Advanced Financial Accounting (ACC204) Assignment Report

VerifiedAdded on 2022/08/17

|13

|2531

|15

Report

AI Summary

This report provides a detailed analysis of advanced financial accounting principles, addressing key concepts such as IFRS and AASB 10. The report begins with an evaluation of relevant accounting standards, specifically focusing on the case of Future Plus Ltd, a biotechnology company, and the capitalization of research expenses under IFRS guidelines. It then delves into a capital lease scenario, presenting general journal entries, a schedule of lease rental payments, a depreciation schedule, and further journal entries. Finally, the report advises the CFO of ABC Pty Ltd on the requirements of AASB 10 concerning the control criterion, providing insights into consolidation principles and their application in different investment situations. The analysis covers the control over the operating and financing decisions of ABC trading trust and the 75% interest in JIB by ABC. Overall, the report offers a comprehensive understanding of complex accounting standards and their practical application.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Question 1: Evaluating the relevant accounting standard................................................................2

Question 2:.......................................................................................................................................4

1.a General journal entries to record the lease on 1 July 2019 for Tech Ltd:..................................4

1.b Preparing a schedule showing the division of the lease rental:.................................................5

1.c Prepare a depreciation schedule for the lessee:..........................................................................5

1.d Prepare general journal entries for the lessee:...........................................................................6

Question 3: Advising the CFO for the requirements of AASB 10 in respect of the control

criterion............................................................................................................................................7

References and Bibliography:........................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Question 1: Evaluating the relevant accounting standard................................................................2

Question 2:.......................................................................................................................................4

1.a General journal entries to record the lease on 1 July 2019 for Tech Ltd:..................................4

1.b Preparing a schedule showing the division of the lease rental:.................................................5

1.c Prepare a depreciation schedule for the lessee:..........................................................................5

1.d Prepare general journal entries for the lessee:...........................................................................6

Question 3: Advising the CFO for the requirements of AASB 10 in respect of the control

criterion............................................................................................................................................7

References and Bibliography:........................................................................................................10

2

ADVANCED FINANCIAL ACCOUNTING

Question 1: Evaluating the relevant accounting standard

The Board of Directors,

Future Plus Ltd

Subject: Analysing the Accounting Aspects on the Research Expenses

After analysing the current situation of Future Plus Ltd is a biotechnology company

relevant accounting standard could be highlighted from the case study, which might help the

organisation in their overall operations. Thus, the analysis of the case study has stated that the

Future Plus Ltd is a biotechnology company incurs huge research and development cost before

actually commercially providing the overall medicine (Iasplus.com 2020). Hence, adequate

adjustment, as per the GAAP (Generally Accepted Accounting Principles) rules, needs to be

used for highlighting the expense in their financial report. In the similar process, the IFRS

(International Financial report System) also has appropriate sections and standards, which can be

used by research and development companies to accommodate for the expenses conducted in

research program in their annual report. Dinh et al. (2015) stated that with different accounting

standards companies can prepare the financial report in accordance with the IFRS guidelines,

while helps in projecting the correct financial report of the organisation.

Therefore, after analysis the case study, it has been detected that Future Plus Ltd operates

in Australian exchange, where the overall operations would directly have effect from the IFRS

system. Thus, the overall expenses that is conducted on the research would be addressed by

using the IFRS standards that can be accommodated in the financial report (Ifrs.org 2020). The

case study has also indicated that the managing director wants to capitalise all the research

ADVANCED FINANCIAL ACCOUNTING

Question 1: Evaluating the relevant accounting standard

The Board of Directors,

Future Plus Ltd

Subject: Analysing the Accounting Aspects on the Research Expenses

After analysing the current situation of Future Plus Ltd is a biotechnology company

relevant accounting standard could be highlighted from the case study, which might help the

organisation in their overall operations. Thus, the analysis of the case study has stated that the

Future Plus Ltd is a biotechnology company incurs huge research and development cost before

actually commercially providing the overall medicine (Iasplus.com 2020). Hence, adequate

adjustment, as per the GAAP (Generally Accepted Accounting Principles) rules, needs to be

used for highlighting the expense in their financial report. In the similar process, the IFRS

(International Financial report System) also has appropriate sections and standards, which can be

used by research and development companies to accommodate for the expenses conducted in

research program in their annual report. Dinh et al. (2015) stated that with different accounting

standards companies can prepare the financial report in accordance with the IFRS guidelines,

while helps in projecting the correct financial report of the organisation.

Therefore, after analysis the case study, it has been detected that Future Plus Ltd operates

in Australian exchange, where the overall operations would directly have effect from the IFRS

system. Thus, the overall expenses that is conducted on the research would be addressed by

using the IFRS standards that can be accommodated in the financial report (Ifrs.org 2020). The

case study has also indicated that the managing director wants to capitalise all the research

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

expenses and other staff salary that were involved in the research objective. However, the current

rule and regulations laid in Australia by the IFRS system does not accommodate the research

expenses to be capitalise by any organisation. Andre, Dionysiou and Tsalavoutas (2018)

indicated that using the IFRS standard companies are bale to detect the level of appropriate

expenses that needs to be included in the financial report for identifying the correct financial

statement in the annual report.

Therefore, from the analysis, it has been detected that the IAS 38 states about the

recognition of research expenditure, which is it par 54 and par 57, where it depicts about the

recognition of development costs. Thus, it is detected that more particular research related terms

expense needs to be capitalised, where the non-disclosure would not be perfect for the annual

report. The analysis has mainly indicated that the research expenses will mainly turn into

intellectual property of the organisation, where the final target of commercial production and

company will be relevant benefits from the expenditure in the long term. According to the IFRS

standard, it is detected the overall expenses that is conducted on the research can be capitalised

by the company, while the overall expenses on staff should not be capitalised, as it is not directly

engaged in the research job. Henceforth, Future Plus Ltd can appropriately utilise the investment

of $30 million, as an appropriate development cost for the organisation. On the contrary, De and

Sharma (2017) indicated that excessive expenses that is conducted by companies in their

research are not included in the development costs, which can be considered as an intellectual

property of the organisation

Future Plus Ltd can use the IFRS standard IAS 38 for listing the $30 million of

development cost, as the overall research which would be commercially viable and might

generate higher revenues in the long run. This measure would allow the company before the tax

ADVANCED FINANCIAL ACCOUNTING

expenses and other staff salary that were involved in the research objective. However, the current

rule and regulations laid in Australia by the IFRS system does not accommodate the research

expenses to be capitalise by any organisation. Andre, Dionysiou and Tsalavoutas (2018)

indicated that using the IFRS standard companies are bale to detect the level of appropriate

expenses that needs to be included in the financial report for identifying the correct financial

statement in the annual report.

Therefore, from the analysis, it has been detected that the IAS 38 states about the

recognition of research expenditure, which is it par 54 and par 57, where it depicts about the

recognition of development costs. Thus, it is detected that more particular research related terms

expense needs to be capitalised, where the non-disclosure would not be perfect for the annual

report. The analysis has mainly indicated that the research expenses will mainly turn into

intellectual property of the organisation, where the final target of commercial production and

company will be relevant benefits from the expenditure in the long term. According to the IFRS

standard, it is detected the overall expenses that is conducted on the research can be capitalised

by the company, while the overall expenses on staff should not be capitalised, as it is not directly

engaged in the research job. Henceforth, Future Plus Ltd can appropriately utilise the investment

of $30 million, as an appropriate development cost for the organisation. On the contrary, De and

Sharma (2017) indicated that excessive expenses that is conducted by companies in their

research are not included in the development costs, which can be considered as an intellectual

property of the organisation

Future Plus Ltd can use the IFRS standard IAS 38 for listing the $30 million of

development cost, as the overall research which would be commercially viable and might

generate higher revenues in the long run. This measure would allow the company before the tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

authorities to capitalise their overall development expenses, while excluding the overall staff

expenses. The staff expenses are not considered to be viable under IAS 38 method, where it is

not disclosed under the standard to be used as the development cost of the organisation. The

standard directly states that the research job does not consider the overall staff expenses, which

in turn could not be capitalised by Future Plus Ltd under IAS 38 (Capkun, Collins and Jeanjean

2016). Thus, the intangible asset arising from development are recognised as follows.

Intention to complete the intangible asset and use or sell it

Ability to use or sell the intangible asset

Intangible asset will generate probable future economic benefits

Thanking You,

Legal Consultant

Question 2:

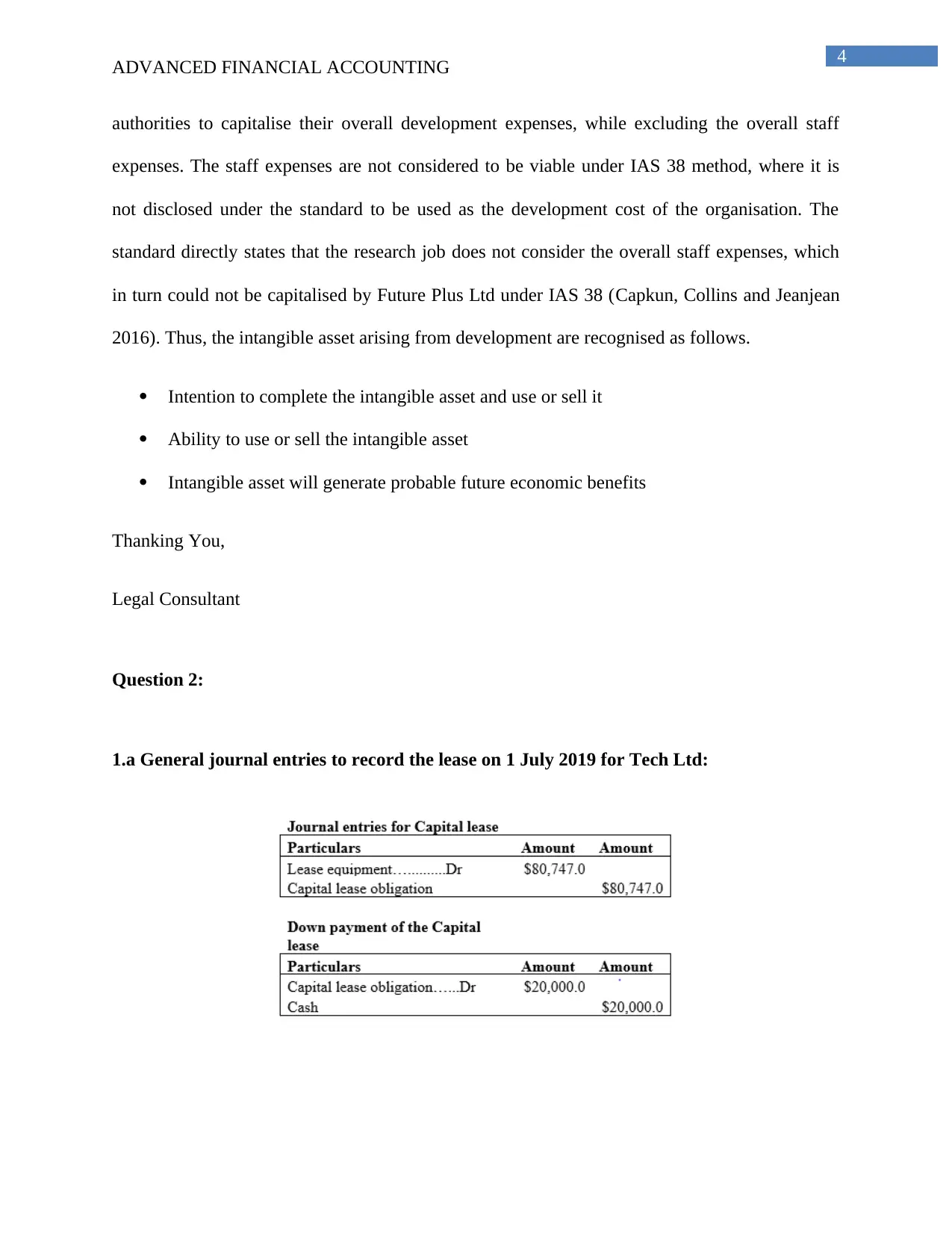

1.a General journal entries to record the lease on 1 July 2019 for Tech Ltd:

ADVANCED FINANCIAL ACCOUNTING

authorities to capitalise their overall development expenses, while excluding the overall staff

expenses. The staff expenses are not considered to be viable under IAS 38 method, where it is

not disclosed under the standard to be used as the development cost of the organisation. The

standard directly states that the research job does not consider the overall staff expenses, which

in turn could not be capitalised by Future Plus Ltd under IAS 38 (Capkun, Collins and Jeanjean

2016). Thus, the intangible asset arising from development are recognised as follows.

Intention to complete the intangible asset and use or sell it

Ability to use or sell the intangible asset

Intangible asset will generate probable future economic benefits

Thanking You,

Legal Consultant

Question 2:

1.a General journal entries to record the lease on 1 July 2019 for Tech Ltd:

5

ADVANCED FINANCIAL ACCOUNTING

The above calculations state about the overall journal entries that would be conducted for

the capital lease before the start of the year. The journal entries mainly comprise of the overall

capital lease obligations and the cash down payment that is conducted from the start of the year.

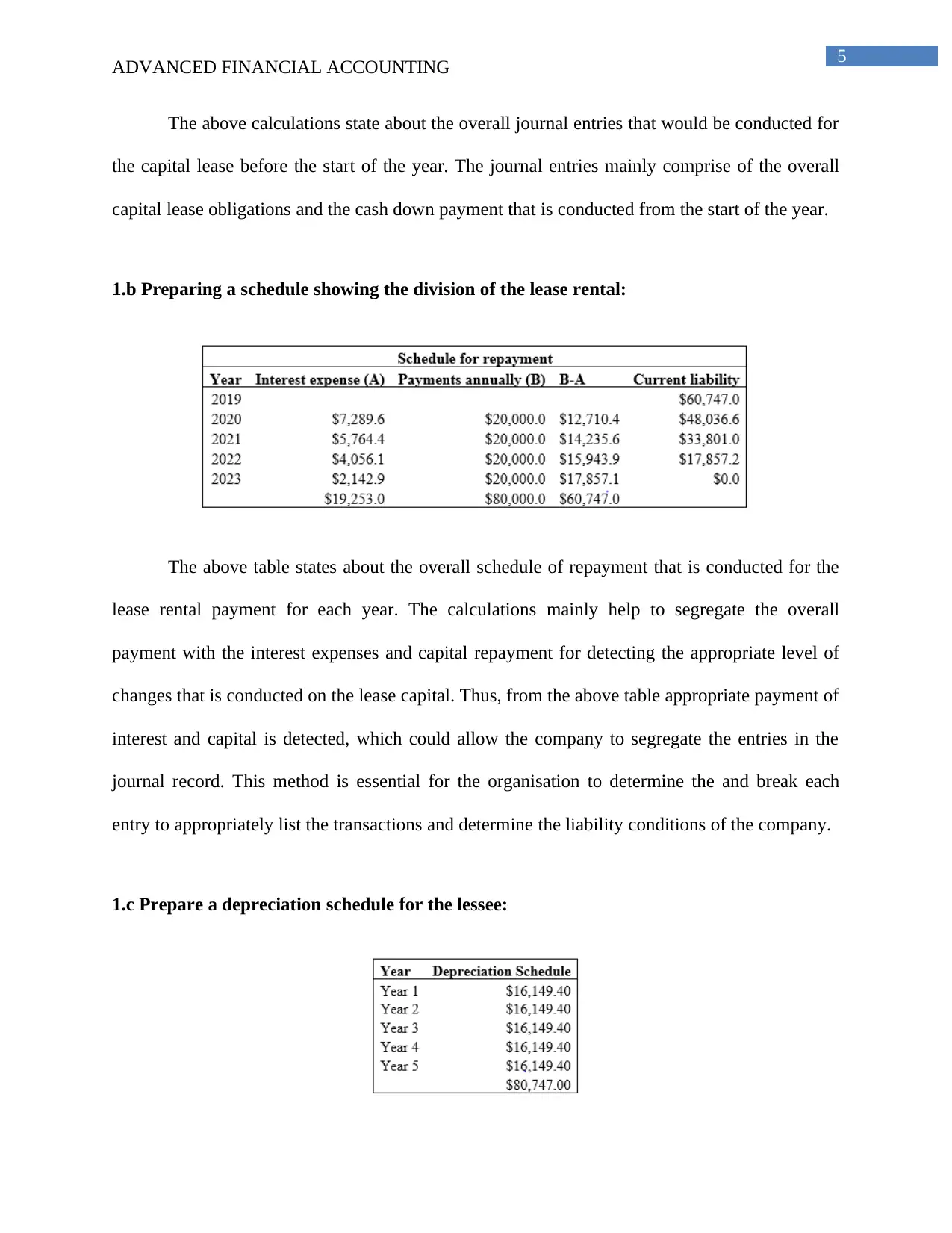

1.b Preparing a schedule showing the division of the lease rental:

The above table states about the overall schedule of repayment that is conducted for the

lease rental payment for each year. The calculations mainly help to segregate the overall

payment with the interest expenses and capital repayment for detecting the appropriate level of

changes that is conducted on the lease capital. Thus, from the above table appropriate payment of

interest and capital is detected, which could allow the company to segregate the entries in the

journal record. This method is essential for the organisation to determine the and break each

entry to appropriately list the transactions and determine the liability conditions of the company.

1.c Prepare a depreciation schedule for the lessee:

ADVANCED FINANCIAL ACCOUNTING

The above calculations state about the overall journal entries that would be conducted for

the capital lease before the start of the year. The journal entries mainly comprise of the overall

capital lease obligations and the cash down payment that is conducted from the start of the year.

1.b Preparing a schedule showing the division of the lease rental:

The above table states about the overall schedule of repayment that is conducted for the

lease rental payment for each year. The calculations mainly help to segregate the overall

payment with the interest expenses and capital repayment for detecting the appropriate level of

changes that is conducted on the lease capital. Thus, from the above table appropriate payment of

interest and capital is detected, which could allow the company to segregate the entries in the

journal record. This method is essential for the organisation to determine the and break each

entry to appropriately list the transactions and determine the liability conditions of the company.

1.c Prepare a depreciation schedule for the lessee:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

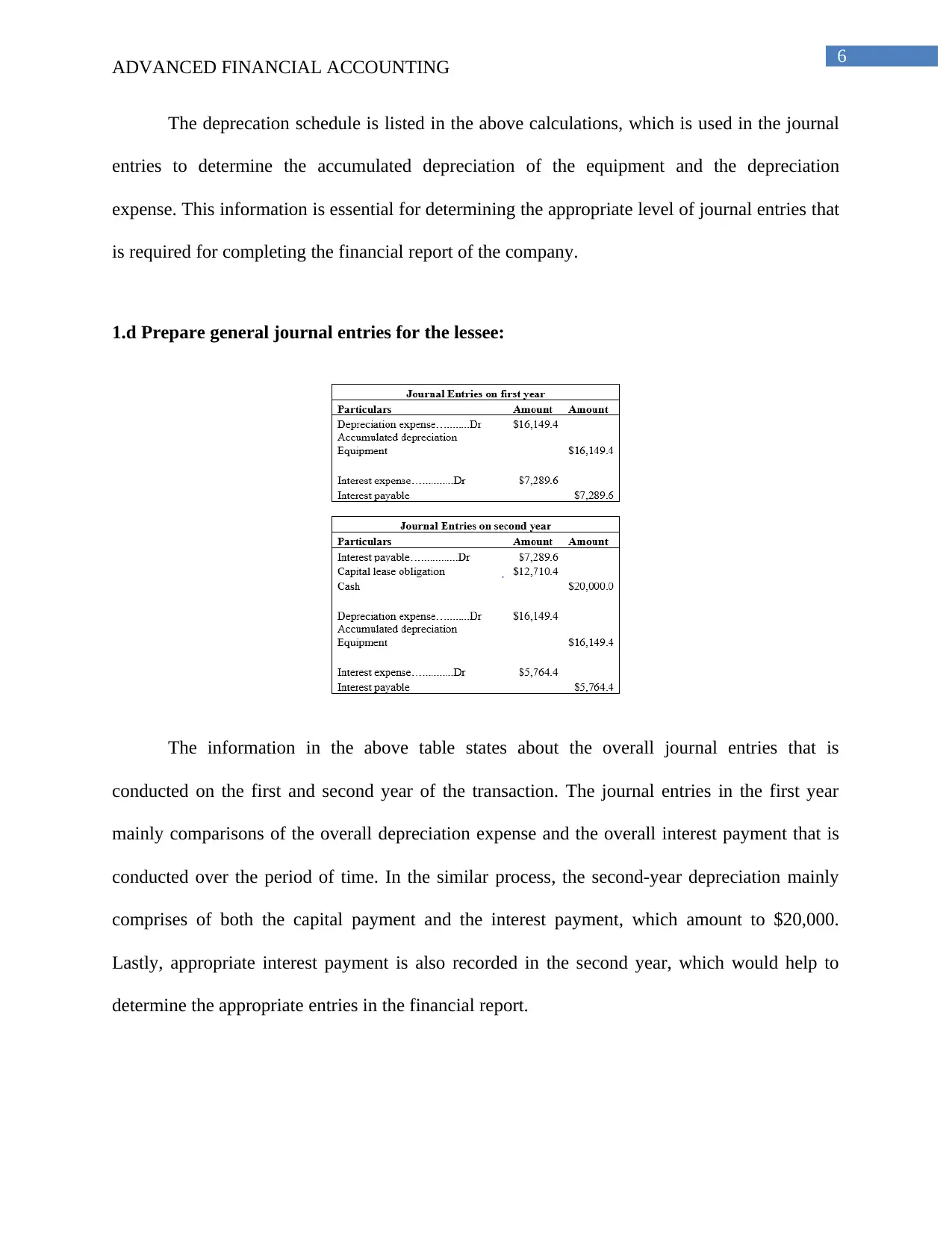

The deprecation schedule is listed in the above calculations, which is used in the journal

entries to determine the accumulated depreciation of the equipment and the depreciation

expense. This information is essential for determining the appropriate level of journal entries that

is required for completing the financial report of the company.

1.d Prepare general journal entries for the lessee:

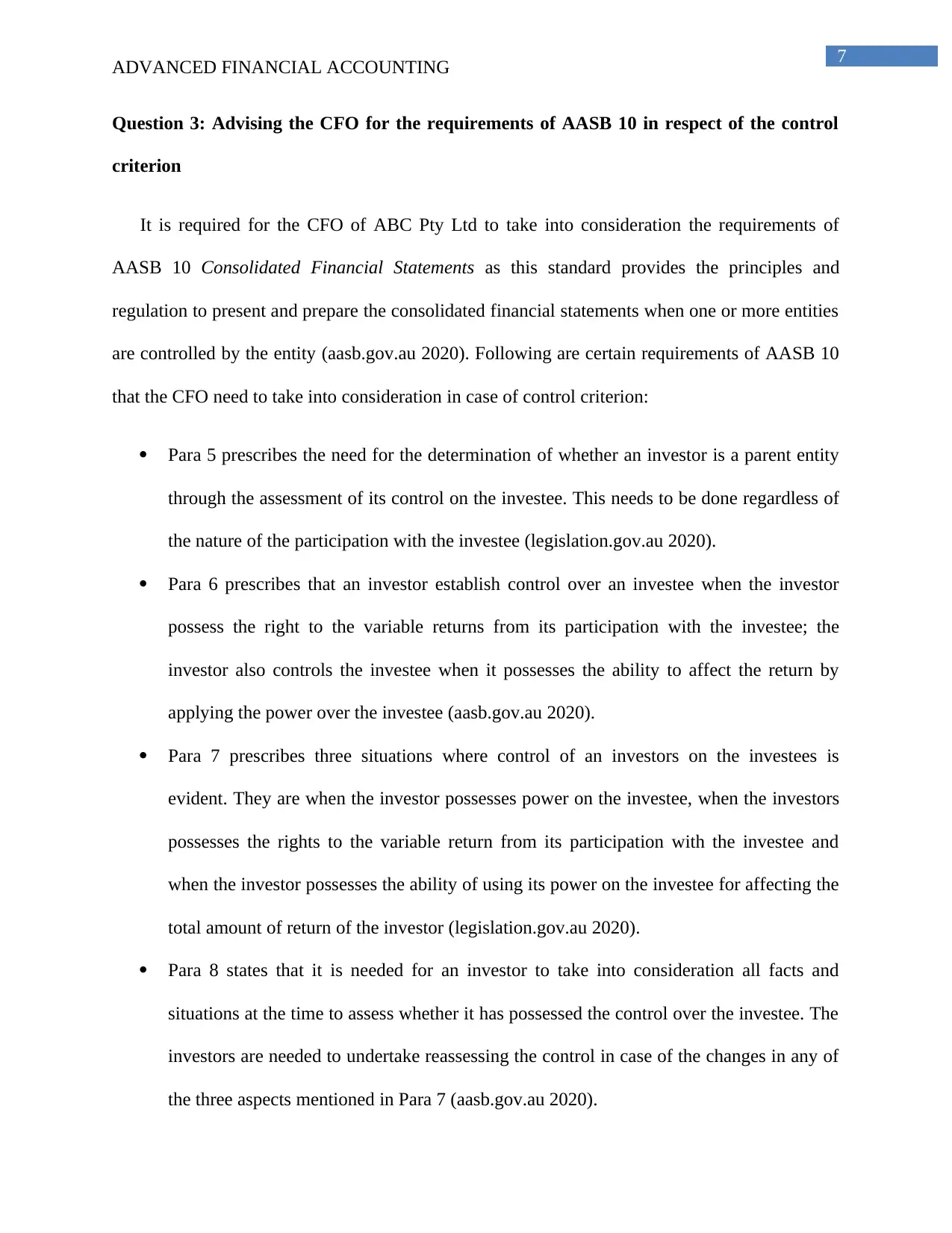

The information in the above table states about the overall journal entries that is

conducted on the first and second year of the transaction. The journal entries in the first year

mainly comparisons of the overall depreciation expense and the overall interest payment that is

conducted over the period of time. In the similar process, the second-year depreciation mainly

comprises of both the capital payment and the interest payment, which amount to $20,000.

Lastly, appropriate interest payment is also recorded in the second year, which would help to

determine the appropriate entries in the financial report.

ADVANCED FINANCIAL ACCOUNTING

The deprecation schedule is listed in the above calculations, which is used in the journal

entries to determine the accumulated depreciation of the equipment and the depreciation

expense. This information is essential for determining the appropriate level of journal entries that

is required for completing the financial report of the company.

1.d Prepare general journal entries for the lessee:

The information in the above table states about the overall journal entries that is

conducted on the first and second year of the transaction. The journal entries in the first year

mainly comparisons of the overall depreciation expense and the overall interest payment that is

conducted over the period of time. In the similar process, the second-year depreciation mainly

comprises of both the capital payment and the interest payment, which amount to $20,000.

Lastly, appropriate interest payment is also recorded in the second year, which would help to

determine the appropriate entries in the financial report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

Question 3: Advising the CFO for the requirements of AASB 10 in respect of the control

criterion

It is required for the CFO of ABC Pty Ltd to take into consideration the requirements of

AASB 10 Consolidated Financial Statements as this standard provides the principles and

regulation to present and prepare the consolidated financial statements when one or more entities

are controlled by the entity (aasb.gov.au 2020). Following are certain requirements of AASB 10

that the CFO need to take into consideration in case of control criterion:

Para 5 prescribes the need for the determination of whether an investor is a parent entity

through the assessment of its control on the investee. This needs to be done regardless of

the nature of the participation with the investee (legislation.gov.au 2020).

Para 6 prescribes that an investor establish control over an investee when the investor

possess the right to the variable returns from its participation with the investee; the

investor also controls the investee when it possesses the ability to affect the return by

applying the power over the investee (aasb.gov.au 2020).

Para 7 prescribes three situations where control of an investors on the investees is

evident. They are when the investor possesses power on the investee, when the investors

possesses the rights to the variable return from its participation with the investee and

when the investor possesses the ability of using its power on the investee for affecting the

total amount of return of the investor (legislation.gov.au 2020).

Para 8 states that it is needed for an investor to take into consideration all facts and

situations at the time to assess whether it has possessed the control over the investee. The

investors are needed to undertake reassessing the control in case of the changes in any of

the three aspects mentioned in Para 7 (aasb.gov.au 2020).

ADVANCED FINANCIAL ACCOUNTING

Question 3: Advising the CFO for the requirements of AASB 10 in respect of the control

criterion

It is required for the CFO of ABC Pty Ltd to take into consideration the requirements of

AASB 10 Consolidated Financial Statements as this standard provides the principles and

regulation to present and prepare the consolidated financial statements when one or more entities

are controlled by the entity (aasb.gov.au 2020). Following are certain requirements of AASB 10

that the CFO need to take into consideration in case of control criterion:

Para 5 prescribes the need for the determination of whether an investor is a parent entity

through the assessment of its control on the investee. This needs to be done regardless of

the nature of the participation with the investee (legislation.gov.au 2020).

Para 6 prescribes that an investor establish control over an investee when the investor

possess the right to the variable returns from its participation with the investee; the

investor also controls the investee when it possesses the ability to affect the return by

applying the power over the investee (aasb.gov.au 2020).

Para 7 prescribes three situations where control of an investors on the investees is

evident. They are when the investor possesses power on the investee, when the investors

possesses the rights to the variable return from its participation with the investee and

when the investor possesses the ability of using its power on the investee for affecting the

total amount of return of the investor (legislation.gov.au 2020).

Para 8 states that it is needed for an investor to take into consideration all facts and

situations at the time to assess whether it has possessed the control over the investee. The

investors are needed to undertake reassessing the control in case of the changes in any of

the three aspects mentioned in Para 7 (aasb.gov.au 2020).

8

ADVANCED FINANCIAL ACCOUNTING

Para 9 prescribes that two or more investors are required to act together for directing the

relevant activities in case they control an investee together. This restricts the single

investor to direct the activities of the investee as direction cannot be given by a single

investee without cooperation (legislation.gov.au 2020).

The following discussion assesses two investments situations in lights of the principles of

AASB 10.

1. As mentioned in the provided situation Mr Frank, Mrs Ada and Mr Leonard are the

directors of ABC that has complete control over the operating and financing decisions of

ABC trading trust. Therefore, as prescribed in AASB 10, ABC is the investor and ABC

trading trust is the investee. As mentioned in the provided situation, ABC has control

over the operations and activities of ABC trading trust as it can direct the operations of

the trust by taking operating and financing decisions; and this decision making power

over the trust provides ABC with the power to affect the return from it

(cpaaustralia.com.au 2020). It indicates that ABC has control over ABC trading trust as

per the principles of AASB 10. Now, it can be seen that ABC has three partners having

different proportions to share income. In line with Para 9 of AASB 10, no member of

ABC can direct the operations of ABC trading trust without cooperation of the others

irrespective of the percentage of sharing the income; and therefore, there is not any

individual control of any member of ABC on the trading trust. Hence, in line with the

same section, all the three members that are Mr Frank, Mrs Ada and Mr Leonard have

collective control over ABC trading trust. Since ABC has control over ABC trading trust,

consolidation will be required in this case (pwc.com.au 2020).

ADVANCED FINANCIAL ACCOUNTING

Para 9 prescribes that two or more investors are required to act together for directing the

relevant activities in case they control an investee together. This restricts the single

investor to direct the activities of the investee as direction cannot be given by a single

investee without cooperation (legislation.gov.au 2020).

The following discussion assesses two investments situations in lights of the principles of

AASB 10.

1. As mentioned in the provided situation Mr Frank, Mrs Ada and Mr Leonard are the

directors of ABC that has complete control over the operating and financing decisions of

ABC trading trust. Therefore, as prescribed in AASB 10, ABC is the investor and ABC

trading trust is the investee. As mentioned in the provided situation, ABC has control

over the operations and activities of ABC trading trust as it can direct the operations of

the trust by taking operating and financing decisions; and this decision making power

over the trust provides ABC with the power to affect the return from it

(cpaaustralia.com.au 2020). It indicates that ABC has control over ABC trading trust as

per the principles of AASB 10. Now, it can be seen that ABC has three partners having

different proportions to share income. In line with Para 9 of AASB 10, no member of

ABC can direct the operations of ABC trading trust without cooperation of the others

irrespective of the percentage of sharing the income; and therefore, there is not any

individual control of any member of ABC on the trading trust. Hence, in line with the

same section, all the three members that are Mr Frank, Mrs Ada and Mr Leonard have

collective control over ABC trading trust. Since ABC has control over ABC trading trust,

consolidation will be required in this case (pwc.com.au 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

2. It can be seen from the provided case ABC has 75 percent interest in JIB and ABC

gained this interest by converting a major loan to JIB into equity due to the uncertainty of

JIB to repay the loan because of poor trading. It is also mentioned that ABC is a passive

investor as it has no seat on the board of directors and has no right to make financing and

operating decisions of JIB. Since ABC has 75 percent interest in JIB, it can apply its

control on JIB and therefore, control rests. As per AASB 10, when there is control on the

investee, consolidation needs to be done. Hence by complying with AASB 10,

consolidation will be required in case ABC exercises its control over JIB (Cîrstea 2014).

ADVANCED FINANCIAL ACCOUNTING

2. It can be seen from the provided case ABC has 75 percent interest in JIB and ABC

gained this interest by converting a major loan to JIB into equity due to the uncertainty of

JIB to repay the loan because of poor trading. It is also mentioned that ABC is a passive

investor as it has no seat on the board of directors and has no right to make financing and

operating decisions of JIB. Since ABC has 75 percent interest in JIB, it can apply its

control on JIB and therefore, control rests. As per AASB 10, when there is control on the

investee, consolidation needs to be done. Hence by complying with AASB 10,

consolidation will be required in case ABC exercises its control over JIB (Cîrstea 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

References and Bibliography:

Aasb.gov.au. 2020. Consolidated Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_07-15_COMPdec17_01-18.pdf

[Accessed 6 Feb. 2020].

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting and

Public Policy, 35(4), pp.352-394.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other

intangible assets in business combinations–the Portuguese case. Australian Accounting

Review, 26(1), pp.4-20.

Cîrstea, A., 2014. The need for public sector consolidated financial statements. Procedia

Economics and Finance, 15, pp.1289-1296.

Cpaaustralia.com.au. 2020. [online] Available at:

https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-resources/ifrs-

factsheets/factsheet-ifrs10-consolidated-financial-statements.pdf?

la=en&rev=b3bfd7428f0b4ec8bb4f4ab740c30180 [Accessed 6 Feb. 2020].

ADVANCED FINANCIAL ACCOUNTING

References and Bibliography:

Aasb.gov.au. 2020. Consolidated Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_07-15_COMPdec17_01-18.pdf

[Accessed 6 Feb. 2020].

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting and

Public Policy, 35(4), pp.352-394.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other

intangible assets in business combinations–the Portuguese case. Australian Accounting

Review, 26(1), pp.4-20.

Cîrstea, A., 2014. The need for public sector consolidated financial statements. Procedia

Economics and Finance, 15, pp.1289-1296.

Cpaaustralia.com.au. 2020. [online] Available at:

https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-resources/ifrs-

factsheets/factsheet-ifrs10-consolidated-financial-statements.pdf?

la=en&rev=b3bfd7428f0b4ec8bb4f4ab740c30180 [Accessed 6 Feb. 2020].

11

ADVANCED FINANCIAL ACCOUNTING

De Villiers, C. and Sharma, U., 2017. A critical reflection on the future of financial, intellectual

capital, sustainability and integrated reporting. Critical Perspectives on Accounting, p.101999.

Denicolai, S., Cotta Ramusino, E. and Sotti, F., 2015. The impact of intangibles on firm

growth. Technology Analysis & Strategic Management, 27(2), pp.219-236.

Dinh, T., Eierle, B., Schultze, W. and Steeger, L., 2015. Research and development, uncertainty,

and analysts’ forecasts: The case of IAS 38. Journal of International Financial Management &

Accounting, 26(3), pp.257-293.

Iasplus.com. 2020. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 6 Feb. 2020].

Ifrs.org. 2020. IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-38-intangible-assets/ [Accessed 6 Feb. 2020].

Legislation.gov.au. 2020. AASB 10 - Consolidated Financial Statements - July 2015 . [online]

Available at: https://www.legislation.gov.au/Details/F2018C00317 [Accessed 6 Feb. 2020].

Öztürk, E. and Zeren, F., 2015. The impact of r&d expenditure on firm performance in

manufacturing industry: further evidence from Turkey. International Journal of Economics and

Research, 6(2), pp.32-36.

Pwc.com.au. 2020. [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/consolidation-are-you-one-big-happy-family.pdf

[Accessed 6 Feb. 2020].

ADVANCED FINANCIAL ACCOUNTING

De Villiers, C. and Sharma, U., 2017. A critical reflection on the future of financial, intellectual

capital, sustainability and integrated reporting. Critical Perspectives on Accounting, p.101999.

Denicolai, S., Cotta Ramusino, E. and Sotti, F., 2015. The impact of intangibles on firm

growth. Technology Analysis & Strategic Management, 27(2), pp.219-236.

Dinh, T., Eierle, B., Schultze, W. and Steeger, L., 2015. Research and development, uncertainty,

and analysts’ forecasts: The case of IAS 38. Journal of International Financial Management &

Accounting, 26(3), pp.257-293.

Iasplus.com. 2020. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 6 Feb. 2020].

Ifrs.org. 2020. IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-38-intangible-assets/ [Accessed 6 Feb. 2020].

Legislation.gov.au. 2020. AASB 10 - Consolidated Financial Statements - July 2015 . [online]

Available at: https://www.legislation.gov.au/Details/F2018C00317 [Accessed 6 Feb. 2020].

Öztürk, E. and Zeren, F., 2015. The impact of r&d expenditure on firm performance in

manufacturing industry: further evidence from Turkey. International Journal of Economics and

Research, 6(2), pp.32-36.

Pwc.com.au. 2020. [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/consolidation-are-you-one-big-happy-family.pdf

[Accessed 6 Feb. 2020].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.