ACC3005 Tax Law Assignment: Trading Stock and Tax Implications

VerifiedAdded on 2020/03/16

|7

|1363

|163

Homework Assignment

AI Summary

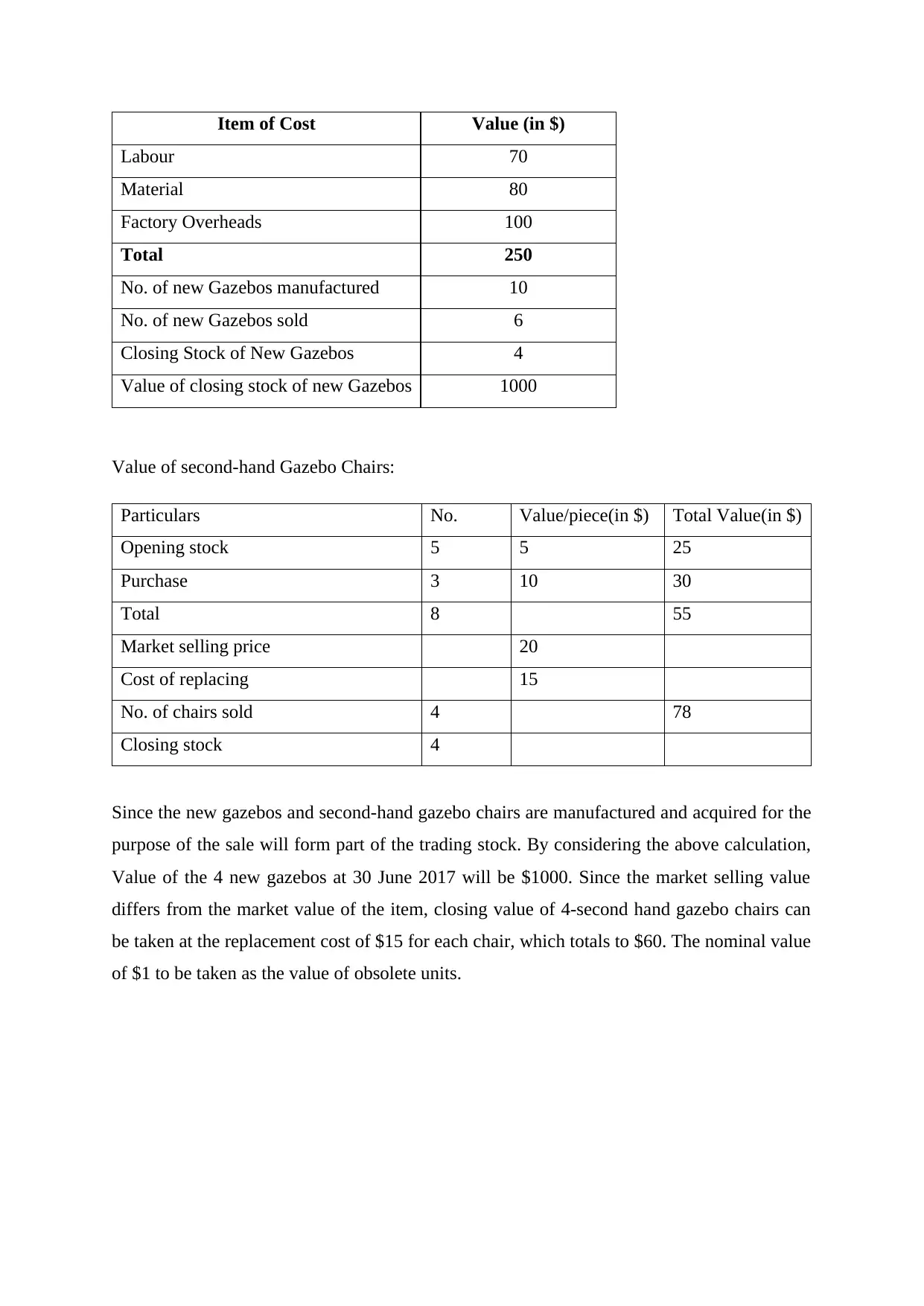

This document presents a comprehensive solution to an ACC3005 Tax Law assignment. The assignment addresses the accounting and tax implications of trading stock, using case studies involving the sale of gazebos and computer spare parts. The analysis covers key issues such as the valuation of trading stock (including new and second-hand items), the treatment of obsolete stock, and the assessability of such stock under Australian tax law. The solution examines the application of relevant sections of the Income Tax Assessment Act 1997, including the definition and valuation of trading stock. Detailed calculations are provided to determine the value of closing stock, considering factors like cost, market selling price, and replacement cost. Furthermore, the assignment explores the tax implications of computer spare parts, considering scenarios involving direct sales, repairs, maintenance agreements, and computer leasing. The solution clarifies whether spare parts are considered trading stock under various circumstances, referencing relevant tax rulings. The document provides a strong foundation for understanding the nuances of trading stock valuation and its tax implications.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.