ACC2103 Managerial Accounting: Cost Analysis and Breakeven Points

VerifiedAdded on 2023/06/12

|8

|1611

|176

Homework Assignment

AI Summary

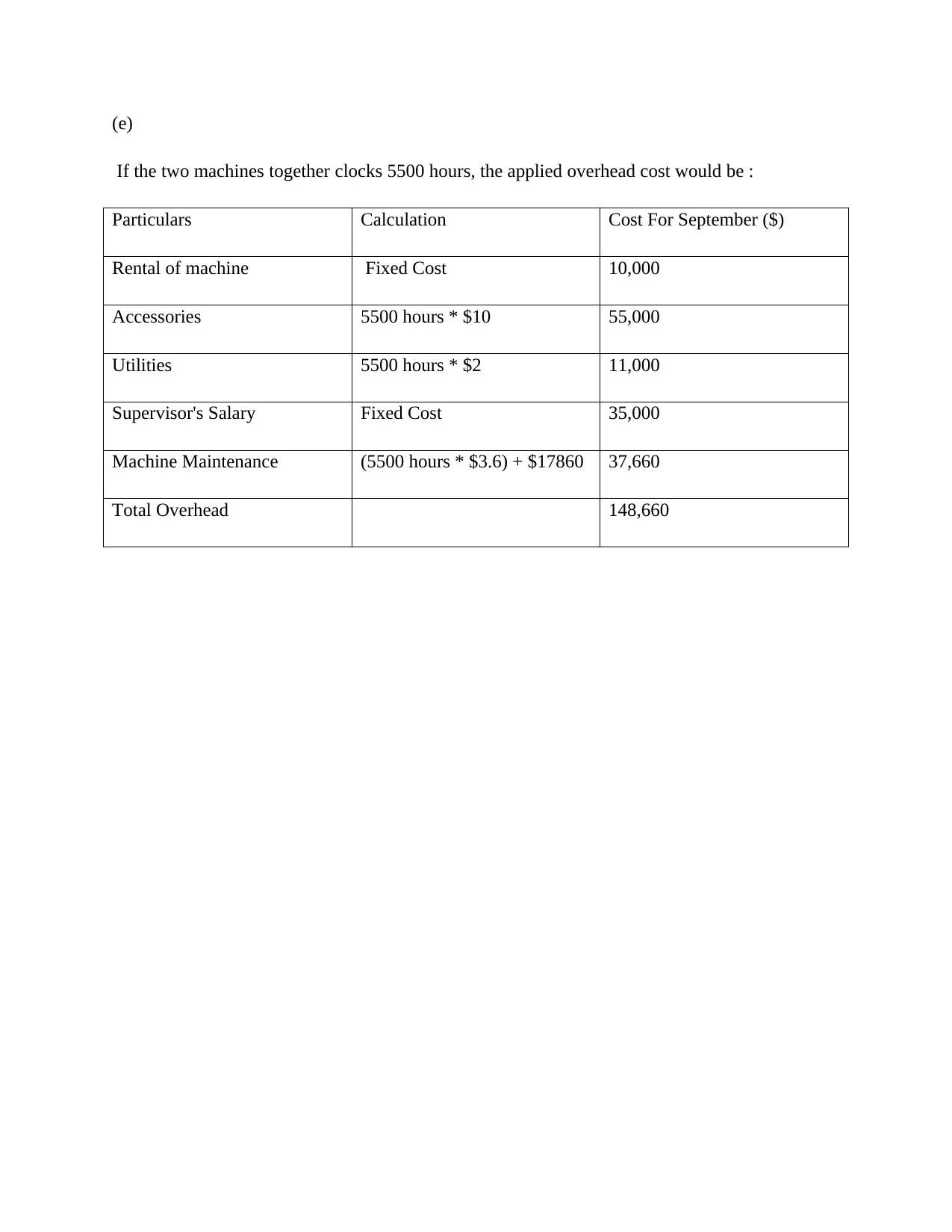

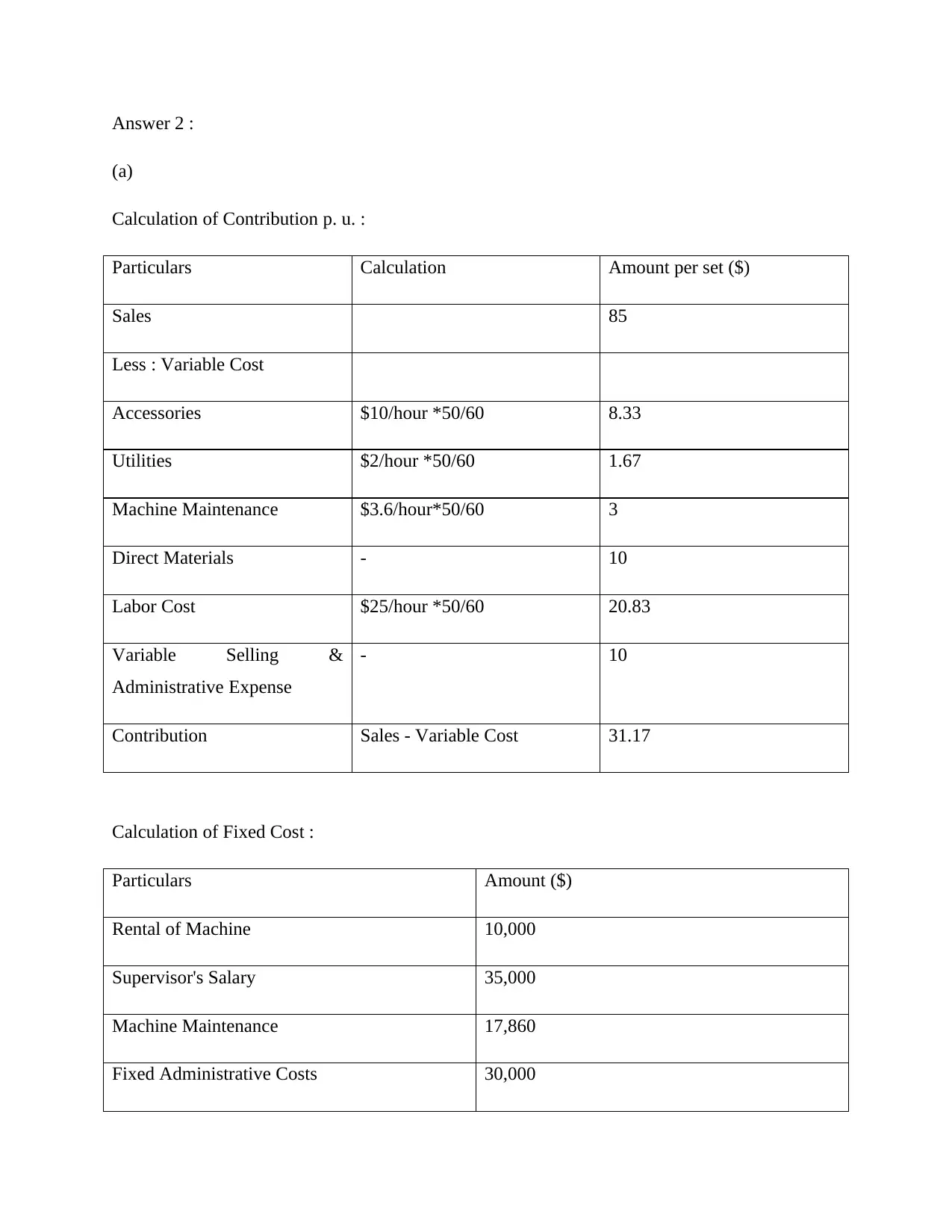

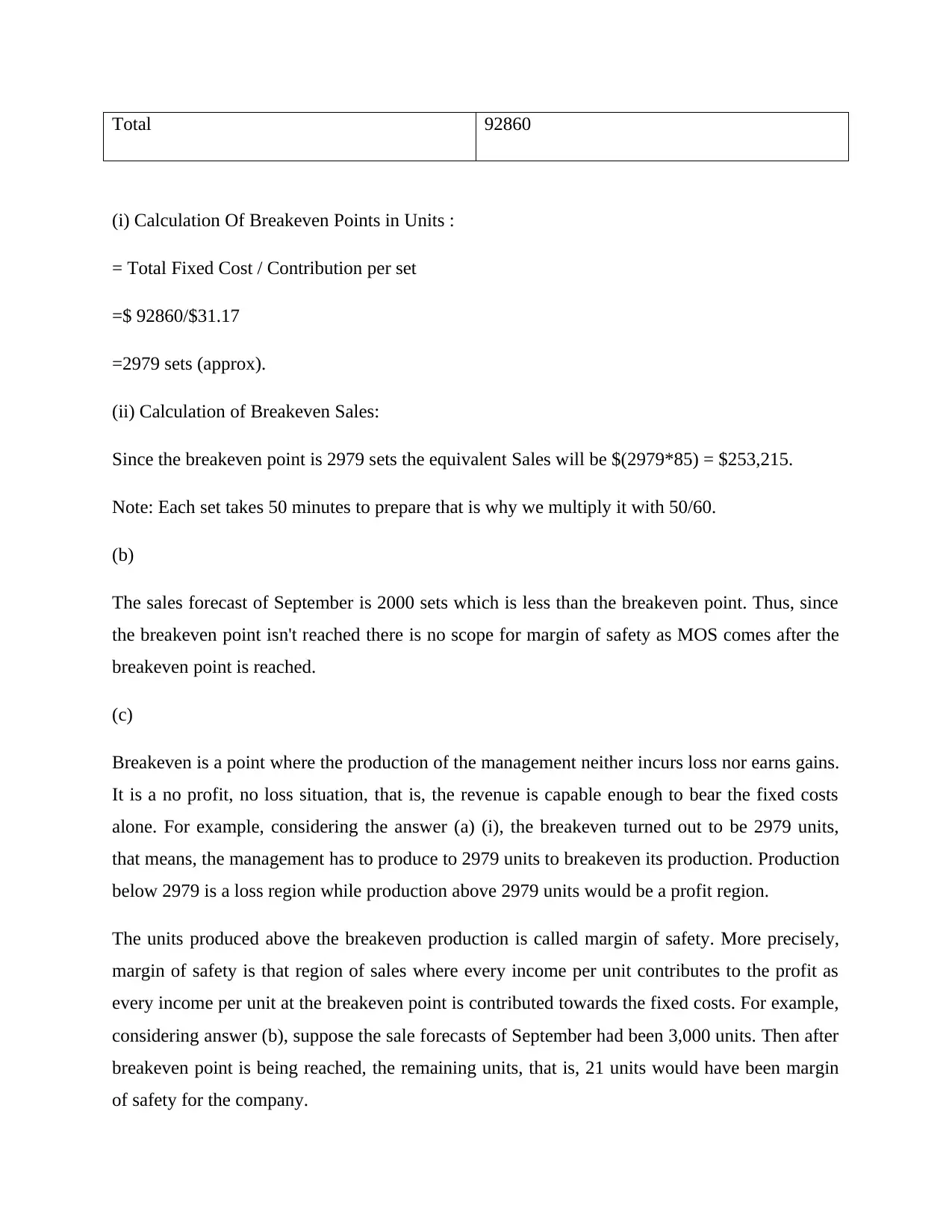

This assignment solution focuses on managerial accounting principles, specifically cost behavior and breakeven analysis. It classifies costs into fixed, variable, and mixed categories, providing detailed calculations and explanations for each. The solution includes determining the breakeven point in units and sales, and discusses the concept of margin of safety. The document also calculates total overhead cost and applied overhead cost based on machine hours. Desklib offers a wide range of academic resources, including past papers and solved assignments, to support students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.