ACC2350 Cost Accounting: Hummer Inc. Solved Assignment, S2 2018

VerifiedAdded on 2023/06/03

|13

|1145

|191

Homework Assignment

AI Summary

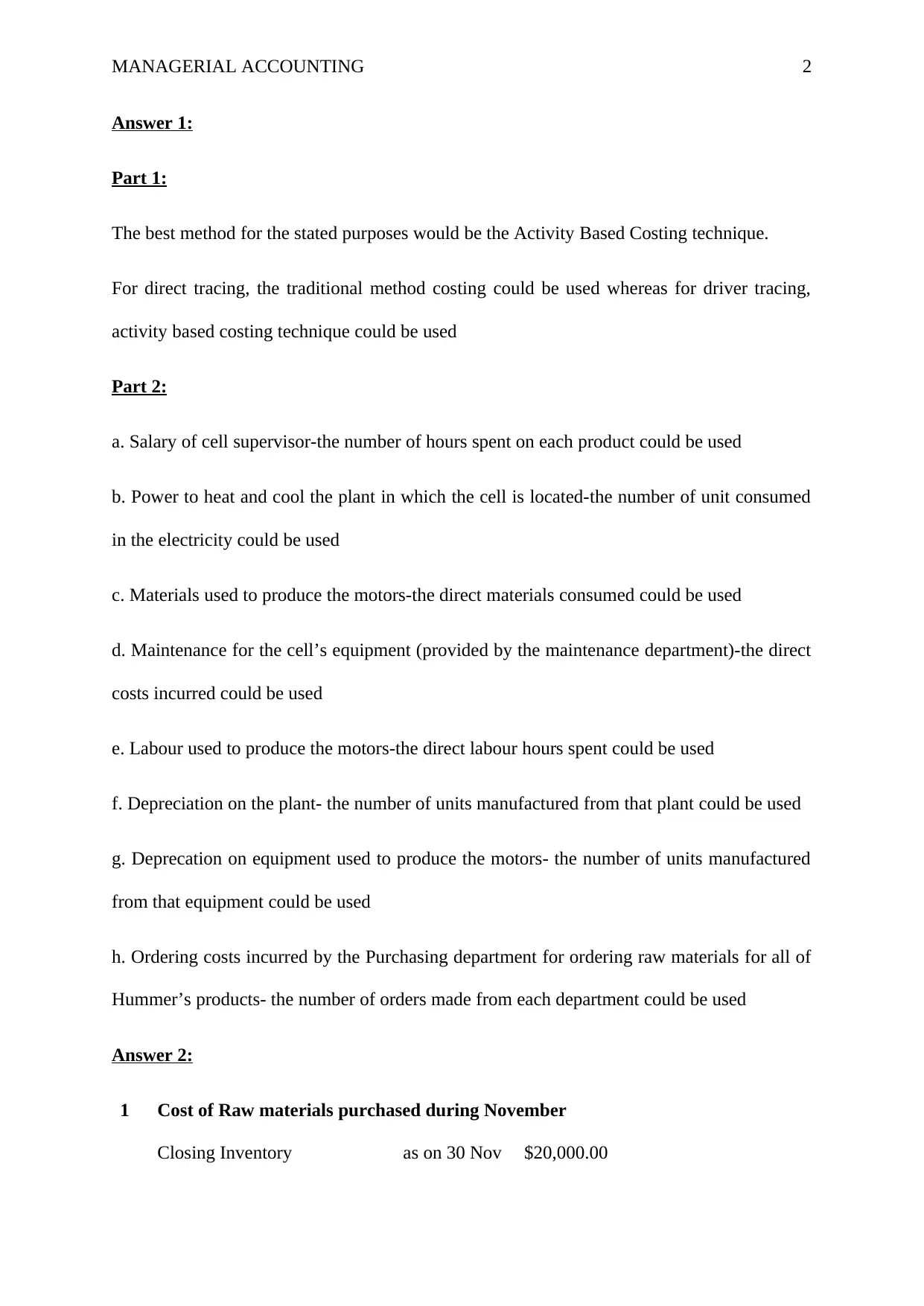

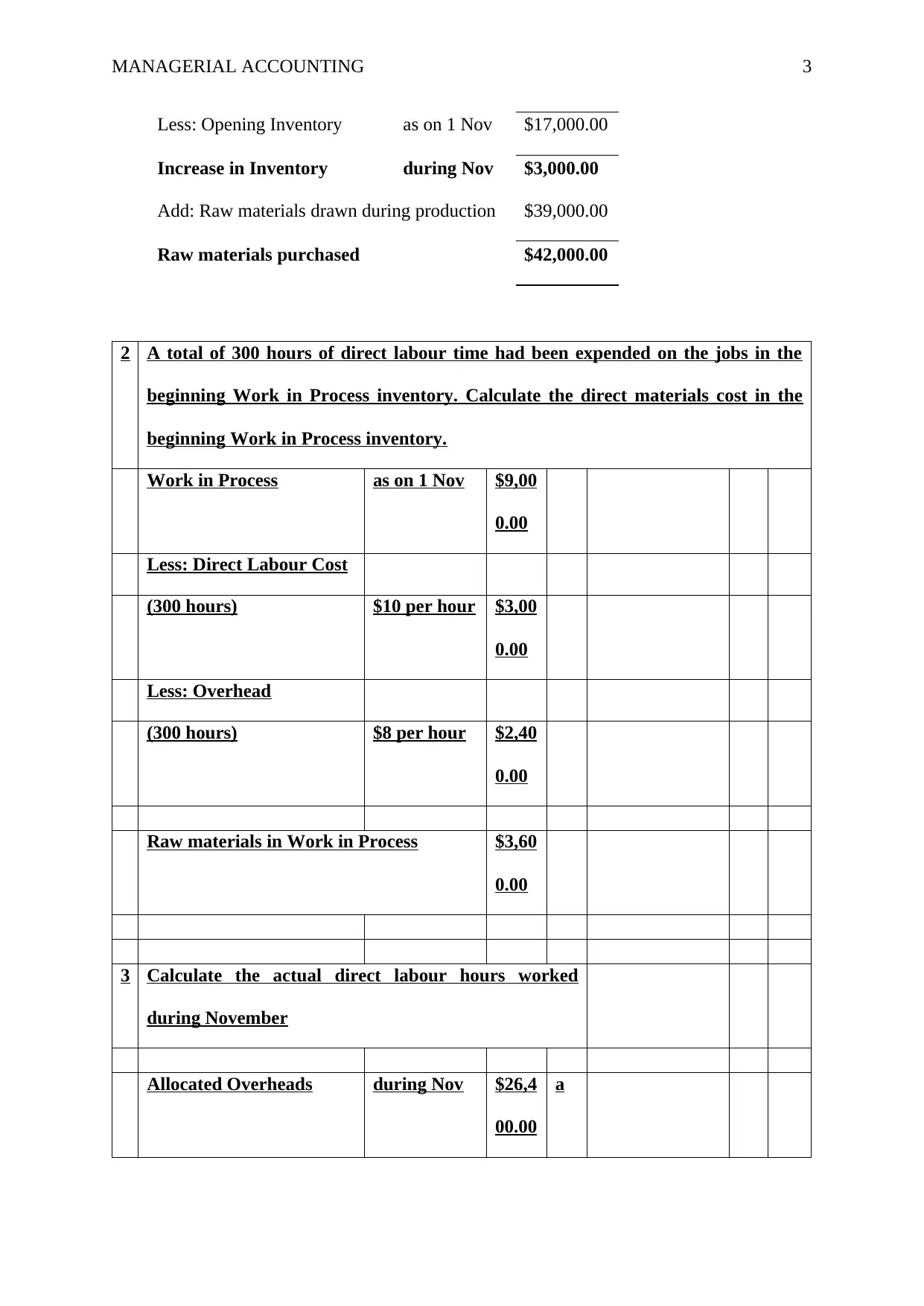

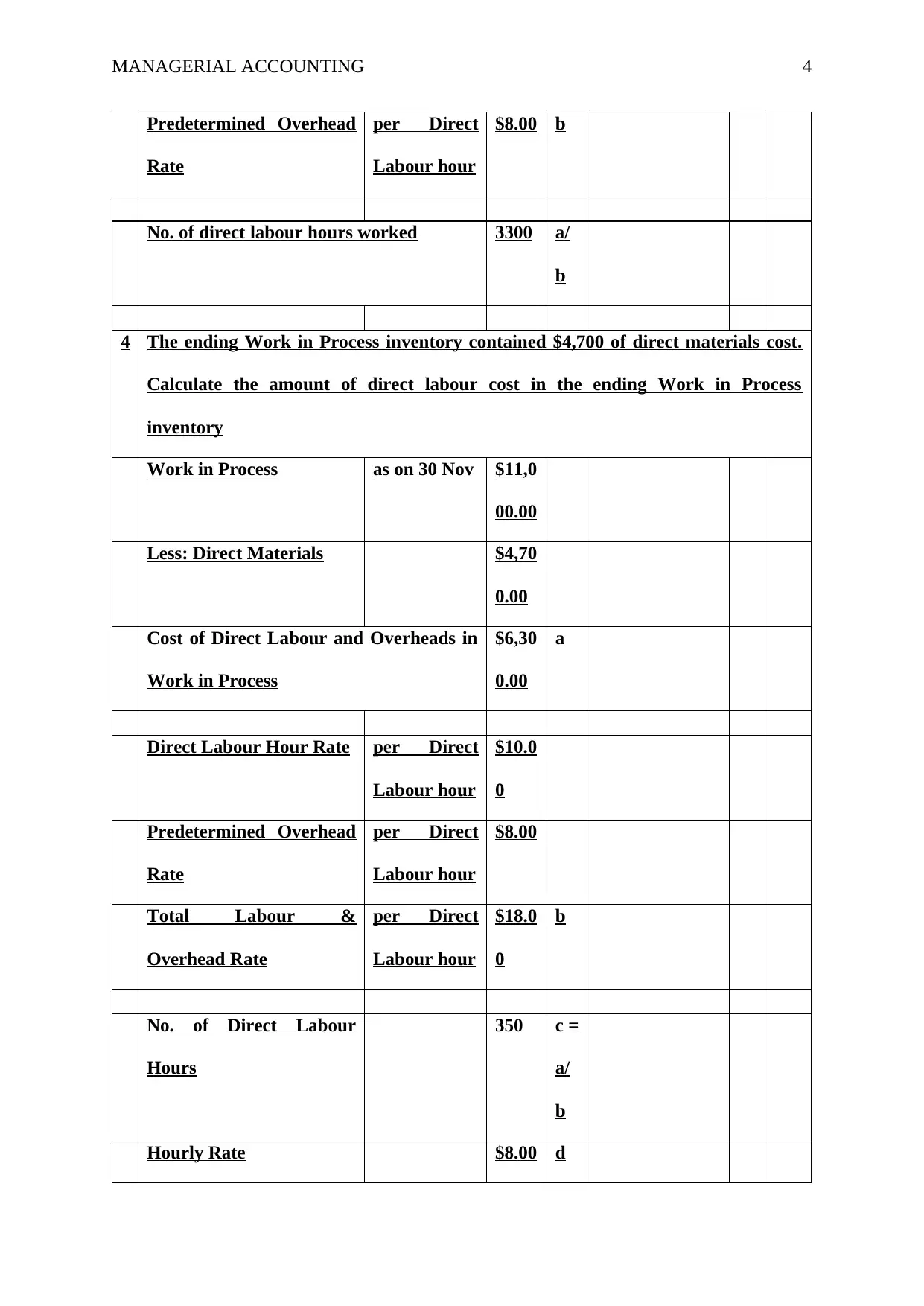

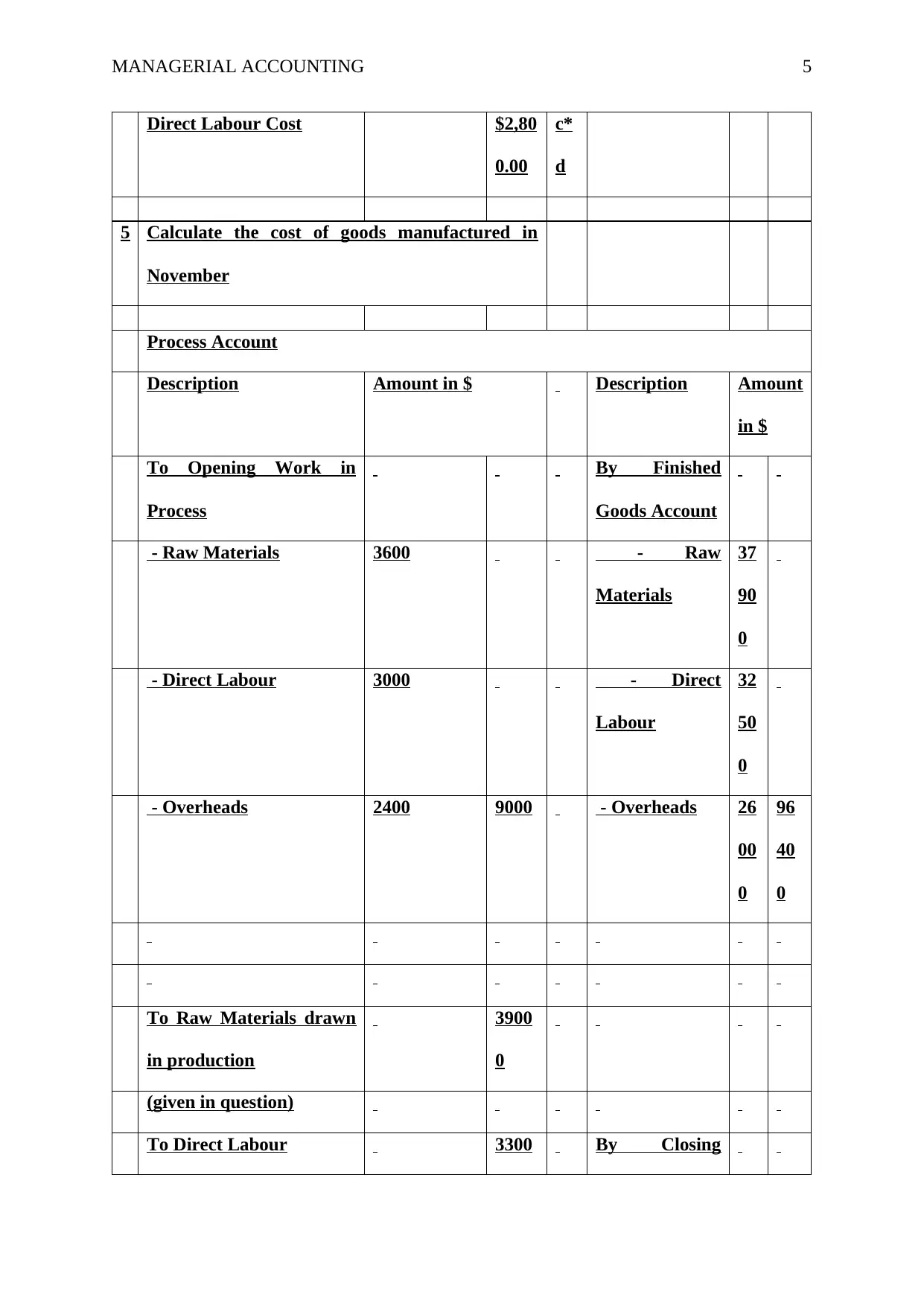

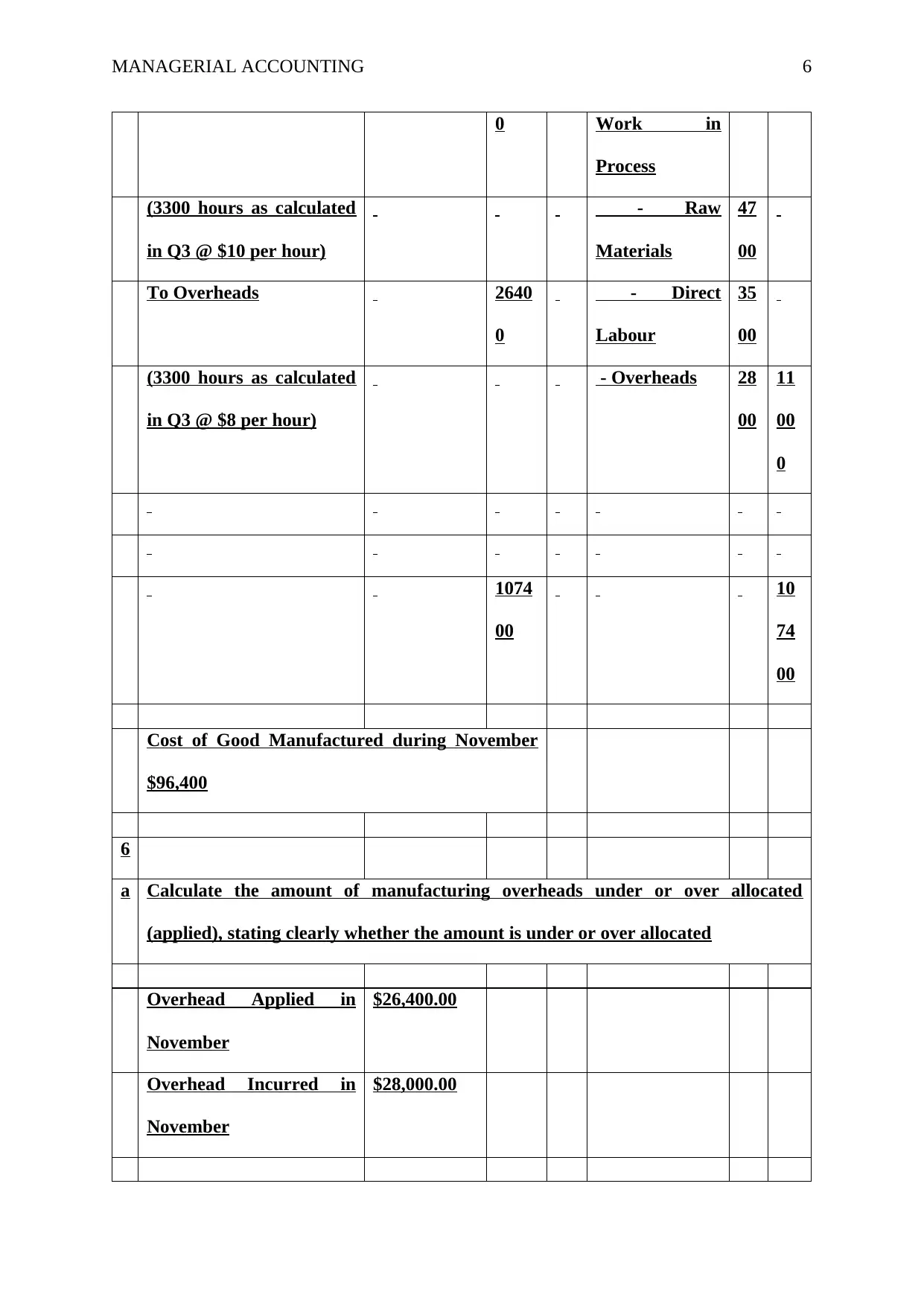

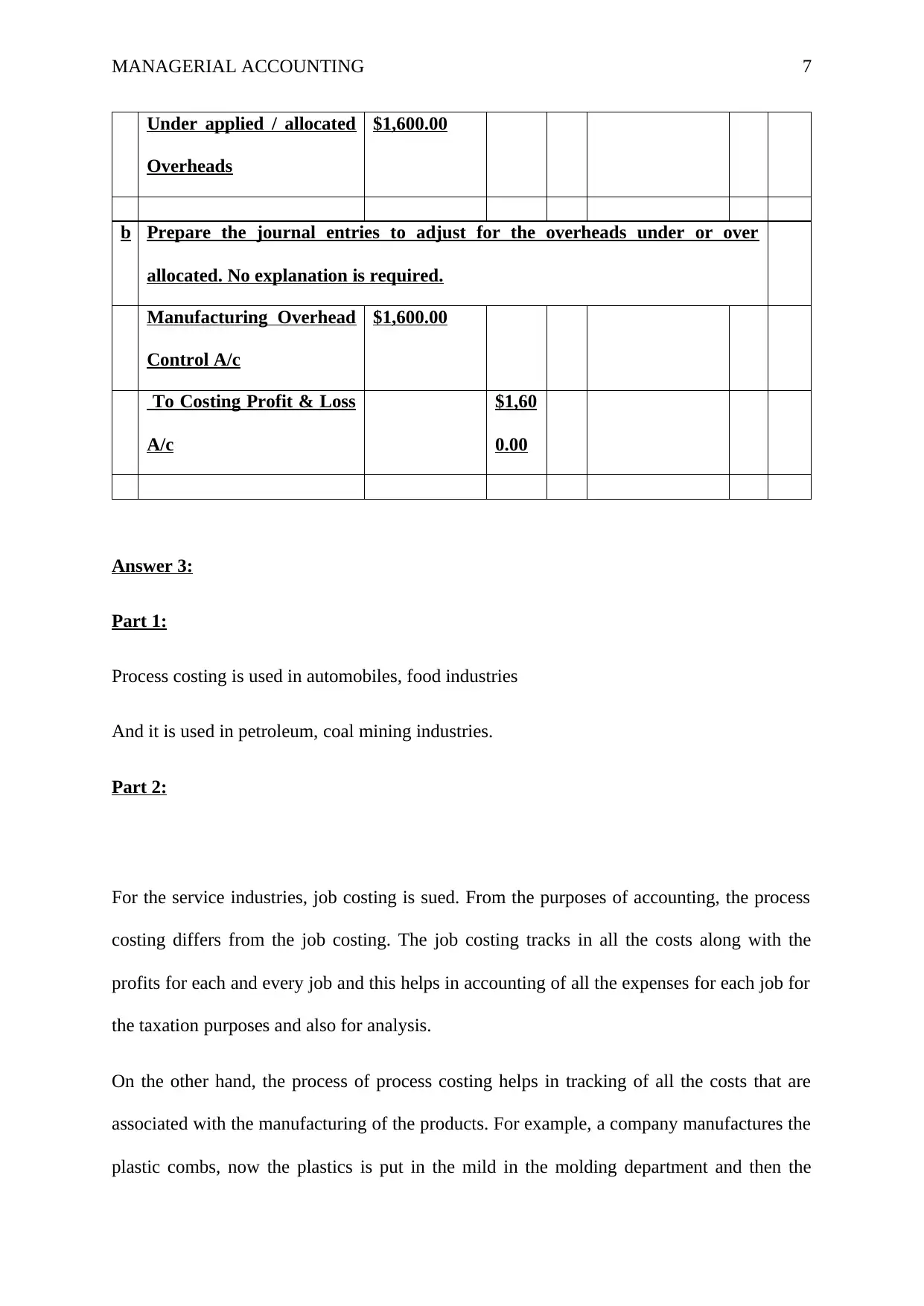

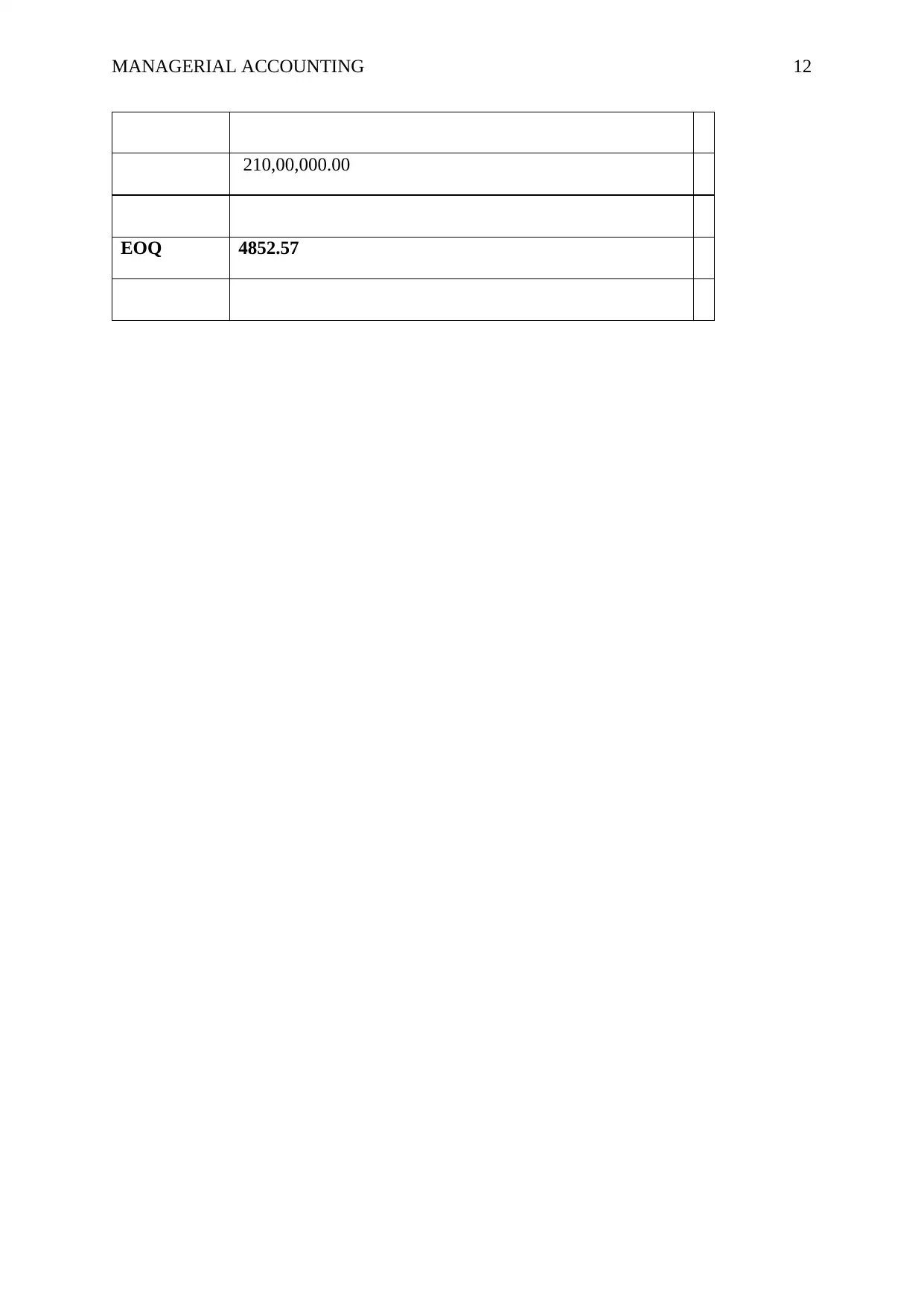

This assignment solution covers key concepts in managerial accounting, including activity-based costing, process costing, and job costing. It addresses questions related to cost assignment within a manufacturing cell, specifically focusing on Hummer Inc. The solution includes calculations for raw material purchases, work-in-process inventory, direct labor hours, and cost of goods manufactured. It also analyzes overhead allocation and provides journal entries for adjustments. Further, it differentiates between process and job costing, highlighting their applications in various industries. The assignment also covers the allocation of service department costs to production departments and calculates economic order quantity (EOQ) for inventory management.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.