ACC203 Assignment: Managerial Accounting and Cost Analysis Report

VerifiedAdded on 2022/10/03

|9

|1893

|15

Homework Assignment

AI Summary

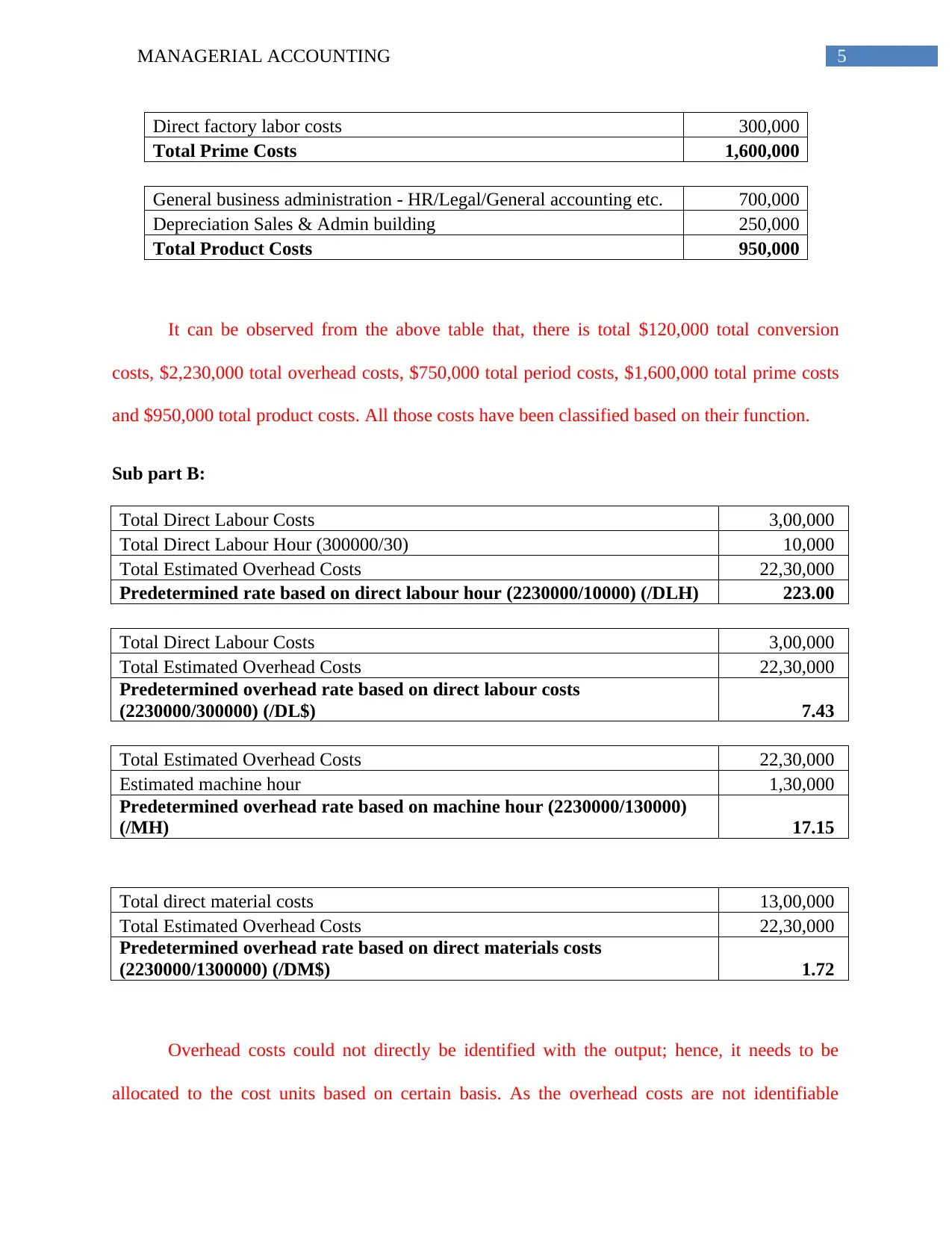

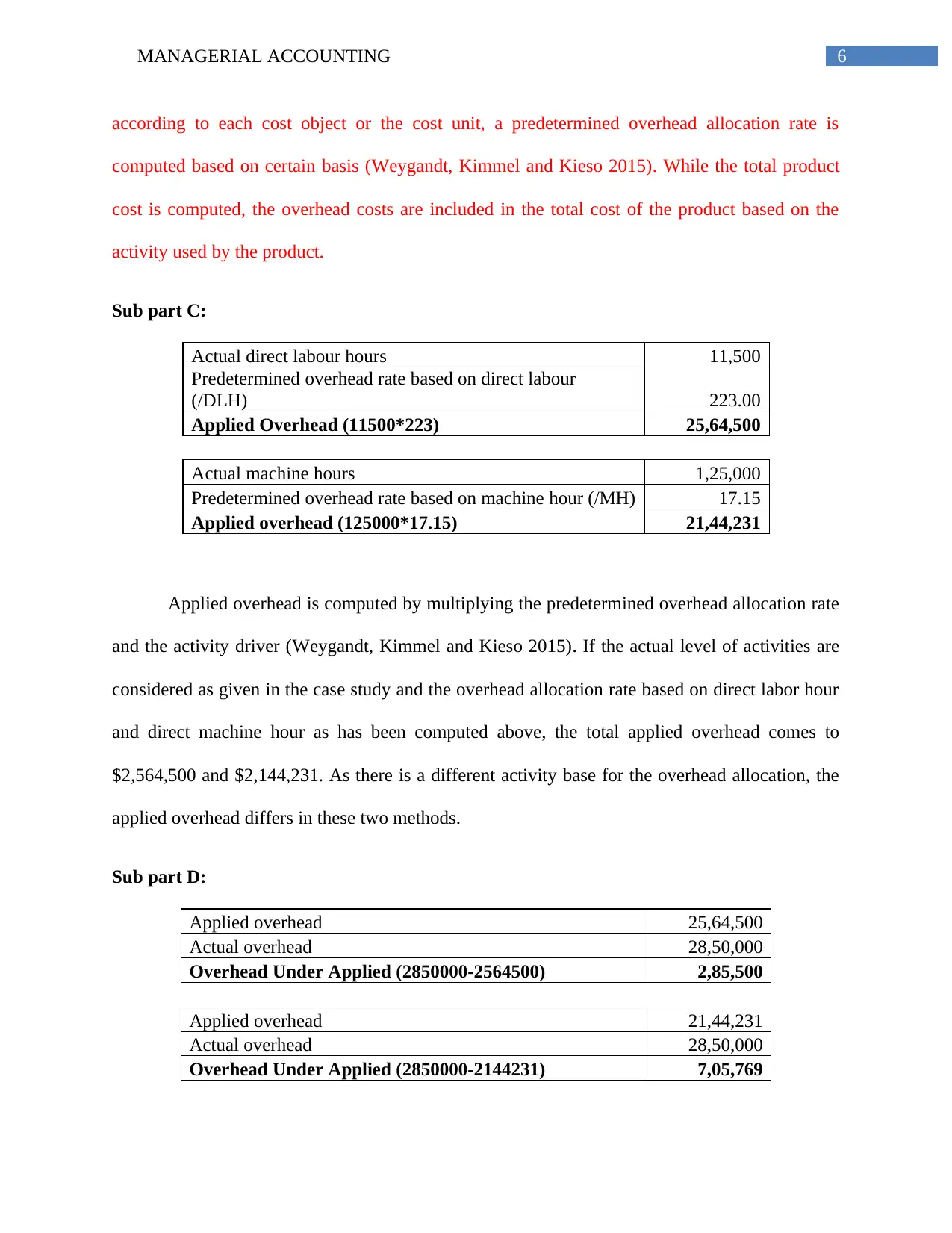

This document presents a comprehensive solution to a managerial accounting assignment. The assignment focuses on analyzing the operational efficiency of Flying Airlines. The solution includes a detailed cost analysis for a loader truck replacement decision, comparing the costs of using the existing truck versus replacing it with a new one. It also addresses cost classification, categorizing various costs into prime, period, overhead, and conversion costs. Furthermore, the solution explores overhead allocation, calculating predetermined overhead rates based on direct labor hours, direct labor costs, machine hours, and direct material costs. The assignment also involves calculating applied overhead and determining whether overhead is under or over applied. The solution provides step-by-step calculations and explanations, making it a valuable resource for students studying managerial accounting. This assignment is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.