ACC201 - Financial Accounting Report: Suncorp Group Analysis, Term 1

VerifiedAdded on 2022/09/14

|12

|2460

|23

Report

AI Summary

This report provides a comprehensive analysis of Suncorp Group Limited's financial performance, focusing on key financial aspects such as revenue, assets, and liabilities. The report begins by identifying Suncorp Group as a finance and banking corporation listed on the Australian Stock Exchange and provides its current share price. The analysis delves into relevant financial information, including the company's revenue generation, asset and liability management, and the application of accounting standards like AASB 13 and IAS 18. The report further examines fair presentation, discussing measurement bases like historical cost and their significance in financial reporting. It also includes a profit and loss statement analysis for Lalchand Ltd, highlighting administrative, finance, selling and distribution, income tax, and investment-related expenses. Finally, the report addresses accounting estimates, particularly how directors can manage gains and losses from hedged items using IAS 39, and how Suncorp Group applies accounting estimates in its financial statements, including the use of historical cost and estimations for insurance contracts and claims liabilities. The report uses the company's annual reports to support its findings.

Running Head: FINANCE

FINANCE

Name of the Student

Name of the University

Author Note

FINANCE

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Task 1.........................................................................................................................................2

Topic 1: Relevant Information for a company...........................................................................2

Topic 2: Fair Presentation..........................................................................................................3

Topic 3: Accounting Estimates..................................................................................................6

References..................................................................................................................................9

Table of Contents

Task 1.........................................................................................................................................2

Topic 1: Relevant Information for a company...........................................................................2

Topic 2: Fair Presentation..........................................................................................................3

Topic 3: Accounting Estimates..................................................................................................6

References..................................................................................................................................9

2FINANCE

Task 1

Suncorp Group Limited is a type of finance and banking corporation that is traded in

Australian Stock Exchange. The company has headquartered in Brisbane, Australia.

The company was founded in the year 1996. It is one of the largest insurance group of

Australia.

Web link of the company:

https://www.suncorpgroup.com.au/uploads/FY19-Annual-Report.pdf

Current share price of Suncorp limited (at end of FY 2019): $13.47

To

The lecturer,

I hereby, likely to say you that the company selected for the accounting estimates is

Suncorp Group Limited, that is traded in the Australian Stock Exchange. The company is one

of the largest insurance group of Australia and has been attracted by many of the investors.

The current stock price of the company is $13.47 at the end of June 2019.

Thankyou

Topic 1: Relevant Information for a company

A. The amount of revenue Suncorp group has generated will help to identify the

performance of the company. In addition to this, how the company has managed its

assets and liabilities will also help the investors to identify the company performance

towards its debts and equity (Suncorpgroup.com.au, 2020). The total revenue

generated at the financial year 2018 was $14,190 million and in 2019 it has increased

to $15,560 million. This means that the company has performed better in the current

year. From the company’s annual report it is found that the company has helped the

Task 1

Suncorp Group Limited is a type of finance and banking corporation that is traded in

Australian Stock Exchange. The company has headquartered in Brisbane, Australia.

The company was founded in the year 1996. It is one of the largest insurance group of

Australia.

Web link of the company:

https://www.suncorpgroup.com.au/uploads/FY19-Annual-Report.pdf

Current share price of Suncorp limited (at end of FY 2019): $13.47

To

The lecturer,

I hereby, likely to say you that the company selected for the accounting estimates is

Suncorp Group Limited, that is traded in the Australian Stock Exchange. The company is one

of the largest insurance group of Australia and has been attracted by many of the investors.

The current stock price of the company is $13.47 at the end of June 2019.

Thankyou

Topic 1: Relevant Information for a company

A. The amount of revenue Suncorp group has generated will help to identify the

performance of the company. In addition to this, how the company has managed its

assets and liabilities will also help the investors to identify the company performance

towards its debts and equity (Suncorpgroup.com.au, 2020). The total revenue

generated at the financial year 2018 was $14,190 million and in 2019 it has increased

to $15,560 million. This means that the company has performed better in the current

year. From the company’s annual report it is found that the company has helped the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

investments to grow by providing $3 billion of new credits in the small business.

They had made commercial solutions of insurance to properly manage their assets and

protects them from their traders and enterprises (Badertscher, Shanthikumar and Teoh

2019). The liabilities of the company has been raised from cash flows, repayments,

transaction costs, changes in fair values, loans & advances, derivatives, short & long-

term borrowings, tax liabilities, gross policy liabilities, outstanding claims, amount

due to reinsurers and many more (Posavac et al. 2019). The total amount of liabilities

found form the comprehensive financial position of the company was $85,360million

in the FY 2018 and then it has been decreased to $83,102million in the FY 2019. This

means that the company has also efficiency managed its liabilities. Hence, from this it

can be found that the company is properly managing its assets and liabilities.

B. According to accounting standard, AASB 13 standard of financial recognition of

investment securities, the carrying amount of these investment securities must be

written at its lowers value or fair value of cost in the financial statements (Weetman

2019). This must be properly disclosed in the company’s financial statements.

According to accounting standard of IAS 18, any kind of profits or revenue

generated from dividends must be recognised only when the shareholders income has

been established. This means that, dividend profits should be recognised only when

the dividend has been declared to the shareholders.

Topic 2: Fair Presentation

i. Measurement bases determines the monetary amounts of the financial elements that

are determined in the financial statement. It is very important to include these

measurement bases for the recognition of assets & liabilities. The financial

performance of an organisation affects every stakeholders and shareholders involved

in the business. Measurement basis helps in making financial reporting process. Any

investments to grow by providing $3 billion of new credits in the small business.

They had made commercial solutions of insurance to properly manage their assets and

protects them from their traders and enterprises (Badertscher, Shanthikumar and Teoh

2019). The liabilities of the company has been raised from cash flows, repayments,

transaction costs, changes in fair values, loans & advances, derivatives, short & long-

term borrowings, tax liabilities, gross policy liabilities, outstanding claims, amount

due to reinsurers and many more (Posavac et al. 2019). The total amount of liabilities

found form the comprehensive financial position of the company was $85,360million

in the FY 2018 and then it has been decreased to $83,102million in the FY 2019. This

means that the company has also efficiency managed its liabilities. Hence, from this it

can be found that the company is properly managing its assets and liabilities.

B. According to accounting standard, AASB 13 standard of financial recognition of

investment securities, the carrying amount of these investment securities must be

written at its lowers value or fair value of cost in the financial statements (Weetman

2019). This must be properly disclosed in the company’s financial statements.

According to accounting standard of IAS 18, any kind of profits or revenue

generated from dividends must be recognised only when the shareholders income has

been established. This means that, dividend profits should be recognised only when

the dividend has been declared to the shareholders.

Topic 2: Fair Presentation

i. Measurement bases determines the monetary amounts of the financial elements that

are determined in the financial statement. It is very important to include these

measurement bases for the recognition of assets & liabilities. The financial

performance of an organisation affects every stakeholders and shareholders involved

in the business. Measurement basis helps in making financial reporting process. Any

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

change in the measurement bases can affect the shareholders and stakeholders. Some

of the measurement bases are historical cost bases, fair value, current cost and net

realizable value (Blanco and Racaza 2018). The measurement bases finds the

reliability and the exact definition of the assets & liabilities. The market value

measurement bases determines the actual price of the assets in the competitive

market. Measurement bases is very important to accomplish the objective of financial

reporting process. The information of measurement bases helps in determining the

accuracy of financial reporting system. The most common bases of measurement is

the historical cost. In historical cost method, the assets are recorded at its fair value

and the amount of cash & cash equivalent paid during the time of acquisition.

Liabilities are recorded at the amount that has been received at the exchange for any

obligations. In case of realizable value measurement bases, the assets are recognised

as the actual amount of cash & cash equivalents that is currently obtained by the

selling of the asset. Liabilities amount are determined by their settlement values

(Burca, Nicolaescu and Draguţ 2019). Hence, the measurement bases is adopted by

most of the business entities to prepare their financial statements. The most common

method is the historical cost method.

Measurement bases helps to determine the economic phenomena of the business in

numbers. Different measurement bases have different implications & information’s related to

the assets & liabilities that is reflected in the comprehensive income statement of the

company. Hence, it is the most fundamental technique to determine that is related to

measurement concept and helps in fairly determine the value of assets and liabilities (Peach

and West 2017). Hence, it is very important to include these measurement bases while

performing the financial reporting process.

(ii) Profit & loss statement of Lalchand Ltd (For the year ended June 30 2016)

change in the measurement bases can affect the shareholders and stakeholders. Some

of the measurement bases are historical cost bases, fair value, current cost and net

realizable value (Blanco and Racaza 2018). The measurement bases finds the

reliability and the exact definition of the assets & liabilities. The market value

measurement bases determines the actual price of the assets in the competitive

market. Measurement bases is very important to accomplish the objective of financial

reporting process. The information of measurement bases helps in determining the

accuracy of financial reporting system. The most common bases of measurement is

the historical cost. In historical cost method, the assets are recorded at its fair value

and the amount of cash & cash equivalent paid during the time of acquisition.

Liabilities are recorded at the amount that has been received at the exchange for any

obligations. In case of realizable value measurement bases, the assets are recognised

as the actual amount of cash & cash equivalents that is currently obtained by the

selling of the asset. Liabilities amount are determined by their settlement values

(Burca, Nicolaescu and Draguţ 2019). Hence, the measurement bases is adopted by

most of the business entities to prepare their financial statements. The most common

method is the historical cost method.

Measurement bases helps to determine the economic phenomena of the business in

numbers. Different measurement bases have different implications & information’s related to

the assets & liabilities that is reflected in the comprehensive income statement of the

company. Hence, it is the most fundamental technique to determine that is related to

measurement concept and helps in fairly determine the value of assets and liabilities (Peach

and West 2017). Hence, it is very important to include these measurement bases while

performing the financial reporting process.

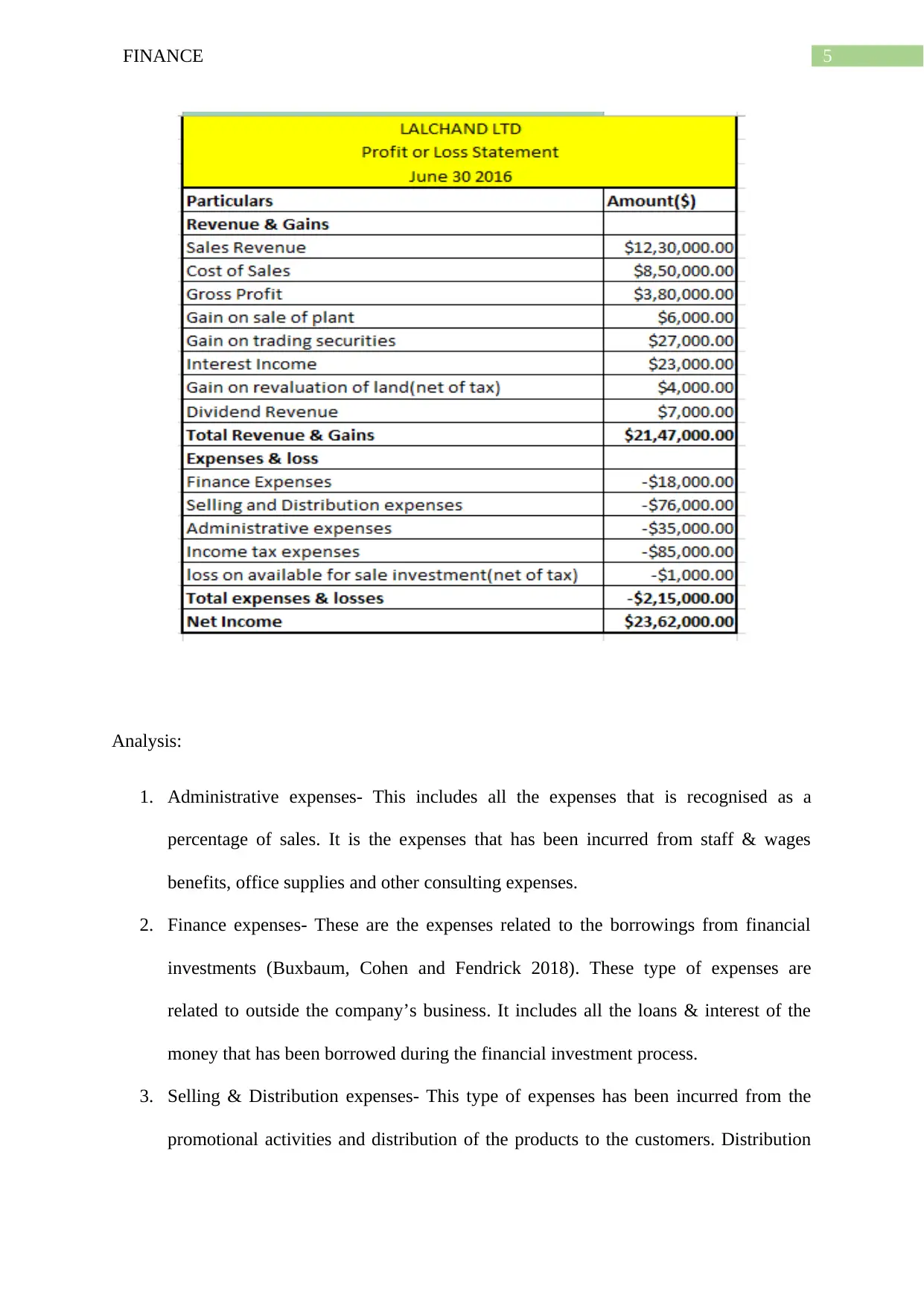

(ii) Profit & loss statement of Lalchand Ltd (For the year ended June 30 2016)

5FINANCE

Analysis:

1. Administrative expenses- This includes all the expenses that is recognised as a

percentage of sales. It is the expenses that has been incurred from staff & wages

benefits, office supplies and other consulting expenses.

2. Finance expenses- These are the expenses related to the borrowings from financial

investments (Buxbaum, Cohen and Fendrick 2018). These type of expenses are

related to outside the company’s business. It includes all the loans & interest of the

money that has been borrowed during the financial investment process.

3. Selling & Distribution expenses- This type of expenses has been incurred from the

promotional activities and distribution of the products to the customers. Distribution

Analysis:

1. Administrative expenses- This includes all the expenses that is recognised as a

percentage of sales. It is the expenses that has been incurred from staff & wages

benefits, office supplies and other consulting expenses.

2. Finance expenses- These are the expenses related to the borrowings from financial

investments (Buxbaum, Cohen and Fendrick 2018). These type of expenses are

related to outside the company’s business. It includes all the loans & interest of the

money that has been borrowed during the financial investment process.

3. Selling & Distribution expenses- This type of expenses has been incurred from the

promotional activities and distribution of the products to the customers. Distribution

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

expenses have been incurred from the warehousing expenses, expenses related to the

packaging of the product and delivering the products to the target customers.

4. Income tax expenses- Income tax expense have been identified by the government

related to the business profit. This is known as the tax that has to be paid to the

government.

5. Loss on available for sale investment- This is the loss of the business that has been

ideally kept and cannot be used for trading purpose because the maturity period is

completed.

The above expenses have been incurred by Lalchand Ltd during the financial year

2016. The total net income generated by the company is $2,362,000 in the FY 2016.

Topic 3: Accounting Estimates

A. The directors can use the accounting standard IAS 39 for writing down the gains and

losses of hedged items. All the derivative instruments that has been used as hedged

instrument must be measured at the fair value. All the capital losses & gains must be

recognised at its fair value. It should reflect the credit quality of the derivative

instrument (Stuber et al. 2018). The hedged items that is traded in the open market

must be written at its market price value of the instrument. The recognition of these

financial instrument must be done on the basis of its risks. Such risks includes; the

interest rate risk, equity price risk, currency risks & commodity risk. There are

different type of risks involved in different derivative instruments. Then the directors

can record the capital gains & loss of the derivative instrument in the income

statement. This must be recognised during the time of sale of the derivative

instrument. In case of any unrealised gains or losses of the derivative instrument must

also be recognised in the income statement. This unrealised amount must be

determined at the value of exchange rate of the hedged items during the financial

expenses have been incurred from the warehousing expenses, expenses related to the

packaging of the product and delivering the products to the target customers.

4. Income tax expenses- Income tax expense have been identified by the government

related to the business profit. This is known as the tax that has to be paid to the

government.

5. Loss on available for sale investment- This is the loss of the business that has been

ideally kept and cannot be used for trading purpose because the maturity period is

completed.

The above expenses have been incurred by Lalchand Ltd during the financial year

2016. The total net income generated by the company is $2,362,000 in the FY 2016.

Topic 3: Accounting Estimates

A. The directors can use the accounting standard IAS 39 for writing down the gains and

losses of hedged items. All the derivative instruments that has been used as hedged

instrument must be measured at the fair value. All the capital losses & gains must be

recognised at its fair value. It should reflect the credit quality of the derivative

instrument (Stuber et al. 2018). The hedged items that is traded in the open market

must be written at its market price value of the instrument. The recognition of these

financial instrument must be done on the basis of its risks. Such risks includes; the

interest rate risk, equity price risk, currency risks & commodity risk. There are

different type of risks involved in different derivative instruments. Then the directors

can record the capital gains & loss of the derivative instrument in the income

statement. This must be recognised during the time of sale of the derivative

instrument. In case of any unrealised gains or losses of the derivative instrument must

also be recognised in the income statement. This unrealised amount must be

determined at the value of exchange rate of the hedged items during the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

period. In case of any hedging transactions done for tax purposes, the hedged item

must be treated as the investments done for future contracts or investments done for

foreign currency contract. This is not determined as the hedged event even if it has

been sold for the tax purpose (Sun 2019). Hence, in this case, the gains and losses

from the hedged items is not recognised. But, the directors should have the

responsibility to clearly identify the transaction of the hedged item on daily basis.

This will help them in easy determination of the taxation related to the income

generated from the hedged item transactions. In every gain or losses of the underlying

contract, the director must determine its capital gain or loss according to the hedging

rules.

Therefore, the directors are advised to determine the fair value of the capital gains or

losses raised from the hedged items. It is best to recognise the amount of losses and gains in

the company’s income statement (Stubb and Higgins 2018). The account policies of

International Accounting Standard 39 needs to be followed for dealing with the classification

of hedged items. This must be done by reporting the risks involved with the hedge items.

B. Accounting Estimates

The accounting estimate of Suncorp Group Limited has done by simply determining

the carrying amount of the assets & liabilities in the financial statement. Some of the

accounting estimates found in the company’s annual report are:

The financial statement has been prepared on the basis of historical cost method (page

88). This means that accounting estimation is done by comparing the historical data

and determining the value at the current financial year.

The liabilities related to general insurance contract has been determined at its carrying

value (Page 110). These liabilities includes the liabilities that has been adopted for

period. In case of any hedging transactions done for tax purposes, the hedged item

must be treated as the investments done for future contracts or investments done for

foreign currency contract. This is not determined as the hedged event even if it has

been sold for the tax purpose (Sun 2019). Hence, in this case, the gains and losses

from the hedged items is not recognised. But, the directors should have the

responsibility to clearly identify the transaction of the hedged item on daily basis.

This will help them in easy determination of the taxation related to the income

generated from the hedged item transactions. In every gain or losses of the underlying

contract, the director must determine its capital gain or loss according to the hedging

rules.

Therefore, the directors are advised to determine the fair value of the capital gains or

losses raised from the hedged items. It is best to recognise the amount of losses and gains in

the company’s income statement (Stubb and Higgins 2018). The account policies of

International Accounting Standard 39 needs to be followed for dealing with the classification

of hedged items. This must be done by reporting the risks involved with the hedge items.

B. Accounting Estimates

The accounting estimate of Suncorp Group Limited has done by simply determining

the carrying amount of the assets & liabilities in the financial statement. Some of the

accounting estimates found in the company’s annual report are:

The financial statement has been prepared on the basis of historical cost method (page

88). This means that accounting estimation is done by comparing the historical data

and determining the value at the current financial year.

The liabilities related to general insurance contract has been determined at its carrying

value (Page 110). These liabilities includes the liabilities that has been adopted for

8FINANCE

LAT (Liability adequacy test). The net premium liabilities are determined at the

carrying value of outstanding claim liabilities.

The carrying value for the financial liabilities like non-interest bearing, variable rate

deposits & fixed rate deposits are determined in the short-term borrowings and

deposits. This carrying value has been written from the estimation of fair value (page

124).

The statutory tax rates for various classes of the business has simply written on the

basis of historical cost (Suncorpgroup.com.au, 2020). The cost of tax rates related to

annuity & pension rates are simply written on the bases of previous year rates (page

30).

The determination of insurance contracts are written on the basis of its estimation

from analysis of the company trends with related to the industrial data. These type of

claims liabilities are simply determined on the basis of accounting estimates (page

112).

There is an accounting estimation done on future payments of the business for the

claims that has been reported on the reporting date from many years ago (Bogdan

2016). These estimation may not be accurate during the next accounting periods (page

165).

Suncorp group has focused on historical experiences for determining the current

estimation of these claims. This estimation may change with respect to time. The

current estimation is determine by finding the variability of the current and historical

estimations. On the basis of variations, the current estimation is done. During this

process the company does many assumptions like future wages, average size of the

claim, associated risk margin and the possible inflations. Some of the examples is

LAT (Liability adequacy test). The net premium liabilities are determined at the

carrying value of outstanding claim liabilities.

The carrying value for the financial liabilities like non-interest bearing, variable rate

deposits & fixed rate deposits are determined in the short-term borrowings and

deposits. This carrying value has been written from the estimation of fair value (page

124).

The statutory tax rates for various classes of the business has simply written on the

basis of historical cost (Suncorpgroup.com.au, 2020). The cost of tax rates related to

annuity & pension rates are simply written on the bases of previous year rates (page

30).

The determination of insurance contracts are written on the basis of its estimation

from analysis of the company trends with related to the industrial data. These type of

claims liabilities are simply determined on the basis of accounting estimates (page

112).

There is an accounting estimation done on future payments of the business for the

claims that has been reported on the reporting date from many years ago (Bogdan

2016). These estimation may not be accurate during the next accounting periods (page

165).

Suncorp group has focused on historical experiences for determining the current

estimation of these claims. This estimation may change with respect to time. The

current estimation is determine by finding the variability of the current and historical

estimations. On the basis of variations, the current estimation is done. During this

process the company does many assumptions like future wages, average size of the

claim, associated risk margin and the possible inflations. Some of the examples is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

related to workers compensation, future uncertainty like earthquakes and many

more( (page 165)

related to workers compensation, future uncertainty like earthquakes and many

more( (page 165)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

References

Badertscher, B.A., Shanthikumar, D.M. and Teoh, S.H., 2019. Private firm investment and

public peer misvaluation. The Accounting Review, 94(6), pp.31-60.

Blanco, M.N. and Racaza, C.R., 2018. FAIR VALUE ACCOUNTING: ITS

DEVELOPMENT AND ITS IMPORTANCE TO FINANCIAL STATEMENTS USERS.

Bogdan, V., 2016. FROM SCHRÖDINGER'S CAT TOWARDS A QUANTUM

APPROACH OF ACCOUNTING ESTIMATES, JUDGMENTS AND DECISION

MAKING. Annals of the University of Oradea, Economic Science Series, 25(2).

Burcă, V., Nicolăescu, C. and Drăguţ, D., 2019. Critical Analysis on the Amendments

Discussed, Concerning Changes in Accounting Estimates. Studies in Business and

Economics, 14(1), pp.17-33.

Buxbaum, J.D., Cohen, A.J. and Fendrick, A.M., 2018. Measures of the Burden of Medical

Expenses. Jama, 319(15), pp.1621-1621.

Peach, K. and West, C.S., 2017. Invitation to comment on ED 277 Disclosure Requirements

for Tier 2 Entities.

Posavac, S.S., Ratchford, M., Bollen, N.P. and Sanbonmatsu, D.M., 2019. Premature

infatuation and commitment in individual investing decisions. Journal of Economic

Psychology, 72, pp.245-259.

Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory reform

in integrated reporting. Journal of Business Ethics, 147(3), pp.489-508.

Stuber, S., Hogan, C., Dennis, J.S., Stanley, J. and Wilkins, M., 2018. Do PCAOB

Inspections Improve the Accuracy of Accounting Estimates?. Working paper, Michigan State

University.

References

Badertscher, B.A., Shanthikumar, D.M. and Teoh, S.H., 2019. Private firm investment and

public peer misvaluation. The Accounting Review, 94(6), pp.31-60.

Blanco, M.N. and Racaza, C.R., 2018. FAIR VALUE ACCOUNTING: ITS

DEVELOPMENT AND ITS IMPORTANCE TO FINANCIAL STATEMENTS USERS.

Bogdan, V., 2016. FROM SCHRÖDINGER'S CAT TOWARDS A QUANTUM

APPROACH OF ACCOUNTING ESTIMATES, JUDGMENTS AND DECISION

MAKING. Annals of the University of Oradea, Economic Science Series, 25(2).

Burcă, V., Nicolăescu, C. and Drăguţ, D., 2019. Critical Analysis on the Amendments

Discussed, Concerning Changes in Accounting Estimates. Studies in Business and

Economics, 14(1), pp.17-33.

Buxbaum, J.D., Cohen, A.J. and Fendrick, A.M., 2018. Measures of the Burden of Medical

Expenses. Jama, 319(15), pp.1621-1621.

Peach, K. and West, C.S., 2017. Invitation to comment on ED 277 Disclosure Requirements

for Tier 2 Entities.

Posavac, S.S., Ratchford, M., Bollen, N.P. and Sanbonmatsu, D.M., 2019. Premature

infatuation and commitment in individual investing decisions. Journal of Economic

Psychology, 72, pp.245-259.

Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory reform

in integrated reporting. Journal of Business Ethics, 147(3), pp.489-508.

Stuber, S., Hogan, C., Dennis, J.S., Stanley, J. and Wilkins, M., 2018. Do PCAOB

Inspections Improve the Accuracy of Accounting Estimates?. Working paper, Michigan State

University.

11FINANCE

Sun, T., 2019. Machine Learning Improves Accounting Estimates.

Suncorpgroup.com.au, 2020. [online] Suncorpgroup.com.au. Available at:

<https://www.suncorpgroup.com.au/uploads/FY19-Annual-Report.pdf> [Accessed 11 April

2020].

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Sun, T., 2019. Machine Learning Improves Accounting Estimates.

Suncorpgroup.com.au, 2020. [online] Suncorpgroup.com.au. Available at:

<https://www.suncorpgroup.com.au/uploads/FY19-Annual-Report.pdf> [Accessed 11 April

2020].

Weetman, P., 2019. Financial and management accounting. Pearson UK.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.