ACC306 - Financial Statement Analysis: Stockland Corporation Limited

VerifiedAdded on 2023/06/10

|14

|3991

|313

Report

AI Summary

This report provides a detailed financial analysis of Stockland Corporation Limited, evaluating its performance over the past three years. It uses ratio analysis to assess profitability, efficiency, liquidity, and capital structure. The analysis reveals that while the company has improved its profitability and efficiency, its capital structure carries a high debt portion, posing potential financial leverage risks. The report further assesses the company's long-term solvency and liquidity position, indicating a generally positive outlook due to increased profitability. The report concludes by touching upon the quality of financial statements and recommending that Stockland establish an equilibrium between its cost of capital, debt portion, and profitability to optimize its financial health. Access this and similar solved assignments and past papers on Desklib.

Stockland Corporation Limited

Financial Management

Financial analysis

Name of the Author

[Pick the date]

Financial Management

Financial analysis

Name of the Author

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Each and every organization needs to use the proper financial tools to make the

effective financial decisions. In this report, Stockland Corporation Company has been

selected. This company has faced high loss due to the sluggish market condition. In addition

to this, company has also faced high downward slope in its share prices which reflects that

shareholders who invested their capital in this company had high amount of loss since last

three years. In addition to this, capital structure of company is also not effective which

reflects that company needs to lower down debt portion in its capital to mitigate the financial

risk. Company might fail to cover its interest coverage from its earnings before interest and

tax due to its less profitability from its business. In context with the efficiency of the

company, it has also failed to deploy its funds effectively which has increased the overall cost

of capital throughout the time

Each and every organization needs to use the proper financial tools to make the

effective financial decisions. In this report, Stockland Corporation Company has been

selected. This company has faced high loss due to the sluggish market condition. In addition

to this, company has also faced high downward slope in its share prices which reflects that

shareholders who invested their capital in this company had high amount of loss since last

three years. In addition to this, capital structure of company is also not effective which

reflects that company needs to lower down debt portion in its capital to mitigate the financial

risk. Company might fail to cover its interest coverage from its earnings before interest and

tax due to its less profitability from its business. In context with the efficiency of the

company, it has also failed to deploy its funds effectively which has increased the overall cost

of capital throughout the time

Table of Contents

Executive Summary...............................................................................................................................1

INTRODUCTION.................................................................................................................................2

Description of company.....................................................................................................................2

Task-1....................................................................................................................................................2

Assess the company’s performance over the last three years..............................................................2

Assessment of the financial position of company..............................................................................4

PROFITABILITY RATIOS..............................................................................................................4

EFFECIENCY RATIO OR ACTIVITY RATIO...............................................................................4

LIQUIDITY RATIOS.......................................................................................................................4

CAPITAL STRUCTURE RATIOS...................................................................................................5

Task-2....................................................................................................................................................5

Long-term solvency of the company over the last three years..............................................................5

Task-3....................................................................................................................................................7

Assess the liquidity position of the company as at the latest financial year......................................7

Liquidity position of Stockland.........................................................................................................7

Task-4....................................................................................................................................................8

Discuss the quality of financial statement.............................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................11

Executive Summary...............................................................................................................................1

INTRODUCTION.................................................................................................................................2

Description of company.....................................................................................................................2

Task-1....................................................................................................................................................2

Assess the company’s performance over the last three years..............................................................2

Assessment of the financial position of company..............................................................................4

PROFITABILITY RATIOS..............................................................................................................4

EFFECIENCY RATIO OR ACTIVITY RATIO...............................................................................4

LIQUIDITY RATIOS.......................................................................................................................4

CAPITAL STRUCTURE RATIOS...................................................................................................5

Task-2....................................................................................................................................................5

Long-term solvency of the company over the last three years..............................................................5

Task-3....................................................................................................................................................7

Assess the liquidity position of the company as at the latest financial year......................................7

Liquidity position of Stockland.........................................................................................................7

Task-4....................................................................................................................................................8

Discuss the quality of financial statement.............................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every organization needs to use the effective financial management to raise and

deploy the funds from the market. It is the process to raise the funds or capital from the

market and deploy the same in the business functioning with an objective to create value on

the investment. There are several financial tools which could be used to assess the financial

performance of company such as ratio analysis, du pont analysis, capital budgeting tool and

financial theories. In this report, three years of financial performance of company has been

assessed to determine whether company has performed well or negative in market. In the first

part of the report, ratio analysis have been used to assess the financial performance of

company and after that capital structure of company has been assessed to determine whether

company has equilibrium point in its financial leverage and cost of capital. After that,

liquidity position of company in the latest financial year has been evaluated to determine

whether company would be able to meet its current liabilities or not. In the end, quality of the

financial statement has been analysed.

Description of company

Stockland Corporation is diversified Australian corporation property Development Company

which has been running its business on international level. This company has business in

shopping centres, housing estates, industrial estates and retirement vilages. This company has

been running its business on international level and all the employees are accustomed to act

as per the directions and instruction of its CEO named Mark Steinert. As per the ASX:SGP,

the share price of company has gone down and reflected 4.14 AUD −0.035 (0.84%)

(Stockland Company, 2017).

Task-1

Assess the company’s performance over the last three years

The ratio analysis is used to assess the financial performance of company and establish the

relation between two financial factors. The below table reflects financial details of company.

FINANCIAL STATEMENT ANAYLYSIS – Stockland Company

Company name: Stockland Company

Company ticker: STKAF

Every organization needs to use the effective financial management to raise and

deploy the funds from the market. It is the process to raise the funds or capital from the

market and deploy the same in the business functioning with an objective to create value on

the investment. There are several financial tools which could be used to assess the financial

performance of company such as ratio analysis, du pont analysis, capital budgeting tool and

financial theories. In this report, three years of financial performance of company has been

assessed to determine whether company has performed well or negative in market. In the first

part of the report, ratio analysis have been used to assess the financial performance of

company and after that capital structure of company has been assessed to determine whether

company has equilibrium point in its financial leverage and cost of capital. After that,

liquidity position of company in the latest financial year has been evaluated to determine

whether company would be able to meet its current liabilities or not. In the end, quality of the

financial statement has been analysed.

Description of company

Stockland Corporation is diversified Australian corporation property Development Company

which has been running its business on international level. This company has business in

shopping centres, housing estates, industrial estates and retirement vilages. This company has

been running its business on international level and all the employees are accustomed to act

as per the directions and instruction of its CEO named Mark Steinert. As per the ASX:SGP,

the share price of company has gone down and reflected 4.14 AUD −0.035 (0.84%)

(Stockland Company, 2017).

Task-1

Assess the company’s performance over the last three years

The ratio analysis is used to assess the financial performance of company and establish the

relation between two financial factors. The below table reflects financial details of company.

FINANCIAL STATEMENT ANAYLYSIS – Stockland Company

Company name: Stockland Company

Company ticker: STKAF

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

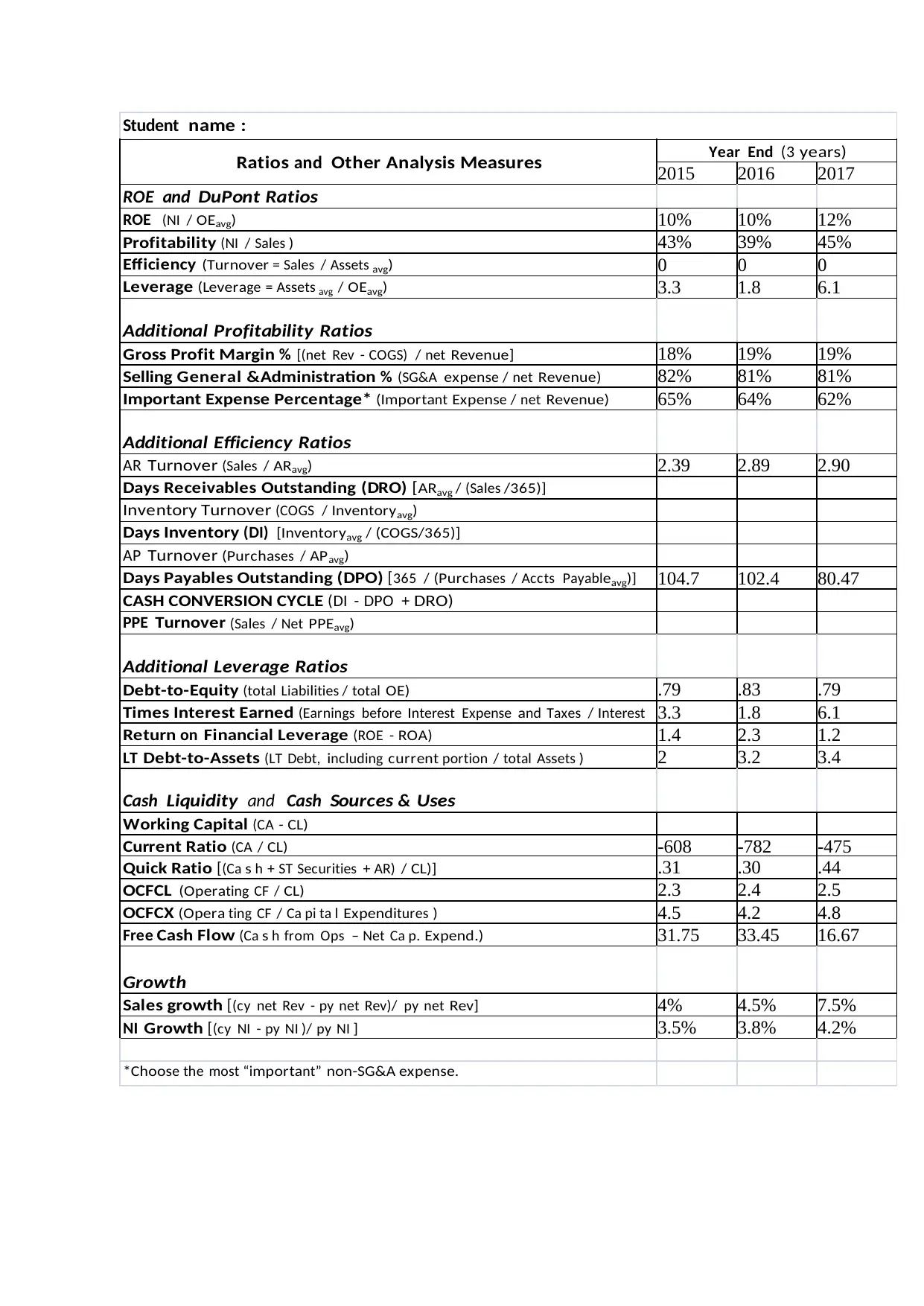

Student name :

Ratios and Other Analysis Measures Year End (3 y ea r s)

2015 2016 2017

ROE and DuPont Ratios

ROE (NI / OE avg ) 10% 10% 12%

Profitability (NI / Sa les ) 43% 39% 45%

Efficiency (Turnover = Sa les / Assets avg ) 0 0 0

Leverage (Leverage = Assets avg / OE avg ) 3.3 1.8 6.1

Additional Profitability Ratios

Gross Profit Margin % [(net Rev - COGS) / net Revenue] 18% 19% 19%

Selling General &Administration % (SG&A expense / net Revenue) 82% 81% 81%

Important Expense Percentage* (Important Expense / net Revenue) 65% 64% 62%

Additional Efficiency Ratios

AR Turnover (Sa les / AR avg ) 2.39 2.89 2.90

Days Receivables Outstanding (DRO) [ AR avg / (Sa les /365)]

Inventory Turnover (COGS / Inventory avg )

Days Inventory (DI) [Inventoryavg / (COGS/365)]

AP Turnover (Purchases / AP avg )

Days Payables Outstanding (DPO) [365 / (Purchases / Accts Payabl e avg )] 104.7 102.4 80.47

CASH CONVERSION CYCLE (DI - DPO + D RO)

PPE Turnover (Sa les / Net PPE avg )

Additional Leverage Ratios

Debt-to-Equity (total Li abi lities / total OE) .79 .83 .79

Times Interest Earned (Earnings before Interest Expense and Taxes / Interest

Exp)

3.3 1.8 6.1

Return on Financial Leverage (ROE - ROA) 1.4 2.3 1.2

LT Debt-to-Assets (LT Debt, including current portion / total Assets ) 2 3.2 3.4

Cash Liquidity and Cash Sources & Uses

Working Capital (CA - CL)

Current Ratio (CA / CL) -608 -782 -475

Quick Ratio [(Ca s h + ST Securities + AR) / CL)] .31 .30 .44

OCFCL (Operating CF / CL) 2.3 2.4 2.5

OCFCX (Opera ting CF / Ca pi ta l Expenditures ) 4.5 4.2 4.8

Free Cash Flow (Ca s h from Ops – Net Ca p. Expend.) 31.75 33.45 16.67

Growth

Sales growth [(cy net Rev - py net Rev)/ py net Rev] 4% 4.5% 7.5%

NI Growth [(cy NI - py NI )/ py NI ] 3.5% 3.8% 4.2%

*Choose the most “i mportant” non-SG&A expense.

Ratios and Other Analysis Measures Year End (3 y ea r s)

2015 2016 2017

ROE and DuPont Ratios

ROE (NI / OE avg ) 10% 10% 12%

Profitability (NI / Sa les ) 43% 39% 45%

Efficiency (Turnover = Sa les / Assets avg ) 0 0 0

Leverage (Leverage = Assets avg / OE avg ) 3.3 1.8 6.1

Additional Profitability Ratios

Gross Profit Margin % [(net Rev - COGS) / net Revenue] 18% 19% 19%

Selling General &Administration % (SG&A expense / net Revenue) 82% 81% 81%

Important Expense Percentage* (Important Expense / net Revenue) 65% 64% 62%

Additional Efficiency Ratios

AR Turnover (Sa les / AR avg ) 2.39 2.89 2.90

Days Receivables Outstanding (DRO) [ AR avg / (Sa les /365)]

Inventory Turnover (COGS / Inventory avg )

Days Inventory (DI) [Inventoryavg / (COGS/365)]

AP Turnover (Purchases / AP avg )

Days Payables Outstanding (DPO) [365 / (Purchases / Accts Payabl e avg )] 104.7 102.4 80.47

CASH CONVERSION CYCLE (DI - DPO + D RO)

PPE Turnover (Sa les / Net PPE avg )

Additional Leverage Ratios

Debt-to-Equity (total Li abi lities / total OE) .79 .83 .79

Times Interest Earned (Earnings before Interest Expense and Taxes / Interest

Exp)

3.3 1.8 6.1

Return on Financial Leverage (ROE - ROA) 1.4 2.3 1.2

LT Debt-to-Assets (LT Debt, including current portion / total Assets ) 2 3.2 3.4

Cash Liquidity and Cash Sources & Uses

Working Capital (CA - CL)

Current Ratio (CA / CL) -608 -782 -475

Quick Ratio [(Ca s h + ST Securities + AR) / CL)] .31 .30 .44

OCFCL (Operating CF / CL) 2.3 2.4 2.5

OCFCX (Opera ting CF / Ca pi ta l Expenditures ) 4.5 4.2 4.8

Free Cash Flow (Ca s h from Ops – Net Ca p. Expend.) 31.75 33.45 16.67

Growth

Sales growth [(cy net Rev - py net Rev)/ py net Rev] 4% 4.5% 7.5%

NI Growth [(cy NI - py NI )/ py NI ] 3.5% 3.8% 4.2%

*Choose the most “i mportant” non-SG&A expense.

Assessment of the financial position of company

PROFITABILITY RATIOS

This ratio measures profitability of the company. It includes net profit margin, gross profit to

sales and return on equity available to equity shareholders of company. The net profit of

company has increased by 3% and resulted to 45% in 2017. It has increased its net profit with

the increase in its overall turnover. The gross profit margin has also increased to 19% in 2017

which is 3% higher since 2015. It reflects that company has decreased its overall expenses

and increased overall turnover. The return on equity of company has increased to 12% in

2017 which is 2% higher since last three years. It reflects that company has increased overall

return available to equity shareholders with the increase in its overall gross profit (Ehiedu,

2014).

EFFECIENCY RATIO OR ACTIVITY RATIO

This ratio measures company’s ability to deploy its funds in its business activities. this

ratio is consists of assets turnover ratio, receivable turnover ratio, inventory turnover ratio

and payable turnover ratio (Ehiedu, 2014).

The assets turnover ratio of company has increased by 19 points since last three years which

reflects that company has increased its efficiency to deploy funds in its assets to increase the

overall turnover. The receivable turnover ratio has increased to 2.90 points in 2017 which

is .40 points higher as compared to last three year data. It has reflected that company has

created value on the investment. Company has zero level of inventory in its business.

Therefore, company has blocked zero investment in keeping the inventory for its business

(Stockland Company, 2017).

LIQUIDITY RATIOS

The liquidity ratio measures company’s ability to cover its all short term and long term debts

out of its available current asset. Company has increased its current ratio to .44 in 2017 which

is .15 points higher as compared to last three year data. Stockland company has zero level of

inventory in its business which reflects that company has same current and quick ratio

(Flannery, 2016).

PROFITABILITY RATIOS

This ratio measures profitability of the company. It includes net profit margin, gross profit to

sales and return on equity available to equity shareholders of company. The net profit of

company has increased by 3% and resulted to 45% in 2017. It has increased its net profit with

the increase in its overall turnover. The gross profit margin has also increased to 19% in 2017

which is 3% higher since 2015. It reflects that company has decreased its overall expenses

and increased overall turnover. The return on equity of company has increased to 12% in

2017 which is 2% higher since last three years. It reflects that company has increased overall

return available to equity shareholders with the increase in its overall gross profit (Ehiedu,

2014).

EFFECIENCY RATIO OR ACTIVITY RATIO

This ratio measures company’s ability to deploy its funds in its business activities. this

ratio is consists of assets turnover ratio, receivable turnover ratio, inventory turnover ratio

and payable turnover ratio (Ehiedu, 2014).

The assets turnover ratio of company has increased by 19 points since last three years which

reflects that company has increased its efficiency to deploy funds in its assets to increase the

overall turnover. The receivable turnover ratio has increased to 2.90 points in 2017 which

is .40 points higher as compared to last three year data. It has reflected that company has

created value on the investment. Company has zero level of inventory in its business.

Therefore, company has blocked zero investment in keeping the inventory for its business

(Stockland Company, 2017).

LIQUIDITY RATIOS

The liquidity ratio measures company’s ability to cover its all short term and long term debts

out of its available current asset. Company has increased its current ratio to .44 in 2017 which

is .15 points higher as compared to last three year data. Stockland company has zero level of

inventory in its business which reflects that company has same current and quick ratio

(Flannery, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPITAL STRUCTURE RATIOS

The capital structure ratio reflects the debt to equity and time interest coverage ratio. This

ratio reflects how well company has managed its capital structure to lower down the financial

leverage and cost of capital (Grant, 2016).

Time interest earned ratio

This ratio reflects how well company has covered its interest out of its earnings before

interest and tax. Stockland has increased its time interest ratio to 6.1 points in 2017 which is 3

points higher as compared to last three year data. It reflects that company has been managing

its interest payment very well out of its earning. However, company has to consistently

increase its time interest coverage ratio to lower down its financial leverage (Jordan, 2014).

Debt to equity ratio

This ratio reflects the debt and equity capital structure of company. Company has lower

down the debt to equity ratio to 76% in 2017 which is 3 % lower since last three years. it has

divulge that company has lower down debt portion from its capital structure. It has reflected

that company has low cost of capital and high financial leverage in its business (Mwangi, and

Murigu, 2015).

Task-2

Long-term solvency of the company over the last three years

The long term solvency of company determines the sustainability of the organisation in long

run. The financial leverage and profitability plays pivotal role in determination of the long

term solvency of the company. It is analyzed that company has kept the debt to equity ratio

to 76% in 2017 which reflects that company has kept high debt portion in its capital structure.

This high debt capital structure poses high amount of financial leverage to company. The

financial leverage reflects that company might face issue to cover its interest payment out of

its available earnings before interest and tax (Stockland Company, 2017).

The capital structure ratio reflects the debt to equity and time interest coverage ratio. This

ratio reflects how well company has managed its capital structure to lower down the financial

leverage and cost of capital (Grant, 2016).

Time interest earned ratio

This ratio reflects how well company has covered its interest out of its earnings before

interest and tax. Stockland has increased its time interest ratio to 6.1 points in 2017 which is 3

points higher as compared to last three year data. It reflects that company has been managing

its interest payment very well out of its earning. However, company has to consistently

increase its time interest coverage ratio to lower down its financial leverage (Jordan, 2014).

Debt to equity ratio

This ratio reflects the debt and equity capital structure of company. Company has lower

down the debt to equity ratio to 76% in 2017 which is 3 % lower since last three years. it has

divulge that company has lower down debt portion from its capital structure. It has reflected

that company has low cost of capital and high financial leverage in its business (Mwangi, and

Murigu, 2015).

Task-2

Long-term solvency of the company over the last three years

The long term solvency of company determines the sustainability of the organisation in long

run. The financial leverage and profitability plays pivotal role in determination of the long

term solvency of the company. It is analyzed that company has kept the debt to equity ratio

to 76% in 2017 which reflects that company has kept high debt portion in its capital structure.

This high debt capital structure poses high amount of financial leverage to company. The

financial leverage reflects that company might face issue to cover its interest payment out of

its available earnings before interest and tax (Stockland Company, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

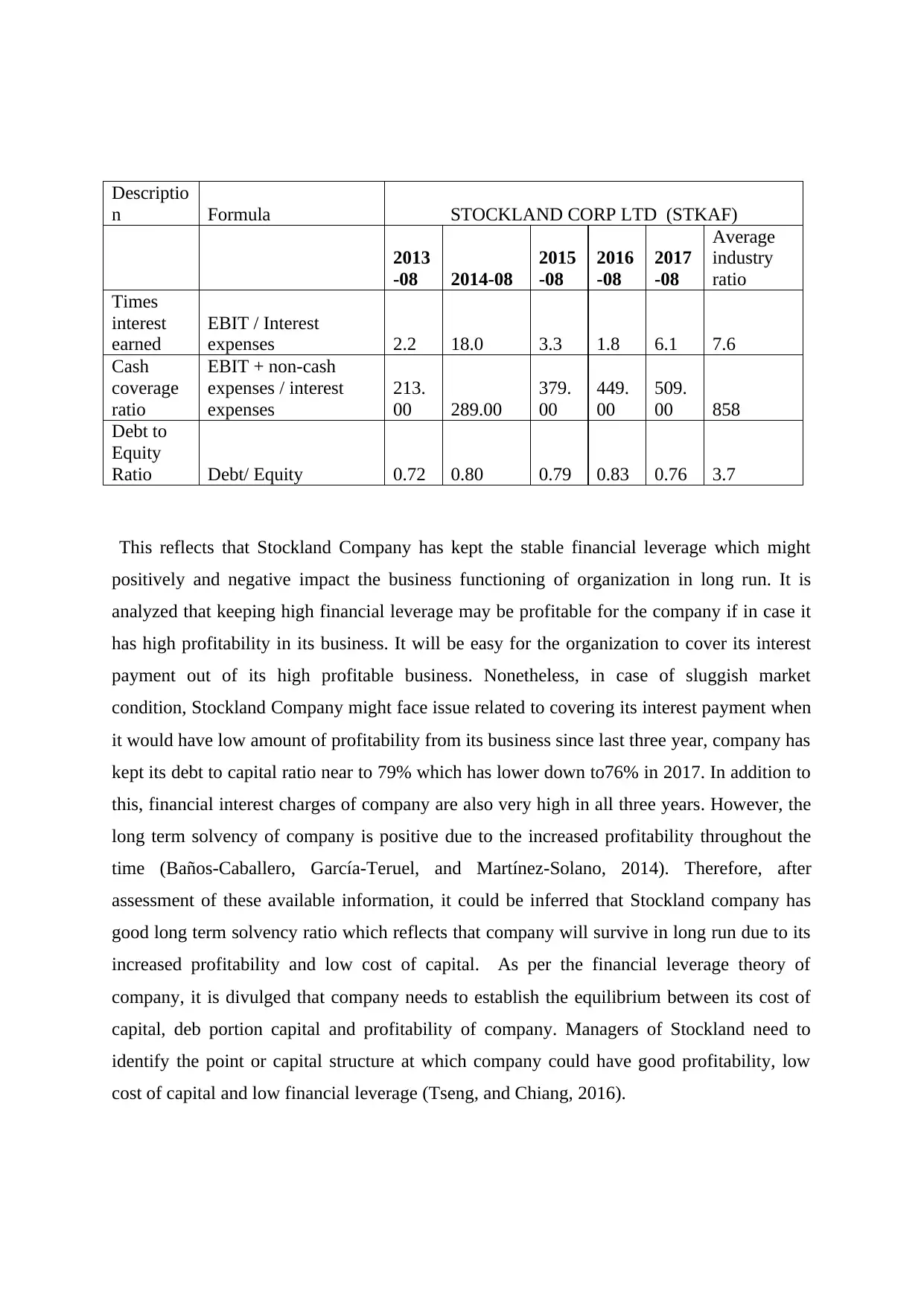

Descriptio

n Formula STOCKLAND CORP LTD (STKAF)

2013

-08 2014-08

2015

-08

2016

-08

2017

-08

Average

industry

ratio

Times

interest

earned

EBIT / Interest

expenses 2.2 18.0 3.3 1.8 6.1 7.6

Cash

coverage

ratio

EBIT + non-cash

expenses / interest

expenses

213.

00 289.00

379.

00

449.

00

509.

00 858

Debt to

Equity

Ratio Debt/ Equity 0.72 0.80 0.79 0.83 0.76 3.7

This reflects that Stockland Company has kept the stable financial leverage which might

positively and negative impact the business functioning of organization in long run. It is

analyzed that keeping high financial leverage may be profitable for the company if in case it

has high profitability in its business. It will be easy for the organization to cover its interest

payment out of its high profitable business. Nonetheless, in case of sluggish market

condition, Stockland Company might face issue related to covering its interest payment when

it would have low amount of profitability from its business since last three year, company has

kept its debt to capital ratio near to 79% which has lower down to76% in 2017. In addition to

this, financial interest charges of company are also very high in all three years. However, the

long term solvency of company is positive due to the increased profitability throughout the

time (Baños-Caballero, García-Teruel, and Martínez-Solano, 2014). Therefore, after

assessment of these available information, it could be inferred that Stockland company has

good long term solvency ratio which reflects that company will survive in long run due to its

increased profitability and low cost of capital. As per the financial leverage theory of

company, it is divulged that company needs to establish the equilibrium between its cost of

capital, deb portion capital and profitability of company. Managers of Stockland need to

identify the point or capital structure at which company could have good profitability, low

cost of capital and low financial leverage (Tseng, and Chiang, 2016).

n Formula STOCKLAND CORP LTD (STKAF)

2013

-08 2014-08

2015

-08

2016

-08

2017

-08

Average

industry

ratio

Times

interest

earned

EBIT / Interest

expenses 2.2 18.0 3.3 1.8 6.1 7.6

Cash

coverage

ratio

EBIT + non-cash

expenses / interest

expenses

213.

00 289.00

379.

00

449.

00

509.

00 858

Debt to

Equity

Ratio Debt/ Equity 0.72 0.80 0.79 0.83 0.76 3.7

This reflects that Stockland Company has kept the stable financial leverage which might

positively and negative impact the business functioning of organization in long run. It is

analyzed that keeping high financial leverage may be profitable for the company if in case it

has high profitability in its business. It will be easy for the organization to cover its interest

payment out of its high profitable business. Nonetheless, in case of sluggish market

condition, Stockland Company might face issue related to covering its interest payment when

it would have low amount of profitability from its business since last three year, company has

kept its debt to capital ratio near to 79% which has lower down to76% in 2017. In addition to

this, financial interest charges of company are also very high in all three years. However, the

long term solvency of company is positive due to the increased profitability throughout the

time (Baños-Caballero, García-Teruel, and Martínez-Solano, 2014). Therefore, after

assessment of these available information, it could be inferred that Stockland company has

good long term solvency ratio which reflects that company will survive in long run due to its

increased profitability and low cost of capital. As per the financial leverage theory of

company, it is divulged that company needs to establish the equilibrium between its cost of

capital, deb portion capital and profitability of company. Managers of Stockland need to

identify the point or capital structure at which company could have good profitability, low

cost of capital and low financial leverage (Tseng, and Chiang, 2016).

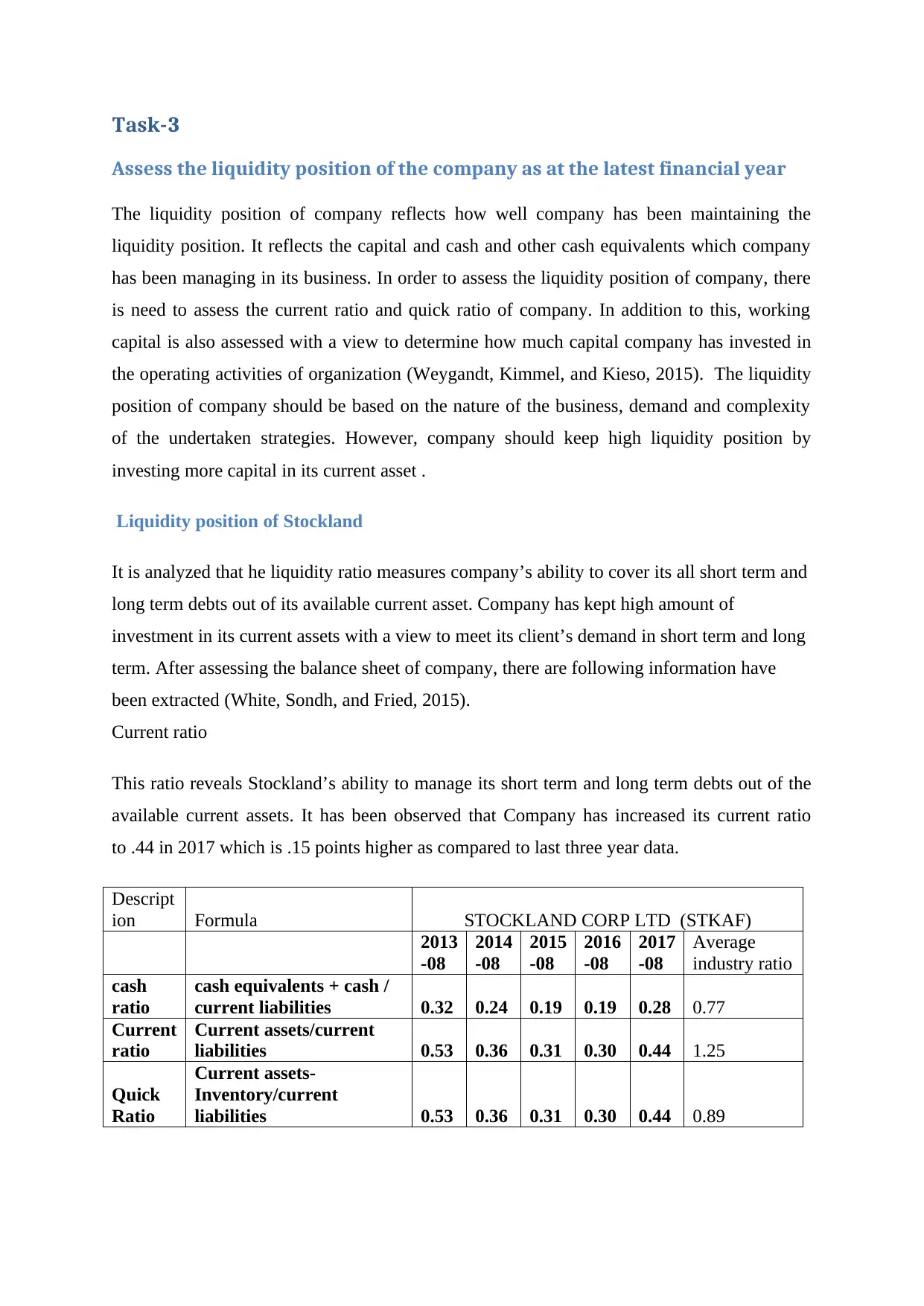

Task-3

Assess the liquidity position of the company as at the latest financial year

The liquidity position of company reflects how well company has been maintaining the

liquidity position. It reflects the capital and cash and other cash equivalents which company

has been managing in its business. In order to assess the liquidity position of company, there

is need to assess the current ratio and quick ratio of company. In addition to this, working

capital is also assessed with a view to determine how much capital company has invested in

the operating activities of organization (Weygandt, Kimmel, and Kieso, 2015). The liquidity

position of company should be based on the nature of the business, demand and complexity

of the undertaken strategies. However, company should keep high liquidity position by

investing more capital in its current asset .

Liquidity position of Stockland

It is analyzed that he liquidity ratio measures company’s ability to cover its all short term and

long term debts out of its available current asset. Company has kept high amount of

investment in its current assets with a view to meet its client’s demand in short term and long

term. After assessing the balance sheet of company, there are following information have

been extracted (White, Sondh, and Fried, 2015).

Current ratio

This ratio reveals Stockland’s ability to manage its short term and long term debts out of the

available current assets. It has been observed that Company has increased its current ratio

to .44 in 2017 which is .15 points higher as compared to last three year data.

Descript

ion Formula STOCKLAND CORP LTD (STKAF)

2013

-08

2014

-08

2015

-08

2016

-08

2017

-08

Average

industry ratio

cash

ratio

cash equivalents + cash /

current liabilities 0.32 0.24 0.19 0.19 0.28 0.77

Current

ratio

Current assets/current

liabilities 0.53 0.36 0.31 0.30 0.44 1.25

Quick

Ratio

Current assets-

Inventory/current

liabilities 0.53 0.36 0.31 0.30 0.44 0.89

Assess the liquidity position of the company as at the latest financial year

The liquidity position of company reflects how well company has been maintaining the

liquidity position. It reflects the capital and cash and other cash equivalents which company

has been managing in its business. In order to assess the liquidity position of company, there

is need to assess the current ratio and quick ratio of company. In addition to this, working

capital is also assessed with a view to determine how much capital company has invested in

the operating activities of organization (Weygandt, Kimmel, and Kieso, 2015). The liquidity

position of company should be based on the nature of the business, demand and complexity

of the undertaken strategies. However, company should keep high liquidity position by

investing more capital in its current asset .

Liquidity position of Stockland

It is analyzed that he liquidity ratio measures company’s ability to cover its all short term and

long term debts out of its available current asset. Company has kept high amount of

investment in its current assets with a view to meet its client’s demand in short term and long

term. After assessing the balance sheet of company, there are following information have

been extracted (White, Sondh, and Fried, 2015).

Current ratio

This ratio reveals Stockland’s ability to manage its short term and long term debts out of the

available current assets. It has been observed that Company has increased its current ratio

to .44 in 2017 which is .15 points higher as compared to last three year data.

Descript

ion Formula STOCKLAND CORP LTD (STKAF)

2013

-08

2014

-08

2015

-08

2016

-08

2017

-08

Average

industry ratio

cash

ratio

cash equivalents + cash /

current liabilities 0.32 0.24 0.19 0.19 0.28 0.77

Current

ratio

Current assets/current

liabilities 0.53 0.36 0.31 0.30 0.44 1.25

Quick

Ratio

Current assets-

Inventory/current

liabilities 0.53 0.36 0.31 0.30 0.44 0.89

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratio

The quick ratio reflects immediate cash position or liquid cash which company could use to

meet its short term and long term debt. It is observed that Stockland Company has zero level

of inventory in its business which reflects that company has same current and quick ratio

(Delen, Kuzey, and Uyar, 2013).

This above given calculation has reflected that company has kept high good amount of

liquidation in its operation. It is considered that on the basis of last three year data and market

factors, company might have high demand of its products and services offered in market.

Therefore, keeping the high liquidation in the process is very much required to meet the

client’s demand in long run (Williams, and Best, 2014).

After assessing the other details and data of market, it is inferred that company needs to keep

its liquidation high by keeping the high investment in its current assets. The working capital

of company should be adequate enough which could assist Stockland to meet its current and

future demand of clients in long run (Wong, and Li, 2015).

Task-4

Discuss the quality of financial statement

Stockland Company has been running its business on international level and listed on

several stock exchanges. It has been observed that company has been following the IFRS rule

and standards while preparing the financial statements of company. Stockland Company has

followed international reporting frameworks to report its financial statement with the

reporting authorities on international level and kept its business and financial transactions

more transparent. It has been assessed that quality of financial statement could be assessed by

evaluating the auditors comment and evaluating the auditor’s report on the prepared financial

statements (Babalola, and biola, 2013). As per the annual report of company, it is considered

that company has created impairment loss of AUD $ 224 million in its business. As per the

IAS- 136 of the IFRS rules and standards, it is considered that company has yearly booked

the impairment loss in its books of account to match the book value of the assets with its

market value. All the financial statements of company have been prepared as consolidated

financial statements. The quality of financial statement has been kept high by strengthen the

The quick ratio reflects immediate cash position or liquid cash which company could use to

meet its short term and long term debt. It is observed that Stockland Company has zero level

of inventory in its business which reflects that company has same current and quick ratio

(Delen, Kuzey, and Uyar, 2013).

This above given calculation has reflected that company has kept high good amount of

liquidation in its operation. It is considered that on the basis of last three year data and market

factors, company might have high demand of its products and services offered in market.

Therefore, keeping the high liquidation in the process is very much required to meet the

client’s demand in long run (Williams, and Best, 2014).

After assessing the other details and data of market, it is inferred that company needs to keep

its liquidation high by keeping the high investment in its current assets. The working capital

of company should be adequate enough which could assist Stockland to meet its current and

future demand of clients in long run (Wong, and Li, 2015).

Task-4

Discuss the quality of financial statement

Stockland Company has been running its business on international level and listed on

several stock exchanges. It has been observed that company has been following the IFRS rule

and standards while preparing the financial statements of company. Stockland Company has

followed international reporting frameworks to report its financial statement with the

reporting authorities on international level and kept its business and financial transactions

more transparent. It has been assessed that quality of financial statement could be assessed by

evaluating the auditors comment and evaluating the auditor’s report on the prepared financial

statements (Babalola, and biola, 2013). As per the annual report of company, it is considered

that company has created impairment loss of AUD $ 224 million in its business. As per the

IAS- 136 of the IFRS rules and standards, it is considered that company has yearly booked

the impairment loss in its books of account to match the book value of the assets with its

market value. All the financial statements of company have been prepared as consolidated

financial statements. The quality of financial statement has been kept high by strengthen the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transparency of the all the details and financial statements (Zhang, and Zhang, 2014). The

directors and managers are accountable for preparation and authorisation of financial

statements and responsible for ensuring the integrity and quality of the financial reporting. In

order to strengthen the quality of the financial statement, directors and managers have issued

management representation latter with tis financial statements (Brigham, Ehrhardt, Nason,

and Gessaroli, 2016).

Furthermore, the quality of the financial statements is also based on the shared imperative

information in the financial statements. Stockland Company has shared all the required

details and imperative information which may be price sensitive to its investors. This type of

practice not only curbs the insider trading practice in organization but also lower down the

financial fluctuation in its stock price. Stockland Company has presented all its financial

information in accordance with the generally accepted accounting principles. In addition to

this, auditor’s plays play important role in improving the quality of the financial reporting. In

the latest shared financial statement of company, auditors have given qualified report on the

disclosed information in the annual report. It divulges that company has complied with the all

the applicable rules and regulations while preparing the financial statement. Nonetheless, in

the contrary to its domestic and international regulatory compliance program, company has

complied with the IFRS rules and standards while preparing the financial statements. It has

not only strengthened the transparency of its business transactions but also increase its overall

brand image on international level. The financial management authority has also cut down

the immaterial details from the financial statement of company to increase the quality of its

shared financial statement. It is analyzed that the clear, concise, and effective financial

information helps investors to make the better-informed investment decisions (Stockland

Company, 2017). Therefore, now in the end, it could be inferred that the quality of the

financial statement prepared by company is very good and it is already backed by the auditors

comment an qualified report.

Conclusion

After assessing the annual report and financial statement of company, it could be

inferred that company will have sustainable business practice. It has been observed that

Stockland Company has kept the stable financial leverage which might positively and

negative impact the business functioning of organization in long run. It is analyzed that

directors and managers are accountable for preparation and authorisation of financial

statements and responsible for ensuring the integrity and quality of the financial reporting. In

order to strengthen the quality of the financial statement, directors and managers have issued

management representation latter with tis financial statements (Brigham, Ehrhardt, Nason,

and Gessaroli, 2016).

Furthermore, the quality of the financial statements is also based on the shared imperative

information in the financial statements. Stockland Company has shared all the required

details and imperative information which may be price sensitive to its investors. This type of

practice not only curbs the insider trading practice in organization but also lower down the

financial fluctuation in its stock price. Stockland Company has presented all its financial

information in accordance with the generally accepted accounting principles. In addition to

this, auditor’s plays play important role in improving the quality of the financial reporting. In

the latest shared financial statement of company, auditors have given qualified report on the

disclosed information in the annual report. It divulges that company has complied with the all

the applicable rules and regulations while preparing the financial statement. Nonetheless, in

the contrary to its domestic and international regulatory compliance program, company has

complied with the IFRS rules and standards while preparing the financial statements. It has

not only strengthened the transparency of its business transactions but also increase its overall

brand image on international level. The financial management authority has also cut down

the immaterial details from the financial statement of company to increase the quality of its

shared financial statement. It is analyzed that the clear, concise, and effective financial

information helps investors to make the better-informed investment decisions (Stockland

Company, 2017). Therefore, now in the end, it could be inferred that the quality of the

financial statement prepared by company is very good and it is already backed by the auditors

comment an qualified report.

Conclusion

After assessing the annual report and financial statement of company, it could be

inferred that company will have sustainable business practice. It has been observed that

Stockland Company has kept the stable financial leverage which might positively and

negative impact the business functioning of organization in long run. It is analyzed that

keeping high financial leverage may be profitable for the company if in case it has high

profitability in its business and if the profitability of company is not adequate enough to

cover the interest payment then company may go in winding up. Now in the end, it could be

inferred that company should maintain the effective debt to equity ratio and liquidity position

should also be adequate enough to cover the market demand of the organization. The quality

of financial statement of company could also be increased if company follow the proper IFRS

rules and regulations in its reporting frameworks.

profitability in its business and if the profitability of company is not adequate enough to

cover the interest payment then company may go in winding up. Now in the end, it could be

inferred that company should maintain the effective debt to equity ratio and liquidity position

should also be adequate enough to cover the market demand of the organization. The quality

of financial statement of company could also be increased if company follow the proper IFRS

rules and regulations in its reporting frameworks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.