ACC2CRE Corporate Reporting Solutions

VerifiedAdded on 2019/11/20

|12

|2340

|218

Homework Assignment

AI Summary

This document provides solutions to two problems related to corporate reporting, specifically focusing on the differences between integrated and stand-alone reporting methods. Solution 1 critically analyzes the limitations of stand-alone reports in capturing social and environmental aspects of a company's performance, contrasting them with the advantages of integrated reporting. It uses Woolworths, an ASX-listed company, as a case study to illustrate the implementation of integrated reporting. Solution 2 presents adjustment entries, an income statement, a statement of changes in equity, and a statement of financial position for Roxy Limited, accompanied by notes to the accounts that detail the accounting policies and standards followed (AASB and IFRS). The solutions demonstrate a comprehensive understanding of accounting principles and their application in preparing financial statements.

Corporate Reporting (ACC2CRE)

Page 1 of 13

Page 1 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution 1:..................................................................................................................................3

Introduction............................................................................................................................3

Discussion...............................................................................................................................3

Stand-alone reports relevant to social and environmental activities are non-integrated....3

Role of integrated reporting by identifying the problems associated with tradition

financial reporting...............................................................................................................4

Company listed on the ASX and identifying whether the company prepare integrated

reporting or not...................................................................................................................4

Conclusion..............................................................................................................................5

Solution 2:..................................................................................................................................6

Notes to accounts.....................................................................................................................11

References................................................................................................................................13

Page 2 of 13

Solution 1:..................................................................................................................................3

Introduction............................................................................................................................3

Discussion...............................................................................................................................3

Stand-alone reports relevant to social and environmental activities are non-integrated....3

Role of integrated reporting by identifying the problems associated with tradition

financial reporting...............................................................................................................4

Company listed on the ASX and identifying whether the company prepare integrated

reporting or not...................................................................................................................4

Conclusion..............................................................................................................................5

Solution 2:..................................................................................................................................6

Notes to accounts.....................................................................................................................11

References................................................................................................................................13

Page 2 of 13

Solution 1:

Introduction

The business entities having subsidiaries often face complications in preparation of

financial statements. This is because of the fact that parent company and its subsidiaries are

distinct legal entities and thus have the responsibility of maintaining their individual

bookkeeping. In this context, the stand-alone statements developed by a parent company treat

each business entity separately and thus provide two ways of analyzing the financial

performance of an entity. However, the stand-alone reports are not able to evaluate the

integrated financial performance, strategy and potential value creation for stakeholders and

thus faced criticism. In this context, the present report critically discusses the role of

integrated reporting by identifying the issues faced in traditional financial reporting. Also, the

reports analyses the compliance of integrated reporting by the ASX listed entities through

selection of a business entity for the purpose.

Discussion

Stand-alone reports relevant to social and environmental activities are non-integrated

The IAS 27 standard of IFRS has outlined the accounting policies and products

regarding the development of separate financial statements. The stand-alone financial reports

are the financial statements developed by a parent company with joint control of its associates

or subsidiaries as per the IFRS standards (IAS 27 — Separate Financial Statements, 2011).

However, the stand-alone reports have faced the criticism of not adequately meeting the

quality of non-financial reporting of business entities. The business entities have the

obligations of not only meeting the shareholders needs but also of its overall community. The

major drawback of stand-alone reports in this regard is that provide non-integrated

information related to the social and environmental performance of a business entity and thus

not capable of disclosing all the relevant non-financial information to its stakeholders. As

such, the stand-alone reports are not able to adequately depict the business performance,

strategy and potential for value creation to all of its stakeholders. The sustainability reports

developed through the use of stand-alone methods lacks the qualitative aspects of

completeness, accuracy, reliability, relevancy and transparency.

Page 3 of 13

Introduction

The business entities having subsidiaries often face complications in preparation of

financial statements. This is because of the fact that parent company and its subsidiaries are

distinct legal entities and thus have the responsibility of maintaining their individual

bookkeeping. In this context, the stand-alone statements developed by a parent company treat

each business entity separately and thus provide two ways of analyzing the financial

performance of an entity. However, the stand-alone reports are not able to evaluate the

integrated financial performance, strategy and potential value creation for stakeholders and

thus faced criticism. In this context, the present report critically discusses the role of

integrated reporting by identifying the issues faced in traditional financial reporting. Also, the

reports analyses the compliance of integrated reporting by the ASX listed entities through

selection of a business entity for the purpose.

Discussion

Stand-alone reports relevant to social and environmental activities are non-integrated

The IAS 27 standard of IFRS has outlined the accounting policies and products

regarding the development of separate financial statements. The stand-alone financial reports

are the financial statements developed by a parent company with joint control of its associates

or subsidiaries as per the IFRS standards (IAS 27 — Separate Financial Statements, 2011).

However, the stand-alone reports have faced the criticism of not adequately meeting the

quality of non-financial reporting of business entities. The business entities have the

obligations of not only meeting the shareholders needs but also of its overall community. The

major drawback of stand-alone reports in this regard is that provide non-integrated

information related to the social and environmental performance of a business entity and thus

not capable of disclosing all the relevant non-financial information to its stakeholders. As

such, the stand-alone reports are not able to adequately depict the business performance,

strategy and potential for value creation to all of its stakeholders. The sustainability reports

developed through the use of stand-alone methods lacks the qualitative aspects of

completeness, accuracy, reliability, relevancy and transparency.

Page 3 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is due to the fact that social and environment reporting done by the business

entities through the use of stand-alone method does not follow the internationally accepted

guidelines for non-financial reporting. The stand-alone method of financial reporting

discloses the non-financial information in discrete sections thus making it difficult to be

understood by the end-users. Thus, it can be said that stand-alone reporting method has

largely failed in its purpose of providing useful non-financial information to its stakeholders.

In the light of above deficiencies present in the stand-alone reporting system, there exist a

high need for the firms to improve their quality of sustainability reporting through adopting

an improved method of non-financial reporting (Wild and van Staden, 2013).

Role of integrated reporting by identifying the problems associated with tradition

financial reporting

The business entities have adopted the method of integrated reporting for disclosing

the non-financial information to its different type of stakeholders in the recent years. This

was done mainly to overcome from the problem associated with traditional method of stand-

alone reporting. As per the International Integrated Reporting Council (IIRC), the main

objective of integrated reporting is to provide complete and reliable information about the

strategy, governance and performance of a business entity. The adoption of integrated

reporting framework within the business enterprises was largely emphasizes after the

occurrence of global financial crisis for meeting the varied needs and demands of all its

stakeholders. The method of integrated reporting overcomes the problems associated with

stand-alone reports prepared by businesses for disclosing their non-financial information by

making compliance to the social and environmental performance of different business units

of a parent company. The integrated reporting has enhanced the quality of non-financial

reporting of business entities by disclosing their initiatives and performance in relation to

environment and social activities (Bernardi, 2015).

The scope of integrated reporting extends beyond the non-financial reporting and is

largely sued by businesses during preparation of their financial reports. The integrated

method of reporting has stated the principle of consolidation for preparation of financial

statements of a business entity having different business units. The consolidated financial

statements developed through the use of integrated reporting framework presents the overall

business activities of a company under a single report. Thus, the integrated reporting

framework system helps in overcoming the potential problem of traditional method of

Page 4 of 13

entities through the use of stand-alone method does not follow the internationally accepted

guidelines for non-financial reporting. The stand-alone method of financial reporting

discloses the non-financial information in discrete sections thus making it difficult to be

understood by the end-users. Thus, it can be said that stand-alone reporting method has

largely failed in its purpose of providing useful non-financial information to its stakeholders.

In the light of above deficiencies present in the stand-alone reporting system, there exist a

high need for the firms to improve their quality of sustainability reporting through adopting

an improved method of non-financial reporting (Wild and van Staden, 2013).

Role of integrated reporting by identifying the problems associated with tradition

financial reporting

The business entities have adopted the method of integrated reporting for disclosing

the non-financial information to its different type of stakeholders in the recent years. This

was done mainly to overcome from the problem associated with traditional method of stand-

alone reporting. As per the International Integrated Reporting Council (IIRC), the main

objective of integrated reporting is to provide complete and reliable information about the

strategy, governance and performance of a business entity. The adoption of integrated

reporting framework within the business enterprises was largely emphasizes after the

occurrence of global financial crisis for meeting the varied needs and demands of all its

stakeholders. The method of integrated reporting overcomes the problems associated with

stand-alone reports prepared by businesses for disclosing their non-financial information by

making compliance to the social and environmental performance of different business units

of a parent company. The integrated reporting has enhanced the quality of non-financial

reporting of business entities by disclosing their initiatives and performance in relation to

environment and social activities (Bernardi, 2015).

The scope of integrated reporting extends beyond the non-financial reporting and is

largely sued by businesses during preparation of their financial reports. The integrated

method of reporting has stated the principle of consolidation for preparation of financial

statements of a business entity having different business units. The consolidated financial

statements developed through the use of integrated reporting framework presents the overall

business activities of a company under a single report. Thus, the integrated reporting

framework system helps in overcoming the potential problem of traditional method of

Page 4 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial reporting under which the financial performance of an entity is presented in discrete

sections (Wild and van Staden, 2013).

Company listed on the ASX and identifying whether the company prepare integrated

reporting or not

Woolworths, a retail giant of Australia listed on ASX, effectively complies with the

integrated reporting framework through developing and publishing its integrated reports as

per the IFRS standards. The company has maintained that the main objective of developing

integrated report is to create value for all its stakeholders by disclosing them all the relevant

financial and non-financial information. The integrated report depicts the overall performance

of the group by incorporating all the information related to its subsidiaries and associates. As

per the IIRC framework, the integrated report of the Woolworths has depicted the method

through which the Group creates value through effective use of six capitals that are, financial,

manufactured, intellectual, human, social and natural capital. The integrated report of the

Group has illustrated its business model for describing the process adopted by it for creating

sustainable value for its stakeholders through optimum utilization of resources available. In

addition to this, the integrated report of the Group also presents the consolidated statement of

financial position by integrating the financial results of all its subsidiaries into a single

economic entity (Woolworths Holdings Limited 2016 Integrated Report, 2016).

Conclusion

Thus, from the overall discussion helps in the report it can be inferred that integrated

method of reporting is much better system of presenting financial statements of business

entities having different operational units as compared to stand-alone reporting method. The

integrated reporting system helps in depicting an interconnection between the financial and

non-financial performance drivers of a business entity.

Page 5 of 13

sections (Wild and van Staden, 2013).

Company listed on the ASX and identifying whether the company prepare integrated

reporting or not

Woolworths, a retail giant of Australia listed on ASX, effectively complies with the

integrated reporting framework through developing and publishing its integrated reports as

per the IFRS standards. The company has maintained that the main objective of developing

integrated report is to create value for all its stakeholders by disclosing them all the relevant

financial and non-financial information. The integrated report depicts the overall performance

of the group by incorporating all the information related to its subsidiaries and associates. As

per the IIRC framework, the integrated report of the Woolworths has depicted the method

through which the Group creates value through effective use of six capitals that are, financial,

manufactured, intellectual, human, social and natural capital. The integrated report of the

Group has illustrated its business model for describing the process adopted by it for creating

sustainable value for its stakeholders through optimum utilization of resources available. In

addition to this, the integrated report of the Group also presents the consolidated statement of

financial position by integrating the financial results of all its subsidiaries into a single

economic entity (Woolworths Holdings Limited 2016 Integrated Report, 2016).

Conclusion

Thus, from the overall discussion helps in the report it can be inferred that integrated

method of reporting is much better system of presenting financial statements of business

entities having different operational units as compared to stand-alone reporting method. The

integrated reporting system helps in depicting an interconnection between the financial and

non-financial performance drivers of a business entity.

Page 5 of 13

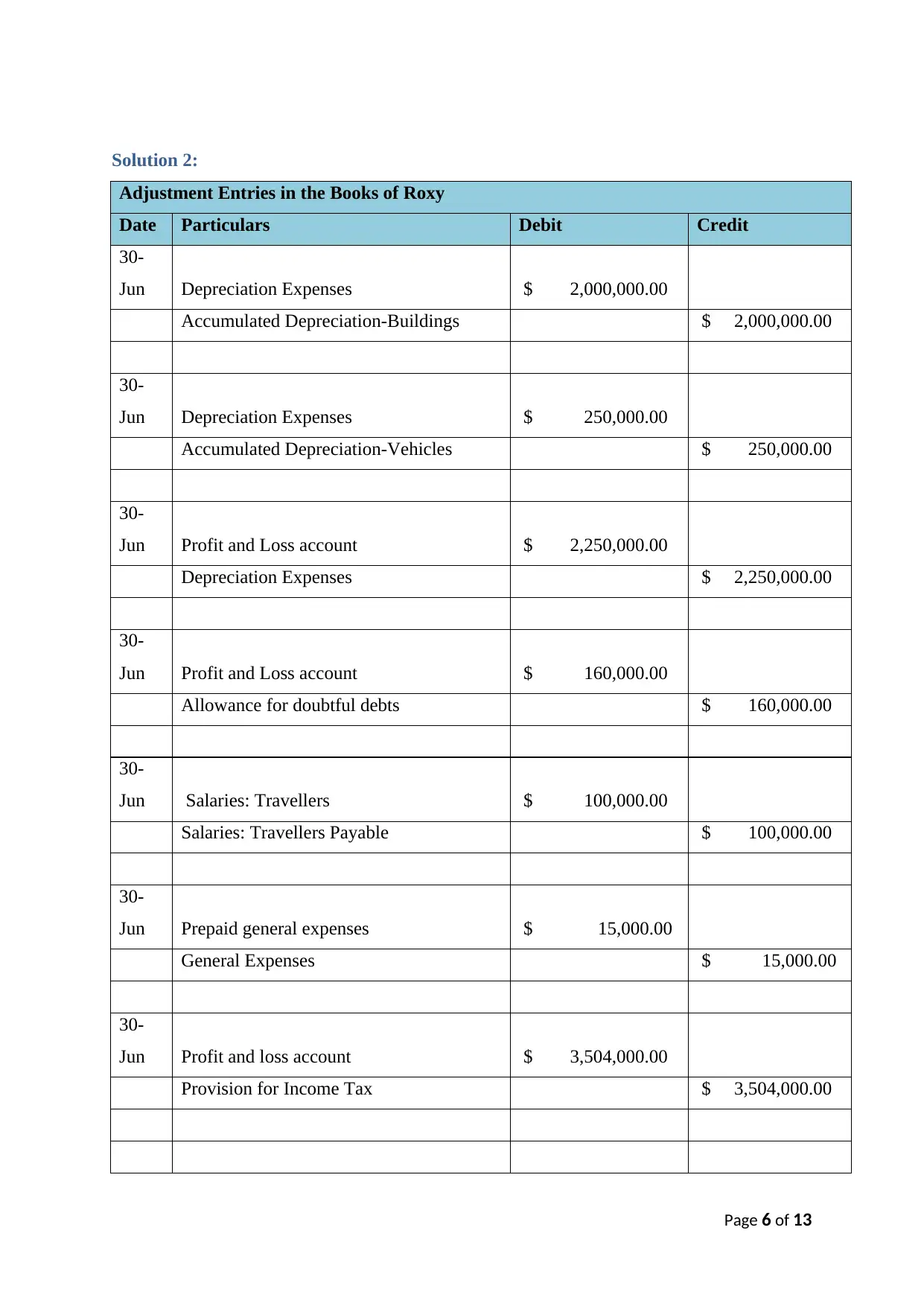

Solution 2:

Adjustment Entries in the Books of Roxy

Date Particulars Debit Credit

30-

Jun Depreciation Expenses $ 2,000,000.00

Accumulated Depreciation-Buildings $ 2,000,000.00

30-

Jun Depreciation Expenses $ 250,000.00

Accumulated Depreciation-Vehicles $ 250,000.00

30-

Jun Profit and Loss account $ 2,250,000.00

Depreciation Expenses $ 2,250,000.00

30-

Jun Profit and Loss account $ 160,000.00

Allowance for doubtful debts $ 160,000.00

30-

Jun Salaries: Travellers $ 100,000.00

Salaries: Travellers Payable $ 100,000.00

30-

Jun Prepaid general expenses $ 15,000.00

General Expenses $ 15,000.00

30-

Jun Profit and loss account $ 3,504,000.00

Provision for Income Tax $ 3,504,000.00

Page 6 of 13

Adjustment Entries in the Books of Roxy

Date Particulars Debit Credit

30-

Jun Depreciation Expenses $ 2,000,000.00

Accumulated Depreciation-Buildings $ 2,000,000.00

30-

Jun Depreciation Expenses $ 250,000.00

Accumulated Depreciation-Vehicles $ 250,000.00

30-

Jun Profit and Loss account $ 2,250,000.00

Depreciation Expenses $ 2,250,000.00

30-

Jun Profit and Loss account $ 160,000.00

Allowance for doubtful debts $ 160,000.00

30-

Jun Salaries: Travellers $ 100,000.00

Salaries: Travellers Payable $ 100,000.00

30-

Jun Prepaid general expenses $ 15,000.00

General Expenses $ 15,000.00

30-

Jun Profit and loss account $ 3,504,000.00

Provision for Income Tax $ 3,504,000.00

Page 6 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

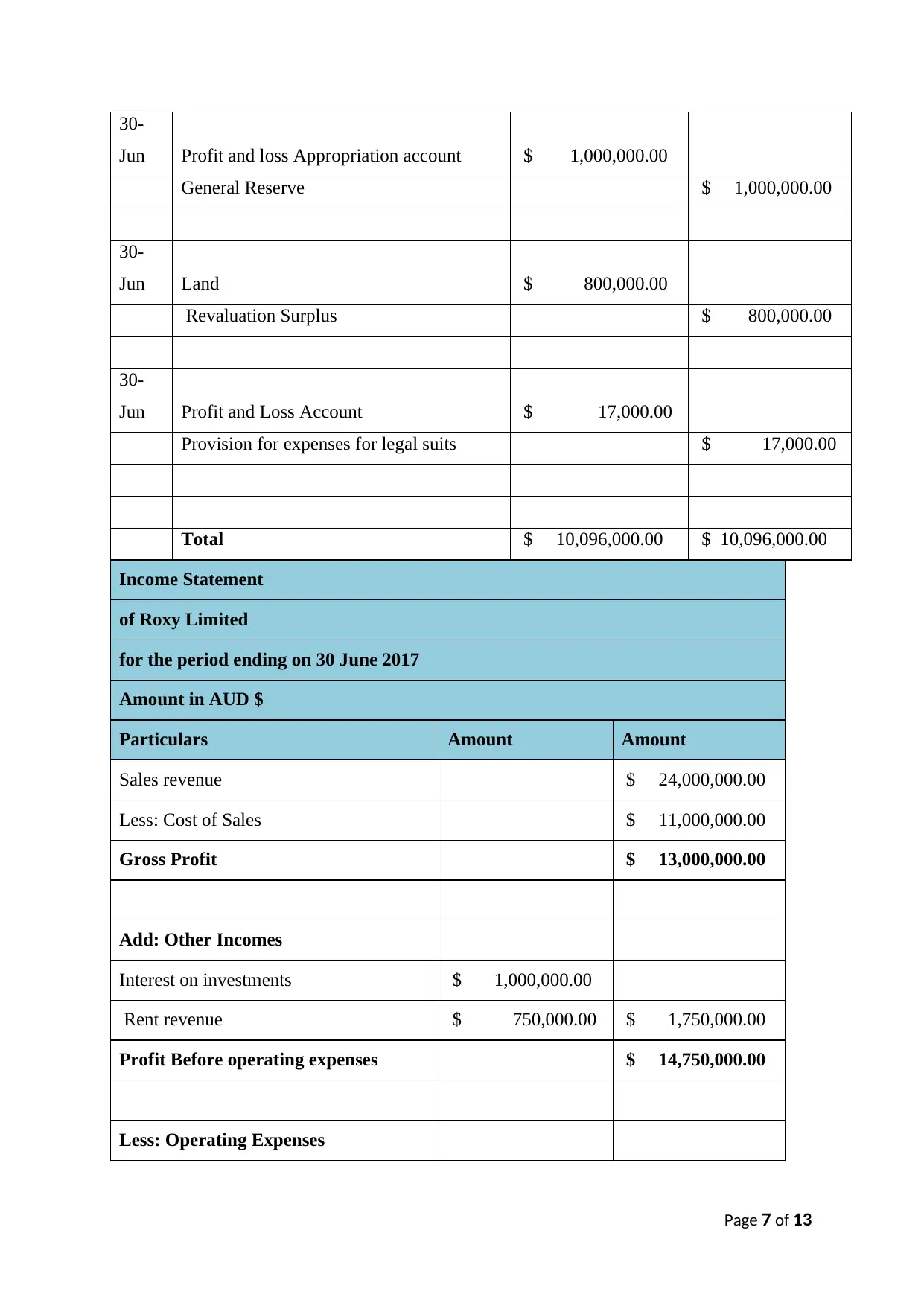

30-

Jun Profit and loss Appropriation account $ 1,000,000.00

General Reserve $ 1,000,000.00

30-

Jun Land $ 800,000.00

Revaluation Surplus $ 800,000.00

30-

Jun Profit and Loss Account $ 17,000.00

Provision for expenses for legal suits $ 17,000.00

Total $ 10,096,000.00 $ 10,096,000.00

Income Statement

of Roxy Limited

for the period ending on 30 June 2017

Amount in AUD $

Particulars Amount Amount

Sales revenue $ 24,000,000.00

Less: Cost of Sales $ 11,000,000.00

Gross Profit $ 13,000,000.00

Add: Other Incomes

Interest on investments $ 1,000,000.00

Rent revenue $ 750,000.00 $ 1,750,000.00

Profit Before operating expenses $ 14,750,000.00

Less: Operating Expenses

Page 7 of 13

Jun Profit and loss Appropriation account $ 1,000,000.00

General Reserve $ 1,000,000.00

30-

Jun Land $ 800,000.00

Revaluation Surplus $ 800,000.00

30-

Jun Profit and Loss Account $ 17,000.00

Provision for expenses for legal suits $ 17,000.00

Total $ 10,096,000.00 $ 10,096,000.00

Income Statement

of Roxy Limited

for the period ending on 30 June 2017

Amount in AUD $

Particulars Amount Amount

Sales revenue $ 24,000,000.00

Less: Cost of Sales $ 11,000,000.00

Gross Profit $ 13,000,000.00

Add: Other Incomes

Interest on investments $ 1,000,000.00

Rent revenue $ 750,000.00 $ 1,750,000.00

Profit Before operating expenses $ 14,750,000.00

Less: Operating Expenses

Page 7 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling Commission expense $ 100,000.00

Delivery expense $ 200,000.00

Salaries: Travellers $ 550,000.00

Salaries: Administration $ 2,000,000.00

Directors fees $ 200,000.00

Depreciation $ 2,250,000.00

Allowance for doubtful debts $ 160,000.00

Audit fees $ 90,000.00

Interest on mortgage $ 1,000,000.00

Provision for expenses for legal suits $ 17,000.00

Provision for Income tax $ 3,504,000.00

Damage due to fire $ 150,000.00

General expenses $ 1,450,000.00 $ 11,671,000.00

Net Profit $ 3,079,000.00

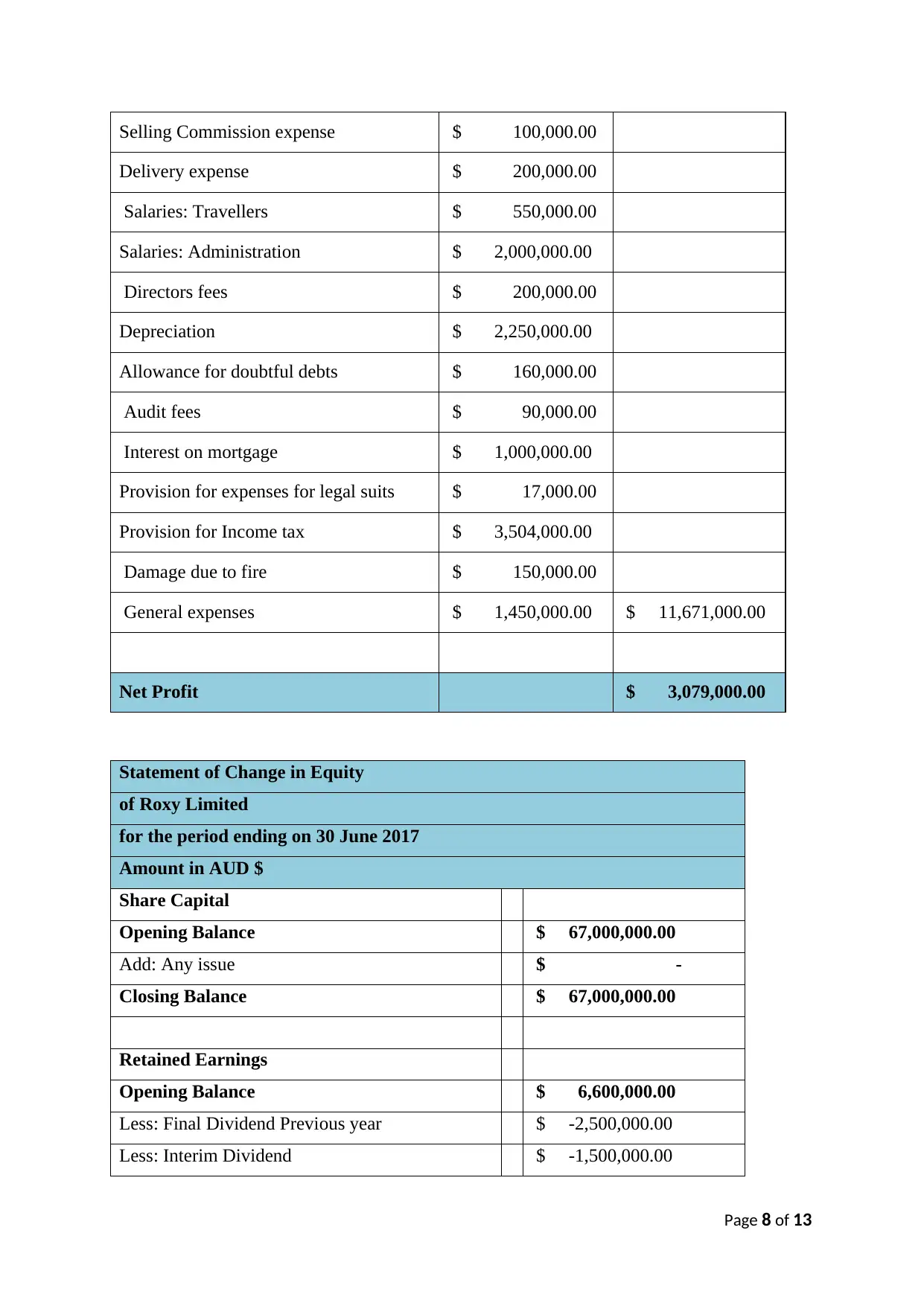

Statement of Change in Equity

of Roxy Limited

for the period ending on 30 June 2017

Amount in AUD $

Share Capital

Opening Balance $ 67,000,000.00

Add: Any issue $ -

Closing Balance $ 67,000,000.00

Retained Earnings

Opening Balance $ 6,600,000.00

Less: Final Dividend Previous year $ -2,500,000.00

Less: Interim Dividend $ -1,500,000.00

Page 8 of 13

Delivery expense $ 200,000.00

Salaries: Travellers $ 550,000.00

Salaries: Administration $ 2,000,000.00

Directors fees $ 200,000.00

Depreciation $ 2,250,000.00

Allowance for doubtful debts $ 160,000.00

Audit fees $ 90,000.00

Interest on mortgage $ 1,000,000.00

Provision for expenses for legal suits $ 17,000.00

Provision for Income tax $ 3,504,000.00

Damage due to fire $ 150,000.00

General expenses $ 1,450,000.00 $ 11,671,000.00

Net Profit $ 3,079,000.00

Statement of Change in Equity

of Roxy Limited

for the period ending on 30 June 2017

Amount in AUD $

Share Capital

Opening Balance $ 67,000,000.00

Add: Any issue $ -

Closing Balance $ 67,000,000.00

Retained Earnings

Opening Balance $ 6,600,000.00

Less: Final Dividend Previous year $ -2,500,000.00

Less: Interim Dividend $ -1,500,000.00

Page 8 of 13

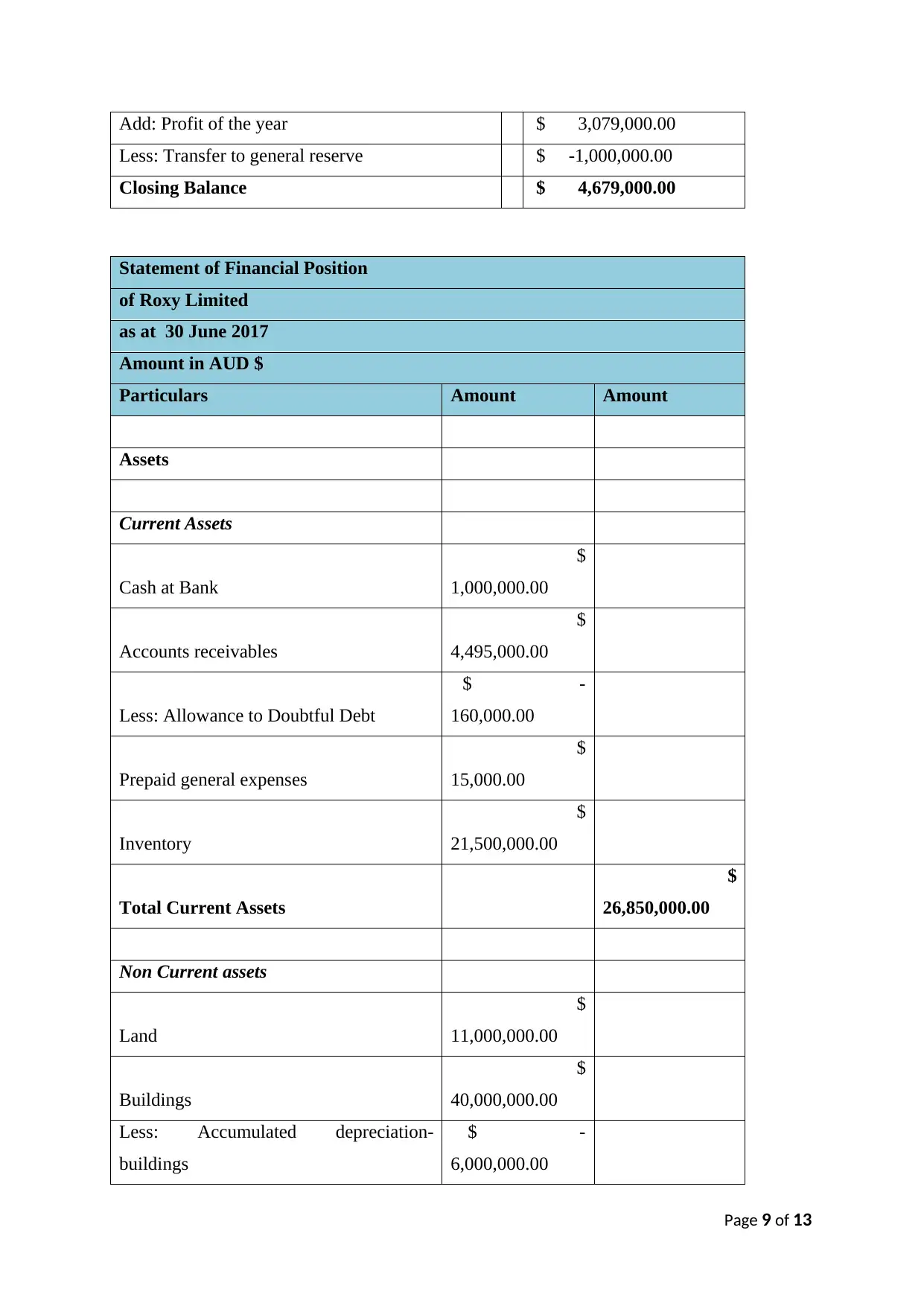

Add: Profit of the year $ 3,079,000.00

Less: Transfer to general reserve $ -1,000,000.00

Closing Balance $ 4,679,000.00

Statement of Financial Position

of Roxy Limited

as at 30 June 2017

Amount in AUD $

Particulars Amount Amount

Assets

Current Assets

Cash at Bank

$

1,000,000.00

Accounts receivables

$

4,495,000.00

Less: Allowance to Doubtful Debt

$ -

160,000.00

Prepaid general expenses

$

15,000.00

Inventory

$

21,500,000.00

Total Current Assets

$

26,850,000.00

Non Current assets

Land

$

11,000,000.00

Buildings

$

40,000,000.00

Less: Accumulated depreciation-

buildings

$ -

6,000,000.00

Page 9 of 13

Less: Transfer to general reserve $ -1,000,000.00

Closing Balance $ 4,679,000.00

Statement of Financial Position

of Roxy Limited

as at 30 June 2017

Amount in AUD $

Particulars Amount Amount

Assets

Current Assets

Cash at Bank

$

1,000,000.00

Accounts receivables

$

4,495,000.00

Less: Allowance to Doubtful Debt

$ -

160,000.00

Prepaid general expenses

$

15,000.00

Inventory

$

21,500,000.00

Total Current Assets

$

26,850,000.00

Non Current assets

Land

$

11,000,000.00

Buildings

$

40,000,000.00

Less: Accumulated depreciation-

buildings

$ -

6,000,000.00

Page 9 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

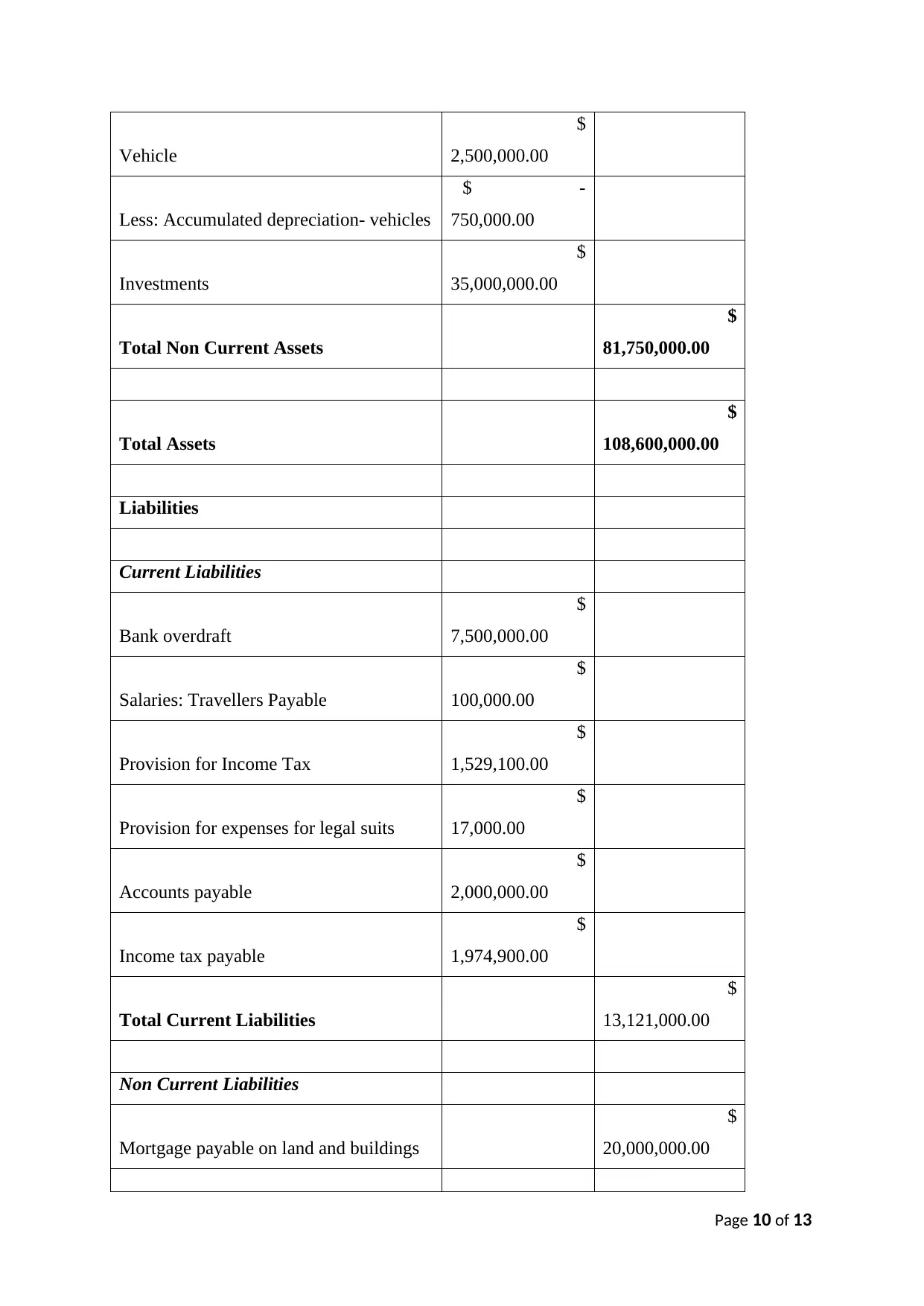

Vehicle

$

2,500,000.00

Less: Accumulated depreciation- vehicles

$ -

750,000.00

Investments

$

35,000,000.00

Total Non Current Assets

$

81,750,000.00

Total Assets

$

108,600,000.00

Liabilities

Current Liabilities

Bank overdraft

$

7,500,000.00

Salaries: Travellers Payable

$

100,000.00

Provision for Income Tax

$

1,529,100.00

Provision for expenses for legal suits

$

17,000.00

Accounts payable

$

2,000,000.00

Income tax payable

$

1,974,900.00

Total Current Liabilities

$

13,121,000.00

Non Current Liabilities

Mortgage payable on land and buildings

$

20,000,000.00

Page 10 of 13

$

2,500,000.00

Less: Accumulated depreciation- vehicles

$ -

750,000.00

Investments

$

35,000,000.00

Total Non Current Assets

$

81,750,000.00

Total Assets

$

108,600,000.00

Liabilities

Current Liabilities

Bank overdraft

$

7,500,000.00

Salaries: Travellers Payable

$

100,000.00

Provision for Income Tax

$

1,529,100.00

Provision for expenses for legal suits

$

17,000.00

Accounts payable

$

2,000,000.00

Income tax payable

$

1,974,900.00

Total Current Liabilities

$

13,121,000.00

Non Current Liabilities

Mortgage payable on land and buildings

$

20,000,000.00

Page 10 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

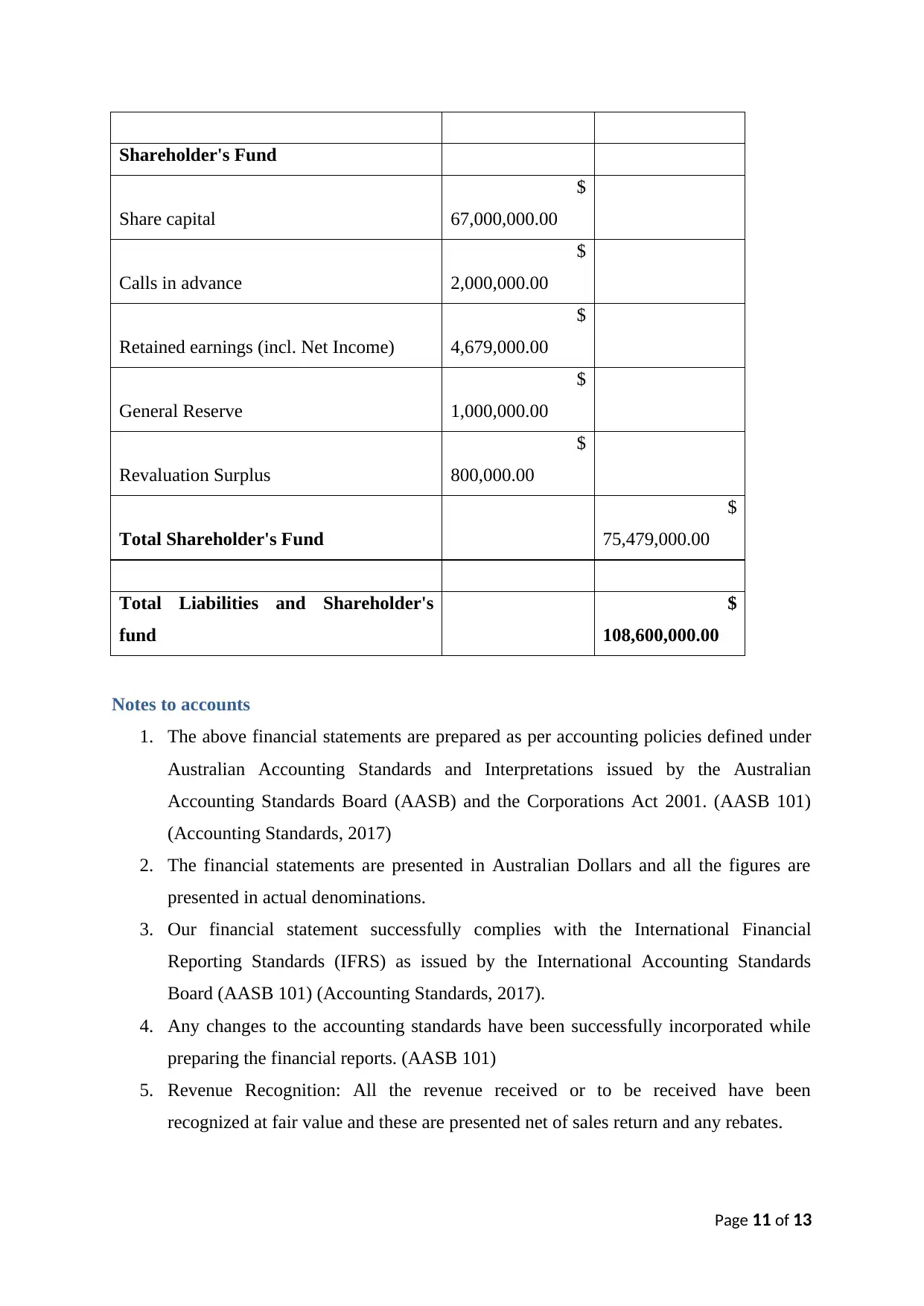

Shareholder's Fund

Share capital

$

67,000,000.00

Calls in advance

$

2,000,000.00

Retained earnings (incl. Net Income)

$

4,679,000.00

General Reserve

$

1,000,000.00

Revaluation Surplus

$

800,000.00

Total Shareholder's Fund

$

75,479,000.00

Total Liabilities and Shareholder's

fund

$

108,600,000.00

Notes to accounts

1. The above financial statements are prepared as per accounting policies defined under

Australian Accounting Standards and Interpretations issued by the Australian

Accounting Standards Board (AASB) and the Corporations Act 2001. (AASB 101)

(Accounting Standards, 2017)

2. The financial statements are presented in Australian Dollars and all the figures are

presented in actual denominations.

3. Our financial statement successfully complies with the International Financial

Reporting Standards (IFRS) as issued by the International Accounting Standards

Board (AASB 101) (Accounting Standards, 2017).

4. Any changes to the accounting standards have been successfully incorporated while

preparing the financial reports. (AASB 101)

5. Revenue Recognition: All the revenue received or to be received have been

recognized at fair value and these are presented net of sales return and any rebates.

Page 11 of 13

Share capital

$

67,000,000.00

Calls in advance

$

2,000,000.00

Retained earnings (incl. Net Income)

$

4,679,000.00

General Reserve

$

1,000,000.00

Revaluation Surplus

$

800,000.00

Total Shareholder's Fund

$

75,479,000.00

Total Liabilities and Shareholder's

fund

$

108,600,000.00

Notes to accounts

1. The above financial statements are prepared as per accounting policies defined under

Australian Accounting Standards and Interpretations issued by the Australian

Accounting Standards Board (AASB) and the Corporations Act 2001. (AASB 101)

(Accounting Standards, 2017)

2. The financial statements are presented in Australian Dollars and all the figures are

presented in actual denominations.

3. Our financial statement successfully complies with the International Financial

Reporting Standards (IFRS) as issued by the International Accounting Standards

Board (AASB 101) (Accounting Standards, 2017).

4. Any changes to the accounting standards have been successfully incorporated while

preparing the financial reports. (AASB 101)

5. Revenue Recognition: All the revenue received or to be received have been

recognized at fair value and these are presented net of sales return and any rebates.

Page 11 of 13

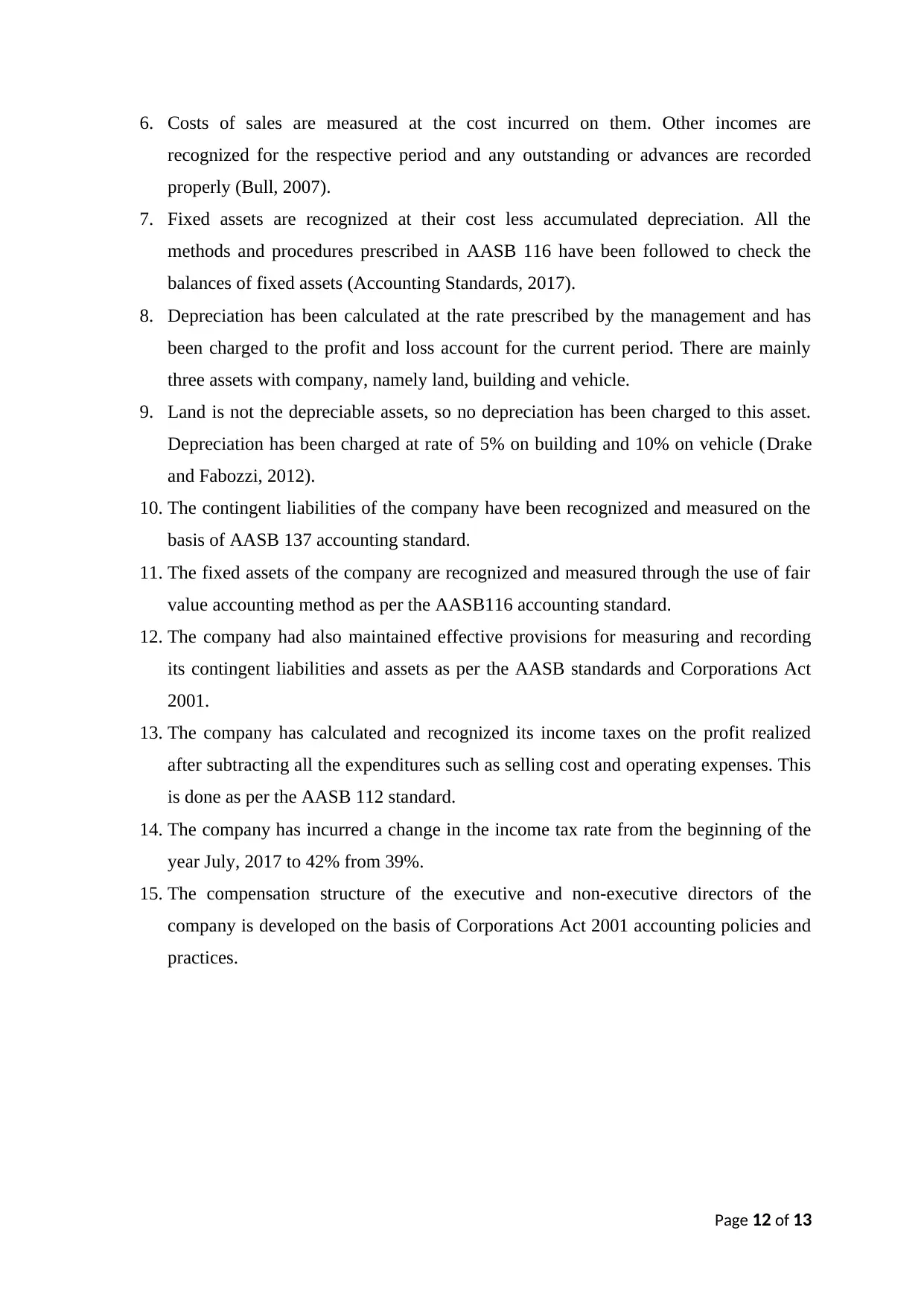

6. Costs of sales are measured at the cost incurred on them. Other incomes are

recognized for the respective period and any outstanding or advances are recorded

properly (Bull, 2007).

7. Fixed assets are recognized at their cost less accumulated depreciation. All the

methods and procedures prescribed in AASB 116 have been followed to check the

balances of fixed assets (Accounting Standards, 2017).

8. Depreciation has been calculated at the rate prescribed by the management and has

been charged to the profit and loss account for the current period. There are mainly

three assets with company, namely land, building and vehicle.

9. Land is not the depreciable assets, so no depreciation has been charged to this asset.

Depreciation has been charged at rate of 5% on building and 10% on vehicle (Drake

and Fabozzi, 2012).

10. The contingent liabilities of the company have been recognized and measured on the

basis of AASB 137 accounting standard.

11. The fixed assets of the company are recognized and measured through the use of fair

value accounting method as per the AASB116 accounting standard.

12. The company had also maintained effective provisions for measuring and recording

its contingent liabilities and assets as per the AASB standards and Corporations Act

2001.

13. The company has calculated and recognized its income taxes on the profit realized

after subtracting all the expenditures such as selling cost and operating expenses. This

is done as per the AASB 112 standard.

14. The company has incurred a change in the income tax rate from the beginning of the

year July, 2017 to 42% from 39%.

15. The compensation structure of the executive and non-executive directors of the

company is developed on the basis of Corporations Act 2001 accounting policies and

practices.

Page 12 of 13

recognized for the respective period and any outstanding or advances are recorded

properly (Bull, 2007).

7. Fixed assets are recognized at their cost less accumulated depreciation. All the

methods and procedures prescribed in AASB 116 have been followed to check the

balances of fixed assets (Accounting Standards, 2017).

8. Depreciation has been calculated at the rate prescribed by the management and has

been charged to the profit and loss account for the current period. There are mainly

three assets with company, namely land, building and vehicle.

9. Land is not the depreciable assets, so no depreciation has been charged to this asset.

Depreciation has been charged at rate of 5% on building and 10% on vehicle (Drake

and Fabozzi, 2012).

10. The contingent liabilities of the company have been recognized and measured on the

basis of AASB 137 accounting standard.

11. The fixed assets of the company are recognized and measured through the use of fair

value accounting method as per the AASB116 accounting standard.

12. The company had also maintained effective provisions for measuring and recording

its contingent liabilities and assets as per the AASB standards and Corporations Act

2001.

13. The company has calculated and recognized its income taxes on the profit realized

after subtracting all the expenditures such as selling cost and operating expenses. This

is done as per the AASB 112 standard.

14. The company has incurred a change in the income tax rate from the beginning of the

year July, 2017 to 42% from 39%.

15. The compensation structure of the executive and non-executive directors of the

company is developed on the basis of Corporations Act 2001 accounting policies and

practices.

Page 12 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.