ACC202 - Customer Profitability and Transfer Pricing Report 2018

VerifiedAdded on 2023/06/07

|8

|1965

|67

Report

AI Summary

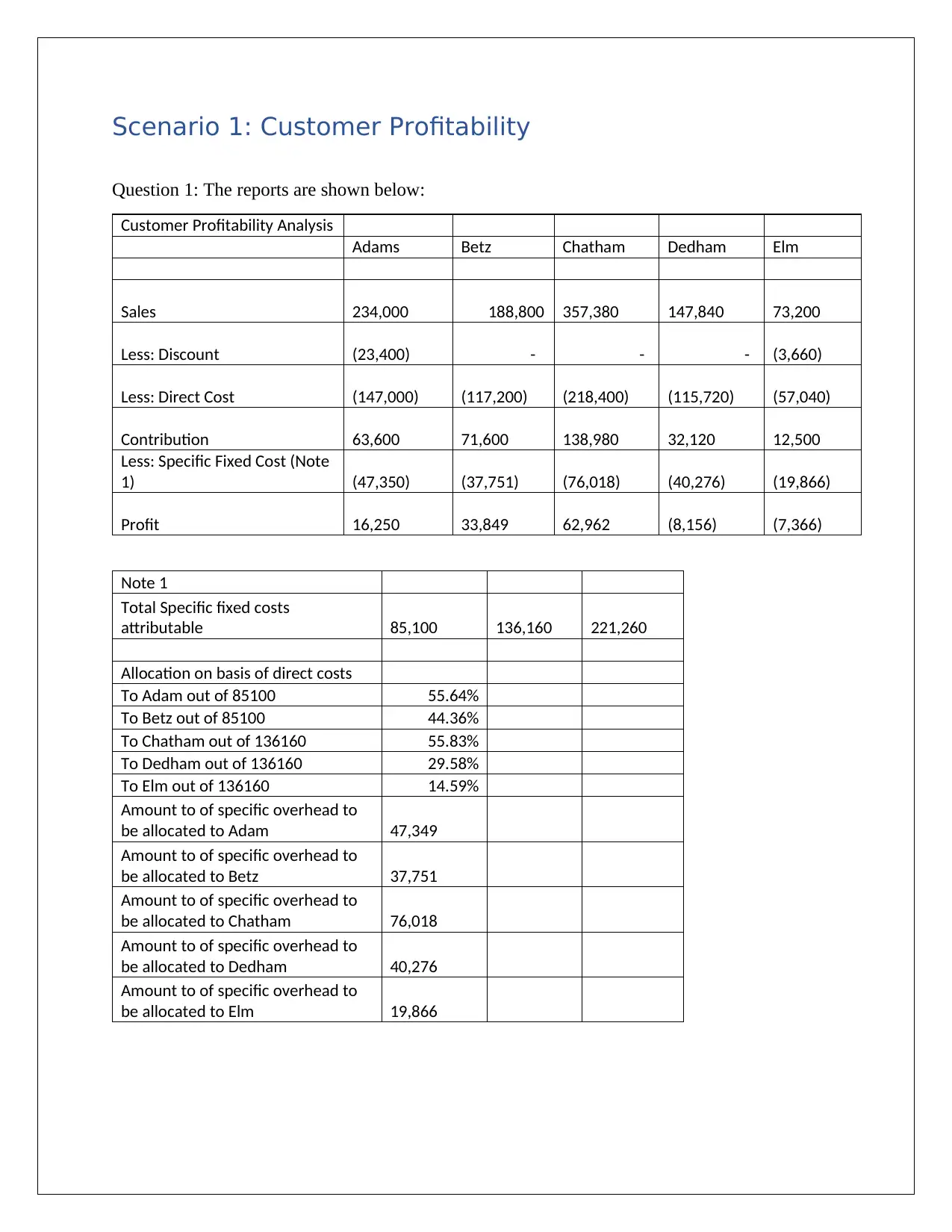

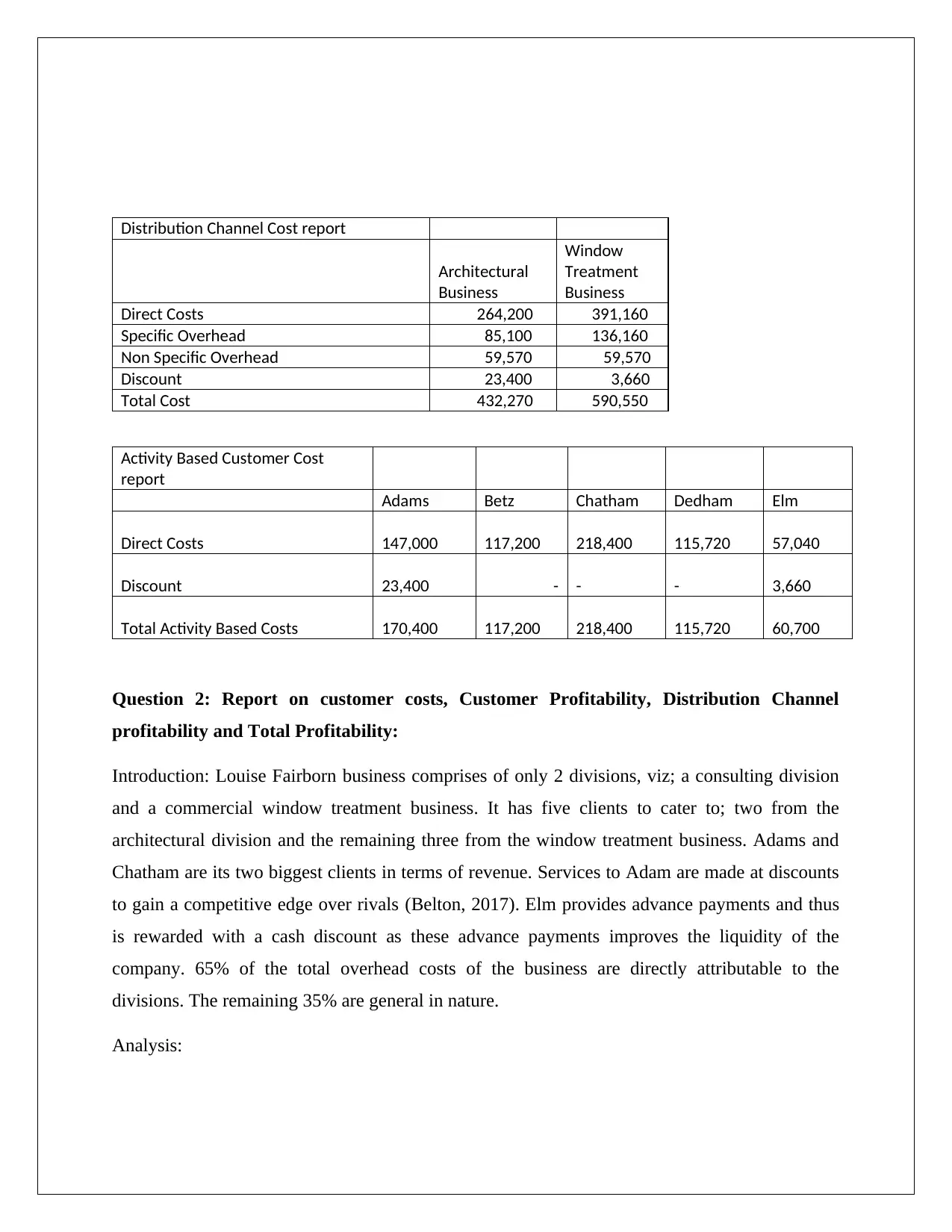

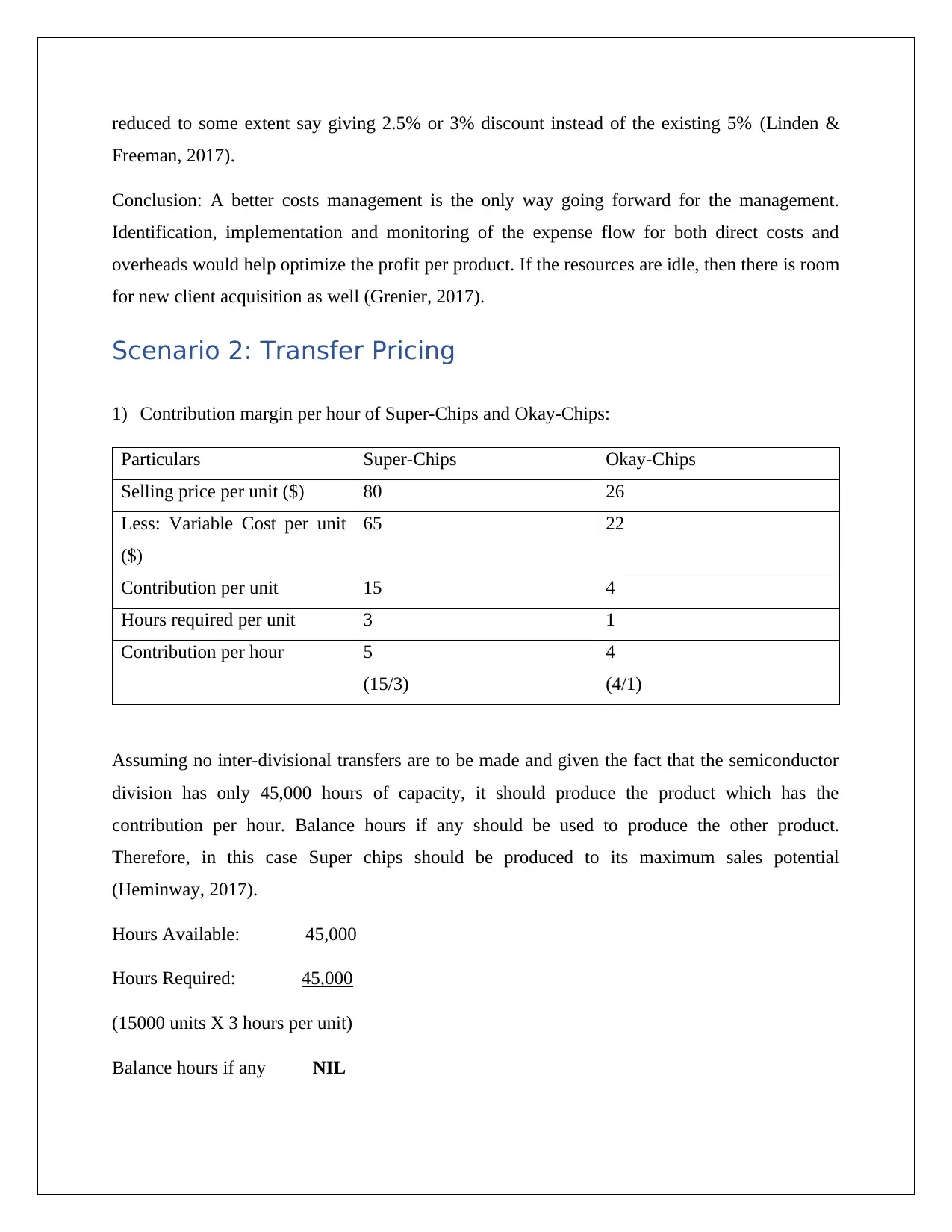

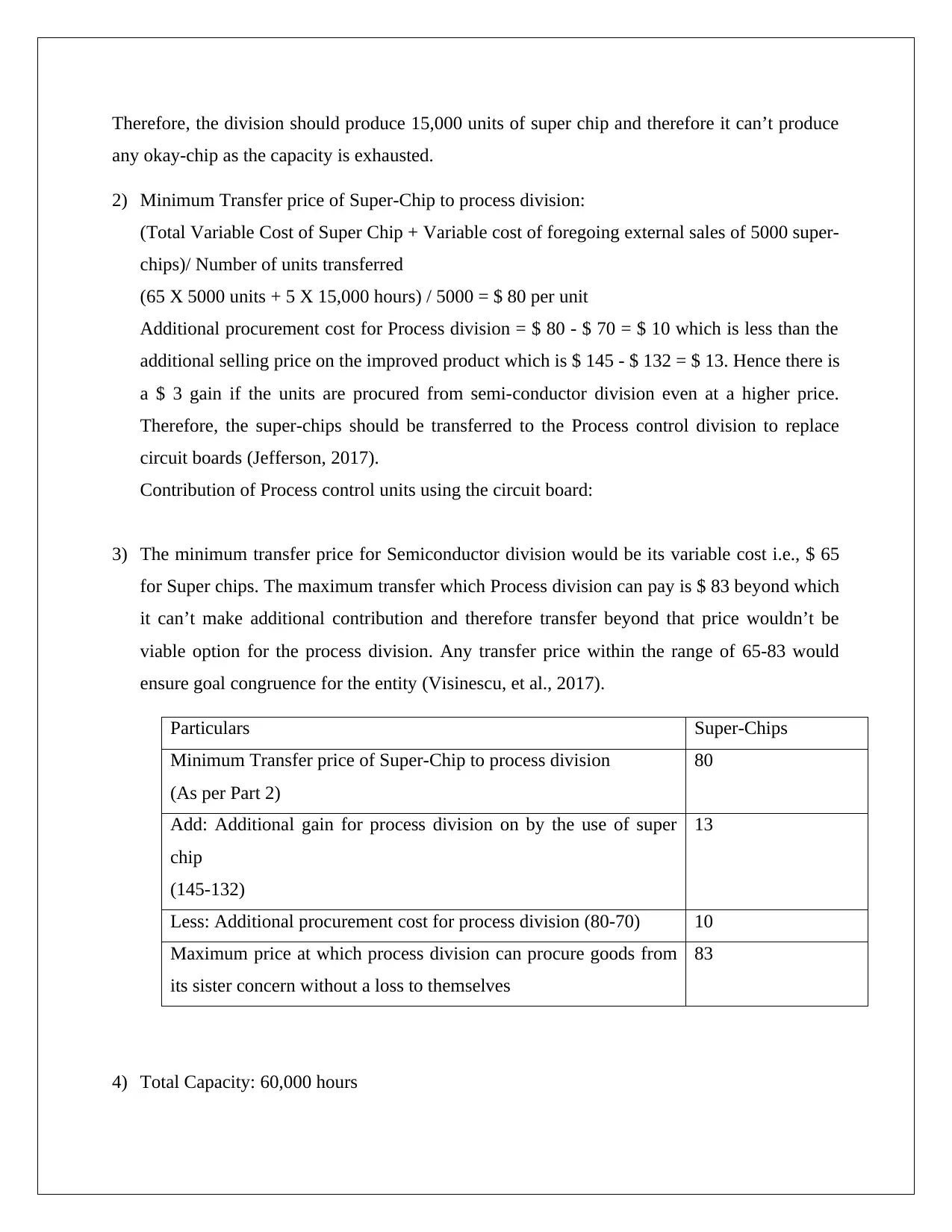

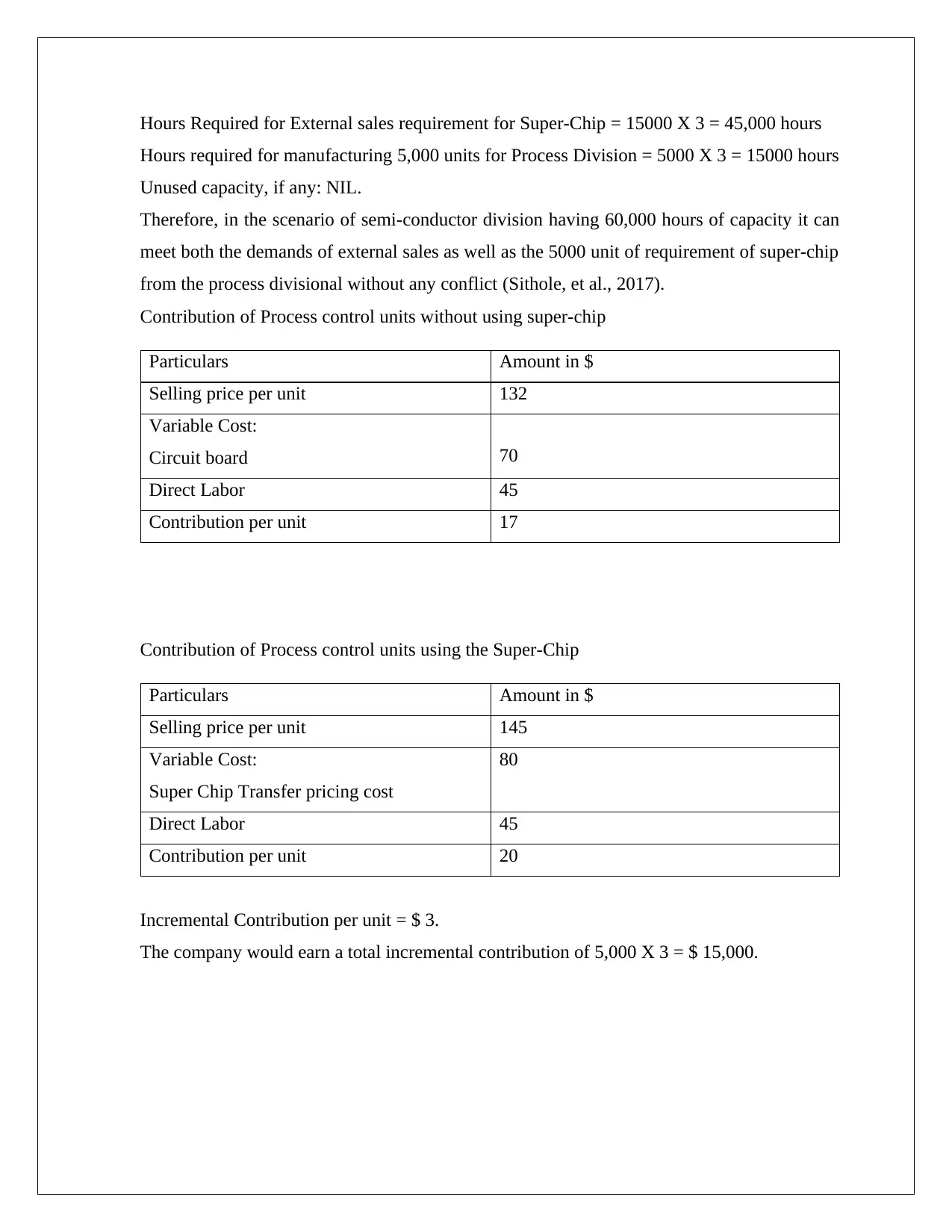

This report provides a comprehensive analysis of customer profitability and transfer pricing within Louise Fairbern's interior design business. Scenario 1 examines customer profitability across two divisions: consulting and commercial window treatment, evaluating contribution margins and recommending cost optimization strategies. The consulting division shows higher revenue from Adams but a better contribution margin from Betz, while the window treatment division identifies Dedham and Elm as loss-making clients due to high direct and specific overhead costs. Scenario 2 focuses on transfer pricing between the semiconductor and process divisions, determining optimal production and transfer prices for Super-Chips and Okay-Chips, considering capacity constraints and incremental contributions. The analysis concludes that the company should prioritize Super-Chip production to maximize profitability and that transfer pricing should fall within a range that ensures goal congruence for both divisions. The report recommends better cost management, resource optimization, and strategic pricing adjustments to improve overall profitability.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.