ACC303 - Relevance of IR Framework in the Contemporary Corporate World

VerifiedAdded on 2022/11/25

|6

|801

|245

Essay

AI Summary

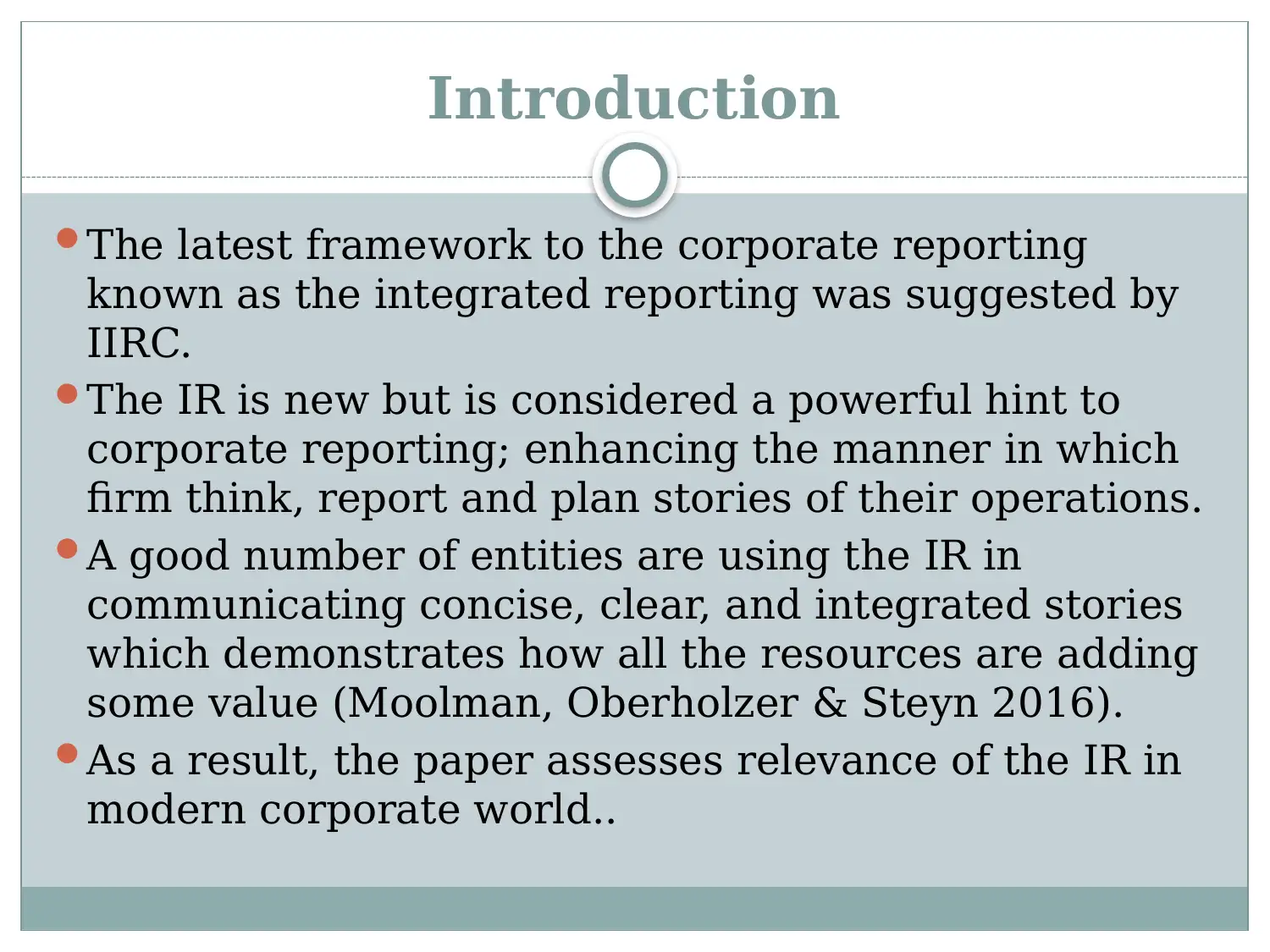

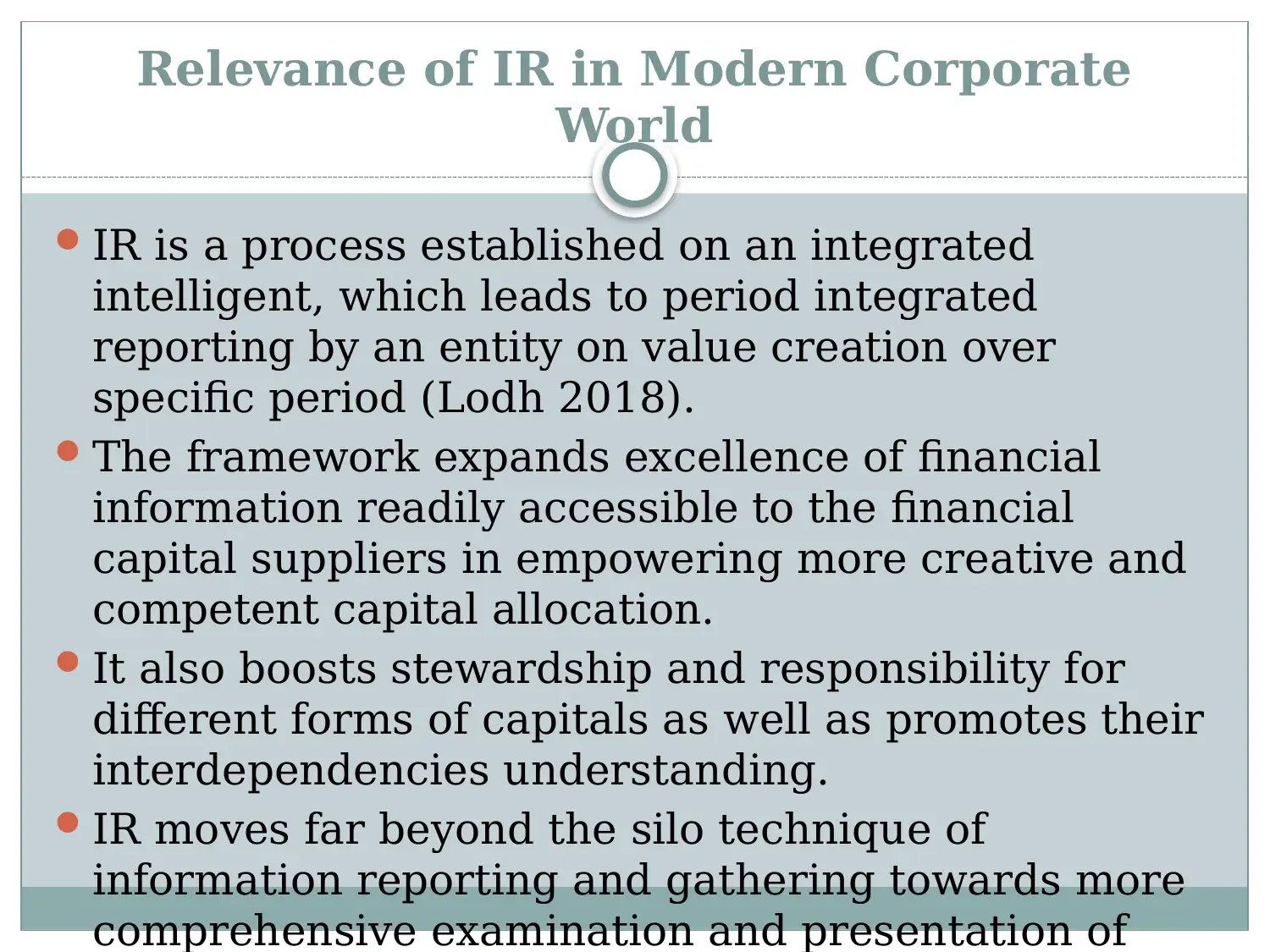

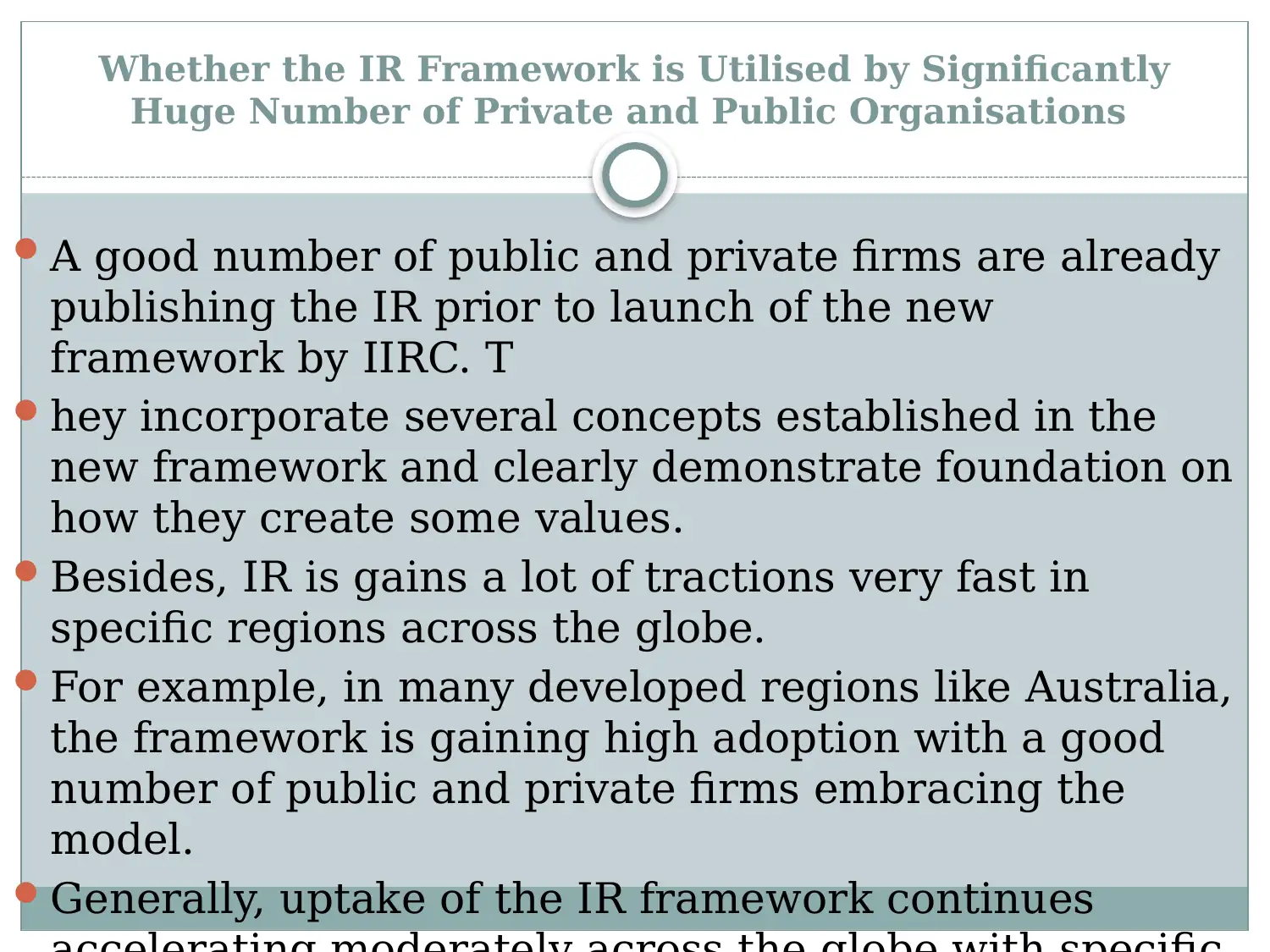

This essay examines the relevance of the Integrated Reporting (IR) Framework in the contemporary corporate world, as advocated by the International Integrated Reporting Council (IIRC). It evaluates the framework's impact on corporate reporting norms, particularly in integrating strategic information across various capitals, including financial, manufactured, intellectual, human, social and relationship, and natural resources. The essay highlights how IR promotes integrated thinking, enhances financial performance, and influences strategic control and value creation within organizations. It also discusses the adoption rate of the IR Framework among public and private firms globally, noting its increasing traction in regions like Australia, Asia, and Europe. The document concludes by emphasizing the framework's role in improving the quality of information available to shareholders and its capacity to create and sustain value.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.