ACC2005 Management Accounting: Budgeting, Technical and Non-Technical

VerifiedAdded on 2023/03/30

|7

|989

|306

Report

AI Summary

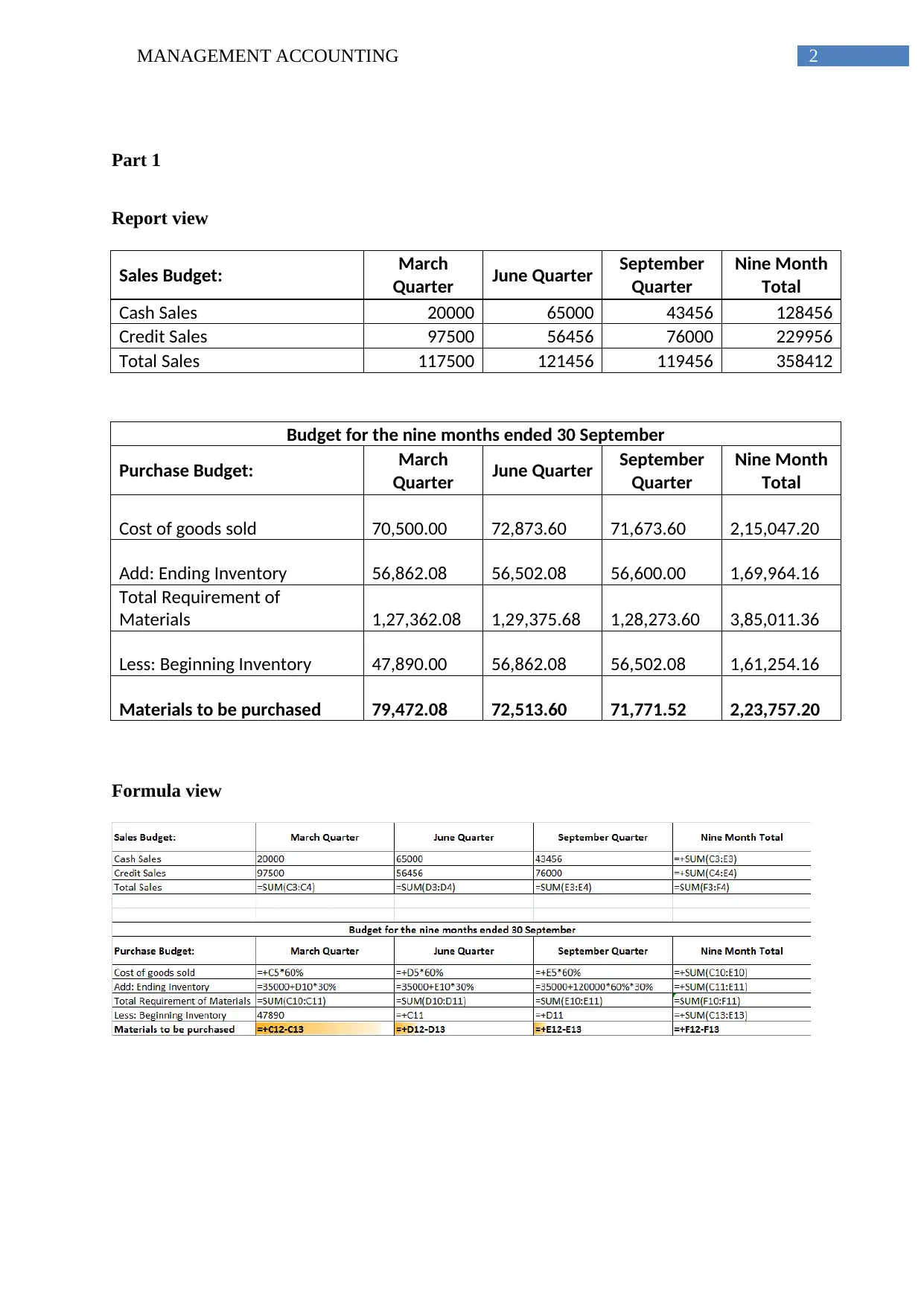

This report provides a detailed analysis of budgeting in management accounting, covering both technical and non-technical aspects. It begins with a practical application of budgeting, presenting a sales and purchase budget for a nine-month period, including calculations for cash sales, credit sales, cost of goods sold, and materials to be purchased. The report then delves into the technical aspects of budgeting, emphasizing the importance of accurate analysis and estimation. Furthermore, it explores the non-technical dimensions, such as satisficing, political influences, and budget ploys. The report concludes that budgeting is not limited to expense estimation but extends to predicting profits and income, highlighting the crucial role of professional expertise and the interplay of technical and non-technical elements in effective budgeting.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.