ACC200 Costing Analysis: Traditional and Activity Based Costing

VerifiedAdded on 2023/04/22

|13

|2568

|98

Report

AI Summary

This report provides a comprehensive costing analysis for Fantori Ltd, comparing traditional and activity-based costing (ABC) methods to understand why an overseas buyer is only interested in the advanced sewing machine model. The analysis includes calculations of cost per unit under both costing methods, income statements, and a discussion of the importance of accurate product costing. It also explains the difference between actual and applied overhead, and the proration method of costing. The report concludes that the traditional costing method may underestimate the cost of the advanced model, leading to the buyer's preference, while ABC costing provides a more accurate view of individual costs. The report highlights the importance of accurate product costing for informed decision-making and maintaining a competitive advantage. Desklib provides a platform for students to access similar solved assignments and past papers.

Running Head: COSTING ANALYSIS

0

Costing Analysis

Traditional and ABC Costing

0

Costing Analysis

Traditional and ABC Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

1

Table of Contents

Answer to Question-1................................................................................................................2

Answer to Question-2................................................................................................................4

Answer to Question-3................................................................................................................7

Analysis................................................................................................................................10

Importance of accurate product costing...............................................................................10

Answer to Question 4...............................................................................................................11

Answer to Question 5...............................................................................................................12

Bibliography.............................................................................................................................14

1

Table of Contents

Answer to Question-1................................................................................................................2

Answer to Question-2................................................................................................................4

Answer to Question-3................................................................................................................7

Analysis................................................................................................................................10

Importance of accurate product costing...............................................................................10

Answer to Question 4...............................................................................................................11

Answer to Question 5...............................................................................................................12

Bibliography.............................................................................................................................14

COSTING ANALYSIS

2

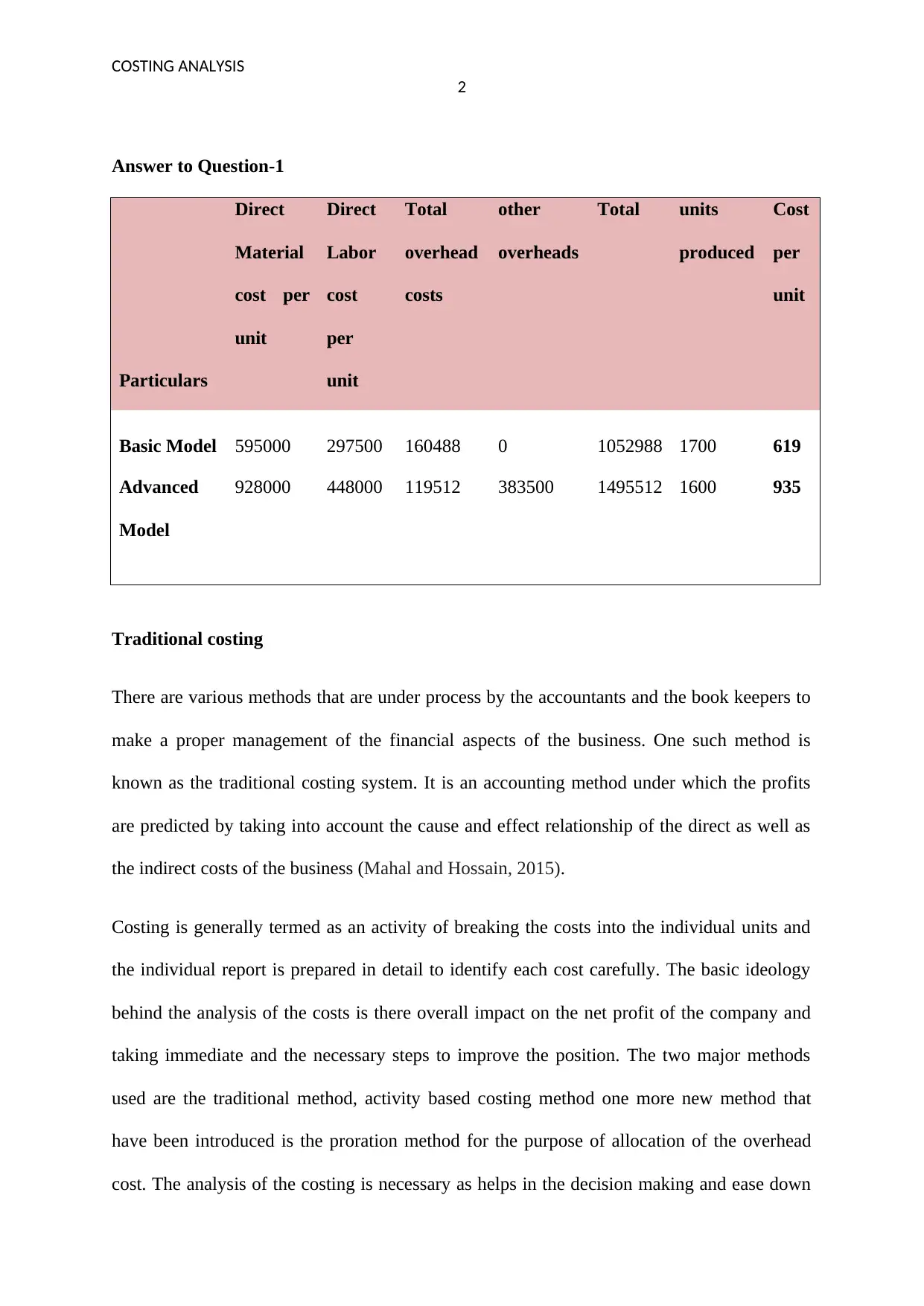

Answer to Question-1

Particulars

Direct

Material

cost per

unit

Direct

Labor

cost

per

unit

Total

overhead

costs

other

overheads

Total units

produced

Cost

per

unit

Basic Model 595000 297500 160488 0 1052988 1700 619

Advanced

Model

928000 448000 119512 383500 1495512 1600 935

Traditional costing

There are various methods that are under process by the accountants and the book keepers to

make a proper management of the financial aspects of the business. One such method is

known as the traditional costing system. It is an accounting method under which the profits

are predicted by taking into account the cause and effect relationship of the direct as well as

the indirect costs of the business (Mahal and Hossain, 2015).

Costing is generally termed as an activity of breaking the costs into the individual units and

the individual report is prepared in detail to identify each cost carefully. The basic ideology

behind the analysis of the costs is there overall impact on the net profit of the company and

taking immediate and the necessary steps to improve the position. The two major methods

used are the traditional method, activity based costing method one more new method that

have been introduced is the proration method for the purpose of allocation of the overhead

cost. The analysis of the costing is necessary as helps in the decision making and ease down

2

Answer to Question-1

Particulars

Direct

Material

cost per

unit

Direct

Labor

cost

per

unit

Total

overhead

costs

other

overheads

Total units

produced

Cost

per

unit

Basic Model 595000 297500 160488 0 1052988 1700 619

Advanced

Model

928000 448000 119512 383500 1495512 1600 935

Traditional costing

There are various methods that are under process by the accountants and the book keepers to

make a proper management of the financial aspects of the business. One such method is

known as the traditional costing system. It is an accounting method under which the profits

are predicted by taking into account the cause and effect relationship of the direct as well as

the indirect costs of the business (Mahal and Hossain, 2015).

Costing is generally termed as an activity of breaking the costs into the individual units and

the individual report is prepared in detail to identify each cost carefully. The basic ideology

behind the analysis of the costs is there overall impact on the net profit of the company and

taking immediate and the necessary steps to improve the position. The two major methods

used are the traditional method, activity based costing method one more new method that

have been introduced is the proration method for the purpose of allocation of the overhead

cost. The analysis of the costing is necessary as helps in the decision making and ease down

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

3

the complex transactions into the simpler ones. It’s necessary of the business to recognise the

potential costs and the benefits associated with them and if the business fails it results into the

sub optimal decisions ultimately. Also performing the cost analysis helps in giving an

opportunity to the management to dive into the specifics of the particular funds required to

spend on the product. The act of defining and the identification of the costs is a technical one

and it reduces time and energy of the employees (Bennett and James, 2017).

Traditional costing is the method where the cost of the overhead is calculated by loading the

percentage of the total overhead costs to the particular and the significant component. The

percentage so arrived is generally the percentage of the machine hours as compared to the

overall percentages and therefore the machine hours are treated as the base for the purpose of

the calculation of the factory overhead (Xu, Frankwick and Ramirez, 2016).

The first table represent the calculation of the cost per unit of the Sewing Easy under the

traditional method. For the purpose of the calculation of the overhead costs the machine

hours are made as the base and thereafter the figure of the overhead calculation is arrived at

60 and 80 respectively for the basic as well as the advanced model (Cooper, 2017).

Further the second table displays the cost per unit taking into consideration the cost of the

direct labour materials per unit and the labour per unit (Patiar, 2016).

Answer to Question-2

Calculation of cost per unit under activity based costing method

Particulars

Basic Model Advanced

Model

Direct Material cost per unit 350 580

Direct Labor cost per unit 175 280

3

the complex transactions into the simpler ones. It’s necessary of the business to recognise the

potential costs and the benefits associated with them and if the business fails it results into the

sub optimal decisions ultimately. Also performing the cost analysis helps in giving an

opportunity to the management to dive into the specifics of the particular funds required to

spend on the product. The act of defining and the identification of the costs is a technical one

and it reduces time and energy of the employees (Bennett and James, 2017).

Traditional costing is the method where the cost of the overhead is calculated by loading the

percentage of the total overhead costs to the particular and the significant component. The

percentage so arrived is generally the percentage of the machine hours as compared to the

overall percentages and therefore the machine hours are treated as the base for the purpose of

the calculation of the factory overhead (Xu, Frankwick and Ramirez, 2016).

The first table represent the calculation of the cost per unit of the Sewing Easy under the

traditional method. For the purpose of the calculation of the overhead costs the machine

hours are made as the base and thereafter the figure of the overhead calculation is arrived at

60 and 80 respectively for the basic as well as the advanced model (Cooper, 2017).

Further the second table displays the cost per unit taking into consideration the cost of the

direct labour materials per unit and the labour per unit (Patiar, 2016).

Answer to Question-2

Calculation of cost per unit under activity based costing method

Particulars

Basic Model Advanced

Model

Direct Material cost per unit 350 580

Direct Labor cost per unit 175 280

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

4

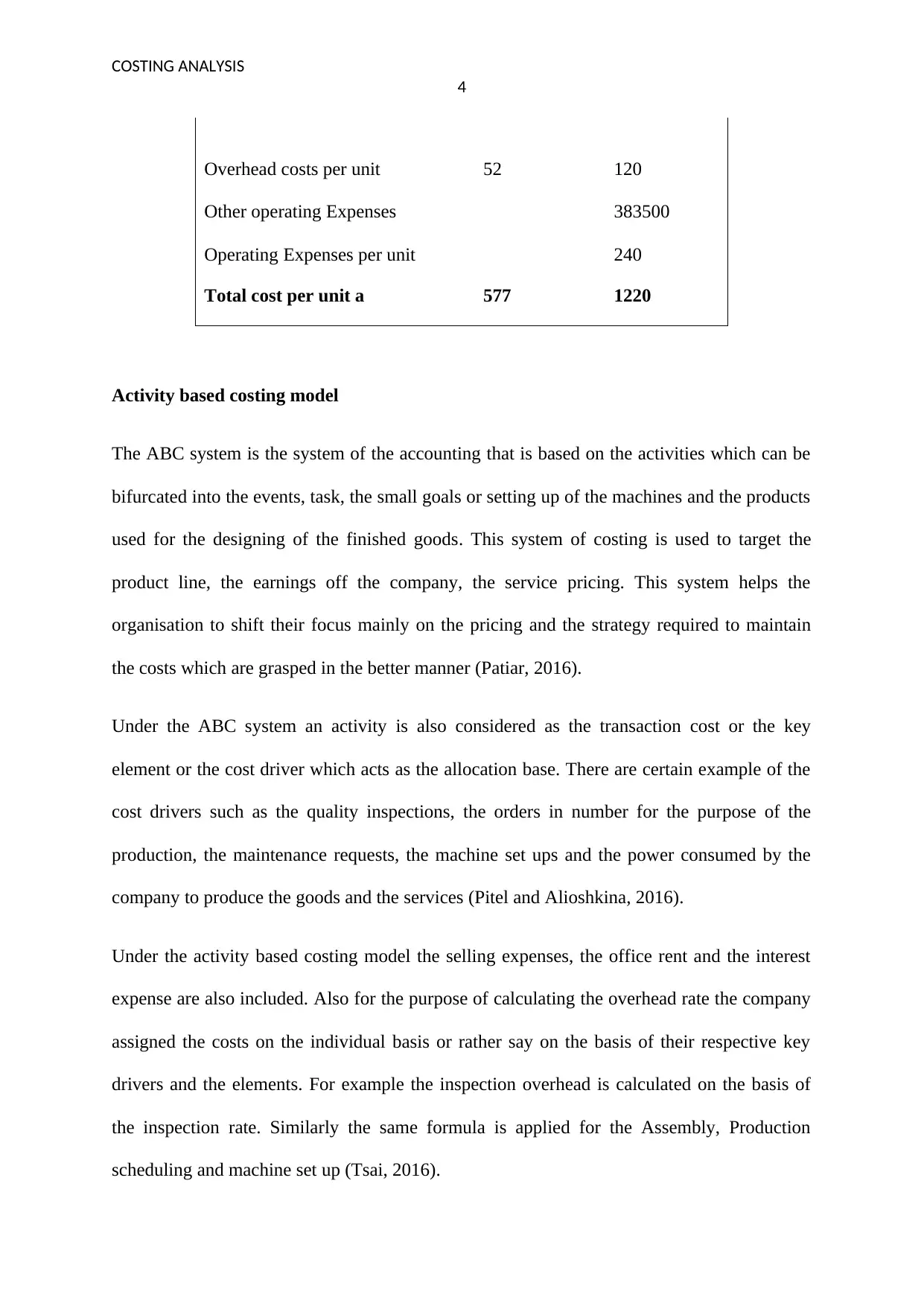

Overhead costs per unit 52 120

Other operating Expenses 383500

Operating Expenses per unit 240

Total cost per unit a 577 1220

Activity based costing model

The ABC system is the system of the accounting that is based on the activities which can be

bifurcated into the events, task, the small goals or setting up of the machines and the products

used for the designing of the finished goods. This system of costing is used to target the

product line, the earnings off the company, the service pricing. This system helps the

organisation to shift their focus mainly on the pricing and the strategy required to maintain

the costs which are grasped in the better manner (Patiar, 2016).

Under the ABC system an activity is also considered as the transaction cost or the key

element or the cost driver which acts as the allocation base. There are certain example of the

cost drivers such as the quality inspections, the orders in number for the purpose of the

production, the maintenance requests, the machine set ups and the power consumed by the

company to produce the goods and the services (Pitel and Alioshkina, 2016).

Under the activity based costing model the selling expenses, the office rent and the interest

expense are also included. Also for the purpose of calculating the overhead rate the company

assigned the costs on the individual basis or rather say on the basis of their respective key

drivers and the elements. For example the inspection overhead is calculated on the basis of

the inspection rate. Similarly the same formula is applied for the Assembly, Production

scheduling and machine set up (Tsai, 2016).

4

Overhead costs per unit 52 120

Other operating Expenses 383500

Operating Expenses per unit 240

Total cost per unit a 577 1220

Activity based costing model

The ABC system is the system of the accounting that is based on the activities which can be

bifurcated into the events, task, the small goals or setting up of the machines and the products

used for the designing of the finished goods. This system of costing is used to target the

product line, the earnings off the company, the service pricing. This system helps the

organisation to shift their focus mainly on the pricing and the strategy required to maintain

the costs which are grasped in the better manner (Patiar, 2016).

Under the ABC system an activity is also considered as the transaction cost or the key

element or the cost driver which acts as the allocation base. There are certain example of the

cost drivers such as the quality inspections, the orders in number for the purpose of the

production, the maintenance requests, the machine set ups and the power consumed by the

company to produce the goods and the services (Pitel and Alioshkina, 2016).

Under the activity based costing model the selling expenses, the office rent and the interest

expense are also included. Also for the purpose of calculating the overhead rate the company

assigned the costs on the individual basis or rather say on the basis of their respective key

drivers and the elements. For example the inspection overhead is calculated on the basis of

the inspection rate. Similarly the same formula is applied for the Assembly, Production

scheduling and machine set up (Tsai, 2016).

COSTING ANALYSIS

5

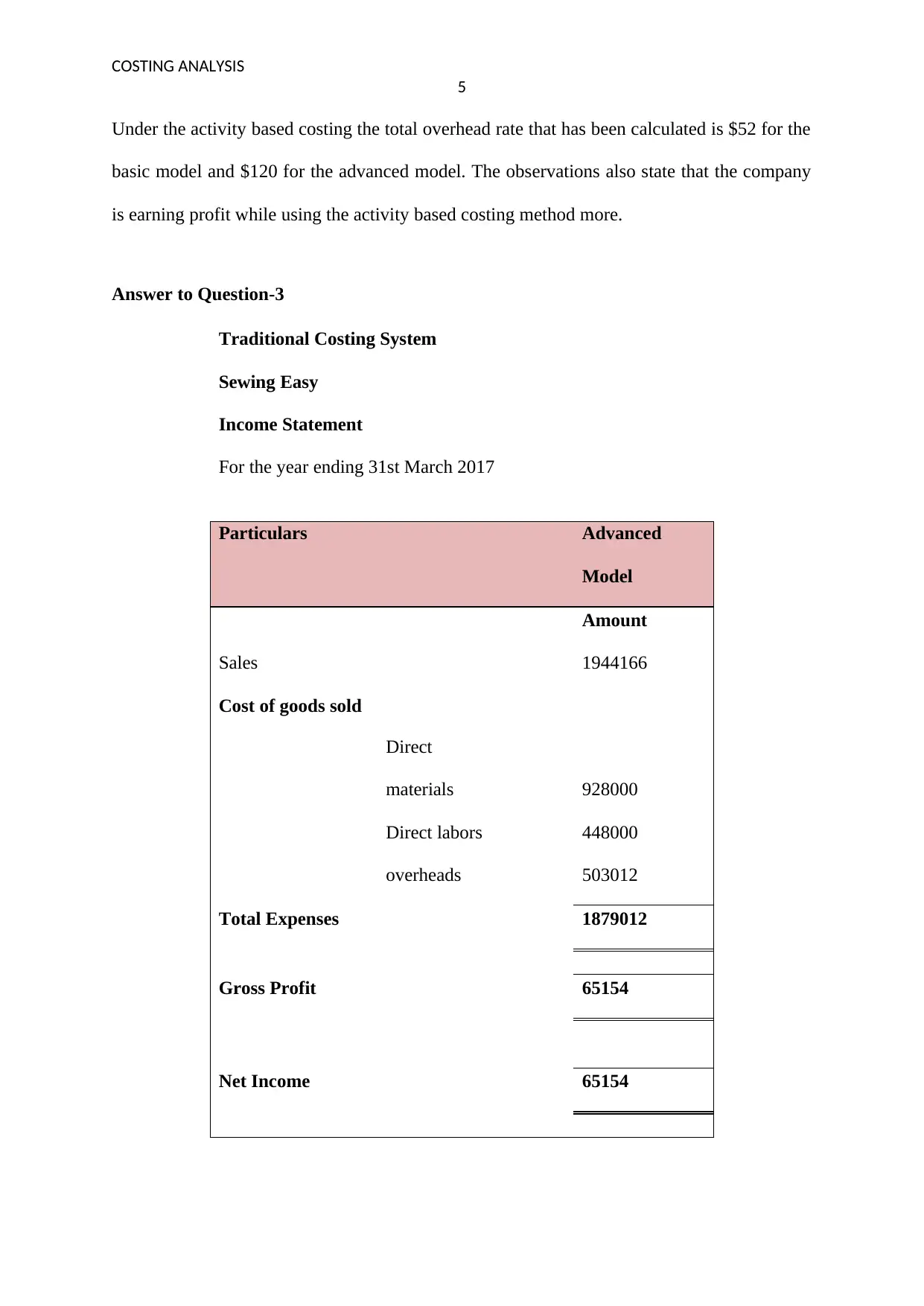

Under the activity based costing the total overhead rate that has been calculated is $52 for the

basic model and $120 for the advanced model. The observations also state that the company

is earning profit while using the activity based costing method more.

Answer to Question-3

Traditional Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials 928000

Direct labors 448000

overheads 503012

Total Expenses 1879012

Gross Profit 65154

Net Income 65154

5

Under the activity based costing the total overhead rate that has been calculated is $52 for the

basic model and $120 for the advanced model. The observations also state that the company

is earning profit while using the activity based costing method more.

Answer to Question-3

Traditional Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials 928000

Direct labors 448000

overheads 503012

Total Expenses 1879012

Gross Profit 65154

Net Income 65154

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

6

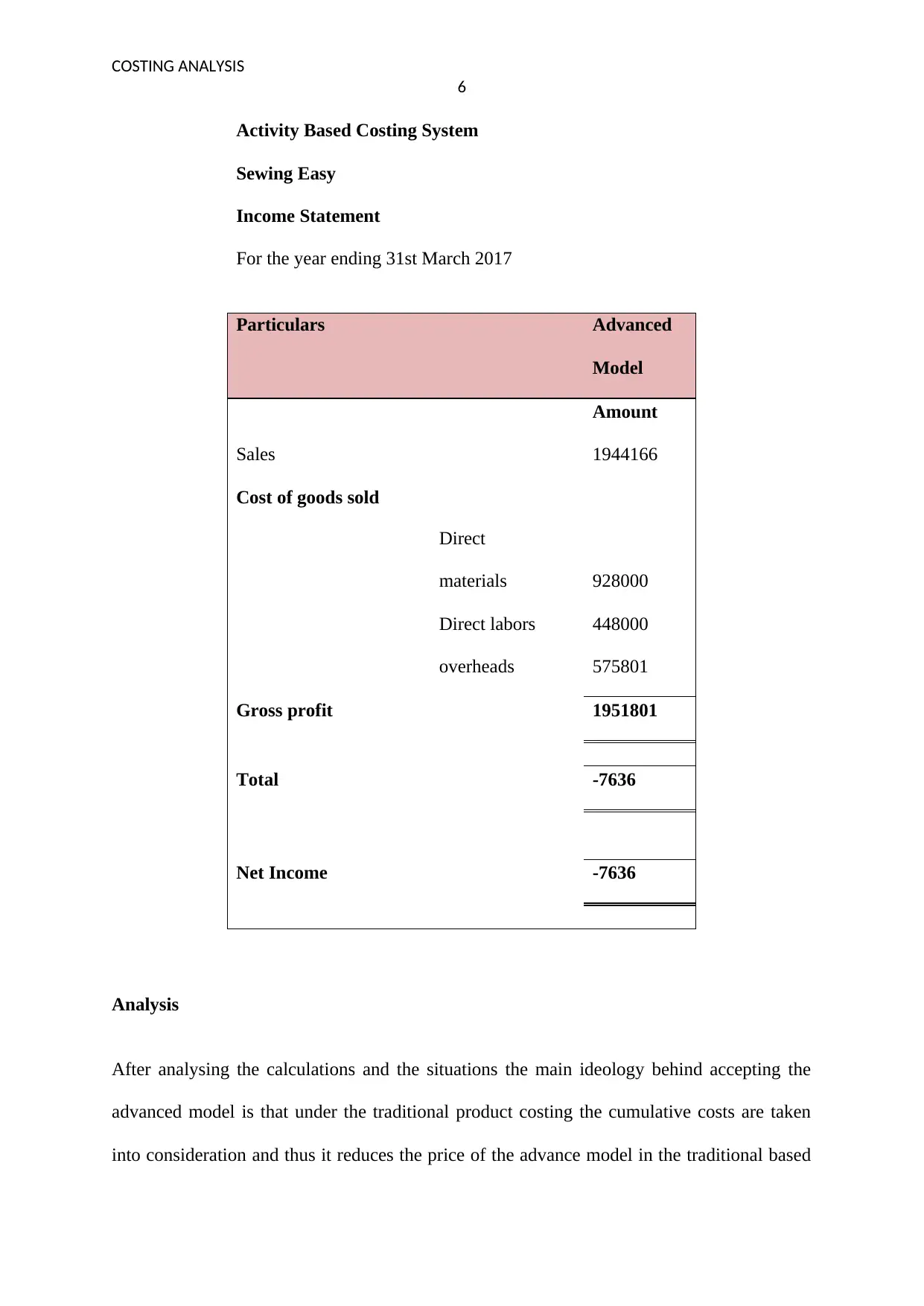

Activity Based Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials 928000

Direct labors 448000

overheads 575801

Gross profit 1951801

Total -7636

Net Income -7636

Analysis

After analysing the calculations and the situations the main ideology behind accepting the

advanced model is that under the traditional product costing the cumulative costs are taken

into consideration and thus it reduces the price of the advance model in the traditional based

6

Activity Based Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Advanced

Model

Amount

Sales 1944166

Cost of goods sold

Direct

materials 928000

Direct labors 448000

overheads 575801

Gross profit 1951801

Total -7636

Net Income -7636

Analysis

After analysing the calculations and the situations the main ideology behind accepting the

advanced model is that under the traditional product costing the cumulative costs are taken

into consideration and thus it reduces the price of the advance model in the traditional based

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

7

costing system. Further under the activity based costing system the overall loss is also

suffered by the company and hence the overseas buyer accepted the idea of the advanced

model because of the low price. Whereas in reality the correct method of calculating is the

activity based costing method that gives the transparent idea of the individual costs (Plank,

2018).

Importance of accurate product costing

For any company the authenticity and the accuracy of the financial statements is the most

important factor not only from the point of view of the managers but also from the point of

view of the investors and the shareholders. The accurate product costing helps the investors

to take the important decisions in deciding whether the funds invested by the investor are in

correct direction or not. The accurate product costing helps in determining the impact of the

budget where the costs are budgeted for the future on the basis of the current costs.

Furthermore, the income statement is also dependent upon the cost of goods sold and the

selling price of the product as well (Schram, et al 2015). This gives the true and fair view of

the costs to ascertain the original position to the investors investing in the company. The

assets and the inventory are also affected by the implications of the accurate product costing

and moreover if the product costs are not calculated correctly the value of the inventory will

be inaccurate. This will distort the calculation and the picture will not be transparent

henceforth, these are the several reasons that determine the importance of the accurate

product costing. The accurate product costing will not only help in enhancing the financial

position of the business but also helps in having the competitive advantage over the

competitors (Stark, 2015).

7

costing system. Further under the activity based costing system the overall loss is also

suffered by the company and hence the overseas buyer accepted the idea of the advanced

model because of the low price. Whereas in reality the correct method of calculating is the

activity based costing method that gives the transparent idea of the individual costs (Plank,

2018).

Importance of accurate product costing

For any company the authenticity and the accuracy of the financial statements is the most

important factor not only from the point of view of the managers but also from the point of

view of the investors and the shareholders. The accurate product costing helps the investors

to take the important decisions in deciding whether the funds invested by the investor are in

correct direction or not. The accurate product costing helps in determining the impact of the

budget where the costs are budgeted for the future on the basis of the current costs.

Furthermore, the income statement is also dependent upon the cost of goods sold and the

selling price of the product as well (Schram, et al 2015). This gives the true and fair view of

the costs to ascertain the original position to the investors investing in the company. The

assets and the inventory are also affected by the implications of the accurate product costing

and moreover if the product costs are not calculated correctly the value of the inventory will

be inaccurate. This will distort the calculation and the picture will not be transparent

henceforth, these are the several reasons that determine the importance of the accurate

product costing. The accurate product costing will not only help in enhancing the financial

position of the business but also helps in having the competitive advantage over the

competitors (Stark, 2015).

COSTING ANALYSIS

8

Answer to Question 4

The accounting includes the wide range of the terms and two such terms are the actual

overhead and the applied overhead. The actual overhead of any company can be termed as

the factory costs of the indirect nature that have been incurred or spent for in reality. This

includes all the overhead costs except the direct material and the cost of the labour. Few

examples of the costs that are under the category of the actual overheads are Equipment

maintenance, factory insurance, factory utilities, production supplies, factory rent, factory

property taxes. There may a slight difference between the actual overheads and the applied

overheads which is based on the standard rate of the overhead (Vaxevanidis and Petropoulos,

2018).

Applied overhead is the overhead under the method of the costing. Applied overhead can be

termed as the fixed charge assigned to a production job or department within a company. In

contrast to the general overheads the applied overheads have the equal importance. The

applied overhead can be displayed by the best example of the depreciation and insurance

(Accounting Coach 2018).

From the point of view of the management the applied overheads is considered as the

standard part of the financial planning and the analysis method. In order to serve and

facilitate the better capital budgeting decisions the review of the applied overheads is

necessary and crucial for the management. For the purpose of the calculation most of the

industries make use of the standard rate rather than bifurcation of the same (Popesko,

Papadaki and Novák, 2015).

Further the actual overhead and the applied overhead is different from each other at the end

of the day because since the future overheads along with the machine hours cannot be judged

with the certainty and in relation to this the actual hours of the machine will not occur in the

8

Answer to Question 4

The accounting includes the wide range of the terms and two such terms are the actual

overhead and the applied overhead. The actual overhead of any company can be termed as

the factory costs of the indirect nature that have been incurred or spent for in reality. This

includes all the overhead costs except the direct material and the cost of the labour. Few

examples of the costs that are under the category of the actual overheads are Equipment

maintenance, factory insurance, factory utilities, production supplies, factory rent, factory

property taxes. There may a slight difference between the actual overheads and the applied

overheads which is based on the standard rate of the overhead (Vaxevanidis and Petropoulos,

2018).

Applied overhead is the overhead under the method of the costing. Applied overhead can be

termed as the fixed charge assigned to a production job or department within a company. In

contrast to the general overheads the applied overheads have the equal importance. The

applied overhead can be displayed by the best example of the depreciation and insurance

(Accounting Coach 2018).

From the point of view of the management the applied overheads is considered as the

standard part of the financial planning and the analysis method. In order to serve and

facilitate the better capital budgeting decisions the review of the applied overheads is

necessary and crucial for the management. For the purpose of the calculation most of the

industries make use of the standard rate rather than bifurcation of the same (Popesko,

Papadaki and Novák, 2015).

Further the actual overhead and the applied overhead is different from each other at the end

of the day because since the future overheads along with the machine hours cannot be judged

with the certainty and in relation to this the actual hours of the machine will not occur in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

9

uniform manner therefore there will always be the difference between the actual as well as

the applied overhead.

In addition to this if the overheads that are assigned more than the actual amount than the

overheads are termed as the applied overhead otherwise the case is the reversal case. As and

when the cost of goods is calculated the amount it is in excessive nature it can be termed as

the under applied overhead.

There are few methods to deal with the situations where there are under and the over applied

issues.

The first method allows the transfer of the amount to the next financial year.

The second method the journal entry is passed and the amount is transferred to the

profit and loss account.

A supplementary rate is considered against the standard rate.

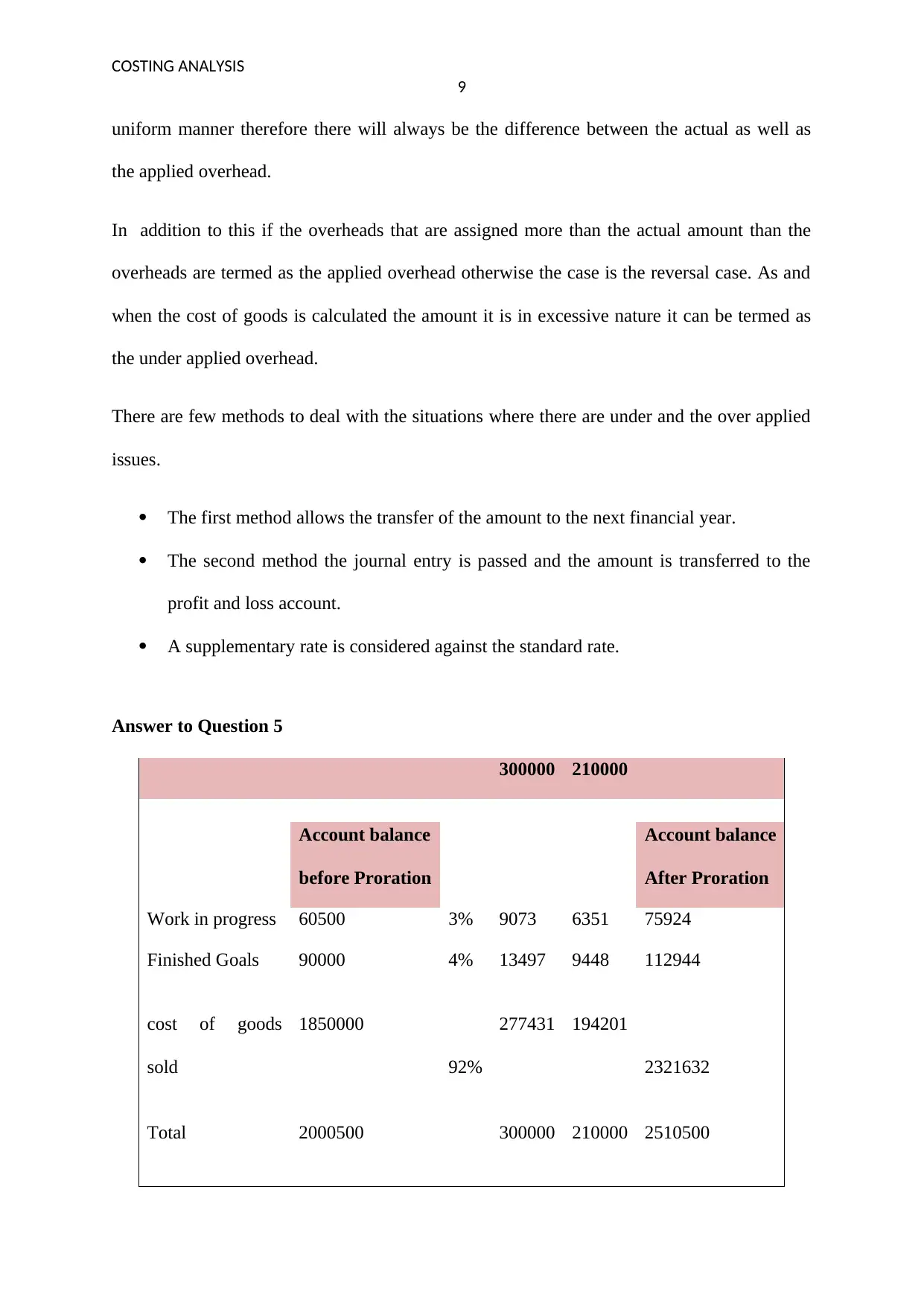

Answer to Question 5

300000 210000

Account balance Account balance

before Proration After Proration

Work in progress 60500 3% 9073 6351 75924

Finished Goals 90000 4% 13497 9448 112944

cost of goods

sold

1850000

92%

277431 194201

2321632

Total 2000500 300000 210000 2510500

9

uniform manner therefore there will always be the difference between the actual as well as

the applied overhead.

In addition to this if the overheads that are assigned more than the actual amount than the

overheads are termed as the applied overhead otherwise the case is the reversal case. As and

when the cost of goods is calculated the amount it is in excessive nature it can be termed as

the under applied overhead.

There are few methods to deal with the situations where there are under and the over applied

issues.

The first method allows the transfer of the amount to the next financial year.

The second method the journal entry is passed and the amount is transferred to the

profit and loss account.

A supplementary rate is considered against the standard rate.

Answer to Question 5

300000 210000

Account balance Account balance

before Proration After Proration

Work in progress 60500 3% 9073 6351 75924

Finished Goals 90000 4% 13497 9448 112944

cost of goods

sold

1850000

92%

277431 194201

2321632

Total 2000500 300000 210000 2510500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

10

Proration method of the costing is the method of costing where the overheads are based on

the actual overheads of the firm. With the use of this method the sum of all amounts is

charged to the project of the overhead (Detek, 2018). The prorated overhead percentage rate

is calculated on the basis of the total amount of the work in progress, cost of goods sold and

the finished goods sold. Rest the amount is bifurcated on the basis of the allocated and the

applied overhead (Manunen, 2013).

10

Proration method of the costing is the method of costing where the overheads are based on

the actual overheads of the firm. With the use of this method the sum of all amounts is

charged to the project of the overhead (Detek, 2018). The prorated overhead percentage rate

is calculated on the basis of the total amount of the work in progress, cost of goods sold and

the finished goods sold. Rest the amount is bifurcated on the basis of the allocated and the

applied overhead (Manunen, 2013).

COSTING ANALYSIS

11

Bibliography

Accounting Coach (2018) What is the difference between actual overhead and applied

overhead? [online] https://www.accountingcoach.com/blog/dfifference-actual-overhead-

applied-overhead [Accessed on 15th January 2018].

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Cooper, R., 2017. Target costing and value engineering. New York: Routledge.

Detek, (2018) Proration Method of Overhead Allocation [online] Available from

https://help.deltek.com/Product/Vision/7.6/oa_proration_method_of_overhead_allocation.ht

ml [Accessed on 18th January 2019]

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), pp.66-74.

Manunen, O. (2013) An activity-based costing model for logistics operations of

manufacturers and wholesalers, International Journal of Logistics, 3(1), 53-65.

Patiar, A., (2016) Costs allocation practices: Evidence of hotels in Australia, Journal of

Hospitality and Tourism Management, 26(1), pp.1-8.

Pitel, N.Y. and Alioshkina, L.P., (2016) ABC analysis as a tool of optimization of marketing

management of export-led enterprises, New York: Springer.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost

Systems (pp. 1-5). Springer Gabler, Wiesbaden.

11

Bibliography

Accounting Coach (2018) What is the difference between actual overhead and applied

overhead? [online] https://www.accountingcoach.com/blog/dfifference-actual-overhead-

applied-overhead [Accessed on 15th January 2018].

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Cooper, R., 2017. Target costing and value engineering. New York: Routledge.

Detek, (2018) Proration Method of Overhead Allocation [online] Available from

https://help.deltek.com/Product/Vision/7.6/oa_proration_method_of_overhead_allocation.ht

ml [Accessed on 18th January 2019]

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), pp.66-74.

Manunen, O. (2013) An activity-based costing model for logistics operations of

manufacturers and wholesalers, International Journal of Logistics, 3(1), 53-65.

Patiar, A., (2016) Costs allocation practices: Evidence of hotels in Australia, Journal of

Hospitality and Tourism Management, 26(1), pp.1-8.

Pitel, N.Y. and Alioshkina, L.P., (2016) ABC analysis as a tool of optimization of marketing

management of export-led enterprises, New York: Springer.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost

Systems (pp. 1-5). Springer Gabler, Wiesbaden.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.