Accounting and Finance for Managers: Aviation Case Study

VerifiedAdded on 2023/01/10

|27

|4544

|82

Case Study

AI Summary

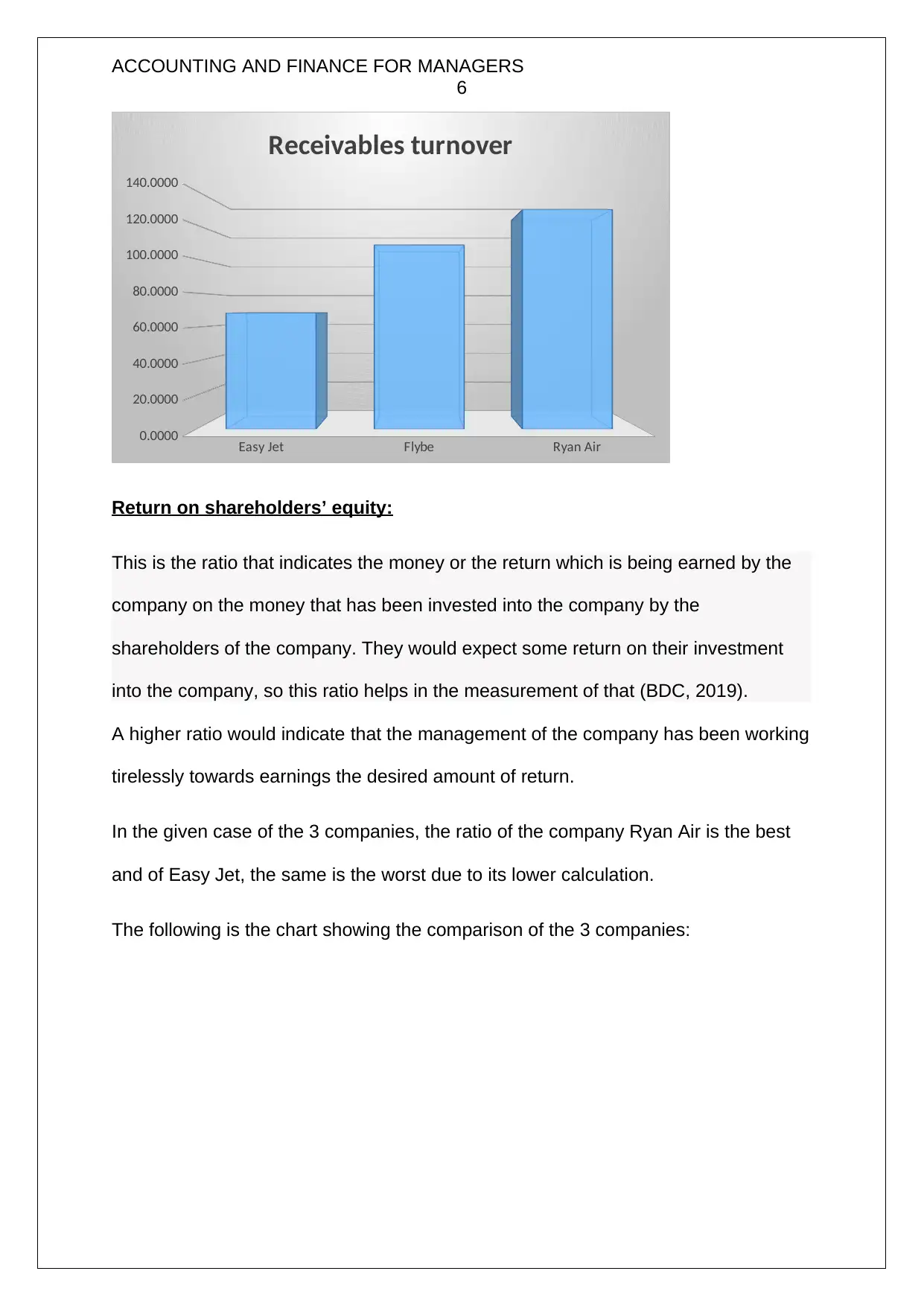

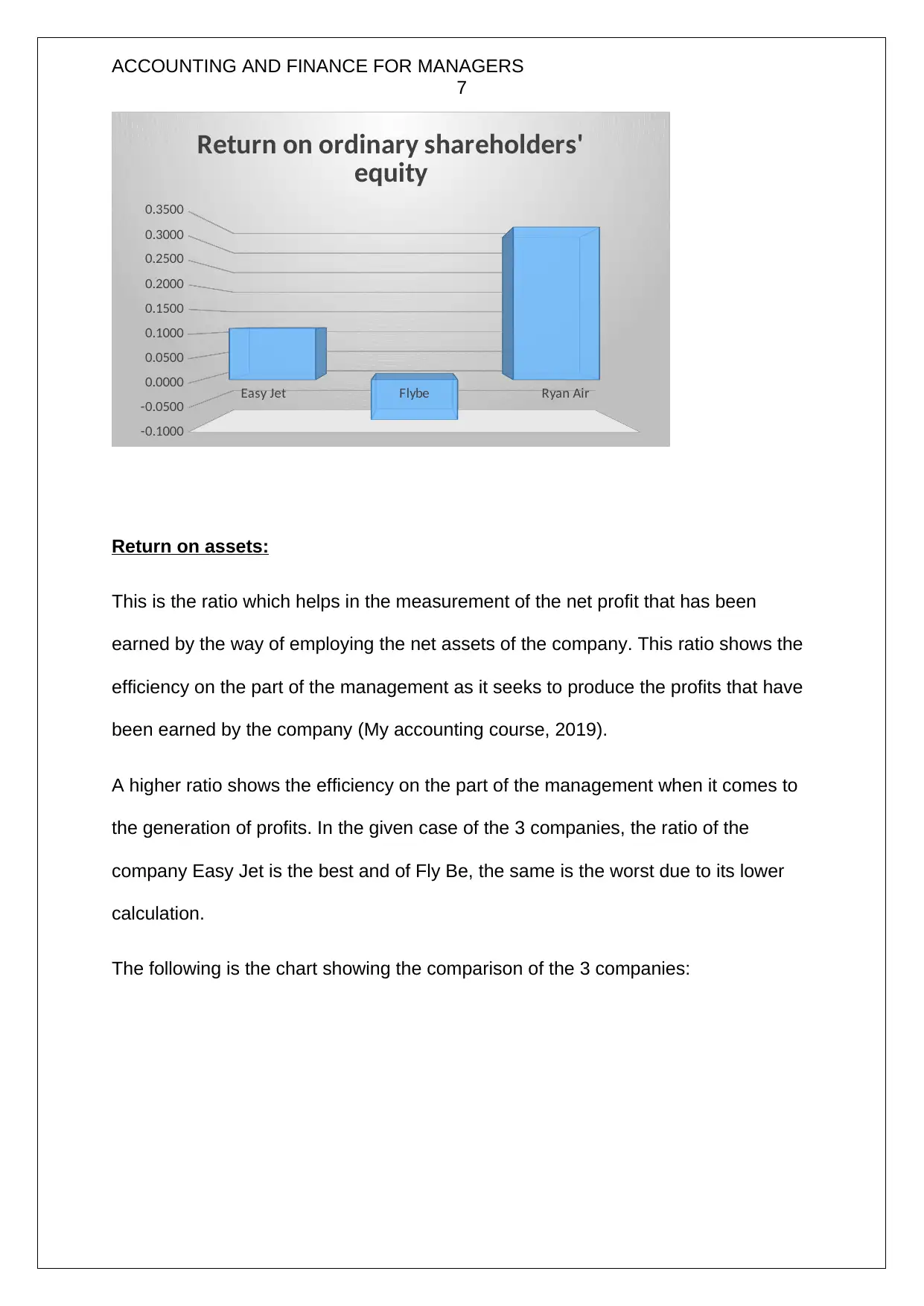

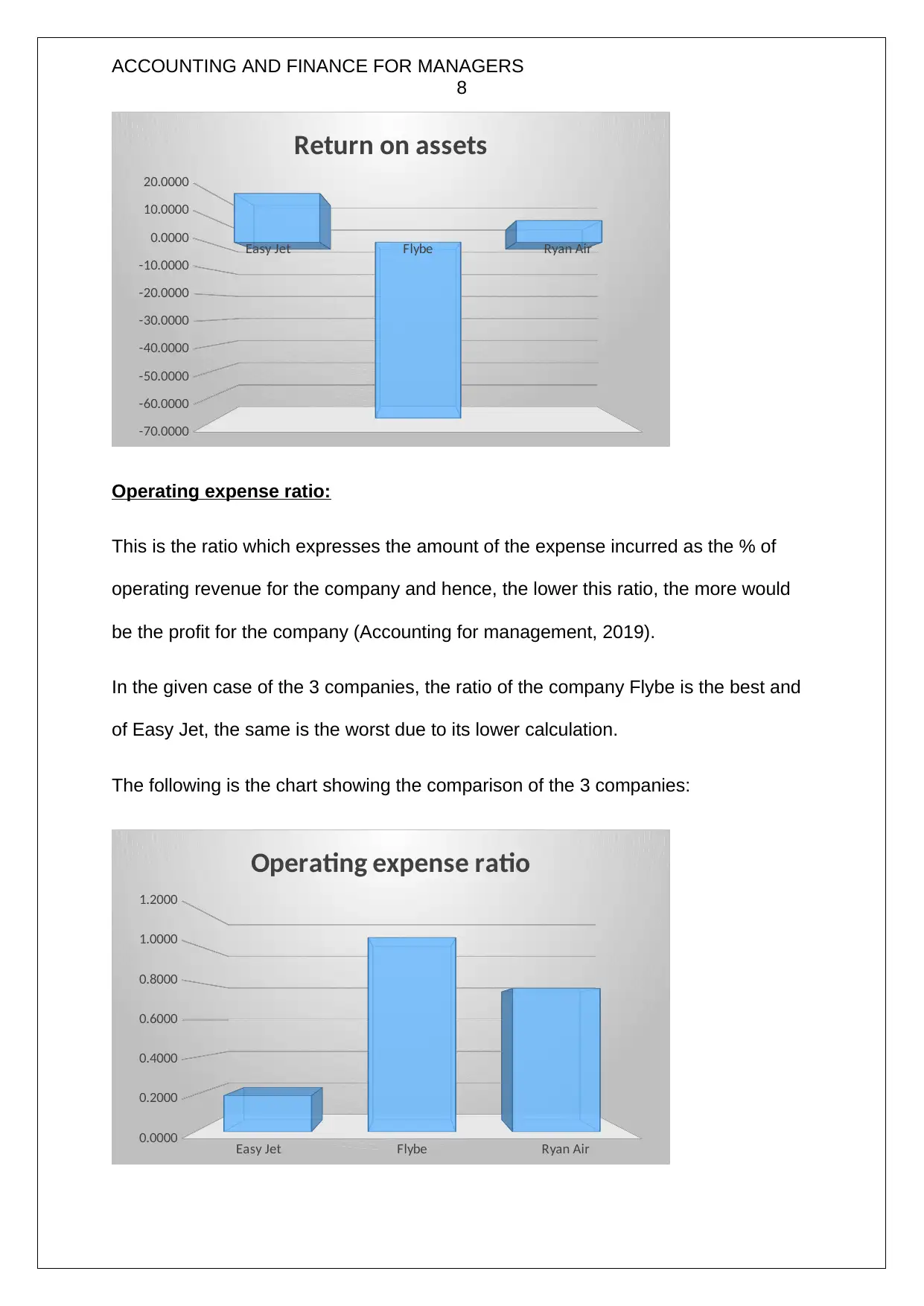

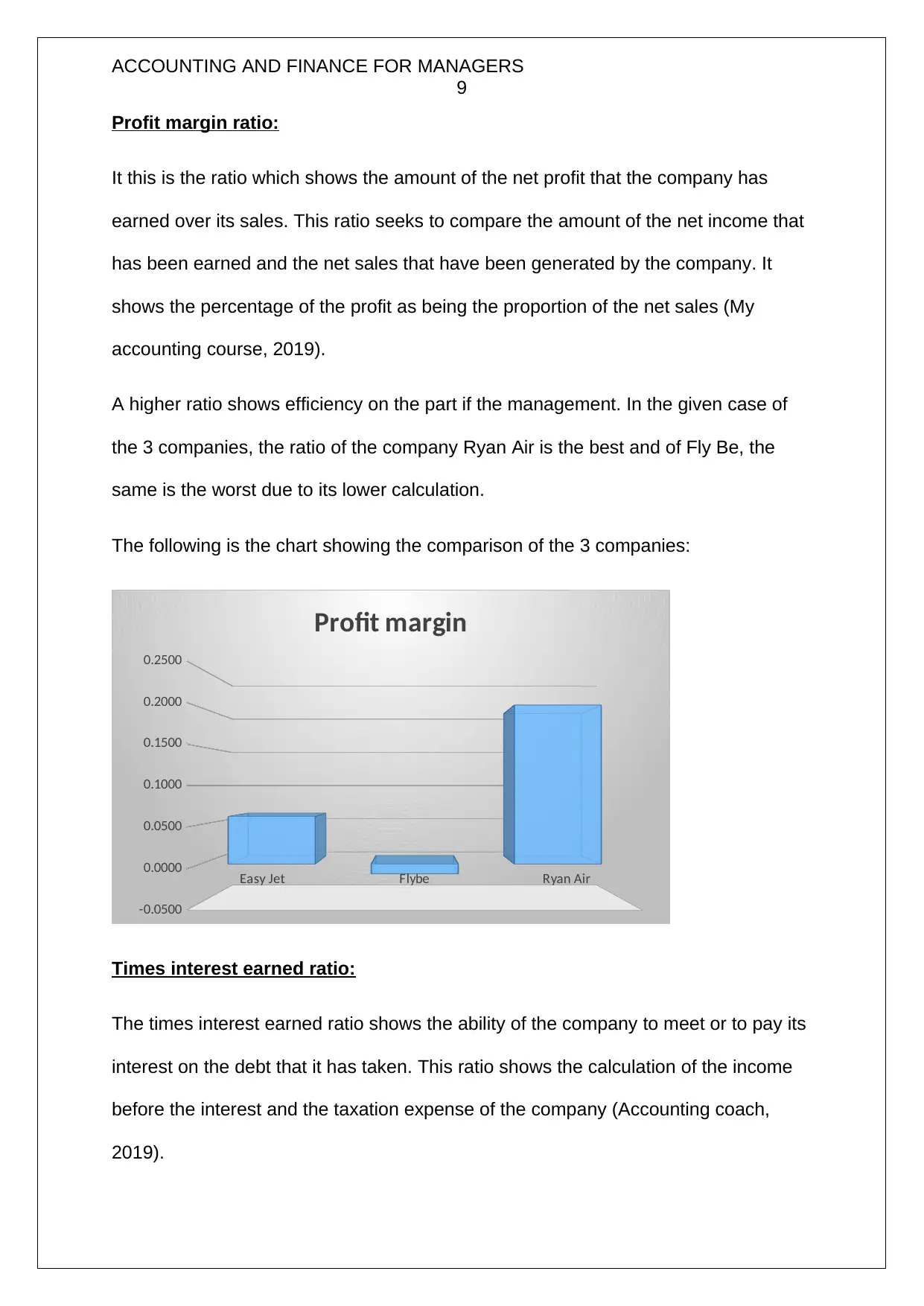

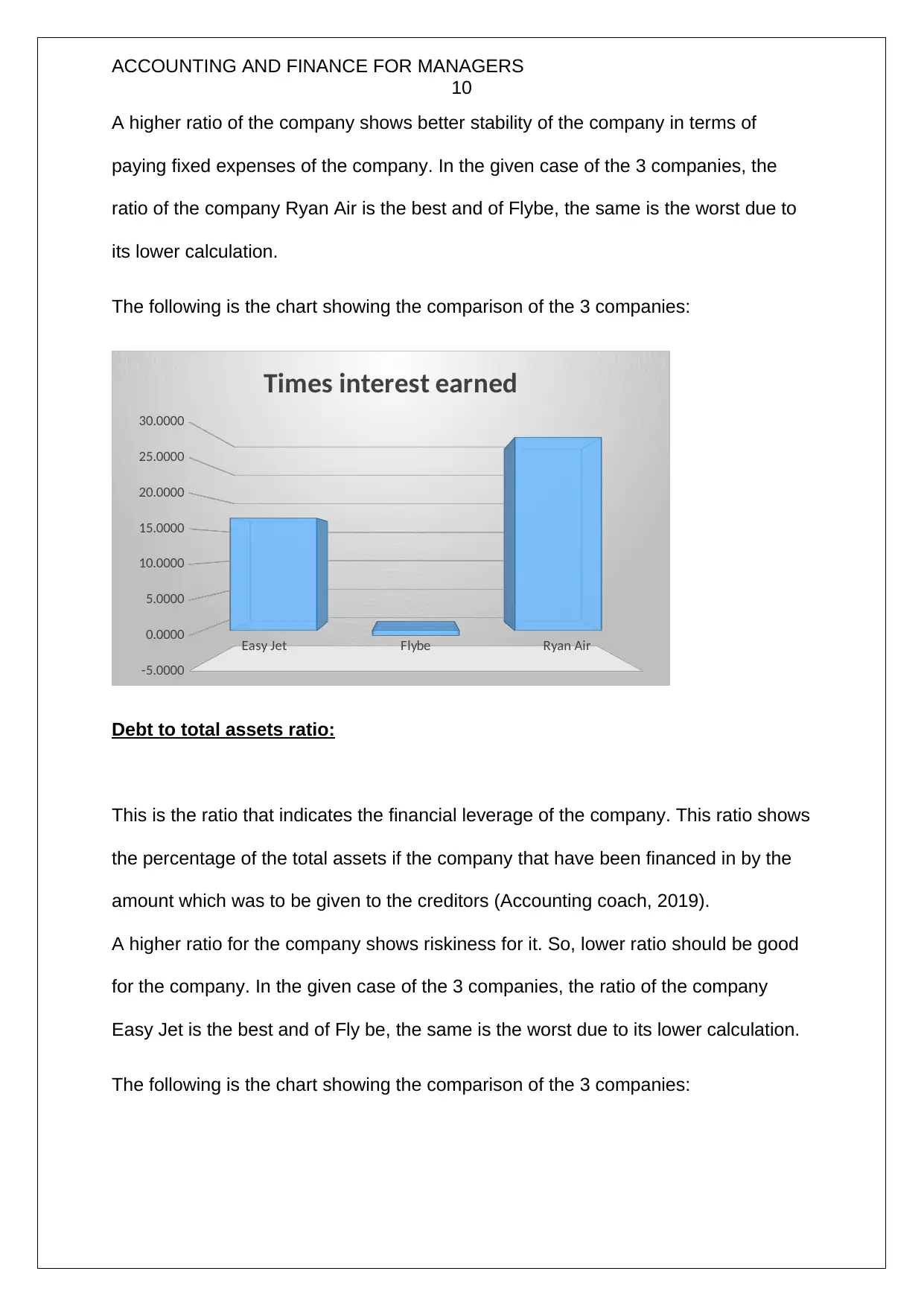

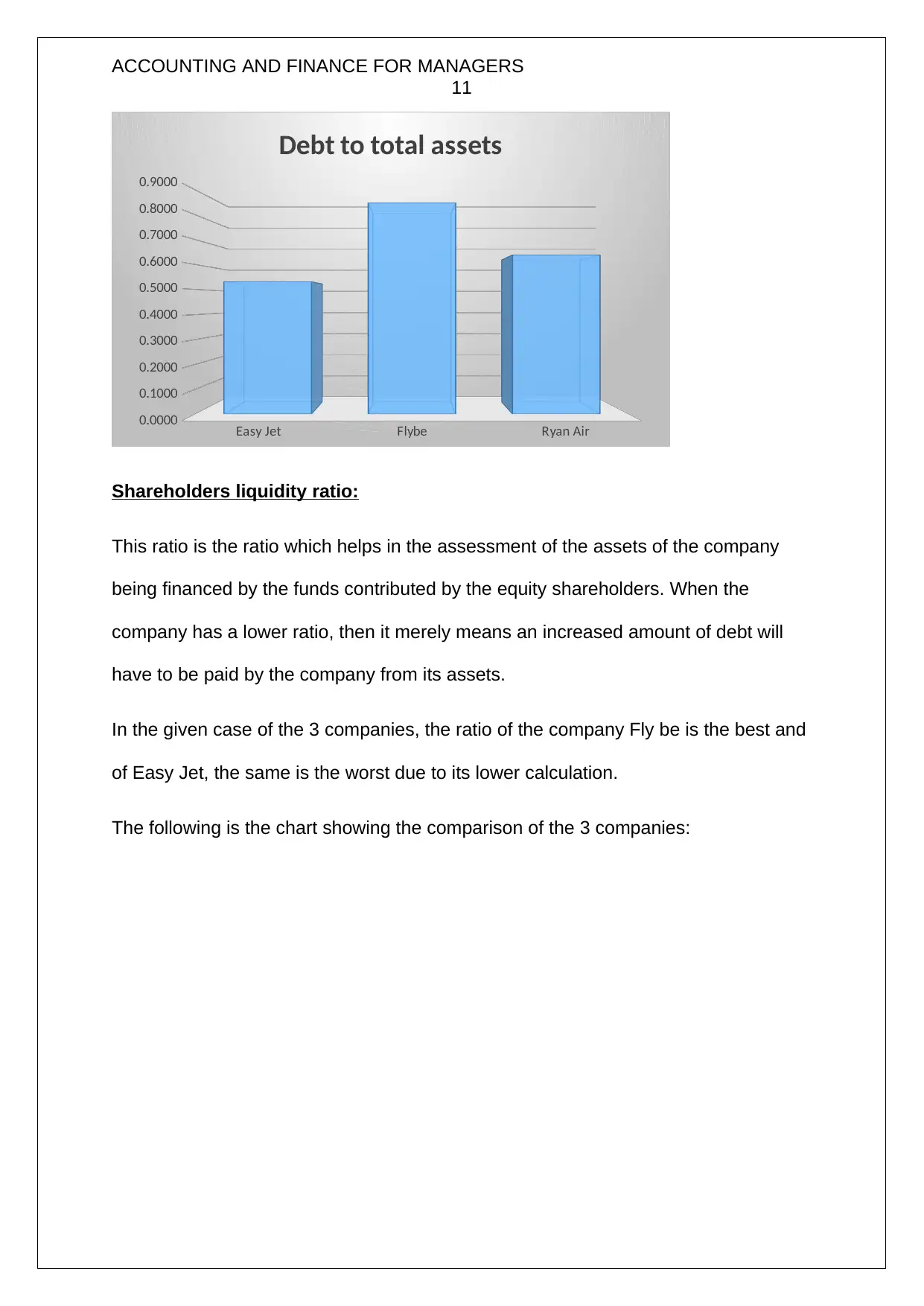

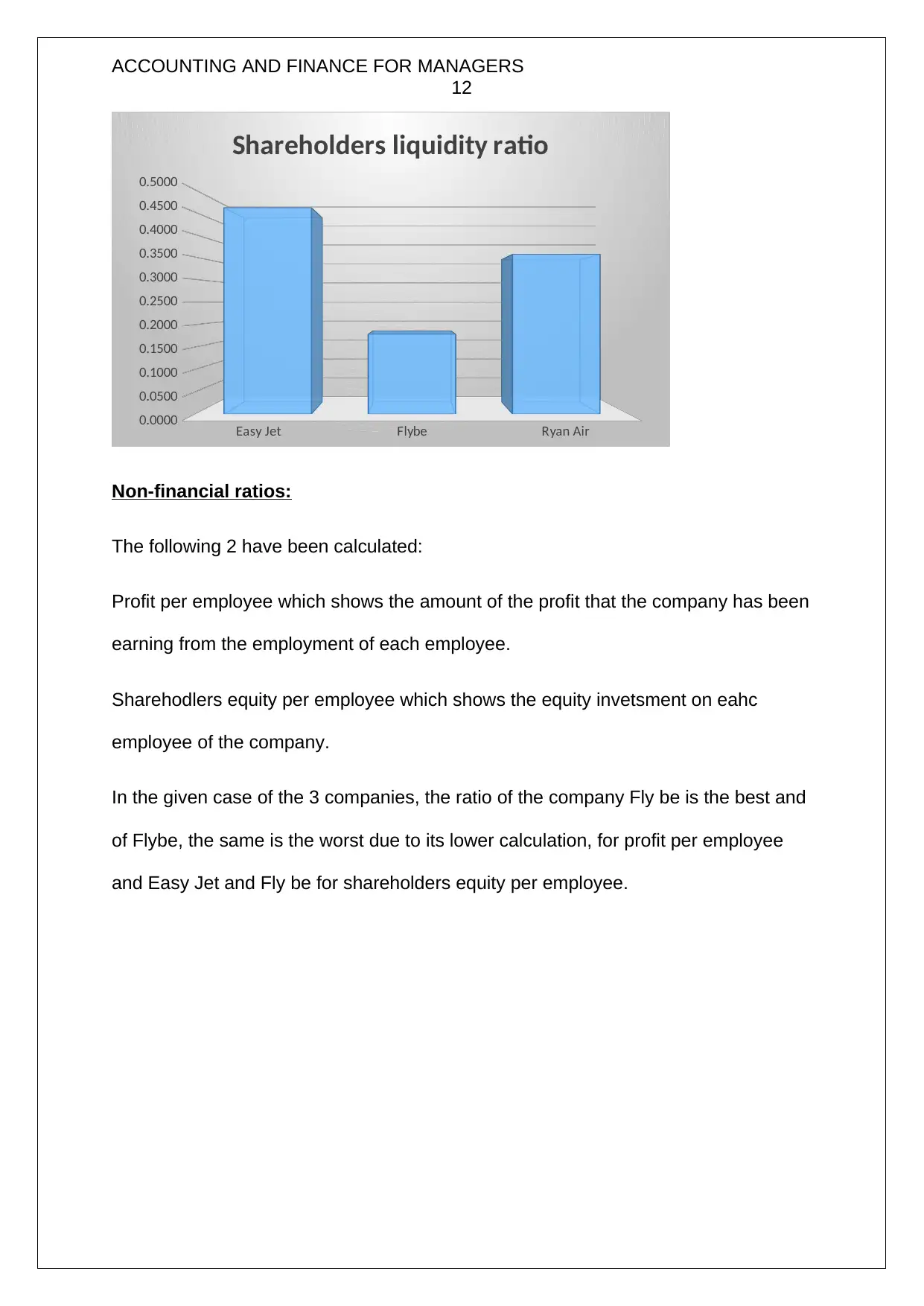

This case study analyzes the financial performance of three aviation companies: EasyJet, Flybe, and Ryan Air. The assignment begins with a detailed analysis of various financial ratios, including current ratio, market cap/cash flow from operations, receivables turnover ratio, return on shareholders’ equity, return on assets, operating expense ratio, profit margin ratio, times interest earned ratio, debt to total assets ratio, shareholders liquidity ratio, and non-financial ratios such as profit per employee and shareholders' equity per employee. The analysis is used to assess the investment viability of each company, with a focus on Ryan Air. Furthermore, the case study provides recommendations for improving the business operations of Flybe. The second part of the assignment covers capital investment techniques, including methods of evaluating investments and the steps involved in the process. The case study is based on the ACC3015 module at the University of Northampton.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.