ACC202 Group Report: Fair Value Reporting Practices - ASX Analysis

VerifiedAdded on 2023/06/03

|14

|2619

|307

Report

AI Summary

This report provides an analysis of fair value accounting and reporting, focusing on its importance and implications in the contemporary world. It examines the fair value concept, which involves valuing assets and liabilities based on their market value. The report selects two ASX Limited companies, Telstra Corporation and TPG Telecom, and analyzes their valuation methods according to the fair value approach. It discusses the challenges companies face in adopting fair value accounting, including the lack of active markets for all assets, potential instability in financial statements, and the complexity of valuation. The report also highlights the different approaches to fair value measurement and the judgment involved in determining fair market value, particularly for intangible assets. Finally, it compares the fair value accounting measures adopted by Telstra and TPG Telecom, noting TPG's more comprehensive disclosures and diverse valuation methods.

Corporate

Accounting

Assignment

Accounting

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 20th Sep 2018.

1 | Page

By student name

Professor

University

Date: 20th Sep 2018.

1 | Page

2

Executive Summary

In the following assignment the importance and implication of fair value accounting and

reporting is stated. Fair value as a concept is very complex and refers to the method based on

which assets and liabilities that are stated on the annual reports of the company are based on the

overall market value that they have. Two ASX Limited Company have been selected and their

methods for valuation of the assets as per the fair value approach has been analysed and

discussed in detail.

2 | Page

Executive Summary

In the following assignment the importance and implication of fair value accounting and

reporting is stated. Fair value as a concept is very complex and refers to the method based on

which assets and liabilities that are stated on the annual reports of the company are based on the

overall market value that they have. Two ASX Limited Company have been selected and their

methods for valuation of the assets as per the fair value approach has been analysed and

discussed in detail.

2 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Table of Contents

PART A.........................................................................................................................................................4

Introduction.................................................................................................................................................4

Analysis........................................................................................................................................................5

Conclusion...................................................................................................................................................7

Part 2...........................................................................................................................................................7

References...................................................................................................................................................9

3 | Page

Table of Contents

PART A.........................................................................................................................................................4

Introduction.................................................................................................................................................4

Analysis........................................................................................................................................................5

Conclusion...................................................................................................................................................7

Part 2...........................................................................................................................................................7

References...................................................................................................................................................9

3 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

PART A

Importance of fair value accounting in contemporary world

Introduction

Fair value is the tool that uses the market prices for the valuation of the assets and

liabilities of the company for the preparation of the financial statements. It is the estimated price

at which an asset is sold or a liability is paid off with any third party under the prevalent market

conditions. The main idea behind fair value accounting is to consider the prices that the

companies are ready to pay under active market. Active market means the one in which there is a

lot of transactions that are very high and that includes lot of sufficient information about the

prancing. Also, it is important that from the market the fair value is taken from should be the

principle market for the assets and liabilities of the company (Andiola, et al., 2018). Greater

volume of transactions leads to better pricing and companies should always look out for that.

Now many companies are trying to adopt this practice of fair value marketing for the preparation

of the financial statements under contemporary world of accounting. This means that the assets

and liabilities would be reflected in the financial statement at their fair values. It is also important

to consider that fair values should be taken as a basis on which the performances of the company

are being evaluated. In this assignment we will discuss what are the overall implication of taking

fair value accounting in the contemporary world and how the companies around the world are

affected by this (Appelbaum, et al., 2018).

4 | Page

PART A

Importance of fair value accounting in contemporary world

Introduction

Fair value is the tool that uses the market prices for the valuation of the assets and

liabilities of the company for the preparation of the financial statements. It is the estimated price

at which an asset is sold or a liability is paid off with any third party under the prevalent market

conditions. The main idea behind fair value accounting is to consider the prices that the

companies are ready to pay under active market. Active market means the one in which there is a

lot of transactions that are very high and that includes lot of sufficient information about the

prancing. Also, it is important that from the market the fair value is taken from should be the

principle market for the assets and liabilities of the company (Andiola, et al., 2018). Greater

volume of transactions leads to better pricing and companies should always look out for that.

Now many companies are trying to adopt this practice of fair value marketing for the preparation

of the financial statements under contemporary world of accounting. This means that the assets

and liabilities would be reflected in the financial statement at their fair values. It is also important

to consider that fair values should be taken as a basis on which the performances of the company

are being evaluated. In this assignment we will discuss what are the overall implication of taking

fair value accounting in the contemporary world and how the companies around the world are

affected by this (Appelbaum, et al., 2018).

4 | Page

5

Analysis

In the given assignment, Laux and Lez have stated that fair value accounting and the debate that

is related to that will not die soon. There are many factors that the companies need to consider

when they are selecting any specific method for the measurement of their items, to make sure

that the measurement is to the best of the ability of the company and incurs the best result under

any given situations (Axelsen, et al., 2017).

Fair value reporting has been considered in many companies as a basis for the measurement of

the value of the financial assets of the company, and the financial instruments that they deal in

the market, but for traditional items of the balance sheet this method is still not consider that

applicable as the management feels that it might under value or over value the asset in some

cases. So, we see that there is a negative approach on part of the management, also one more

reason why companies don’t consider this is a good option is because they are not having active

market for all the items so at any given point it becomes difficult to ascertain what the fair value

would be. Also, there are lot of fluctuation happening and that gives an unstable approach to the

financial statements if they are prepared based on the fair value accounting (Bailey, et al., 2017).

The aim should be that companies should present the correct value of their assets and liabilities

and that is possible only when there is stability in the overall approach of the management and

that is not possible in this context.

Also, we see that companies both private and public are very sceptical when it comes to applying

these principles given the overall level of complexity involved in the valuation of the same.

Thus, they do not prefer that they use it for their overall general reporting framework, though the

authorities are trying to incorporate the same in their corporate reporting framework. There are

many challenges that the companies must face in general thus they do not prefer to apply such

5 | Page

Analysis

In the given assignment, Laux and Lez have stated that fair value accounting and the debate that

is related to that will not die soon. There are many factors that the companies need to consider

when they are selecting any specific method for the measurement of their items, to make sure

that the measurement is to the best of the ability of the company and incurs the best result under

any given situations (Axelsen, et al., 2017).

Fair value reporting has been considered in many companies as a basis for the measurement of

the value of the financial assets of the company, and the financial instruments that they deal in

the market, but for traditional items of the balance sheet this method is still not consider that

applicable as the management feels that it might under value or over value the asset in some

cases. So, we see that there is a negative approach on part of the management, also one more

reason why companies don’t consider this is a good option is because they are not having active

market for all the items so at any given point it becomes difficult to ascertain what the fair value

would be. Also, there are lot of fluctuation happening and that gives an unstable approach to the

financial statements if they are prepared based on the fair value accounting (Bailey, et al., 2017).

The aim should be that companies should present the correct value of their assets and liabilities

and that is possible only when there is stability in the overall approach of the management and

that is not possible in this context.

Also, we see that companies both private and public are very sceptical when it comes to applying

these principles given the overall level of complexity involved in the valuation of the same.

Thus, they do not prefer that they use it for their overall general reporting framework, though the

authorities are trying to incorporate the same in their corporate reporting framework. There are

many challenges that the companies must face in general thus they do not prefer to apply such

5 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

kind of measurement method that would require added cost and efforts as they must take help

from valuation experts for the determination of the fair market value (Bumgarner & Vasarhelyi,

2018). Also, there are various approach for its measurement like the market value approach,

income approach and cost approach. So different companies can opt for different methods and

measuring very item of the balance sheet on different approaches is not feasible as it will render

a redundancy to the information that the management is providing in their annual reports. It will

be difficult for the stakeholders also to ascertain which measure has been adopted and whether it

is feasible or not (Garon, 2018). Thus, it means that on various grounds the management will

struggle in case they adopt this basis of measurement for the company. They should also see that

the authorities are trying that they can incorporate this principle of corporate reporting in the

long run, but in that way, we can see that there are areas in which it won’t be feasible like

measurement of the inventory, or the property plant and equipment, because they need to

consider the concept of depreciation also. So, we see that it is a very complex method altogether

(Fukukawa & Mock, 2011).

Also the concept of fair value accounting is having relevant effect on the subprime and other

crises of the world because people are considering which methods to employ for the

measurement of the assets, as at any given day the market price would be the amount that which

the companies would sale of their products and that should be its value technically but when it

comes to preparation of the financial statement this is a wrong method and can make the process

very complex, thus the need of the hour is that the issues that are related to contemporary

accounting should be taken care of in such a way that correct value is presented in that

(Heminway, 2017). Fair value measurement is adopted as a technique for the measurement of

assets of the company like financial instruments because they are traded in market and there is

6 | Page

kind of measurement method that would require added cost and efforts as they must take help

from valuation experts for the determination of the fair market value (Bumgarner & Vasarhelyi,

2018). Also, there are various approach for its measurement like the market value approach,

income approach and cost approach. So different companies can opt for different methods and

measuring very item of the balance sheet on different approaches is not feasible as it will render

a redundancy to the information that the management is providing in their annual reports. It will

be difficult for the stakeholders also to ascertain which measure has been adopted and whether it

is feasible or not (Garon, 2018). Thus, it means that on various grounds the management will

struggle in case they adopt this basis of measurement for the company. They should also see that

the authorities are trying that they can incorporate this principle of corporate reporting in the

long run, but in that way, we can see that there are areas in which it won’t be feasible like

measurement of the inventory, or the property plant and equipment, because they need to

consider the concept of depreciation also. So, we see that it is a very complex method altogether

(Fukukawa & Mock, 2011).

Also the concept of fair value accounting is having relevant effect on the subprime and other

crises of the world because people are considering which methods to employ for the

measurement of the assets, as at any given day the market price would be the amount that which

the companies would sale of their products and that should be its value technically but when it

comes to preparation of the financial statement this is a wrong method and can make the process

very complex, thus the need of the hour is that the issues that are related to contemporary

accounting should be taken care of in such a way that correct value is presented in that

(Heminway, 2017). Fair value measurement is adopted as a technique for the measurement of

assets of the company like financial instruments because they are traded in market and there is

6 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

active market present for them, which is not available for many other items of the balance sheet.

Hence it makes the entire process complex.

Conclusion

Based on the overall analysis it can be said that companies should try to see whether they can

employ these measurement policy of fair value reporting and with time there would be many

changes that would make it feasible enough to apply these principles but the authorities need to

do a lot of research for that because accounting as a concept should remain static if not anything

else and investors should get the correct information of what they are indulging and investing in

and in what ways would this be feasible for them in the long run.

Part 2

In the given case two companies have been selected that are listed on the Australian

Stock Exchange. The two companies are Telstra Corporation and TPG Telecom. Both are

companies belongs to the telecommunication sector and are one of the leading companies in

Industry (Mock, et al., 2018).

Telstra Corporation deals in consumer electronic goods like mobile phones, software etc. It also

helps in providing services to the business for installation and management of their

telecommunication lines. It works under two levels, business to consumer and business to

business. The overall operations of the company are limited to Australia and the company is also

considering moving to other countries also.

TPG Telecom is an Australian Company that provides consumer mobile services and business

internet services. It is more of consumer oriented company and there is not much business to

7 | Page

active market present for them, which is not available for many other items of the balance sheet.

Hence it makes the entire process complex.

Conclusion

Based on the overall analysis it can be said that companies should try to see whether they can

employ these measurement policy of fair value reporting and with time there would be many

changes that would make it feasible enough to apply these principles but the authorities need to

do a lot of research for that because accounting as a concept should remain static if not anything

else and investors should get the correct information of what they are indulging and investing in

and in what ways would this be feasible for them in the long run.

Part 2

In the given case two companies have been selected that are listed on the Australian

Stock Exchange. The two companies are Telstra Corporation and TPG Telecom. Both are

companies belongs to the telecommunication sector and are one of the leading companies in

Industry (Mock, et al., 2018).

Telstra Corporation deals in consumer electronic goods like mobile phones, software etc. It also

helps in providing services to the business for installation and management of their

telecommunication lines. It works under two levels, business to consumer and business to

business. The overall operations of the company are limited to Australia and the company is also

considering moving to other countries also.

TPG Telecom is an Australian Company that provides consumer mobile services and business

internet services. It is more of consumer oriented company and there is not much business to

7 | Page

8

business transactions. Most of the services that they provide are very reliable and easy to use for

the consumer.

In the given part, the fair value accounting measures that these specific companies adopted is

cited and presented and explained below.

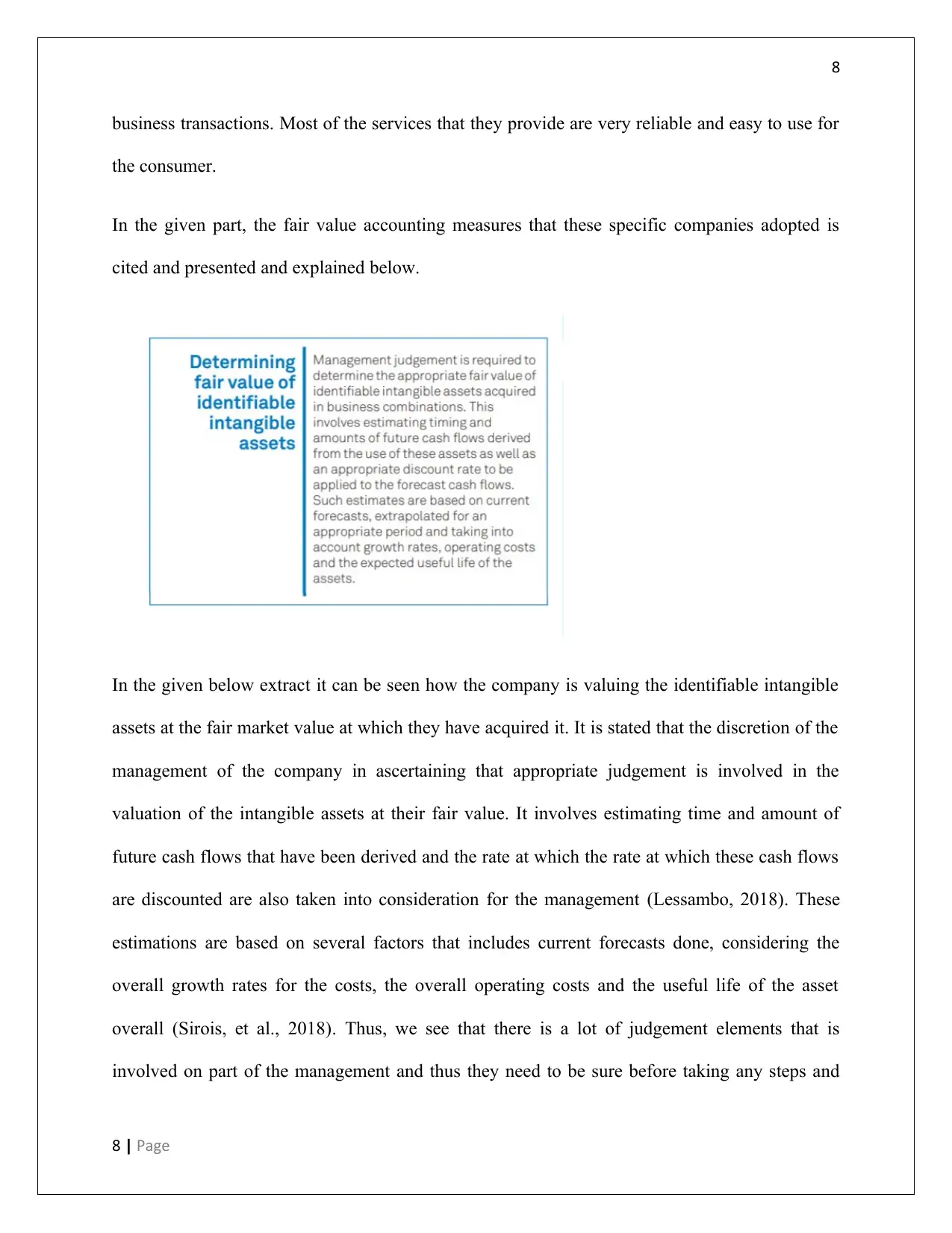

In the given below extract it can be seen how the company is valuing the identifiable intangible

assets at the fair market value at which they have acquired it. It is stated that the discretion of the

management of the company in ascertaining that appropriate judgement is involved in the

valuation of the intangible assets at their fair value. It involves estimating time and amount of

future cash flows that have been derived and the rate at which the rate at which these cash flows

are discounted are also taken into consideration for the management (Lessambo, 2018). These

estimations are based on several factors that includes current forecasts done, considering the

overall growth rates for the costs, the overall operating costs and the useful life of the asset

overall (Sirois, et al., 2018). Thus, we see that there is a lot of judgement elements that is

involved on part of the management and thus they need to be sure before taking any steps and

8 | Page

business transactions. Most of the services that they provide are very reliable and easy to use for

the consumer.

In the given part, the fair value accounting measures that these specific companies adopted is

cited and presented and explained below.

In the given below extract it can be seen how the company is valuing the identifiable intangible

assets at the fair market value at which they have acquired it. It is stated that the discretion of the

management of the company in ascertaining that appropriate judgement is involved in the

valuation of the intangible assets at their fair value. It involves estimating time and amount of

future cash flows that have been derived and the rate at which the rate at which these cash flows

are discounted are also taken into consideration for the management (Lessambo, 2018). These

estimations are based on several factors that includes current forecasts done, considering the

overall growth rates for the costs, the overall operating costs and the useful life of the asset

overall (Sirois, et al., 2018). Thus, we see that there is a lot of judgement elements that is

involved on part of the management and thus they need to be sure before taking any steps and

8 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

often requires help of valuation specialists. But this can be applied only in case of intangible

assets, in case of property plant and equipment the same is not considered (Segal, 2017). The

auditor has stated the same in their audit report under key audit matters and considered it as a

matter of importance and where there can be certain risk elements involved that can affect the

position of the company and of the investors.

TPG Telecom

9 | Page

often requires help of valuation specialists. But this can be applied only in case of intangible

assets, in case of property plant and equipment the same is not considered (Segal, 2017). The

auditor has stated the same in their audit report under key audit matters and considered it as a

matter of importance and where there can be certain risk elements involved that can affect the

position of the company and of the investors.

TPG Telecom

9 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

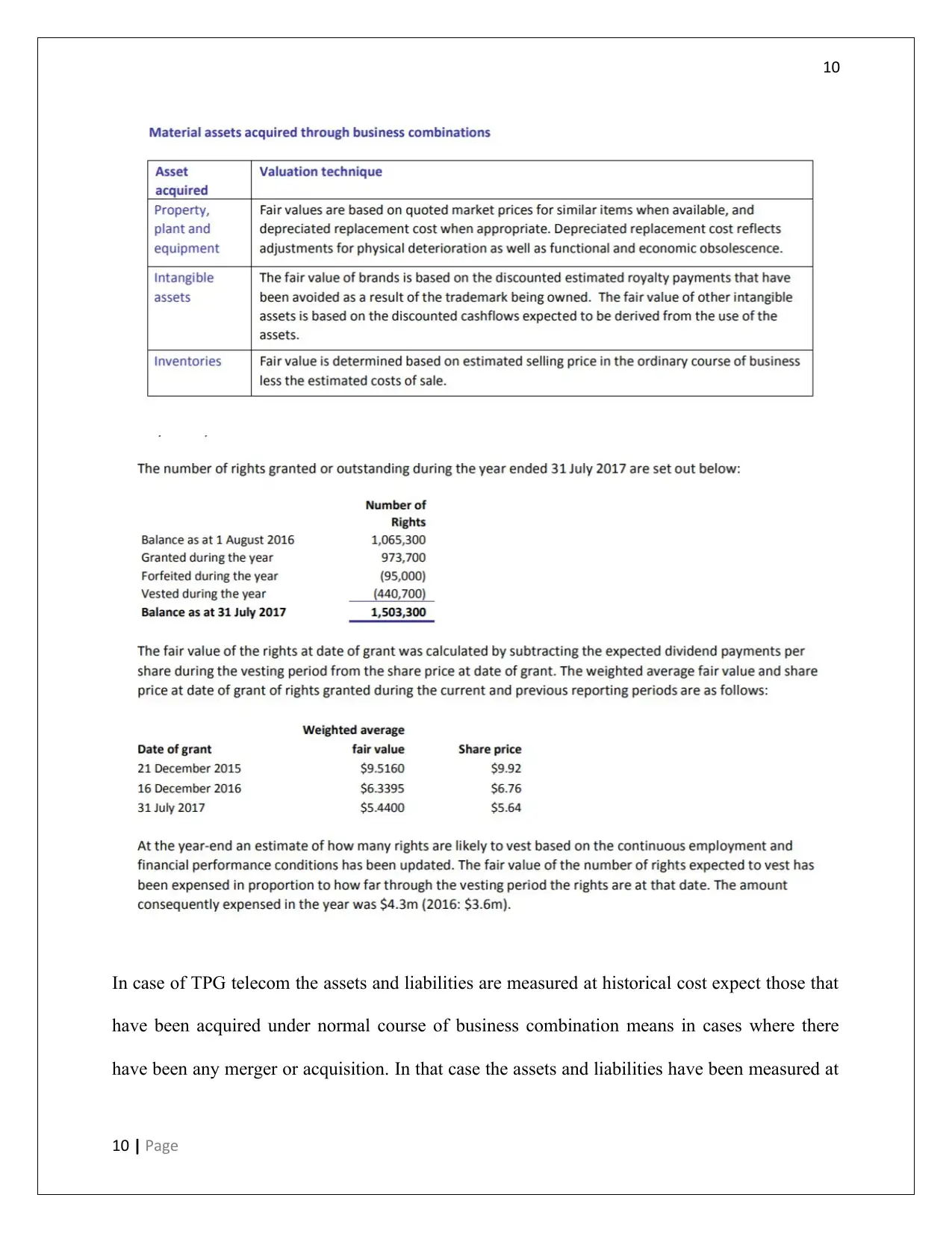

In case of TPG telecom the assets and liabilities are measured at historical cost expect those that

have been acquired under normal course of business combination means in cases where there

have been any merger or acquisition. In that case the assets and liabilities have been measured at

10 | Page

In case of TPG telecom the assets and liabilities are measured at historical cost expect those that

have been acquired under normal course of business combination means in cases where there

have been any merger or acquisition. In that case the assets and liabilities have been measured at

10 | Page

11

fair value of accounting and their position has been considered as an important element for the

corporate reporting segment of the company.

The company has given off right shares to the shareholder and have valued the same at fair

value. For assets that have been acquired under business combination the company has followed

Inventories are measured at normal sales prices that prevail under normal business conditions,

and in case of intangible assets they have taken into consideration the discounted cash flow

method. For valuation of property plant and equipment they have quoted market price for similar

items.

Thus, based on all this it can be said that method of valuation is Many but it depends on entities

which they choose. Between the two companies TPG has made better disclosure of the methods

adopted and have stated it clearly the methods are also very diverse. Which in case of Telstra is

very limited and there is only very asset that are valued as per fair value approach.

References

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit Documentation,

and Closing Review Notes in the Audit of Accounts Receivable.

Issues in Accounting Education, 33(2), pp.

43-55.

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics..

Journal of Accounting

Literature, 40(1), pp. 83-101.

11 | Page

fair value of accounting and their position has been considered as an important element for the

corporate reporting segment of the company.

The company has given off right shares to the shareholder and have valued the same at fair

value. For assets that have been acquired under business combination the company has followed

Inventories are measured at normal sales prices that prevail under normal business conditions,

and in case of intangible assets they have taken into consideration the discounted cash flow

method. For valuation of property plant and equipment they have quoted market price for similar

items.

Thus, based on all this it can be said that method of valuation is Many but it depends on entities

which they choose. Between the two companies TPG has made better disclosure of the methods

adopted and have stated it clearly the methods are also very diverse. Which in case of Telstra is

very limited and there is only very asset that are valued as per fair value approach.

References

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit Documentation,

and Closing Review Notes in the Audit of Accounts Receivable.

Issues in Accounting Education, 33(2), pp.

43-55.

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics..

Journal of Accounting

Literature, 40(1), pp. 83-101.

11 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.