ACC303 Contemporary Issues: GWA Group & AASB Framework Analysis

VerifiedAdded on 2023/06/08

|20

|2465

|129

Report

AI Summary

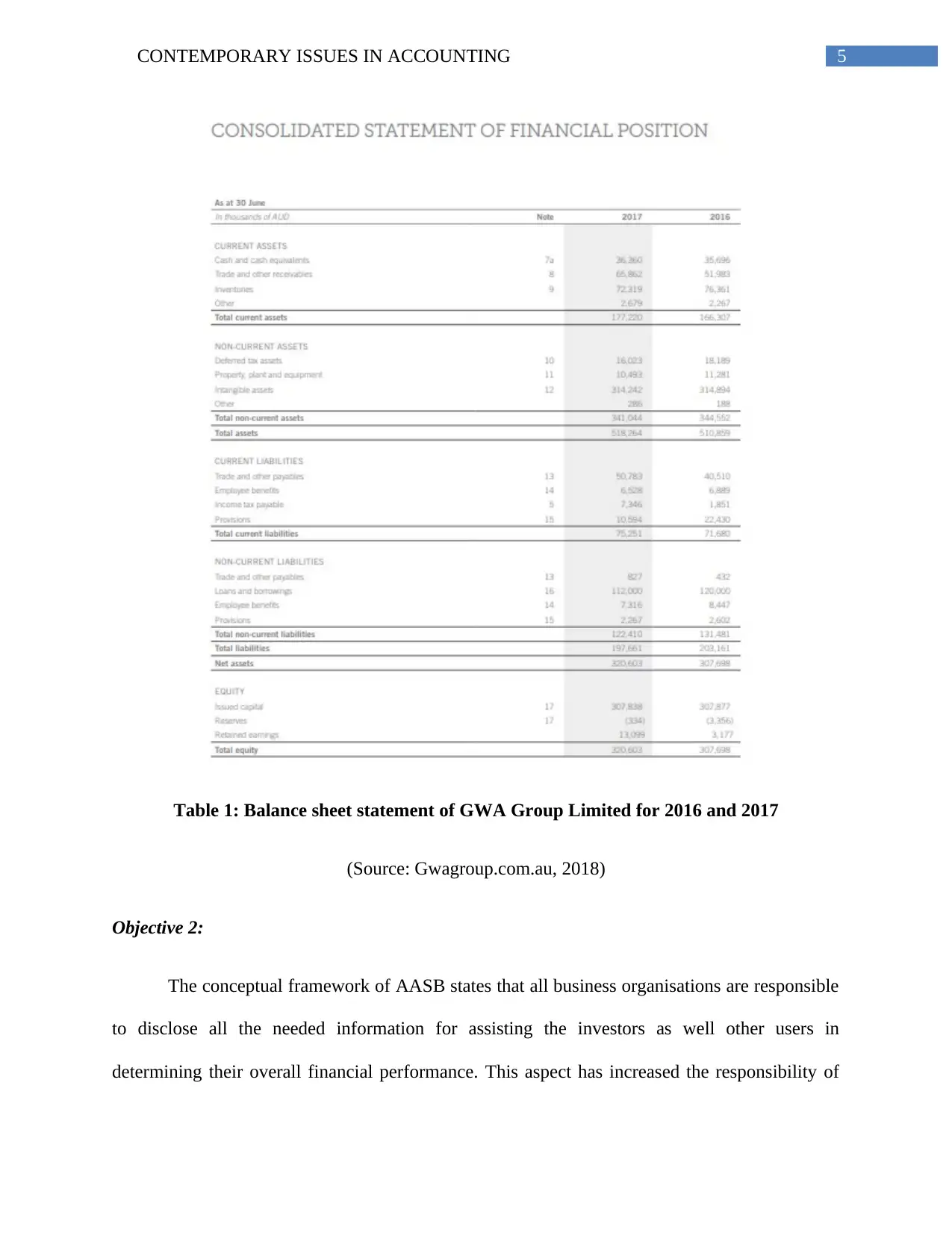

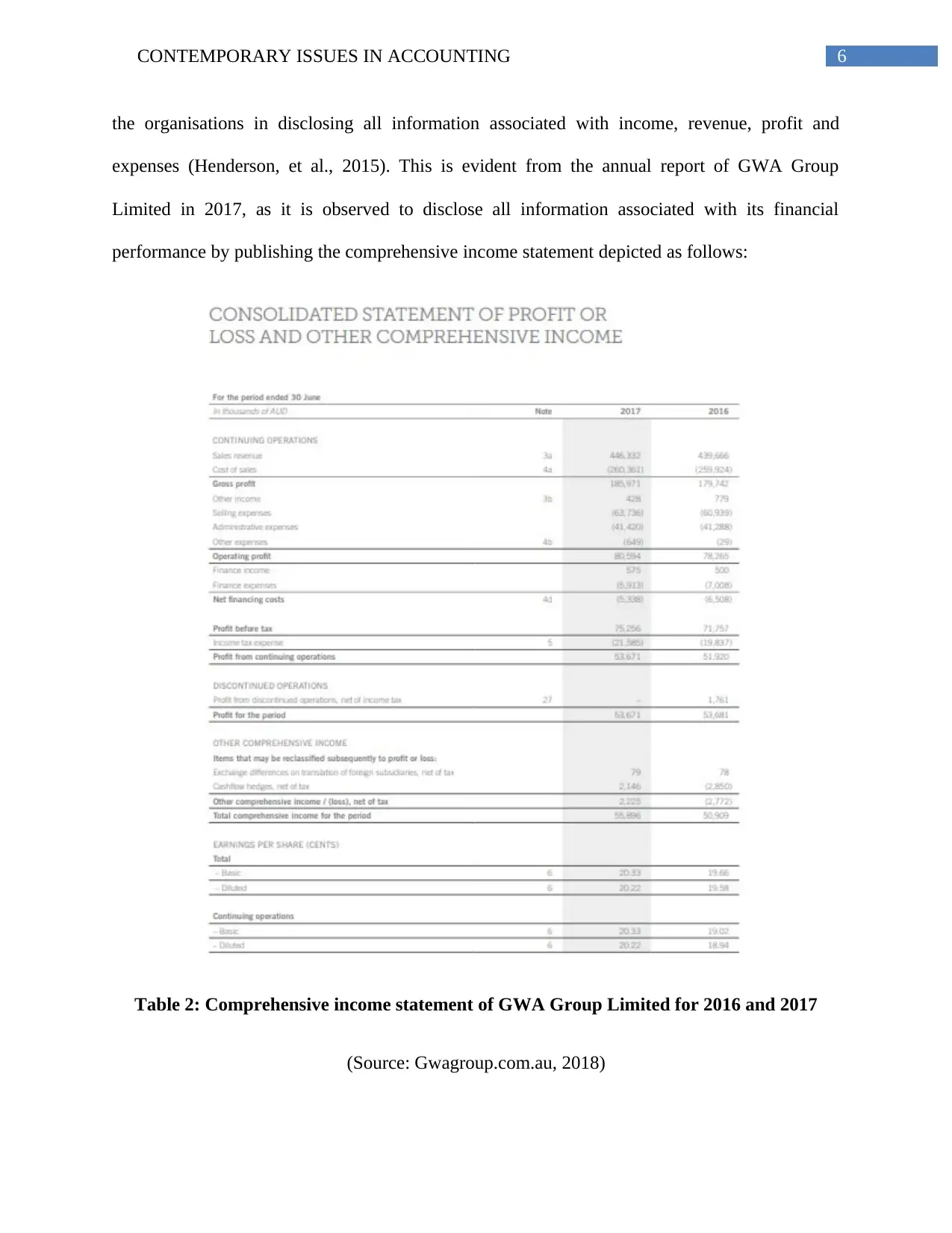

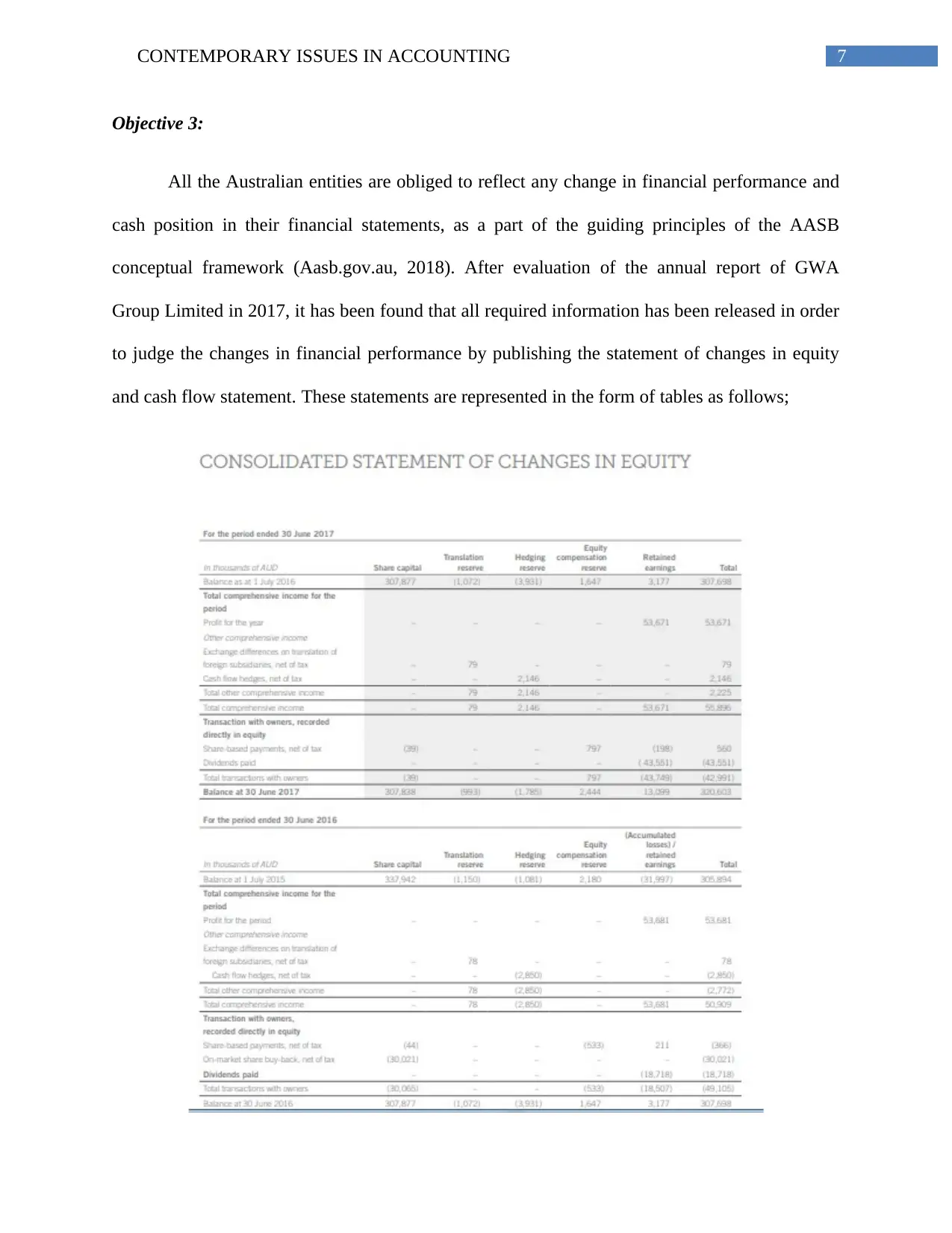

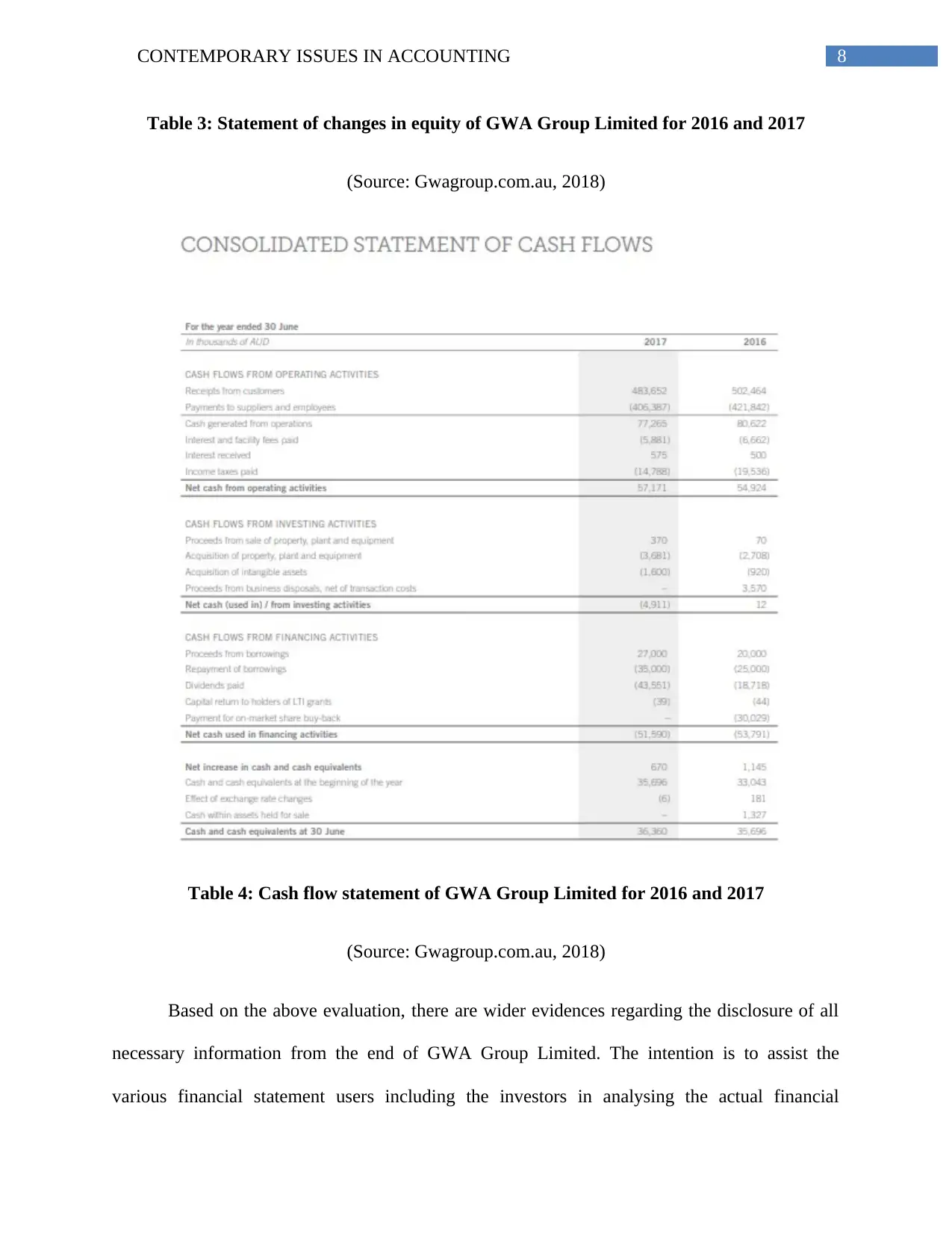

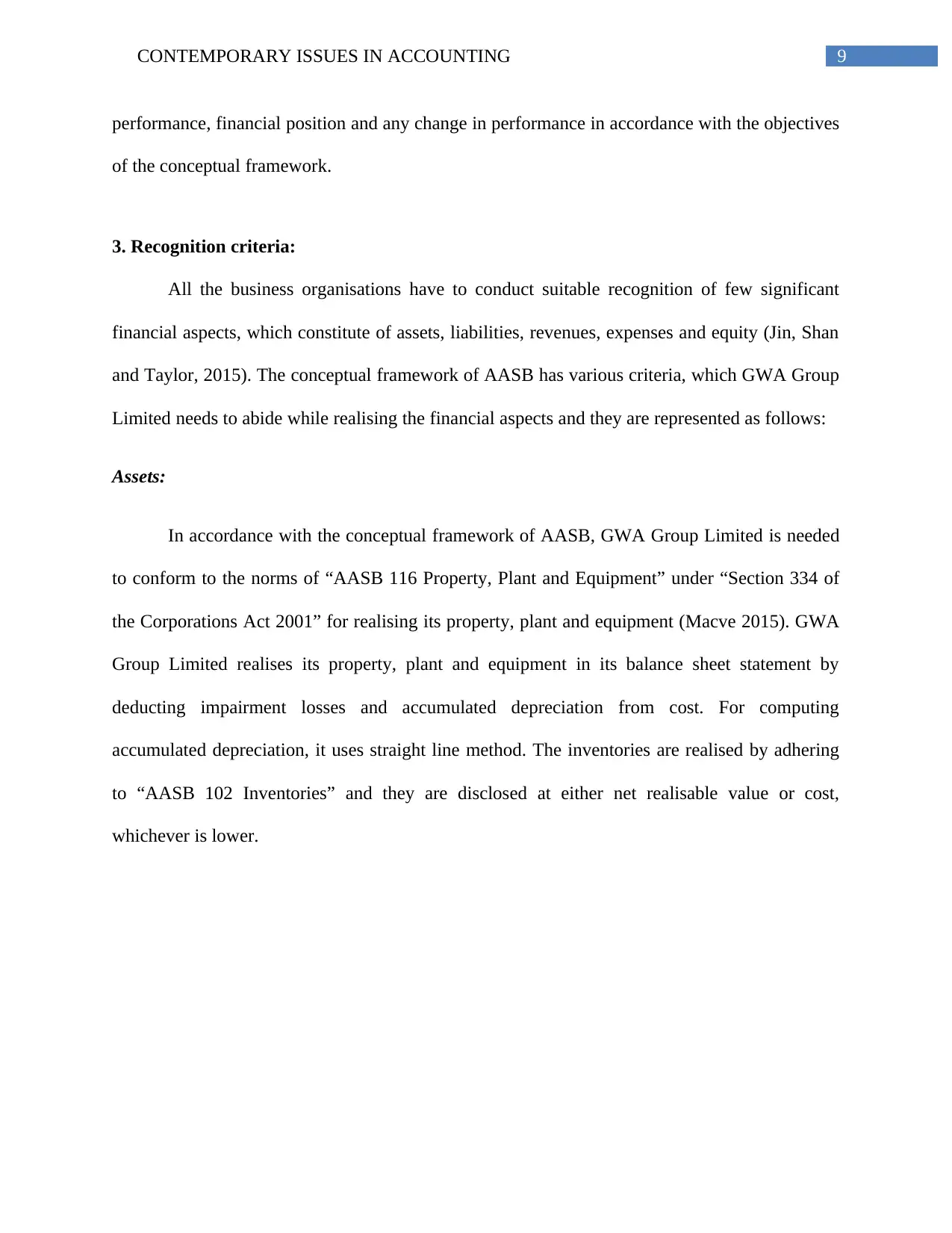

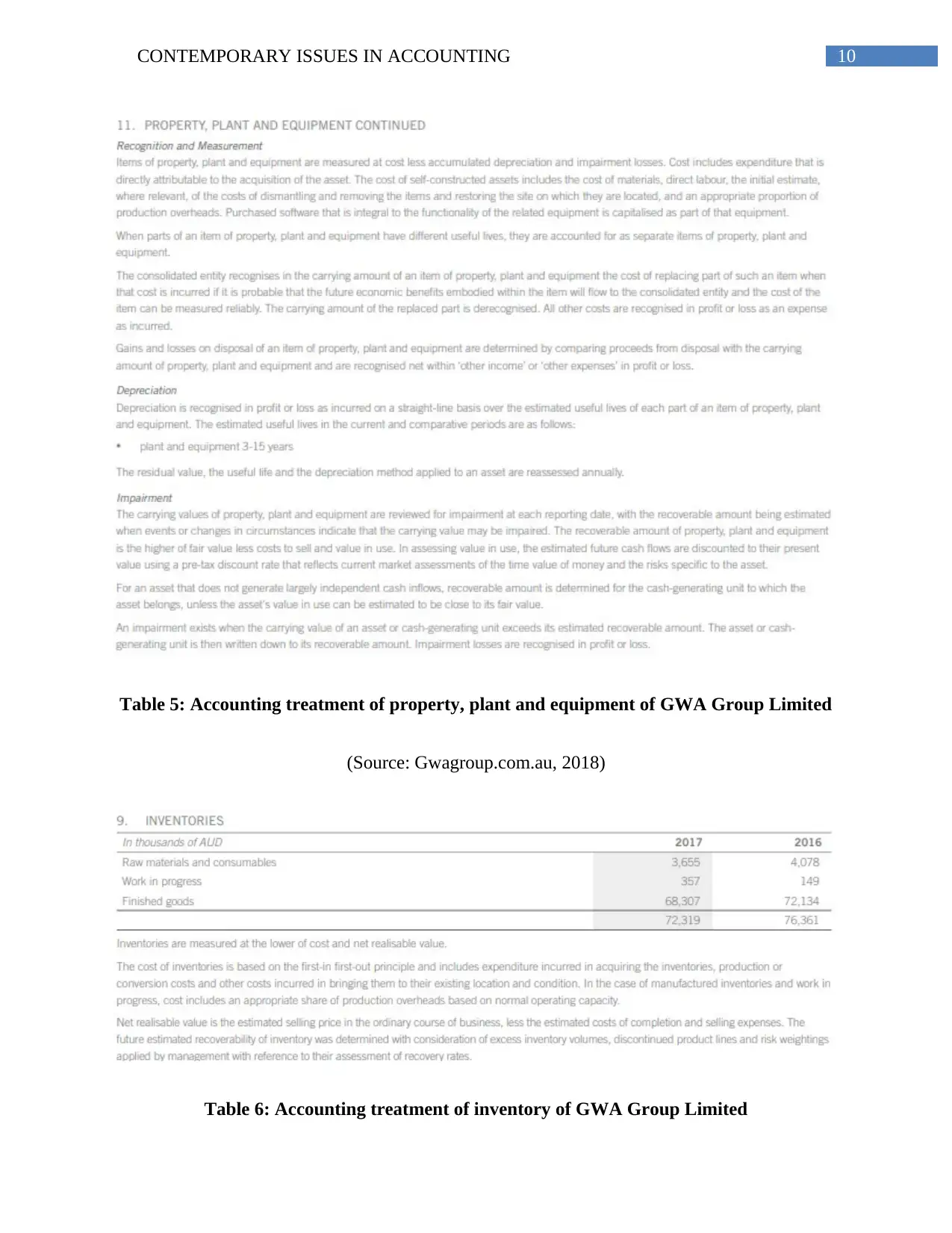

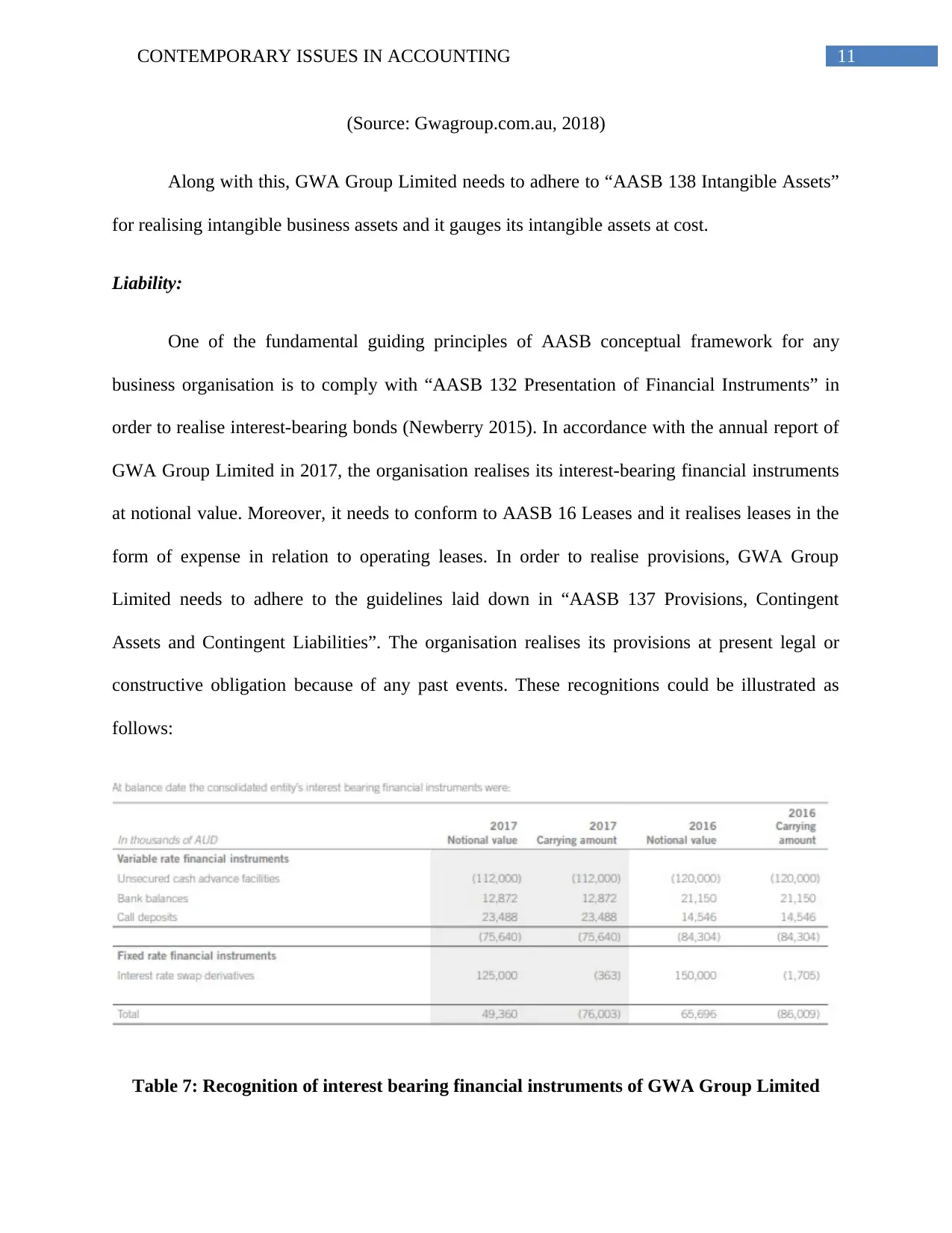

This report analyzes GWA Group Limited's adherence to the AASB conceptual framework, examining the objectives of general-purpose financial reporting, recognition criteria for assets, liabilities, equity, revenue, and expenses, and the qualitative characteristics of financial reporting. The analysis reveals that GWA Group Limited generally conforms to the AASB framework in its financial reporting practices, providing necessary information to investors and users for evaluating the organization's financial condition. The report recommends continued adherence to AASB guidelines to avoid accounting issues in the future. Desklib provides a platform for students to access similar solved assignments and past papers.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.