ACC201 Financial Accounting: In-depth Analysis of Ansell Ltd. Report

VerifiedAdded on 2023/06/12

|13

|2530

|404

Report

AI Summary

This report provides a financial analysis of Ansell Ltd., focusing on the company's expense classification methods, accounting policies, and treatment of depreciation. It examines the rationale behind using a functional classification of expenses, highlighting its suitability for larger multinational corporations. The report also delves into Ansell's accounting policies, particularly concerning consolidation principles, foreign currency transactions, and the valuation of noncurrent assets. Furthermore, it analyzes the notes to the 2016 financial statement, detailing the cost of plant, properties, and equipment, as well as the depreciation amount, period, and method used. Finally, the report discusses the company's approach to impairment, particularly for intangible assets and goodwill, providing a comprehensive overview of Ansell Ltd.'s financial reporting practices. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of Student:

Name of University:

Author’s Note:

Financial Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Table of Contents

Part 1................................................................................................................................................2

Part 2................................................................................................................................................2

Introduction......................................................................................................................................2

Task 1: Analysis of Expenses..........................................................................................................2

a. Determination of expenses.......................................................................................................2

b. Reasons for different method of classification of expenses used by the company.................3

Task 2: Accounting Policy...............................................................................................................3

Task 3: Notes to the 2016 financial statement.................................................................................5

a. Cost of plant, properties and equipment..................................................................................5

b. Depreciation amount................................................................................................................5

c. Depreciation period..................................................................................................................6

d. Depreciation method................................................................................................................7

e. Impairment...............................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Part 1................................................................................................................................................2

Part 2................................................................................................................................................2

Introduction......................................................................................................................................2

Task 1: Analysis of Expenses..........................................................................................................2

a. Determination of expenses.......................................................................................................2

b. Reasons for different method of classification of expenses used by the company.................3

Task 2: Accounting Policy...............................................................................................................3

Task 3: Notes to the 2016 financial statement.................................................................................5

a. Cost of plant, properties and equipment..................................................................................5

b. Depreciation amount................................................................................................................5

c. Depreciation period..................................................................................................................6

d. Depreciation method................................................................................................................7

e. Impairment...............................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

2FINANCIAL ACCOUNTING

Part 1

a. Name of the company - Ansell Ltd.

b. Annual Report Web Link-

http://sc-cdn-prod.azureedge.net/-/media/Corporate/MainWebsite/About/Investor-Center/

Annual-Report-2016/Annual-Report-to-Shareholders-2016.pdf?

la=en&modified=20160826151358

c. Current Share Price of the company- AUD 26.1

Part 2

Introduction

Ansell Ltd. Is recognised as the global leader in terms of facilitating the various types of

the safety equipment. The development and design of the manufacturing activities are considered

with the range of activities which includes increasing demand from the customers. Some of the

various types of the important products of the company has been seen to be ranging from

“industry gloves and sleeve, medical grade glove, protective clothing and medical safety

devices”. The discourse of the study has been seen to be considered with various types of the

facets which are seen to be considered with the expenses for Ansell Ltd. The other evaluations of

the study have been able to focus on the different rationale for the classification of the expenses.

The second part of the report has been further able to consider the relevant disclosures associated

to the accounting policies and changes in the accounting estimates and presence of the any error.

The final section of the study has made use of the financial notes in the annual report to depict

the relevant treatment of depreciation (Ansell.com 2018).

Task 1: Analysis of Expenses

a. Determination of expenses

The significant considerations in the financial statement of Ansell Ltd. has followed the

income statement preparation by considering the function of expenses. Therefore, the disclosure

of the expenses is seen to be based on the functions such as “distribution, cost of goods sold,

Part 1

a. Name of the company - Ansell Ltd.

b. Annual Report Web Link-

http://sc-cdn-prod.azureedge.net/-/media/Corporate/MainWebsite/About/Investor-Center/

Annual-Report-2016/Annual-Report-to-Shareholders-2016.pdf?

la=en&modified=20160826151358

c. Current Share Price of the company- AUD 26.1

Part 2

Introduction

Ansell Ltd. Is recognised as the global leader in terms of facilitating the various types of

the safety equipment. The development and design of the manufacturing activities are considered

with the range of activities which includes increasing demand from the customers. Some of the

various types of the important products of the company has been seen to be ranging from

“industry gloves and sleeve, medical grade glove, protective clothing and medical safety

devices”. The discourse of the study has been seen to be considered with various types of the

facets which are seen to be considered with the expenses for Ansell Ltd. The other evaluations of

the study have been able to focus on the different rationale for the classification of the expenses.

The second part of the report has been further able to consider the relevant disclosures associated

to the accounting policies and changes in the accounting estimates and presence of the any error.

The final section of the study has made use of the financial notes in the annual report to depict

the relevant treatment of depreciation (Ansell.com 2018).

Task 1: Analysis of Expenses

a. Determination of expenses

The significant considerations in the financial statement of Ansell Ltd. has followed the

income statement preparation by considering the function of expenses. Therefore, the disclosure

of the expenses is seen to be based on the functions such as “distribution, cost of goods sold,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

selling, general and administration expenses”. The calculation procedure of the expenses applied

with the multistep format is seen with the disclosure of the individual expenses as per each

function (Jack 2015).

Figure: Expenses classified by function for Ansell Ltd.

(Source: Sc-cdn-prod.azureedge.net. 2018)

b. Reasons for different method of classification of expenses used by the company

The main rationale for expenses is considered with the simplicity of the presentation

structured followed in the report. The small organizations tend to prefer disclosure associated to

the expenses based on the single step income statement. Therefore, the disclosing of the expenses

by nature which is more relevant in terms of following the expenses as function. The main

rationale for the classification of the expenses based on the functional role of in the bigger

multinationals in order to monitor the direct units which are assigned immediately to the

individual outputs, premium, rewards, material consumption directly associated to the outputs.

Moreover, the use of simple method of single step is considered with the presentation of the

expenses with the individual items like as “beginning inventory, purchases, rent expense,

depreciation expense, supplies expense, utilities expense, interest expense and purchases”

(Kallamu, Ashikin and Saat 2015).

Task 2: Accounting Policy

The compliance statement of the accounting policy is recognised as per the principles

which are stated in the “Australian Accounting Standards adopted by the Australian Accounting

Standards Board (AASB) and the Corporations Act 2001”. Moreover, it is further discerned that

selling, general and administration expenses”. The calculation procedure of the expenses applied

with the multistep format is seen with the disclosure of the individual expenses as per each

function (Jack 2015).

Figure: Expenses classified by function for Ansell Ltd.

(Source: Sc-cdn-prod.azureedge.net. 2018)

b. Reasons for different method of classification of expenses used by the company

The main rationale for expenses is considered with the simplicity of the presentation

structured followed in the report. The small organizations tend to prefer disclosure associated to

the expenses based on the single step income statement. Therefore, the disclosing of the expenses

by nature which is more relevant in terms of following the expenses as function. The main

rationale for the classification of the expenses based on the functional role of in the bigger

multinationals in order to monitor the direct units which are assigned immediately to the

individual outputs, premium, rewards, material consumption directly associated to the outputs.

Moreover, the use of simple method of single step is considered with the presentation of the

expenses with the individual items like as “beginning inventory, purchases, rent expense,

depreciation expense, supplies expense, utilities expense, interest expense and purchases”

(Kallamu, Ashikin and Saat 2015).

Task 2: Accounting Policy

The compliance statement of the accounting policy is recognised as per the principles

which are stated in the “Australian Accounting Standards adopted by the Australian Accounting

Standards Board (AASB) and the Corporations Act 2001”. Moreover, it is further discerned that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

the group adheres to the “International Financial Reporting Standards (IFRS)” which are

accepted by “International Accounting Standards Board (IAS)”. The three concern areas in this

report has been mentioned with the application of with “principles of consolidation”, “foreign

currency” and “recoverable amount on noncurrent asset” (Needles, Powers, and Susan

Crosson 2014). The consolidation process has been discerned with the several types of the

consideration taken with the effect of the transaction among the groups which are not fully

eliminated. Some of the major uses in the report has been traced in form of the differences in the

recording of the foreign currency translation reserve. The important issues in the recoverable

amount on the “noncurrent assets” are seen to be valued with the changes associated to the

carrying amount of these assets (Muhammad and Scrimgeour 2014).

the group adheres to the “International Financial Reporting Standards (IFRS)” which are

accepted by “International Accounting Standards Board (IAS)”. The three concern areas in this

report has been mentioned with the application of with “principles of consolidation”, “foreign

currency” and “recoverable amount on noncurrent asset” (Needles, Powers, and Susan

Crosson 2014). The consolidation process has been discerned with the several types of the

consideration taken with the effect of the transaction among the groups which are not fully

eliminated. Some of the major uses in the report has been traced in form of the differences in the

recording of the foreign currency translation reserve. The important issues in the recoverable

amount on the “noncurrent assets” are seen to be valued with the changes associated to the

carrying amount of these assets (Muhammad and Scrimgeour 2014).

5FINANCIAL ACCOUNTING

Figure: Accounting Policy main areas of concern in Ansell Ltd.

(Source: Sc-cdn-prod.azureedge.net. 2018)

Task 3: Notes to the 2016 financial statement

a. Cost of plant, properties and equipment

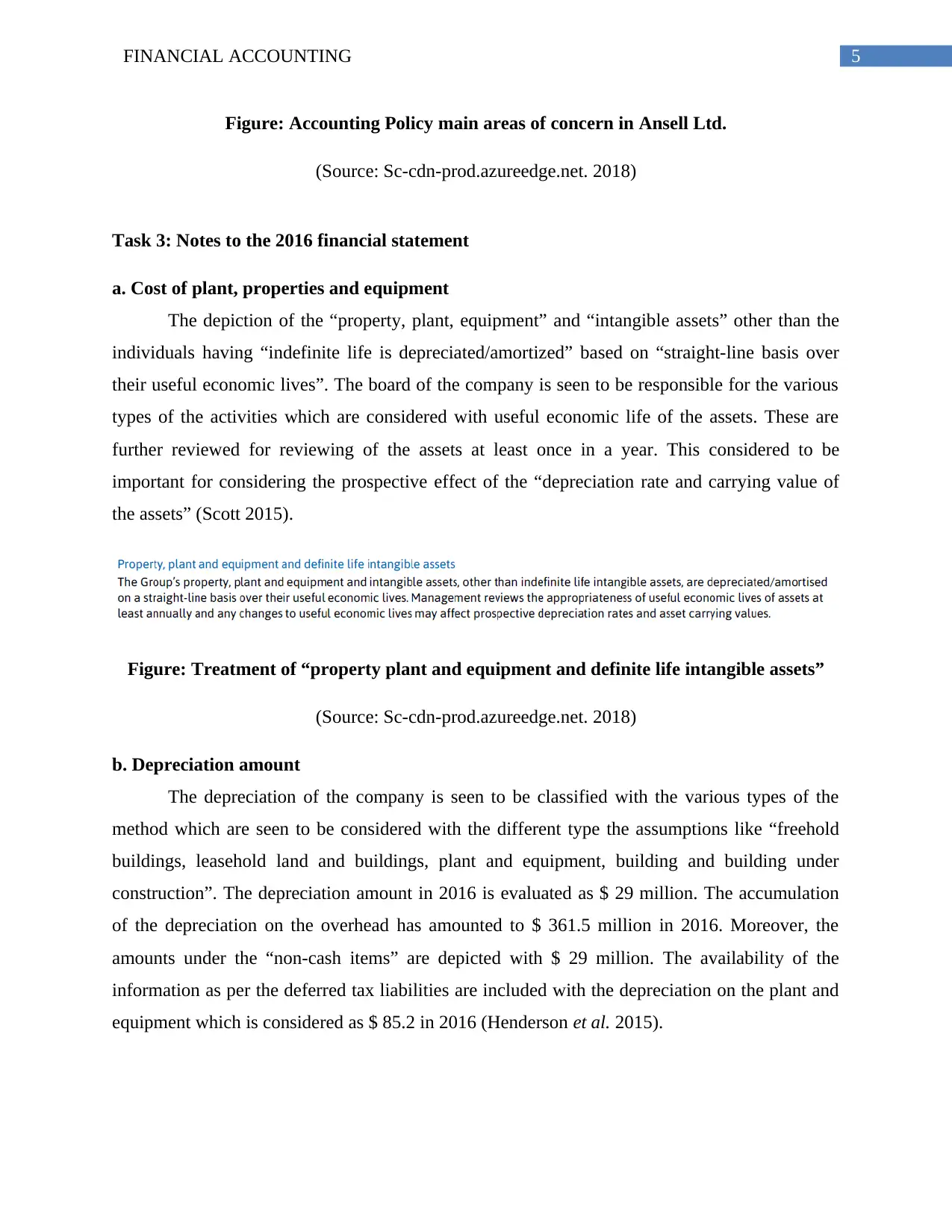

The depiction of the “property, plant, equipment” and “intangible assets” other than the

individuals having “indefinite life is depreciated/amortized” based on “straight-line basis over

their useful economic lives”. The board of the company is seen to be responsible for the various

types of the activities which are considered with useful economic life of the assets. These are

further reviewed for reviewing of the assets at least once in a year. This considered to be

important for considering the prospective effect of the “depreciation rate and carrying value of

the assets” (Scott 2015).

Figure: Treatment of “property plant and equipment and definite life intangible assets”

(Source: Sc-cdn-prod.azureedge.net. 2018)

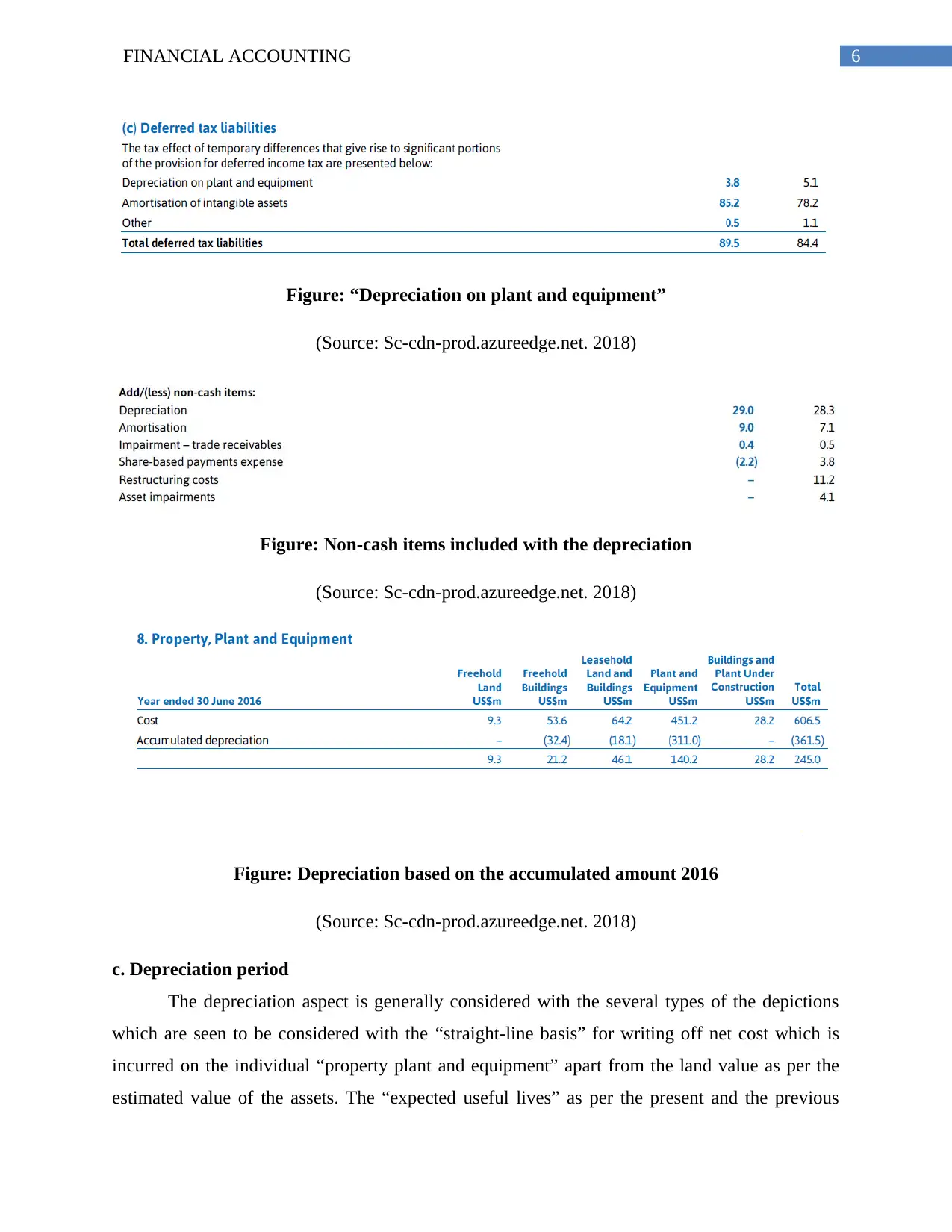

b. Depreciation amount

The depreciation of the company is seen to be classified with the various types of the

method which are seen to be considered with the different type the assumptions like “freehold

buildings, leasehold land and buildings, plant and equipment, building and building under

construction”. The depreciation amount in 2016 is evaluated as $ 29 million. The accumulation

of the depreciation on the overhead has amounted to $ 361.5 million in 2016. Moreover, the

amounts under the “non-cash items” are depicted with $ 29 million. The availability of the

information as per the deferred tax liabilities are included with the depreciation on the plant and

equipment which is considered as $ 85.2 in 2016 (Henderson et al. 2015).

Figure: Accounting Policy main areas of concern in Ansell Ltd.

(Source: Sc-cdn-prod.azureedge.net. 2018)

Task 3: Notes to the 2016 financial statement

a. Cost of plant, properties and equipment

The depiction of the “property, plant, equipment” and “intangible assets” other than the

individuals having “indefinite life is depreciated/amortized” based on “straight-line basis over

their useful economic lives”. The board of the company is seen to be responsible for the various

types of the activities which are considered with useful economic life of the assets. These are

further reviewed for reviewing of the assets at least once in a year. This considered to be

important for considering the prospective effect of the “depreciation rate and carrying value of

the assets” (Scott 2015).

Figure: Treatment of “property plant and equipment and definite life intangible assets”

(Source: Sc-cdn-prod.azureedge.net. 2018)

b. Depreciation amount

The depreciation of the company is seen to be classified with the various types of the

method which are seen to be considered with the different type the assumptions like “freehold

buildings, leasehold land and buildings, plant and equipment, building and building under

construction”. The depreciation amount in 2016 is evaluated as $ 29 million. The accumulation

of the depreciation on the overhead has amounted to $ 361.5 million in 2016. Moreover, the

amounts under the “non-cash items” are depicted with $ 29 million. The availability of the

information as per the deferred tax liabilities are included with the depreciation on the plant and

equipment which is considered as $ 85.2 in 2016 (Henderson et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

Figure: “Depreciation on plant and equipment”

(Source: Sc-cdn-prod.azureedge.net. 2018)

Figure: Non-cash items included with the depreciation

(Source: Sc-cdn-prod.azureedge.net. 2018)

Figure: Depreciation based on the accumulated amount 2016

(Source: Sc-cdn-prod.azureedge.net. 2018)

c. Depreciation period

The depreciation aspect is generally considered with the several types of the depictions

which are seen to be considered with the “straight-line basis” for writing off net cost which is

incurred on the individual “property plant and equipment” apart from the land value as per the

estimated value of the assets. The “expected useful lives” as per the present and the previous

Figure: “Depreciation on plant and equipment”

(Source: Sc-cdn-prod.azureedge.net. 2018)

Figure: Non-cash items included with the depreciation

(Source: Sc-cdn-prod.azureedge.net. 2018)

Figure: Depreciation based on the accumulated amount 2016

(Source: Sc-cdn-prod.azureedge.net. 2018)

c. Depreciation period

The depreciation aspect is generally considered with the several types of the depictions

which are seen to be considered with the “straight-line basis” for writing off net cost which is

incurred on the individual “property plant and equipment” apart from the land value as per the

estimated value of the assets. The “expected useful lives” as per the present and the previous

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

years has been considered with the 20 to 40 years for “freehold buildings, lesser than 50 years or

life of lease for leasehold buildings, 3 to 20 years for plant and equipment”. It is also discerned

that the rates considered with the amortization and position are considered for reviewed every

year for more relevancy (Beatty and Liao 2014).

Figure: Depiction of depreciation period for Ansell

(Source: Sc-cdn-prod.azureedge.net. 2018)

d. Depreciation method

The depreciation method for the measurement and recognition of “property, plant and

equipment”, which has been duly included in the company by using “cost less accumulated

depreciation and impairment losses”. It is also understood that the cost related to the

expenditures are directly associated with the “acquisition of the items”. Moreover, the various

costs are further seen to be considered with the “carrying amount” of the assets which are

considered as per the “future economic benefit” related to the assets life. In this case the assets

are measured as per the measurement of the company in a reliable manner (Mullinova 2016).

Figure: Procedure Measurement and depreciation of asset for Ansell Ltd

(Source: Sc-cdn-prod.azureedge.net. 2018)

years has been considered with the 20 to 40 years for “freehold buildings, lesser than 50 years or

life of lease for leasehold buildings, 3 to 20 years for plant and equipment”. It is also discerned

that the rates considered with the amortization and position are considered for reviewed every

year for more relevancy (Beatty and Liao 2014).

Figure: Depiction of depreciation period for Ansell

(Source: Sc-cdn-prod.azureedge.net. 2018)

d. Depreciation method

The depreciation method for the measurement and recognition of “property, plant and

equipment”, which has been duly included in the company by using “cost less accumulated

depreciation and impairment losses”. It is also understood that the cost related to the

expenditures are directly associated with the “acquisition of the items”. Moreover, the various

costs are further seen to be considered with the “carrying amount” of the assets which are

considered as per the “future economic benefit” related to the assets life. In this case the assets

are measured as per the measurement of the company in a reliable manner (Mullinova 2016).

Figure: Procedure Measurement and depreciation of asset for Ansell Ltd

(Source: Sc-cdn-prod.azureedge.net. 2018)

8FINANCIAL ACCOUNTING

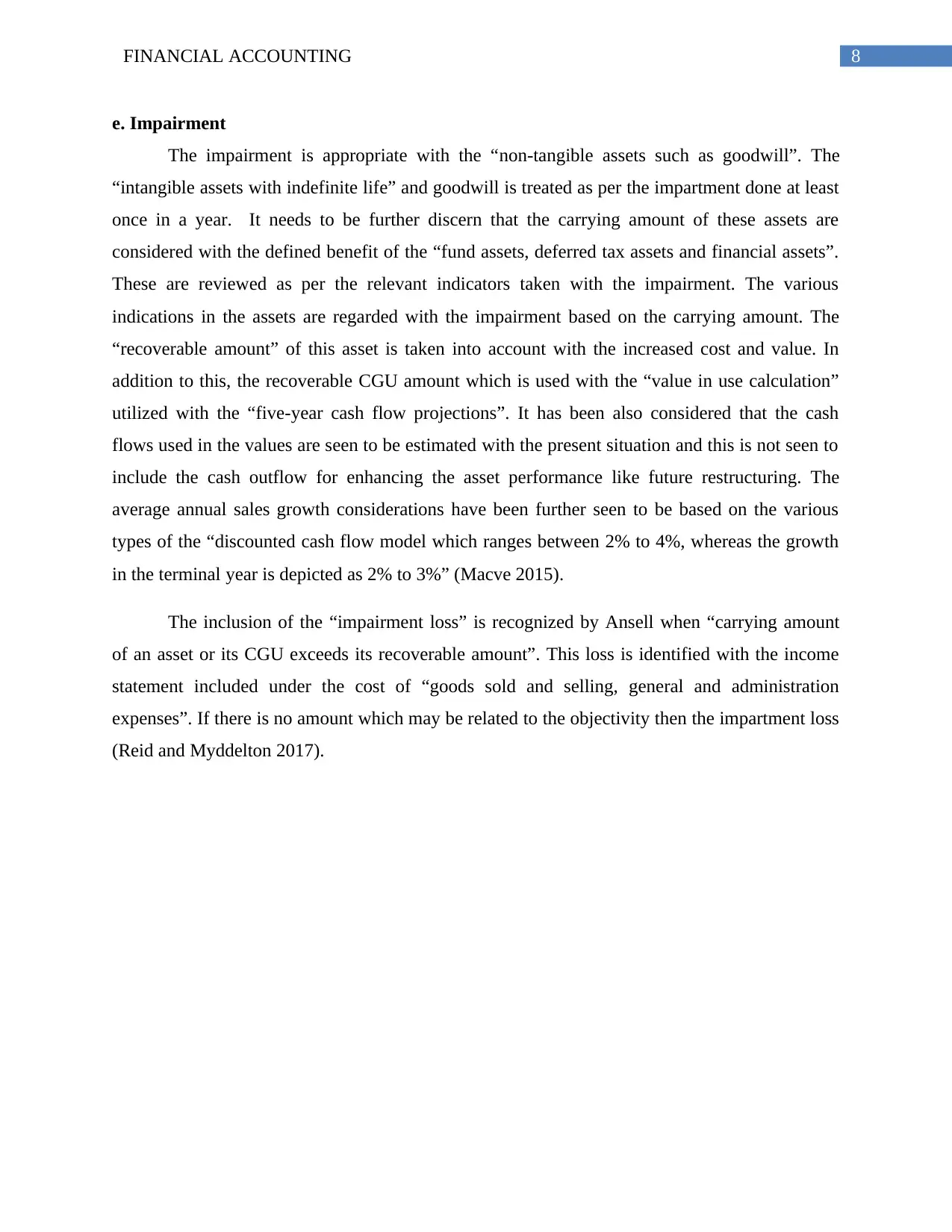

e. Impairment

The impairment is appropriate with the “non-tangible assets such as goodwill”. The

“intangible assets with indefinite life” and goodwill is treated as per the impartment done at least

once in a year. It needs to be further discern that the carrying amount of these assets are

considered with the defined benefit of the “fund assets, deferred tax assets and financial assets”.

These are reviewed as per the relevant indicators taken with the impairment. The various

indications in the assets are regarded with the impairment based on the carrying amount. The

“recoverable amount” of this asset is taken into account with the increased cost and value. In

addition to this, the recoverable CGU amount which is used with the “value in use calculation”

utilized with the “five-year cash flow projections”. It has been also considered that the cash

flows used in the values are seen to be estimated with the present situation and this is not seen to

include the cash outflow for enhancing the asset performance like future restructuring. The

average annual sales growth considerations have been further seen to be based on the various

types of the “discounted cash flow model which ranges between 2% to 4%, whereas the growth

in the terminal year is depicted as 2% to 3%” (Macve 2015).

The inclusion of the “impairment loss” is recognized by Ansell when “carrying amount

of an asset or its CGU exceeds its recoverable amount”. This loss is identified with the income

statement included under the cost of “goods sold and selling, general and administration

expenses”. If there is no amount which may be related to the objectivity then the impartment loss

(Reid and Myddelton 2017).

e. Impairment

The impairment is appropriate with the “non-tangible assets such as goodwill”. The

“intangible assets with indefinite life” and goodwill is treated as per the impartment done at least

once in a year. It needs to be further discern that the carrying amount of these assets are

considered with the defined benefit of the “fund assets, deferred tax assets and financial assets”.

These are reviewed as per the relevant indicators taken with the impairment. The various

indications in the assets are regarded with the impairment based on the carrying amount. The

“recoverable amount” of this asset is taken into account with the increased cost and value. In

addition to this, the recoverable CGU amount which is used with the “value in use calculation”

utilized with the “five-year cash flow projections”. It has been also considered that the cash

flows used in the values are seen to be estimated with the present situation and this is not seen to

include the cash outflow for enhancing the asset performance like future restructuring. The

average annual sales growth considerations have been further seen to be based on the various

types of the “discounted cash flow model which ranges between 2% to 4%, whereas the growth

in the terminal year is depicted as 2% to 3%” (Macve 2015).

The inclusion of the “impairment loss” is recognized by Ansell when “carrying amount

of an asset or its CGU exceeds its recoverable amount”. This loss is identified with the income

statement included under the cost of “goods sold and selling, general and administration

expenses”. If there is no amount which may be related to the objectivity then the impartment loss

(Reid and Myddelton 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ACCOUNTING

Figure: “Notes to impairment for Ansell Ltd”

(Source: Sc-cdn-prod.azureedge.net. 2018)

Figure: “Notes to impairment for Ansell Ltd”

(Source: Sc-cdn-prod.azureedge.net. 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ACCOUNTING

Conclusion

The determination of the consideration of financial statement of Ansell Ltd. has followed

the income statement preparation by considering the function of expenses. Therefore, the

disclosure of the expenses is seen to be based on the functions such as “distribution, cost of

goods sold, selling, general and administration expenses”. in addition to this, main reason for

expenses is considered with the simplicity of the presentation structured followed in the report.

The small organizations tend to prefer disclosure associated to the expenses based on the single

step income statement. Therefore, the disclosing of the expenses by nature which is more

relevant in terms of following the expenses as function. The main rationale for the classification

of the expenses based on the functional role of in the bigger multinationals in order to monitor

the direct units which are assigned immediately to the individual outputs, premium, rewards,

material consumption directly associated to the outputs. The three concern areas in this report

has been mentioned with the application of with “principles of consolidation”, “foreign

currency” and “recoverable amount on noncurrent asset”. The depiction of the “property, plant,

equipment” and “intangible assets” other than the individuals having “indefinite life is

depreciated/amortized” based on “straight-line basis over their useful economic lives”. The

depreciation amount in 2016 is evaluated as $ 29 million. The accumulation of the depreciation

on the overhead has amounted to $ 361.5 million in 2016. Moreover, the amounts under the

“non-cash items” are depicted with $ 29 million.

Conclusion

The determination of the consideration of financial statement of Ansell Ltd. has followed

the income statement preparation by considering the function of expenses. Therefore, the

disclosure of the expenses is seen to be based on the functions such as “distribution, cost of

goods sold, selling, general and administration expenses”. in addition to this, main reason for

expenses is considered with the simplicity of the presentation structured followed in the report.

The small organizations tend to prefer disclosure associated to the expenses based on the single

step income statement. Therefore, the disclosing of the expenses by nature which is more

relevant in terms of following the expenses as function. The main rationale for the classification

of the expenses based on the functional role of in the bigger multinationals in order to monitor

the direct units which are assigned immediately to the individual outputs, premium, rewards,

material consumption directly associated to the outputs. The three concern areas in this report

has been mentioned with the application of with “principles of consolidation”, “foreign

currency” and “recoverable amount on noncurrent asset”. The depiction of the “property, plant,

equipment” and “intangible assets” other than the individuals having “indefinite life is

depreciated/amortized” based on “straight-line basis over their useful economic lives”. The

depreciation amount in 2016 is evaluated as $ 29 million. The accumulation of the depreciation

on the overhead has amounted to $ 361.5 million in 2016. Moreover, the amounts under the

“non-cash items” are depicted with $ 29 million.

11FINANCIAL ACCOUNTING

References

Ansell.com. (2018). Mission and Values. [online] Available at:

http://www.ansell.com/en/About/Corporate/Mission-and-Values.aspx [Accessed 17 May 2018].

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Jack, L. (2015) ‘Future making in farm management accounting: The Australian “Blue Book”’,

Accounting History, 20(2), pp. 158–182. doi: 10.1177/1032373215579423.

Kallamu, B. S., Ashikin, N. and Saat, M. (2015) ‘Asian Review of Accounting’, Asian Review of

Accounting Asian Review of Accounting Asian Review of Accounting, 23(3), pp. 232–255. doi:

10.1108/ARA-11-2013-0076.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Muhammad, N. and Scrimgeour, F. (2014) ‘Stock Returns and Fundamentals in the Australian

Market’, Asian Journal of Finance & Accounting, 6(1), p. 271. doi: 10.5296/ajfa.v6i1.5486.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-64.

Needles, B. E., Powers, M. and Susan V. Crosson (2014) Principles of Accounting, Financial

Accounting. doi: 10.1037/h0092877.

Reid, W. and Myddelton, D.R., 2017. The meaning of company accounts. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Wilson, R., 2014. Sean T. McGuire. Accounting Review, 89, p.4.

References

Ansell.com. (2018). Mission and Values. [online] Available at:

http://www.ansell.com/en/About/Corporate/Mission-and-Values.aspx [Accessed 17 May 2018].

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Jack, L. (2015) ‘Future making in farm management accounting: The Australian “Blue Book”’,

Accounting History, 20(2), pp. 158–182. doi: 10.1177/1032373215579423.

Kallamu, B. S., Ashikin, N. and Saat, M. (2015) ‘Asian Review of Accounting’, Asian Review of

Accounting Asian Review of Accounting Asian Review of Accounting, 23(3), pp. 232–255. doi:

10.1108/ARA-11-2013-0076.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Muhammad, N. and Scrimgeour, F. (2014) ‘Stock Returns and Fundamentals in the Australian

Market’, Asian Journal of Finance & Accounting, 6(1), p. 271. doi: 10.5296/ajfa.v6i1.5486.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-64.

Needles, B. E., Powers, M. and Susan V. Crosson (2014) Principles of Accounting, Financial

Accounting. doi: 10.1037/h0092877.

Reid, W. and Myddelton, D.R., 2017. The meaning of company accounts. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Wilson, R., 2014. Sean T. McGuire. Accounting Review, 89, p.4.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.