Corporate Governance and Accounting Theory Report - ACC302 Analysis

VerifiedAdded on 2022/09/05

|14

|2799

|17

Report

AI Summary

This report analyzes the relationship between accounting theory and corporate governance, focusing on the practices of two ASX-listed companies, Wesfarmers and Woolworths. The report examines their corporate governance policies, including board composition, CEO and Chairman statements, and disclosure practices, referencing the ASX Principles. Part A of the report provides a comparative analysis of the two companies, addressing aspects like board structure, director independence, and executive leadership. Part B delves into the role of corporate governance in accounting, discussing its importance in ensuring transparency, accountability, and ethical financial reporting. The report explores the impact of corporate governance failures and the role of accounting standards and regulatory bodies like ASIC. It emphasizes the need for good corporate governance to maintain investor confidence and protect companies from corruption, highlighting the importance of independent committees, timely disclosure, and adherence to accounting regulations like CLERP9. The study concludes by emphasizing that companies can improve the extent of independence on board sub committees.

Running head: ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Accounting Theory and Corporate Governance

Name of the Student

Name of the University

Authors Note

Course ID

Accounting Theory and Corporate Governance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Table of Contents

Answer to Part A:.......................................................................................................................2

Answer to 1:...............................................................................................................................2

Answer to 2:...............................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................3

Answer to D:..........................................................................................................................3

Answer E:...............................................................................................................................4

Answer to 3:...............................................................................................................................4

Part B: Role of Corporate Governance in Accounting...............................................................6

References:...............................................................................................................................11

Table of Contents

Answer to Part A:.......................................................................................................................2

Answer to 1:...............................................................................................................................2

Answer to 2:...............................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................3

Answer to D:..........................................................................................................................3

Answer E:...............................................................................................................................4

Answer to 3:...............................................................................................................................4

Part B: Role of Corporate Governance in Accounting...............................................................6

References:...............................................................................................................................11

2ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Answer to Part A:

Answer to 1:

Wesfarmers board believe that the corporate governance policies and practices that

are implemented all through the reporting period of 30th June 2019 adheres with the

references given in ASX Principles (Group, 2019). Wesfarmers corporate governance

policies consist of conflict of interest, code of conduct, Whistle blower policy, market

disclosure policy and environmental policy.

While the Woolworths corporate governance is considered central to the company in

creating a sustainable growth and improving the long-term value of shareholders. The

directors and the team members of Woolworths is anticipated to act in an ethical manner and

responsibly all the time. The ambition of Woolworths goes further than the legal compliance

(Woolworthsgroup 2019). The purpose of the company is to construct a healthier experience

together for a better tomorrow with the objective of shaping the company’s commitment for

meeting the requirements of its customers, teams and key stakeholders.

Answer to 2:

Answer A:

Total number of directors for Wesfarmers and Woolworths are as follows;

Total number of directors

Wesfarmers 10

Woolworths 8

Answer to Part A:

Answer to 1:

Wesfarmers board believe that the corporate governance policies and practices that

are implemented all through the reporting period of 30th June 2019 adheres with the

references given in ASX Principles (Group, 2019). Wesfarmers corporate governance

policies consist of conflict of interest, code of conduct, Whistle blower policy, market

disclosure policy and environmental policy.

While the Woolworths corporate governance is considered central to the company in

creating a sustainable growth and improving the long-term value of shareholders. The

directors and the team members of Woolworths is anticipated to act in an ethical manner and

responsibly all the time. The ambition of Woolworths goes further than the legal compliance

(Woolworthsgroup 2019). The purpose of the company is to construct a healthier experience

together for a better tomorrow with the objective of shaping the company’s commitment for

meeting the requirements of its customers, teams and key stakeholders.

Answer to 2:

Answer A:

Total number of directors for Wesfarmers and Woolworths are as follows;

Total number of directors

Wesfarmers 10

Woolworths 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Answer B:

No disclosure is made by Wesfarmers and Woolworths regarding the percentage of

non-executive directors in the financial statement and corporate governance report of the

respective companies.

Answer C:

No disclosure is made by Wesfarmers and Woolworths regarding the percentage of

independent directors in the financial statement and corporate governance report of the

respective companies (Francis, Hasan and Wu, 2015).

Answer to D:

The name of chairman of Woolworths is Gordon Cairns while the name of CEO is

Brad Branducci.

Summary of CEO and Chairman statement Woolworths:

CEO:

As per the CEO the company has made a pleasing progress in its transformation by

achieving a strong focus on the customer differentiation and fundamental simplification of

process. The company has completed a number of initiative that would materially reshape the

company’s support towards evolution in food and daily needs of retail ecosystem.

Chairman:

The chairman constantly supports Australia’s commitment under the Paris agreement

and would be reporting in agreement with the rules of task force on financial releases relating

to climate. Till date it has reduced its carbon emission by 18%. As per chairman, in 2019 the

company returned $1.7 billion to the shareholders.

Answer B:

No disclosure is made by Wesfarmers and Woolworths regarding the percentage of

non-executive directors in the financial statement and corporate governance report of the

respective companies.

Answer C:

No disclosure is made by Wesfarmers and Woolworths regarding the percentage of

independent directors in the financial statement and corporate governance report of the

respective companies (Francis, Hasan and Wu, 2015).

Answer to D:

The name of chairman of Woolworths is Gordon Cairns while the name of CEO is

Brad Branducci.

Summary of CEO and Chairman statement Woolworths:

CEO:

As per the CEO the company has made a pleasing progress in its transformation by

achieving a strong focus on the customer differentiation and fundamental simplification of

process. The company has completed a number of initiative that would materially reshape the

company’s support towards evolution in food and daily needs of retail ecosystem.

Chairman:

The chairman constantly supports Australia’s commitment under the Paris agreement

and would be reporting in agreement with the rules of task force on financial releases relating

to climate. Till date it has reduced its carbon emission by 18%. As per chairman, in 2019 the

company returned $1.7 billion to the shareholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND CORPORATE GOVERNANCE

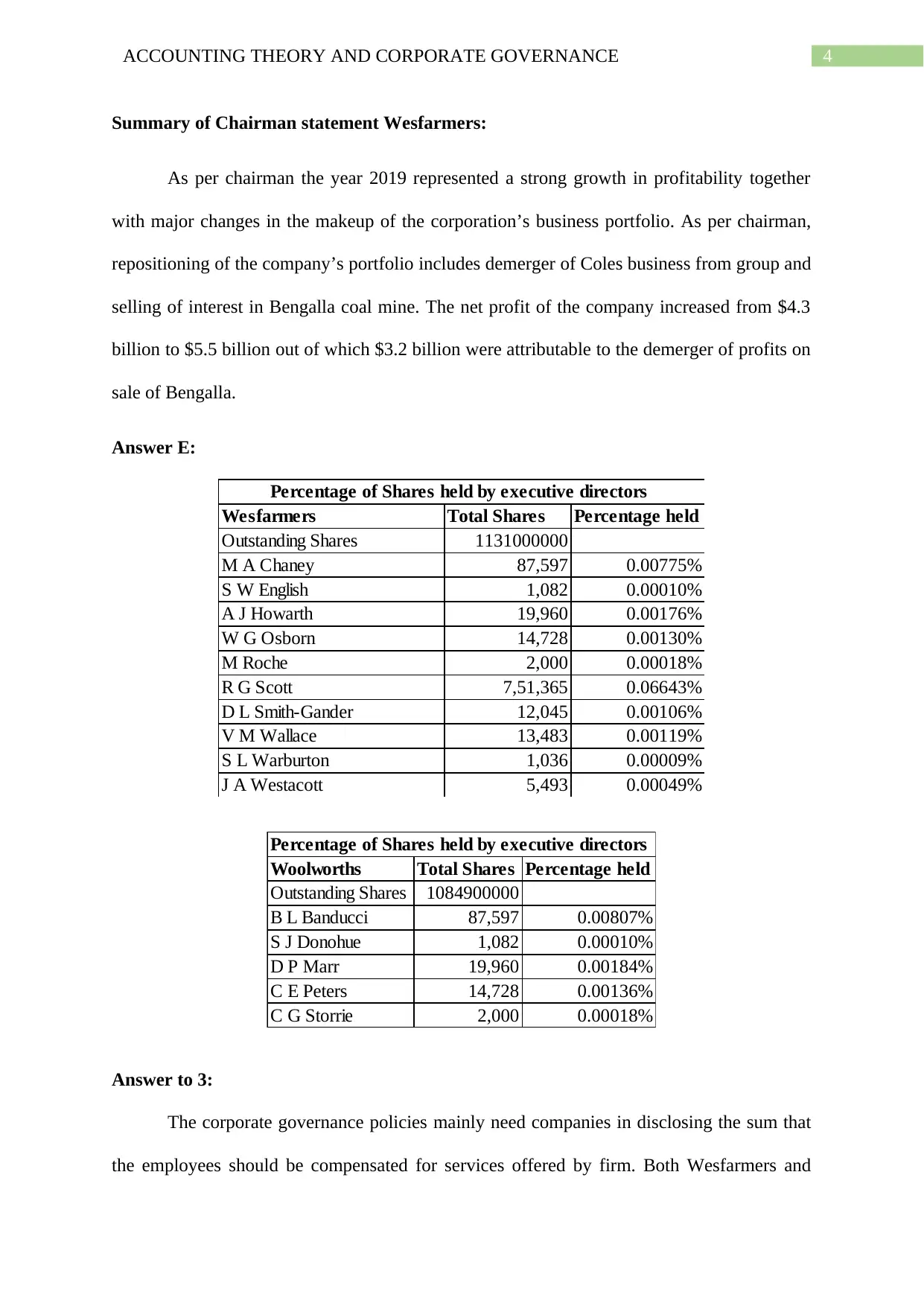

Summary of Chairman statement Wesfarmers:

As per chairman the year 2019 represented a strong growth in profitability together

with major changes in the makeup of the corporation’s business portfolio. As per chairman,

repositioning of the company’s portfolio includes demerger of Coles business from group and

selling of interest in Bengalla coal mine. The net profit of the company increased from $4.3

billion to $5.5 billion out of which $3.2 billion were attributable to the demerger of profits on

sale of Bengalla.

Answer E:

Wesfarmers Total Shares Percentage held

Outstanding Shares 1131000000

M A Chaney 87,597 0.00775%

S W English 1,082 0.00010%

A J Howarth 19,960 0.00176%

W G Osborn 14,728 0.00130%

M Roche 2,000 0.00018%

R G Scott 7,51,365 0.06643%

D L Smith-Gander 12,045 0.00106%

V M Wallace 13,483 0.00119%

S L Warburton 1,036 0.00009%

J A Westacott 5,493 0.00049%

Percentage of Shares held by executive directors

Woolworths Total Shares Percentage held

Outstanding Shares 1084900000

B L Banducci 87,597 0.00807%

S J Donohue 1,082 0.00010%

D P Marr 19,960 0.00184%

C E Peters 14,728 0.00136%

C G Storrie 2,000 0.00018%

Percentage of Shares held by executive directors

Answer to 3:

The corporate governance policies mainly need companies in disclosing the sum that

the employees should be compensated for services offered by firm. Both Wesfarmers and

Summary of Chairman statement Wesfarmers:

As per chairman the year 2019 represented a strong growth in profitability together

with major changes in the makeup of the corporation’s business portfolio. As per chairman,

repositioning of the company’s portfolio includes demerger of Coles business from group and

selling of interest in Bengalla coal mine. The net profit of the company increased from $4.3

billion to $5.5 billion out of which $3.2 billion were attributable to the demerger of profits on

sale of Bengalla.

Answer E:

Wesfarmers Total Shares Percentage held

Outstanding Shares 1131000000

M A Chaney 87,597 0.00775%

S W English 1,082 0.00010%

A J Howarth 19,960 0.00176%

W G Osborn 14,728 0.00130%

M Roche 2,000 0.00018%

R G Scott 7,51,365 0.06643%

D L Smith-Gander 12,045 0.00106%

V M Wallace 13,483 0.00119%

S L Warburton 1,036 0.00009%

J A Westacott 5,493 0.00049%

Percentage of Shares held by executive directors

Woolworths Total Shares Percentage held

Outstanding Shares 1084900000

B L Banducci 87,597 0.00807%

S J Donohue 1,082 0.00010%

D P Marr 19,960 0.00184%

C E Peters 14,728 0.00136%

C G Storrie 2,000 0.00018%

Percentage of Shares held by executive directors

Answer to 3:

The corporate governance policies mainly need companies in disclosing the sum that

the employees should be compensated for services offered by firm. Both Wesfarmers and

5ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Woolworths corporate governance practices involves prudence in financial statements which

assures that there should be a fair representation of financial information regarding the

company (Tricker and Tricker 2015). finally, this helps in corporate reporting and governance

for Wesfarmers and Woolworths.

Woolworths corporate governance practices involves prudence in financial statements which

assures that there should be a fair representation of financial information regarding the

company (Tricker and Tricker 2015). finally, this helps in corporate reporting and governance

for Wesfarmers and Woolworths.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND CORPORATE GOVERNANCE

Part B: Role of Corporate Governance in Accounting

Introduction:

Corporate governance is regarded as the outline of instructions, relations,

arrangements and procedure through which power is exercised for controlled environment

within companies. Corporate Governance involves devices through which businesses and

those that are in control are held answerable (Hermalin 2014). The corporate governance act

as an influence how the purposes of a business is set and achieved, how the risks are observed

and assessed or how the performance can be optimised. Good corporate governance is

necessary in the present world by each shareholder groups.

Decline of big business firms in the last two eras has additionally strengthened its

demand. Astonishingly, in some catastrophes, accounting is considered as the main discipline

held responsible. The manner in which accounting is practiced give rise to different

treatments in the certain circumstances are some of the dark areas which may open the scope

for corrupt accountants. The author here considers that such kind of claim against accounting

is uncalled-for and unsubstantiated (Armstrong et al. 2015). The essay is based on the role of

corporate governance in accounting, its present status in Australia and how accounting

practice can protect the corporate firms from corruption by setting up governance.

Discussion:

Accounting is regarded as the procedure of compiling the evidence for reporting the

interior matters of an organization to different interested party at the end of definite interval.

It is referred as a language of business and plays a vital role in assuring and continuing with

corporate governance. In global set up, accounting activities is usually measured by the

accounting standards (Yermack 2017). As accounting has become a worldwide discipline and

Part B: Role of Corporate Governance in Accounting

Introduction:

Corporate governance is regarded as the outline of instructions, relations,

arrangements and procedure through which power is exercised for controlled environment

within companies. Corporate Governance involves devices through which businesses and

those that are in control are held answerable (Hermalin 2014). The corporate governance act

as an influence how the purposes of a business is set and achieved, how the risks are observed

and assessed or how the performance can be optimised. Good corporate governance is

necessary in the present world by each shareholder groups.

Decline of big business firms in the last two eras has additionally strengthened its

demand. Astonishingly, in some catastrophes, accounting is considered as the main discipline

held responsible. The manner in which accounting is practiced give rise to different

treatments in the certain circumstances are some of the dark areas which may open the scope

for corrupt accountants. The author here considers that such kind of claim against accounting

is uncalled-for and unsubstantiated (Armstrong et al. 2015). The essay is based on the role of

corporate governance in accounting, its present status in Australia and how accounting

practice can protect the corporate firms from corruption by setting up governance.

Discussion:

Accounting is regarded as the procedure of compiling the evidence for reporting the

interior matters of an organization to different interested party at the end of definite interval.

It is referred as a language of business and plays a vital role in assuring and continuing with

corporate governance. In global set up, accounting activities is usually measured by the

accounting standards (Yermack 2017). As accounting has become a worldwide discipline and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CORPORATE GOVERNANCE

the accounting practice is coordinated allied with the numerous need of shareholders, it can

be used as the instrument for assuring good governance inside a commercial setup.

The corporate governance failure in 1970 and 1980 sets the mind of regulators and

public to improve the governance of companies. The outcome led to a plethora of good

governance code issued across the world from stock exchanges and investors association

(Edmans 2014). The main objective relating to all these committees was that good

governance needs effective functioning of board with the help of informed, empowered

subcommittees of board, independent directors and transparency in functioning of

management. The recommendations were mainly aimed at improving the objectivity,

processes and efficiency of audit groups.

As the central point of reference for the companies is to understand the stakeholder

anticipation, for promoting and maintaining the confidence of investors, ASX introduced the

“ASX Corporate Governance Council” in August 2002. The main purpose is to form

recommendations that would reflect an international good practice (Du Plessis, Hargovan and

Harris 2018). As apparent from the conversation that the occupation of accounting has got

involved either directly or indirectly with good governance. Nevertheless, the purpose of

accountants is to make sure that good corporate governance is followed by lowering the gap

amid the insiders and outsiders to a company with the aid of timely disclosure of correct

information.

Accountants have discovered ways to evade rules of accounting while investment

bankers have innovated difficult financial structures to make compulsory disclosure appear

rosier. No wonder that such type of climate has resulted in spectacular collapse of Enron in

2001 and downfall of WorldCom in 2002 (Chan, Watson and Woodliff 2014). It is projected

that scandals such as in Enron, WorldCom and others have contributed to a loss of greater

the accounting practice is coordinated allied with the numerous need of shareholders, it can

be used as the instrument for assuring good governance inside a commercial setup.

The corporate governance failure in 1970 and 1980 sets the mind of regulators and

public to improve the governance of companies. The outcome led to a plethora of good

governance code issued across the world from stock exchanges and investors association

(Edmans 2014). The main objective relating to all these committees was that good

governance needs effective functioning of board with the help of informed, empowered

subcommittees of board, independent directors and transparency in functioning of

management. The recommendations were mainly aimed at improving the objectivity,

processes and efficiency of audit groups.

As the central point of reference for the companies is to understand the stakeholder

anticipation, for promoting and maintaining the confidence of investors, ASX introduced the

“ASX Corporate Governance Council” in August 2002. The main purpose is to form

recommendations that would reflect an international good practice (Du Plessis, Hargovan and

Harris 2018). As apparent from the conversation that the occupation of accounting has got

involved either directly or indirectly with good governance. Nevertheless, the purpose of

accountants is to make sure that good corporate governance is followed by lowering the gap

amid the insiders and outsiders to a company with the aid of timely disclosure of correct

information.

Accountants have discovered ways to evade rules of accounting while investment

bankers have innovated difficult financial structures to make compulsory disclosure appear

rosier. No wonder that such type of climate has resulted in spectacular collapse of Enron in

2001 and downfall of WorldCom in 2002 (Chan, Watson and Woodliff 2014). It is projected

that scandals such as in Enron, WorldCom and others have contributed to a loss of greater

8ACCOUNTING THEORY AND CORPORATE GOVERNANCE

than $7 trillion in market capital which is biggest in capitalism history. Australian firms such

as HIH and ABC Learning failed mainly due to the domination of poor management and

governance by joint creator of the company. There is also an extensive criticism in the report

that concerned the accounting practices within the group. On the other hand, the governance

of One Tel was mainly poor (Edmans 2014). There were huge gaps in the reporting of its

information regarding the director’s shareholdings and three of its committees, namely the

audit committees, remuneration and corporate governance that consist of similar two board

members with none being an independent director.

The doctrine that companies are separate legal entity was existent well before the

registered companies and applied to common law corporations. The proposition that directors

owe their duties towards company has attained growth over the time on the basis that they are

the proprietors of the company that have risked their capital in the anticipation of gain.

According to the central principle of company law directors is obliged to fulfil their duties

towards their company as a whole (Jiang and Kim 2015). The directors and the board is held

answerable for management of company. Nevertheless, the constitution of the company

might permit the board to delegate this authority. Typically, the board may delegate the daily

management duties of the company to the management team.

The extent of matters that are reserved to the board and those that are delegated to the

management is dependent on the size, complexity and structure of ownership within the

entity is influenced by its history and company culture. This might change over the time as

the company evolves (Larcker and Tayan 2015). The board is regularly required to review the

division of functions among the board and management to make sure that it should be

appropriate with the needs of the company.

than $7 trillion in market capital which is biggest in capitalism history. Australian firms such

as HIH and ABC Learning failed mainly due to the domination of poor management and

governance by joint creator of the company. There is also an extensive criticism in the report

that concerned the accounting practices within the group. On the other hand, the governance

of One Tel was mainly poor (Edmans 2014). There were huge gaps in the reporting of its

information regarding the director’s shareholdings and three of its committees, namely the

audit committees, remuneration and corporate governance that consist of similar two board

members with none being an independent director.

The doctrine that companies are separate legal entity was existent well before the

registered companies and applied to common law corporations. The proposition that directors

owe their duties towards company has attained growth over the time on the basis that they are

the proprietors of the company that have risked their capital in the anticipation of gain.

According to the central principle of company law directors is obliged to fulfil their duties

towards their company as a whole (Jiang and Kim 2015). The directors and the board is held

answerable for management of company. Nevertheless, the constitution of the company

might permit the board to delegate this authority. Typically, the board may delegate the daily

management duties of the company to the management team.

The extent of matters that are reserved to the board and those that are delegated to the

management is dependent on the size, complexity and structure of ownership within the

entity is influenced by its history and company culture. This might change over the time as

the company evolves (Larcker and Tayan 2015). The board is regularly required to review the

division of functions among the board and management to make sure that it should be

appropriate with the needs of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND CORPORATE GOVERNANCE

The directors on the other hand are accountable to exercise their duty with care and

diligence. The director is also responsible with the duty of acting in the good faith in the best

interest of the firm and for a reasonable purpose. The duty of directors also relies on not

improperly using the position or information and should not be in the position of conflict of

interest (De Haan and Vlahu 2016). The director also holds the responsibility of disclosing

the material personal interest and should execute their duties to exercise the discretion.

The ASIC on the other hand is regarded as Australia’s combined corporate,

marketplaces, financial services and customer credit regulatory. It is a self-governing

government body of Australia and mainly performs majority of its work under the

Corporation Act. The main role of ASCI is to facilitate, maintain and develop the overall

performance of the financial system and entities in it. The ASIC also plays a dynamic role in

promoting confidence and informs the participation by investors and consumers within the

financial system for better corporate governance (Sapra, Subramanian and Subramanian

2014). It administrates the law efficiently and with lowest amount of procedural requirements

for information regarding the companies and other bodies which is accessible to public as

soon as it becomes practicable.

While CLERP9 in an effort to promote corporate governance makes sure that business

regulations are constant with endorsing a strong and vibrant economy. It also offers an

outline which helps the business in adapting to the change. CLERP9 plays a vital role in

developing the controlling and judicial framework which is reliable, elastic, adaptable and

cost effective (Cai et al. 2015). CLERP9 also helps in creating an appropriate balance among

the government and industry regulation and plays a pivotal role in improving the

harmonisation among the regulatory frameworks of Australia with those that are applying in

the major financial markets.

The directors on the other hand are accountable to exercise their duty with care and

diligence. The director is also responsible with the duty of acting in the good faith in the best

interest of the firm and for a reasonable purpose. The duty of directors also relies on not

improperly using the position or information and should not be in the position of conflict of

interest (De Haan and Vlahu 2016). The director also holds the responsibility of disclosing

the material personal interest and should execute their duties to exercise the discretion.

The ASIC on the other hand is regarded as Australia’s combined corporate,

marketplaces, financial services and customer credit regulatory. It is a self-governing

government body of Australia and mainly performs majority of its work under the

Corporation Act. The main role of ASCI is to facilitate, maintain and develop the overall

performance of the financial system and entities in it. The ASIC also plays a dynamic role in

promoting confidence and informs the participation by investors and consumers within the

financial system for better corporate governance (Sapra, Subramanian and Subramanian

2014). It administrates the law efficiently and with lowest amount of procedural requirements

for information regarding the companies and other bodies which is accessible to public as

soon as it becomes practicable.

While CLERP9 in an effort to promote corporate governance makes sure that business

regulations are constant with endorsing a strong and vibrant economy. It also offers an

outline which helps the business in adapting to the change. CLERP9 plays a vital role in

developing the controlling and judicial framework which is reliable, elastic, adaptable and

cost effective (Cai et al. 2015). CLERP9 also helps in creating an appropriate balance among

the government and industry regulation and plays a pivotal role in improving the

harmonisation among the regulatory frameworks of Australia with those that are applying in

the major financial markets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND CORPORATE GOVERNANCE

A commitment towards good corporate governance is regarded as a simple term of

say, well-defined rights of shareholders, strong controlled environment, higher level of

transparency and disclosure etc. makes the company highly attractive towards investors and

lenders that are more profitable. Shareholders generally look forward for this which attracts

premium valuation in each aspect (Armstrong et al. 2014). Since accounting is internationally

mentioned as the vehicle for assuring good corporate governance, it is thought that the world

must accept the universal international accounting standard and it has already been done. The

journey has been in progress long before and this move would make it easy to relate the

performance of the companies within the industry and across the countries.

The study clearly shows that companies can improve the extent of independence on

board sub committees (Yermack 2017). The significance of independence differs from every

committee. For example, the nomination committee should be independent in order to assure

that correct person with correct skills set is elected to board instead of someone who is

selected by CEO to carry out their job as instructed. It will also help in assuring that a

transparent nomination and director’s evaluations helps in effective succession planning.

Conclusions:

Corporate governance is very much important in the present multifaceted and active

business background to make sure long-term sustainability. As a result, it must be cultivated

and practiced on a regular basis inside the present business structure. Companies should learn

lessons from Enron, WorldCom and ABC Learning, as companies may fail to recover the

trust of public which is very much indispensable to the long-term success and survival of the

business. Companies that genuinely identify and embrace the principles of good governance

would obtain higher benefits, availability and lower cost of capital along with the ability of

attracting business partners. Undoubtedly, accounting helps in showing the way forward to

A commitment towards good corporate governance is regarded as a simple term of

say, well-defined rights of shareholders, strong controlled environment, higher level of

transparency and disclosure etc. makes the company highly attractive towards investors and

lenders that are more profitable. Shareholders generally look forward for this which attracts

premium valuation in each aspect (Armstrong et al. 2014). Since accounting is internationally

mentioned as the vehicle for assuring good corporate governance, it is thought that the world

must accept the universal international accounting standard and it has already been done. The

journey has been in progress long before and this move would make it easy to relate the

performance of the companies within the industry and across the countries.

The study clearly shows that companies can improve the extent of independence on

board sub committees (Yermack 2017). The significance of independence differs from every

committee. For example, the nomination committee should be independent in order to assure

that correct person with correct skills set is elected to board instead of someone who is

selected by CEO to carry out their job as instructed. It will also help in assuring that a

transparent nomination and director’s evaluations helps in effective succession planning.

Conclusions:

Corporate governance is very much important in the present multifaceted and active

business background to make sure long-term sustainability. As a result, it must be cultivated

and practiced on a regular basis inside the present business structure. Companies should learn

lessons from Enron, WorldCom and ABC Learning, as companies may fail to recover the

trust of public which is very much indispensable to the long-term success and survival of the

business. Companies that genuinely identify and embrace the principles of good governance

would obtain higher benefits, availability and lower cost of capital along with the ability of

attracting business partners. Undoubtedly, accounting helps in showing the way forward to

11ACCOUNTING THEORY AND CORPORATE GOVERNANCE

proceed with the corporate governance where bad governance usually arises from financial

discontent and over use of power.

proceed with the corporate governance where bad governance usually arises from financial

discontent and over use of power.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.