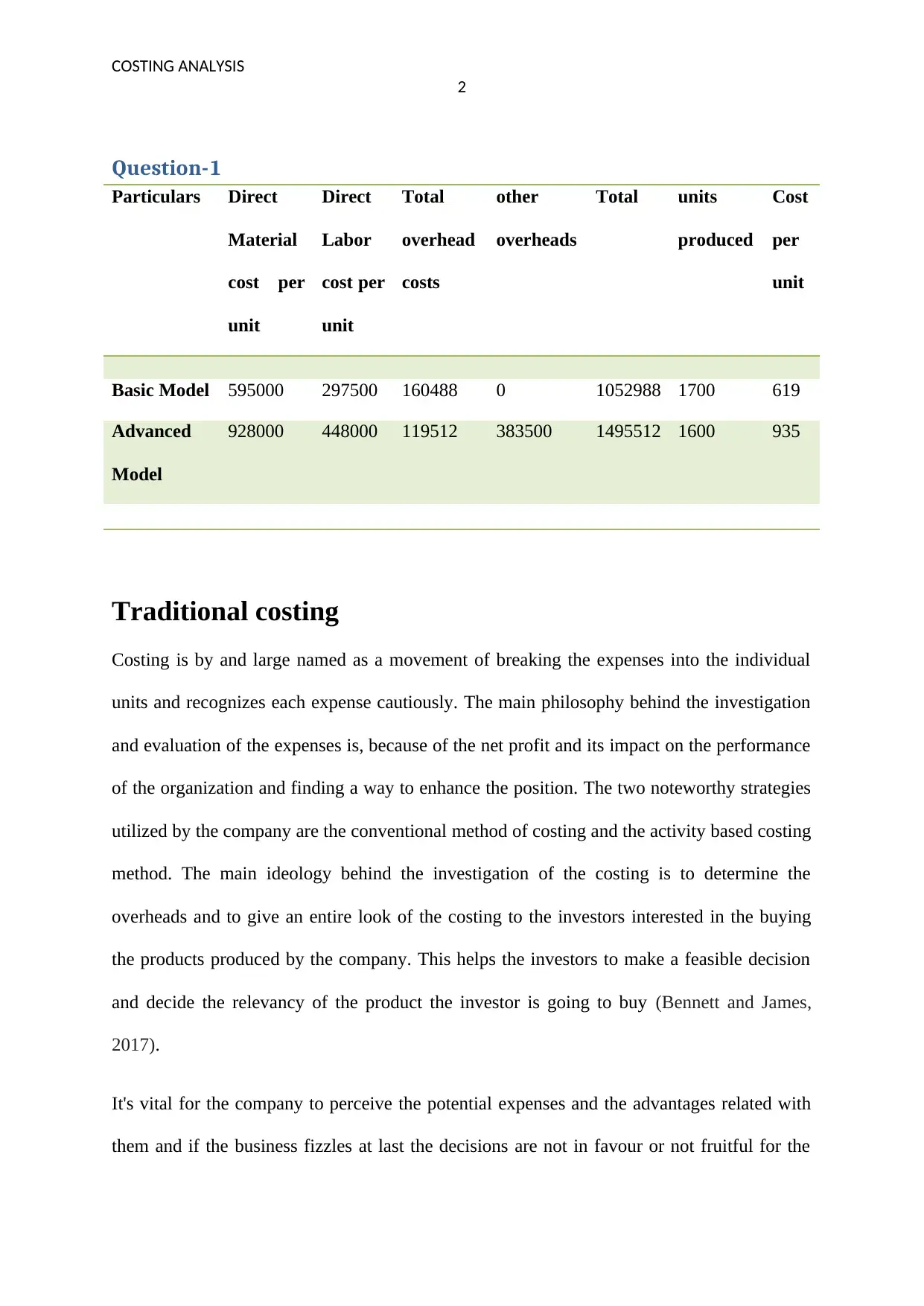

Question-1

Particulars Direct

Material

cost per

unit

Direct

Labor

cost per

unit

Total

overhead

costs

other

overheads

Total units

produced

Cost

per

unit

Basic Model 595000 297500 160488 0 1052988 1700 619

Advanced

Model

928000 448000 119512 383500 1495512 1600 935

Traditional costing

Costing is by and large named as a movement of breaking the expenses into the individual

units and recognizes each expense cautiously. The main philosophy behind the investigation

and evaluation of the expenses is, because of the net profit and its impact on the performance

of the organization and finding a way to enhance the position. The two noteworthy strategies

utilized by the company are the conventional method of costing and the activity based costing

method. The main ideology behind the investigation of the costing is to determine the

overheads and to give an entire look of the costing to the investors interested in the buying

the products produced by the company. This helps the investors to make a feasible decision

and decide the relevancy of the product the investor is going to buy (Bennett and James,

2017).

It's vital for the company to perceive the potential expenses and the advantages related with

them and if the business fizzles at last the decisions are not in favour or not fruitful for the

2

Question-1

Particulars Direct

Material

cost per

unit

Direct

Labor

cost per

unit

Total

overhead

costs

other

overheads

Total units

produced

Cost

per

unit

Basic Model 595000 297500 160488 0 1052988 1700 619

Advanced

Model

928000 448000 119512 383500 1495512 1600 935

Traditional costing

Costing is by and large named as a movement of breaking the expenses into the individual

units and recognizes each expense cautiously. The main philosophy behind the investigation

and evaluation of the expenses is, because of the net profit and its impact on the performance

of the organization and finding a way to enhance the position. The two noteworthy strategies

utilized by the company are the conventional method of costing and the activity based costing

method. The main ideology behind the investigation of the costing is to determine the

overheads and to give an entire look of the costing to the investors interested in the buying

the products produced by the company. This helps the investors to make a feasible decision

and decide the relevancy of the product the investor is going to buy (Bennett and James,

2017).

It's vital for the company to perceive the potential expenses and the advantages related with

them and if the business fizzles at last the decisions are not in favour or not fruitful for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

3

future health of the company. Additionally the cost examination assists in allowing a chance

to administer and get into the deep analysis of the funds and their spending.

Traditional costing also known as the conventional costing is the method of calculating the

costs to be allocated to the product. There are different techniques that are under process

required by the management and the accountants to make a legitimate administration of the

money related matters of the business. One such strategy is known as the traditional costing

framework. It is a strategy or technique under which the benefits are anticipated by deeply

analysing the profits incurred by the business and also after considering the circumstances

relevant to the indirect costs (Cooper, 2017).

Under the Conventional costing the allocation of the overhead is done by loading the

percentage of the overall overheads on the particular item or segment. The rate so calculated

is commonly the rate derived from the machine hours in comparison to the general rates and

the machine hours are treated as the baseline to calculate the overall factory overheads.

From the above table it can be stated that the cost per unit of the Sewing easy’s product that

is the basic model and the advanced model is $619 and $935. This can be seen in the first

table of the report and the same shall be considered under the traditional costing system

which the company is currently applying.

Question-2

Calculation of cost per unit under activity based costing method

Particulars Basic Model Advanced

Model

Direct Material cost per unit 350 580

Direct Labor cost per unit 175 280

3

future health of the company. Additionally the cost examination assists in allowing a chance

to administer and get into the deep analysis of the funds and their spending.

Traditional costing also known as the conventional costing is the method of calculating the

costs to be allocated to the product. There are different techniques that are under process

required by the management and the accountants to make a legitimate administration of the

money related matters of the business. One such strategy is known as the traditional costing

framework. It is a strategy or technique under which the benefits are anticipated by deeply

analysing the profits incurred by the business and also after considering the circumstances

relevant to the indirect costs (Cooper, 2017).

Under the Conventional costing the allocation of the overhead is done by loading the

percentage of the overall overheads on the particular item or segment. The rate so calculated

is commonly the rate derived from the machine hours in comparison to the general rates and

the machine hours are treated as the baseline to calculate the overall factory overheads.

From the above table it can be stated that the cost per unit of the Sewing easy’s product that

is the basic model and the advanced model is $619 and $935. This can be seen in the first

table of the report and the same shall be considered under the traditional costing system

which the company is currently applying.

Question-2

Calculation of cost per unit under activity based costing method

Particulars Basic Model Advanced

Model

Direct Material cost per unit 350 580

Direct Labor cost per unit 175 280

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

4

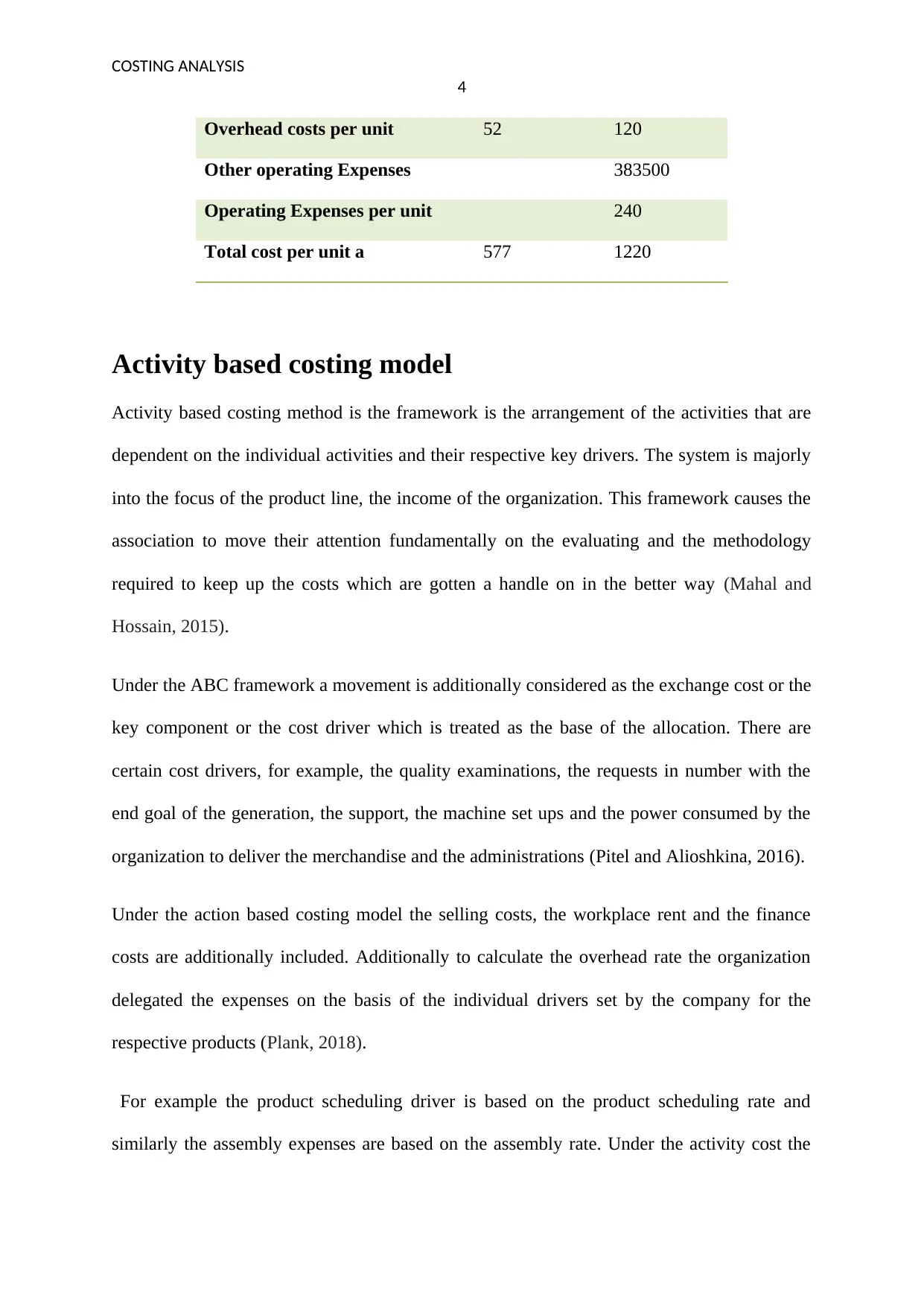

Overhead costs per unit 52 120

Other operating Expenses 383500

Operating Expenses per unit 240

Total cost per unit a 577 1220

Activity based costing model

Activity based costing method is the framework is the arrangement of the activities that are

dependent on the individual activities and their respective key drivers. The system is majorly

into the focus of the product line, the income of the organization. This framework causes the

association to move their attention fundamentally on the evaluating and the methodology

required to keep up the costs which are gotten a handle on in the better way (Mahal and

Hossain, 2015).

Under the ABC framework a movement is additionally considered as the exchange cost or the

key component or the cost driver which is treated as the base of the allocation. There are

certain cost drivers, for example, the quality examinations, the requests in number with the

end goal of the generation, the support, the machine set ups and the power consumed by the

organization to deliver the merchandise and the administrations (Pitel and Alioshkina, 2016).

Under the action based costing model the selling costs, the workplace rent and the finance

costs are additionally included. Additionally to calculate the overhead rate the organization

delegated the expenses on the basis of the individual drivers set by the company for the

respective products (Plank, 2018).

For example the product scheduling driver is based on the product scheduling rate and

similarly the assembly expenses are based on the assembly rate. Under the activity cost the

4

Overhead costs per unit 52 120

Other operating Expenses 383500

Operating Expenses per unit 240

Total cost per unit a 577 1220

Activity based costing model

Activity based costing method is the framework is the arrangement of the activities that are

dependent on the individual activities and their respective key drivers. The system is majorly

into the focus of the product line, the income of the organization. This framework causes the

association to move their attention fundamentally on the evaluating and the methodology

required to keep up the costs which are gotten a handle on in the better way (Mahal and

Hossain, 2015).

Under the ABC framework a movement is additionally considered as the exchange cost or the

key component or the cost driver which is treated as the base of the allocation. There are

certain cost drivers, for example, the quality examinations, the requests in number with the

end goal of the generation, the support, the machine set ups and the power consumed by the

organization to deliver the merchandise and the administrations (Pitel and Alioshkina, 2016).

Under the action based costing model the selling costs, the workplace rent and the finance

costs are additionally included. Additionally to calculate the overhead rate the organization

delegated the expenses on the basis of the individual drivers set by the company for the

respective products (Plank, 2018).

For example the product scheduling driver is based on the product scheduling rate and

similarly the assembly expenses are based on the assembly rate. Under the activity cost the

COSTING ANALYSIS

5

cost of the total overheads that are calculated are specified with the rate of the basic and the

advanced model and the rates are $52 and $120 (Popesko, Papadaki and Novák, 2015).

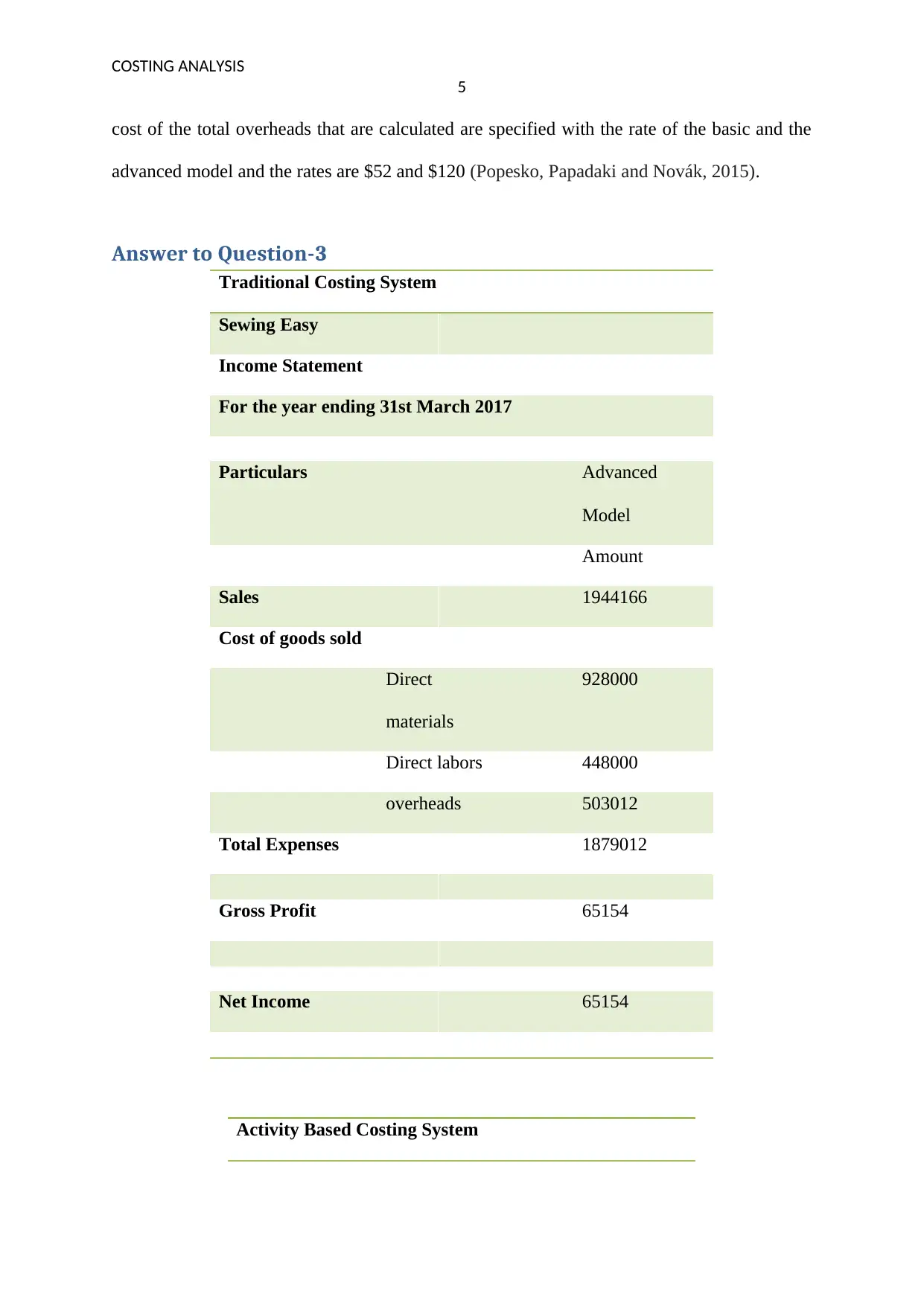

Answer to Question-3

Traditional Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials

928000

Direct labors 448000

overheads 503012

Total Expenses 1879012

Gross Profit 65154

Net Income 65154

Activity Based Costing System

5

cost of the total overheads that are calculated are specified with the rate of the basic and the

advanced model and the rates are $52 and $120 (Popesko, Papadaki and Novák, 2015).

Answer to Question-3

Traditional Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials

928000

Direct labors 448000

overheads 503012

Total Expenses 1879012

Gross Profit 65154

Net Income 65154

Activity Based Costing System

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

6

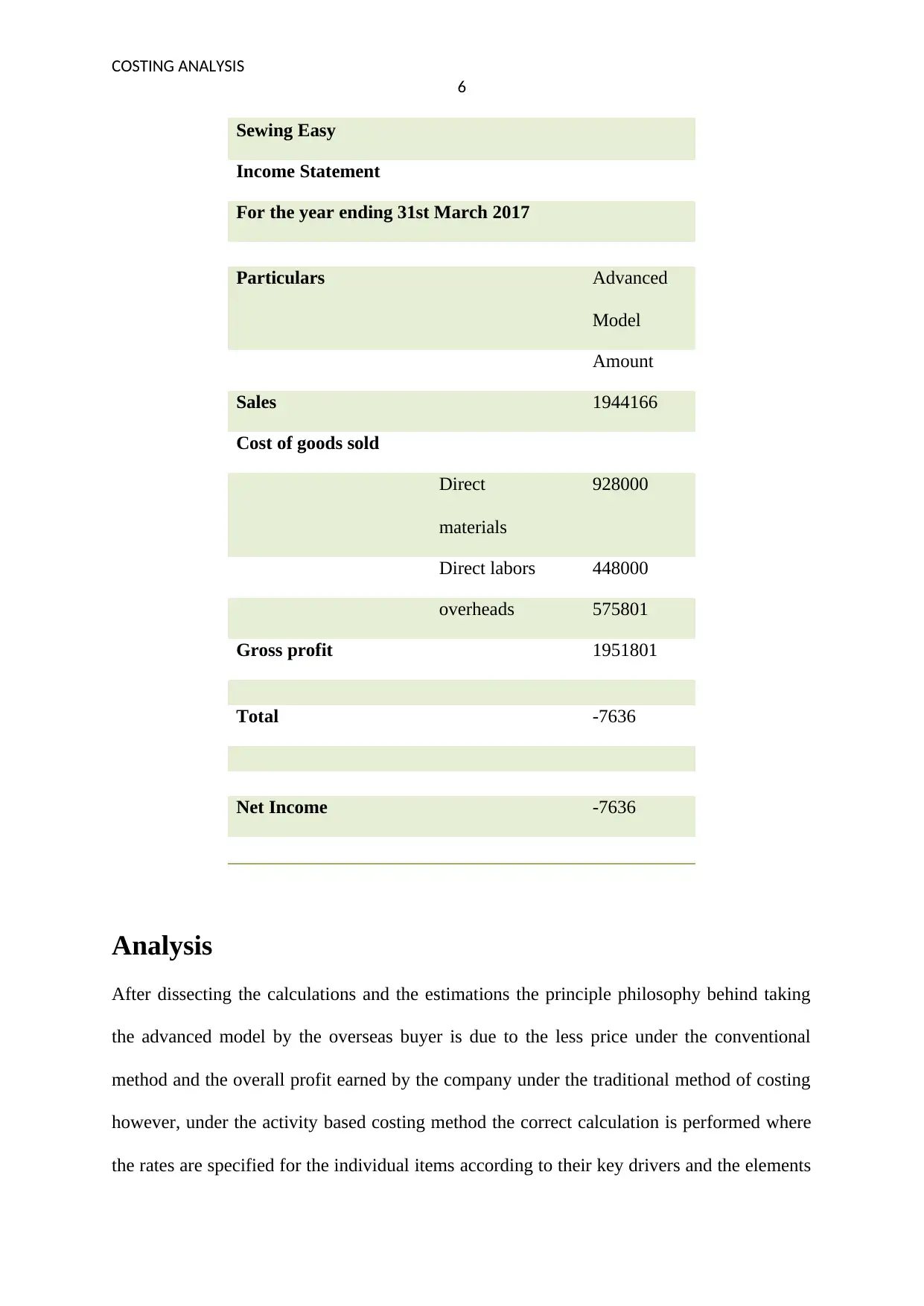

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials

928000

Direct labors 448000

overheads 575801

Gross profit 1951801

Total -7636

Net Income -7636

Analysis

After dissecting the calculations and the estimations the principle philosophy behind taking

the advanced model by the overseas buyer is due to the less price under the conventional

method and the overall profit earned by the company under the traditional method of costing

however, under the activity based costing method the correct calculation is performed where

the rates are specified for the individual items according to their key drivers and the elements

6

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials

928000

Direct labors 448000

overheads 575801

Gross profit 1951801

Total -7636

Net Income -7636

Analysis

After dissecting the calculations and the estimations the principle philosophy behind taking

the advanced model by the overseas buyer is due to the less price under the conventional

method and the overall profit earned by the company under the traditional method of costing

however, under the activity based costing method the correct calculation is performed where

the rates are specified for the individual items according to their key drivers and the elements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

7

and the same are allocated on the basis of their respective rate and hence the company is

selling the advanced model under the ABC costing method at $1225 which is higher than the

normal selling price of $1215 after the cost plus 30% under the traditional method and hence

the overseas buyer is more interested in choosing the advanced model rather than the activity

based costing model (Schram, et al 2015).

Importance of accurate product costing

For any organization the financial statements are the proof that the operations of the company

are true or false. The users of the financial statements are much in prevalence only because

these are the reports the investors can rely upon once they have decided to invest in the

products of the business. The accurate item costing causes the financial specialists to take the

essential choices in choosing whether the assets put by the speculator are right way or not.

The accurate item costing aides in deciding the effect of the spending where the expenses are

planned for the future based on the present expenses. This gives the genuine and reasonable

perspective of the expenses to find out the first position to the financial specialists putting

resources into the organization. Not only this but the asset and the inventory are also under

the impact of the accurate product costing as these two figures are the major and the critical

issues from the point of the view of the investors and the shareholders. The precise item

costing won't just help in improving the monetary position of the business yet additionally

helps in having the upper hand over the contenders (Plunkett and Dale, 2018).

Furthermore, the income statement is also dependent upon the cost of goods sold and the

selling price of the product as well. This gives the true and fair view of the costs to ascertain

the original position to the investors investing in the company. The assets and the inventory

are also affected by the implications of the accurate product costing and moreover if the

product costs are not calculated correctly the value of the inventory will be inaccurate. This

7

and the same are allocated on the basis of their respective rate and hence the company is

selling the advanced model under the ABC costing method at $1225 which is higher than the

normal selling price of $1215 after the cost plus 30% under the traditional method and hence

the overseas buyer is more interested in choosing the advanced model rather than the activity

based costing model (Schram, et al 2015).

Importance of accurate product costing

For any organization the financial statements are the proof that the operations of the company

are true or false. The users of the financial statements are much in prevalence only because

these are the reports the investors can rely upon once they have decided to invest in the

products of the business. The accurate item costing causes the financial specialists to take the

essential choices in choosing whether the assets put by the speculator are right way or not.

The accurate item costing aides in deciding the effect of the spending where the expenses are

planned for the future based on the present expenses. This gives the genuine and reasonable

perspective of the expenses to find out the first position to the financial specialists putting

resources into the organization. Not only this but the asset and the inventory are also under

the impact of the accurate product costing as these two figures are the major and the critical

issues from the point of the view of the investors and the shareholders. The precise item

costing won't just help in improving the monetary position of the business yet additionally

helps in having the upper hand over the contenders (Plunkett and Dale, 2018).

Furthermore, the income statement is also dependent upon the cost of goods sold and the

selling price of the product as well. This gives the true and fair view of the costs to ascertain

the original position to the investors investing in the company. The assets and the inventory

are also affected by the implications of the accurate product costing and moreover if the

product costs are not calculated correctly the value of the inventory will be inaccurate. This

COSTING ANALYSIS

8

will distort the calculation and the picture will not be transparent henceforth, these are the

several reasons that determine the importance of the accurate product costing (Angelopoulos

and Pollalis, 2017). The accurate product costing will not only help in enhancing the financial

position of the business but also helps in having the competitive advantage over the

competitors.

Question 4

The accounting incorporates the wide scope of the terms and two such terms are the actual

overhead and the applied overhead. The actual overhead of any organization can be termed as

the facility expenses of the circular nature that have been brought about or spent for in

actuality. This incorporates all the overhead expenses aside from the immediate material and

the expense of the work. The example so incorporated are Equipment repairs and

maintenance, manufacturing plant protection, plant utilities, creation supplies, production line

lease, industrial facility property charges. There may a slight distinction between the actual

overheads and the applied overheads which depends on the standard rate of the overhead

(Christian, 2018).

Applied overhead is the overhead under the strategy for the costing. Applied overhead can be

named as the settled charge allocated to a generation employment or division inside an

organization. Rather than the general overheads the applied overheads have the equivalent

significance. Depreciation and the insurance are the best example of the applied overheads

(Hada, Chakravarty and Mukherjee, 2014).

From the perspective of the administration the applied overheads is considered as the

standard piece of the budgetary arranging and the investigation strategy. So as to serve and

encourage the better capital planning choices the survey of the applied overheads is important

8

will distort the calculation and the picture will not be transparent henceforth, these are the

several reasons that determine the importance of the accurate product costing (Angelopoulos

and Pollalis, 2017). The accurate product costing will not only help in enhancing the financial

position of the business but also helps in having the competitive advantage over the

competitors.

Question 4

The accounting incorporates the wide scope of the terms and two such terms are the actual

overhead and the applied overhead. The actual overhead of any organization can be termed as

the facility expenses of the circular nature that have been brought about or spent for in

actuality. This incorporates all the overhead expenses aside from the immediate material and

the expense of the work. The example so incorporated are Equipment repairs and

maintenance, manufacturing plant protection, plant utilities, creation supplies, production line

lease, industrial facility property charges. There may a slight distinction between the actual

overheads and the applied overheads which depends on the standard rate of the overhead

(Christian, 2018).

Applied overhead is the overhead under the strategy for the costing. Applied overhead can be

named as the settled charge allocated to a generation employment or division inside an

organization. Rather than the general overheads the applied overheads have the equivalent

significance. Depreciation and the insurance are the best example of the applied overheads

(Hada, Chakravarty and Mukherjee, 2014).

From the perspective of the administration the applied overheads is considered as the

standard piece of the budgetary arranging and the investigation strategy. So as to serve and

encourage the better capital planning choices the survey of the applied overheads is important

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

9

and vital for the administration. Further the genuine overhead and the applied overhead is not

the same at the need of the day because the difference arises with the change in the

uniformity of the rates and the implication of the rates at the different time period. The

decisions of the business can be changed with the change in the choice of the actual or the

applied overhead (Horngren, et al 2012).

Likewise if the overheads that are relegated more than the actual sum than the overheads are

named as the applied overhead generally the case is the inversion case. As and when the

expense of cogs of the company is determined below the actual amount it is considered as the

under applied overheads (Jiménez Duarte and Afonso, 2015).

There are couple of techniques to manage the circumstances where there are under and the

over connected issues.

• The first technique enables the exchange of the sum to the following budgetary year.

• The second technique the diary section is passed and the sum is exchanged to the

benefit and misfortune account.

• A beneficial rate is considered against the standard rate.

Question 5

300000 210000

Account balance Account balance

before Proration After Proration

Work in 60500 3% 9073 6351 75924

9

and vital for the administration. Further the genuine overhead and the applied overhead is not

the same at the need of the day because the difference arises with the change in the

uniformity of the rates and the implication of the rates at the different time period. The

decisions of the business can be changed with the change in the choice of the actual or the

applied overhead (Horngren, et al 2012).

Likewise if the overheads that are relegated more than the actual sum than the overheads are

named as the applied overhead generally the case is the inversion case. As and when the

expense of cogs of the company is determined below the actual amount it is considered as the

under applied overheads (Jiménez Duarte and Afonso, 2015).

There are couple of techniques to manage the circumstances where there are under and the

over connected issues.

• The first technique enables the exchange of the sum to the following budgetary year.

• The second technique the diary section is passed and the sum is exchanged to the

benefit and misfortune account.

• A beneficial rate is considered against the standard rate.

Question 5

300000 210000

Account balance Account balance

before Proration After Proration

Work in 60500 3% 9073 6351 75924

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

10

progress

Finished Goals 90000 4% 13497 9448 112944

cost of goods sold 1850000 92% 277431 194201 2321632

Total 2000500 300000 210000 2510500

Allocation technique for the costing is the strategy for costing where the overheads depend on

the genuine overheads of the firm. With the utilization of this technique the whole of all sums

is charged to the undertaking of the overhead. The allocated overhead rate is determined

based on the aggregate sum of the work in advancement, cost of merchandise sold and the

completed products sold. Rest the sum is bifurcated based on the distributed and the applied

overhead (Detek, 2018). Therefore the method of the proration of the costs of the overheads

are utilised by the company when both the applied and the actual overhead are given to the

company and the combination of both is required.

10

progress

Finished Goals 90000 4% 13497 9448 112944

cost of goods sold 1850000 92% 277431 194201 2321632

Total 2000500 300000 210000 2510500

Allocation technique for the costing is the strategy for costing where the overheads depend on

the genuine overheads of the firm. With the utilization of this technique the whole of all sums

is charged to the undertaking of the overhead. The allocated overhead rate is determined

based on the aggregate sum of the work in advancement, cost of merchandise sold and the

completed products sold. Rest the sum is bifurcated based on the distributed and the applied

overhead (Detek, 2018). Therefore the method of the proration of the costs of the overheads

are utilised by the company when both the applied and the actual overhead are given to the

company and the combination of both is required.

COSTING ANALYSIS

11

References

Angelopoulos, M., and Pollalis, Y. (2017) Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Bennett, M. and James, P., (2017) The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Christian, D. (2018) Building Cost Management: Case Study Using Costing

Methods. IJAME.

Cooper, R., (2017) Target costing and value engineering. New York: Routledge.

Detek, (2018) Proration Method of Overhead Allocation [online] Available from

https://help.deltek.com/Product/Vision/7.6/oa_proration_method_of_overhead_allocation.ht

ml [Accessed on 18th January 2019]

Hada, M. S., Chakravarty, A., and Mukherjee, P. (2014) Activity based costing of diagnostic

procedures at a nuclear medicine center of a tertiary care hospital. Indian journal of nuclear

medicine: IJNM: the official journal of the Society of Nuclear Medicine, India, 29(4), 241.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T. (2012) Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Jiménez, V., Duarte, C., and Afonso, P. (2015) Cost System Under Uncertainty: A Case

Study in the Imaging Area of a Hospital. In Enhancing Synergies in a Collaborative

Environment (pp. 325-333). Springer, Cham.

Mahal, I. and Hossain, A., (2015) Activity-Based Costing (ABC)–An Effective Tool for

Better Management. Research Journal of Finance and Accounting, 6(4), pp.66-74.

11

References

Angelopoulos, M., and Pollalis, Y. (2017) Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Bennett, M. and James, P., (2017) The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Christian, D. (2018) Building Cost Management: Case Study Using Costing

Methods. IJAME.

Cooper, R., (2017) Target costing and value engineering. New York: Routledge.

Detek, (2018) Proration Method of Overhead Allocation [online] Available from

https://help.deltek.com/Product/Vision/7.6/oa_proration_method_of_overhead_allocation.ht

ml [Accessed on 18th January 2019]

Hada, M. S., Chakravarty, A., and Mukherjee, P. (2014) Activity based costing of diagnostic

procedures at a nuclear medicine center of a tertiary care hospital. Indian journal of nuclear

medicine: IJNM: the official journal of the Society of Nuclear Medicine, India, 29(4), 241.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T. (2012) Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Jiménez, V., Duarte, C., and Afonso, P. (2015) Cost System Under Uncertainty: A Case

Study in the Imaging Area of a Hospital. In Enhancing Synergies in a Collaborative

Environment (pp. 325-333). Springer, Cham.

Mahal, I. and Hossain, A., (2015) Activity-Based Costing (ABC)–An Effective Tool for

Better Management. Research Journal of Finance and Accounting, 6(4), pp.66-74.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.