ACC320 Research: Shareholder Value vs Stakeholder Value Governance

VerifiedAdded on 2023/06/04

|14

|3396

|255

Report

AI Summary

This research proposal for ACC320 Contemporary Issues in Accounting examines the ongoing debate between prioritizing shareholder value versus stakeholder value in modern corporate governance. It introduces the practical and theoretical motivations behind the research, highlighting the need for companies to balance immediate financial value for shareholders with comprehensive and sustainable value for stakeholders. The literature review explores various theories, including the social contract, triple bottom line, and stakeholder theory, while also pointing out the limitations of agency theory. The proposal presents two hypotheses: that companies focusing on stakeholders perform better, and that there is no significant difference between stakeholder and shareholder value. The ultimate aim is to determine whether prioritizing shareholders yields more value than focusing on stakeholders in the context of contemporary corporate governance.

Shareholder value vs Stakeholder value in Modern Corporate Governance 1

ACC320 Contemporary Issues in Accounting

Research Proposal

Student Name:

Student ID:

Title:

Submission Date:

ACC320 Contemporary Issues in Accounting

Research Proposal

Student Name:

Student ID:

Title:

Submission Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder value vs Stakeholder value in Modern Corporate Governance 2

Introduction:

Should corporate governances focus more on fulfilling the interest of shareholders or should it

focus more on stakeholders? This is one of the challenges faced by most of the companies. The

challenge started following the introduction of idea of sustainable reporting. Determining the answer to

this question would be handy not only for academic purposes but also for companies wishing to know

the direction they should take.

Practical Motivation:

Ability to answer the question as to whether corporate governance should focus more on

fulfilling the interest of shareholders or whether it should focus more on stakeholders is very crucial to

companies, accountants, shareholders and all stakeholders. This is because shareholders and business

managers are increasingly faced with a double imperative (Carlsson 2007) to integrate a creation of

immediate financial value for shareholders (or Shareholders) and creation of comprehensive and

sustainable value for stakeholders (or stakeholders). The lifting of this contradiction requires them to

master eclectic models in the fields of economics and law, but also sociology and ethics (Carlsson

2007). Aligning their decisions, discourses and behaviours with CSR repositories implies a

reconfiguration of their governance system. The corporate governance (corporate governance) covers

all the institutions, rules and practices that legitimize the power of leaders (Carlsson 2007).

Theoretical Motivation:

The current research will expand and perhaps give some recommendation on how the current

theories should be adjusted to meet the new demands brought about by the issue of sustainable

reporting. According to the traditional approach, it assumes that the incentive and control systems of

the latter depend in particular on the firm's financing structure, and more particularly on the

composition of its shareholding (Porta et al., 1997). According to the extended approach to

governance, supported in particular by Charreaux and Desbrieres, (1998), the problem of the

effectiveness of governance systems can only be posed within the framework extended to all

stakeholders. It must be studied from a systemic perspective, considering the firm's concrete value

Introduction:

Should corporate governances focus more on fulfilling the interest of shareholders or should it

focus more on stakeholders? This is one of the challenges faced by most of the companies. The

challenge started following the introduction of idea of sustainable reporting. Determining the answer to

this question would be handy not only for academic purposes but also for companies wishing to know

the direction they should take.

Practical Motivation:

Ability to answer the question as to whether corporate governance should focus more on

fulfilling the interest of shareholders or whether it should focus more on stakeholders is very crucial to

companies, accountants, shareholders and all stakeholders. This is because shareholders and business

managers are increasingly faced with a double imperative (Carlsson 2007) to integrate a creation of

immediate financial value for shareholders (or Shareholders) and creation of comprehensive and

sustainable value for stakeholders (or stakeholders). The lifting of this contradiction requires them to

master eclectic models in the fields of economics and law, but also sociology and ethics (Carlsson

2007). Aligning their decisions, discourses and behaviours with CSR repositories implies a

reconfiguration of their governance system. The corporate governance (corporate governance) covers

all the institutions, rules and practices that legitimize the power of leaders (Carlsson 2007).

Theoretical Motivation:

The current research will expand and perhaps give some recommendation on how the current

theories should be adjusted to meet the new demands brought about by the issue of sustainable

reporting. According to the traditional approach, it assumes that the incentive and control systems of

the latter depend in particular on the firm's financing structure, and more particularly on the

composition of its shareholding (Porta et al., 1997). According to the extended approach to

governance, supported in particular by Charreaux and Desbrieres, (1998), the problem of the

effectiveness of governance systems can only be posed within the framework extended to all

stakeholders. It must be studied from a systemic perspective, considering the firm's concrete value

Shareholder value vs Stakeholder value in Modern Corporate Governance 3

creation processes. This prescription responds to the criticisms made by Rajan and Zingalès (2001)

against the purely shareholder view of governance, which they believe is inappropriate for new forms

of enterprise. Through "responsible governance", directors and company leaders must seek to integrate

economic goals, social and environmental intentions (Perez, 2005). The new model would be based on

modifying and tailoring the existing theories to match the new needs of corporate governance theory.

This is because there are gaps on how the need to focus on shareholders and the need to focus on

stakeholders should be reconciled.

Literature Review:

The notion of corporate governance is based, according to Donaldson and Preston (1995), on

the concept of "social contract" between the company and its direct stakeholders (shareholders,

employees, suppliers, customers, etc.) and indirect (administrations, local communities, interest

groups, opinion leaders, civil society ...). It is defined by the European Commission as companies

voluntary integration of social and environmental concerns into their business activities and

relationships with their stakeholders "(Green Paper, 2001). It was notably translated by the notion of

Triple Bottom Line (Elkington, 1998), which is based on three pillars respectively economic (the

search for profitability and sustainability of the company), social and societal (the quest for social

equity and respect for human rights) , and environmental (the desire to protect the environment and

preserve natural resources). Carroll (1991) proposes a four-tier pyramid of corporate CSR: economic

responsibilities, which force the company to produce and make profits; legal responsibilities that

require the company to comply with applicable legislation and standards; philanthropic

responsibilities, which reflect the company's desire to improve the well-being of society; ethical

responsibilities.

The contractual theories and the instrumental approach to agency theory offer great proximity

in that they focus on a single managerial objective, namely value creation, analyzed in the first case

according to a purely shareholder and, in the second case, a partnership approach (Bradley, Schipani,

Sundaram and Walsh 1999). Stakeholder’s theory differs from the first in the sense that it is the social

creation processes. This prescription responds to the criticisms made by Rajan and Zingalès (2001)

against the purely shareholder view of governance, which they believe is inappropriate for new forms

of enterprise. Through "responsible governance", directors and company leaders must seek to integrate

economic goals, social and environmental intentions (Perez, 2005). The new model would be based on

modifying and tailoring the existing theories to match the new needs of corporate governance theory.

This is because there are gaps on how the need to focus on shareholders and the need to focus on

stakeholders should be reconciled.

Literature Review:

The notion of corporate governance is based, according to Donaldson and Preston (1995), on

the concept of "social contract" between the company and its direct stakeholders (shareholders,

employees, suppliers, customers, etc.) and indirect (administrations, local communities, interest

groups, opinion leaders, civil society ...). It is defined by the European Commission as companies

voluntary integration of social and environmental concerns into their business activities and

relationships with their stakeholders "(Green Paper, 2001). It was notably translated by the notion of

Triple Bottom Line (Elkington, 1998), which is based on three pillars respectively economic (the

search for profitability and sustainability of the company), social and societal (the quest for social

equity and respect for human rights) , and environmental (the desire to protect the environment and

preserve natural resources). Carroll (1991) proposes a four-tier pyramid of corporate CSR: economic

responsibilities, which force the company to produce and make profits; legal responsibilities that

require the company to comply with applicable legislation and standards; philanthropic

responsibilities, which reflect the company's desire to improve the well-being of society; ethical

responsibilities.

The contractual theories and the instrumental approach to agency theory offer great proximity

in that they focus on a single managerial objective, namely value creation, analyzed in the first case

according to a purely shareholder and, in the second case, a partnership approach (Bradley, Schipani,

Sundaram and Walsh 1999). Stakeholder’s theory differs from the first in the sense that it is the social

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shareholder value vs Stakeholder value in Modern Corporate Governance 4

integration of the economic entity that takes precedence over the creation of financial value. Societal

information is of intrinsic value here in that it explains the impact of the company's activity and

therefore its way of carrying out transactions or exchanges with its environment. As such, the societal

reporting fulfils a justification function, that is to say that it is interested in the role of the company in

these exchanges: how does the company respond to the expectations expressed by the actors in society

and what does it get in return? Societal reporting is used as a mechanism for clearing and maintaining

the social contract that authorizes and organizes exchanges between the company and the various

actors of society (Bradley, Schipani, Sundaram and Walsh 1999). Although the instrumental view of

stakeholder theory opposes the goal of maximizing value creation for shareholders alone, advocated by

agency theory, it nonetheless advocates cost-effective management which favors the continuity of the

operation and thus the maintenance of the jobs and the respect of the contractual conditions concluded

with the suppliers, the customers and the creditors. Its ambitions thus seem consistent with those of the

theory of dependence on resources, according to which social responsibility must be combined with

financial logic, via considering the firm's strategy the stakeholder requirements it needs to survive

(Pfeffer and Salancik, 1978). Only social and environmental actions facilitating access to new

resources therefore seem to have to be privileged.

Alignment with these frames of reference implies a reconsideration of the theory of

governance, because it partially calls into question the purpose of the company, defined by the

classical theory (Freeman 1984), which aims to reduce agency costs, securing the investor's capital and

seeking profit in the short term. This alignment extends the company's responsibilities both over time

(in the long term) and in the socio-economic space (stakeholders). Blair (1995) the concept of

pluralistic enterprise (or plural firm) open to its partners, to that of monist company centered on its

shareholders. This pluralistic representation of the firm implies a redefinition of the theory of value

creation. Milgrom and Roberts (1992) propose to substitute the notion of partnership value for that of

shareholder value, to share this value among all the stakeholders according to the contributions of each

to the process of value creation. They observe that this distribution has a direct influence on the

process because of the transaction costs of unavoidable conflicts between partners. Each of them bears

integration of the economic entity that takes precedence over the creation of financial value. Societal

information is of intrinsic value here in that it explains the impact of the company's activity and

therefore its way of carrying out transactions or exchanges with its environment. As such, the societal

reporting fulfils a justification function, that is to say that it is interested in the role of the company in

these exchanges: how does the company respond to the expectations expressed by the actors in society

and what does it get in return? Societal reporting is used as a mechanism for clearing and maintaining

the social contract that authorizes and organizes exchanges between the company and the various

actors of society (Bradley, Schipani, Sundaram and Walsh 1999). Although the instrumental view of

stakeholder theory opposes the goal of maximizing value creation for shareholders alone, advocated by

agency theory, it nonetheless advocates cost-effective management which favors the continuity of the

operation and thus the maintenance of the jobs and the respect of the contractual conditions concluded

with the suppliers, the customers and the creditors. Its ambitions thus seem consistent with those of the

theory of dependence on resources, according to which social responsibility must be combined with

financial logic, via considering the firm's strategy the stakeholder requirements it needs to survive

(Pfeffer and Salancik, 1978). Only social and environmental actions facilitating access to new

resources therefore seem to have to be privileged.

Alignment with these frames of reference implies a reconsideration of the theory of

governance, because it partially calls into question the purpose of the company, defined by the

classical theory (Freeman 1984), which aims to reduce agency costs, securing the investor's capital and

seeking profit in the short term. This alignment extends the company's responsibilities both over time

(in the long term) and in the socio-economic space (stakeholders). Blair (1995) the concept of

pluralistic enterprise (or plural firm) open to its partners, to that of monist company centered on its

shareholders. This pluralistic representation of the firm implies a redefinition of the theory of value

creation. Milgrom and Roberts (1992) propose to substitute the notion of partnership value for that of

shareholder value, to share this value among all the stakeholders according to the contributions of each

to the process of value creation. They observe that this distribution has a direct influence on the

process because of the transaction costs of unavoidable conflicts between partners. Each of them bears

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder value vs Stakeholder value in Modern Corporate Governance 5

a residual risk associated with its specific investment in the company. Donaldson and Preston (1995)

find that "ingrained" leaders in the firm play a central role in the equitable distribution of created

value. Such approaches, according to Charreaux and Desbrière (1998), simply contractual, but also co-

constructed in duration and space. They recommend assessing the governance system in terms of its

ability to create partnership value and reduce the loss of value due to conflicts between stakeholders.

In attempting to find out what is more valuable to company’s corporate governance, Adams,

Licht, and Sagiv (2011) delved specifically in analysing specific variables that have influence on

whether the CEOs will support shareholders or stakeholders. They explored the variables related to

stakeholderism and shareholderism. Some of the variables they explored include shareholderism,

conformity, tradition, universalism, self-direction, power, security, gender, employee rep, age, CEO,

equity holding. The findings revealed that board members are more likely to make decision that

favours shareholders rather than stakeholders. The findings further shows that board members tend to

follow internal goals rather than external goals.

Evidently, most of the variables that have been tested in previous studies focus on

stakeholderism and shareholderism. They include conformity, tradition, universalism, self-direction,

power, security, gender, employee rep, age, CEO, equity holding. The findings revealed that board

members are more likely to make decision that favours shareholders rather than stakeholders. The

findings further shows that board members tend to follow internal goals rather than external goals. The

existing studies are always inclined towards the sharaholder’s value rather than the socio-economic

value. For example, the agency theory (Jensen and Meckling, 1976) states that the priority of any

company must remain the maximization of shareholder value. With this in mind, societal reporting

must enable financial players to have a better understanding of the risks that the company faces in the

medium and long term (natural as well as - and above all - legal) risks. This design corresponds to the

current trend of better identifying off-balance sheet liabilities, which are related to the sustainability of

the resources needed to produce, as well as those related to potential conflicts associated with

restructuring. To consider the question of sustainable development from the point of view of

a residual risk associated with its specific investment in the company. Donaldson and Preston (1995)

find that "ingrained" leaders in the firm play a central role in the equitable distribution of created

value. Such approaches, according to Charreaux and Desbrière (1998), simply contractual, but also co-

constructed in duration and space. They recommend assessing the governance system in terms of its

ability to create partnership value and reduce the loss of value due to conflicts between stakeholders.

In attempting to find out what is more valuable to company’s corporate governance, Adams,

Licht, and Sagiv (2011) delved specifically in analysing specific variables that have influence on

whether the CEOs will support shareholders or stakeholders. They explored the variables related to

stakeholderism and shareholderism. Some of the variables they explored include shareholderism,

conformity, tradition, universalism, self-direction, power, security, gender, employee rep, age, CEO,

equity holding. The findings revealed that board members are more likely to make decision that

favours shareholders rather than stakeholders. The findings further shows that board members tend to

follow internal goals rather than external goals.

Evidently, most of the variables that have been tested in previous studies focus on

stakeholderism and shareholderism. They include conformity, tradition, universalism, self-direction,

power, security, gender, employee rep, age, CEO, equity holding. The findings revealed that board

members are more likely to make decision that favours shareholders rather than stakeholders. The

findings further shows that board members tend to follow internal goals rather than external goals. The

existing studies are always inclined towards the sharaholder’s value rather than the socio-economic

value. For example, the agency theory (Jensen and Meckling, 1976) states that the priority of any

company must remain the maximization of shareholder value. With this in mind, societal reporting

must enable financial players to have a better understanding of the risks that the company faces in the

medium and long term (natural as well as - and above all - legal) risks. This design corresponds to the

current trend of better identifying off-balance sheet liabilities, which are related to the sustainability of

the resources needed to produce, as well as those related to potential conflicts associated with

restructuring. To consider the question of sustainable development from the point of view of

Shareholder value vs Stakeholder value in Modern Corporate Governance 6

contractual theories thus presupposes that social and environmental actions are likely to create

additional value, or at least to avoid the occurrence of potential social or environmental risks, which

could lead to a reduction in cash. In other words, societal dimensions would participate in the process

of value creation and should therefore be considered in sharing this value. That is why overreliance on

agency and stakeholder theory is no longer recommendable in the modern era because success of

businesses is no longer determined by the economic benefits alone. There is therefore a need to

determine whether the value obtained by focusing on shareholders is more important than the value

obtained by focusing on stakeholders

Hypotheses:

Hypothesis 1: Companies that focus more on stakeholders are likely to perform better than companies

that focus more on shareholders

Hypothesis 2: There is no significant difference between stakeholder value and shareholder value in

terms of their impact on the success of the company

contractual theories thus presupposes that social and environmental actions are likely to create

additional value, or at least to avoid the occurrence of potential social or environmental risks, which

could lead to a reduction in cash. In other words, societal dimensions would participate in the process

of value creation and should therefore be considered in sharing this value. That is why overreliance on

agency and stakeholder theory is no longer recommendable in the modern era because success of

businesses is no longer determined by the economic benefits alone. There is therefore a need to

determine whether the value obtained by focusing on shareholders is more important than the value

obtained by focusing on stakeholders

Hypotheses:

Hypothesis 1: Companies that focus more on stakeholders are likely to perform better than companies

that focus more on shareholders

Hypothesis 2: There is no significant difference between stakeholder value and shareholder value in

terms of their impact on the success of the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shareholder value vs Stakeholder value in Modern Corporate Governance 7

List of References

Adams R, Hermalin B, Weisbach M (2010) The role of boards of directors in corporate governance a

conceptual framework and survey, Journal of Economic Literature 48 (2010), pp.59-108

Adams, RB, Licht, AN and Sagiv L (2011) Shareholders and Stakeholders: How Do Directors Decide?

Strategic Management Journal, 32 (12), pp. 1331-1355

Agle BR, Mitchell RK, Sonnenfeld JA (1999) Who matters to CEOs? An investigation of stakeholder

attributes and salience, corporate performance, and CEO values, Academy of Management 42 (1999)

pp. 507-525

Blair MM (1995) Ownership and Control: Rethinking Governance for the Twenty-First Century , The

Brookings Institution.

Bradley M, Schipani CA, Sundaram AK, Walsh JP (1999) The purposes and accountability of the

Carlsson RH (2007) Swedish corporate governance and value creation: owners still in the driver's seat,

Corporate Governance: An International Review 15 (2007), pp.1038-1055

Carroll AB (1991) "The Pyramid of Corporate Social Responsibility: Toward the Moral Management

of Organizational Stakeholders," Business Horizons , Vol. 34, pp. 39-48.

Charreaux, GJ and Desbrieres, B (1998) Corporate Governance: Stakeholder Value Versus

Shareholder Value, Available at

SSRN: https://ssrn.com/abstract=262902 or http://dx.doi.org/10.2139/ssrn.262902

corporation in contemporary society: corporate governance at a crossroads, Law and Contemporary

Problems 62 (1999), pp.9-86

Donaldson T. and Preston LE (1995), "The Stakeholder's Theory of the Corporation: Concepts,

Evidence and Implications," Academy of Management Review , Vol. 20 (1): 65-91.

Elkington J (1998), Cannibals with Forks: The Triple Bottom Line of 21st Century Business , New

Society Publishers.

List of References

Adams R, Hermalin B, Weisbach M (2010) The role of boards of directors in corporate governance a

conceptual framework and survey, Journal of Economic Literature 48 (2010), pp.59-108

Adams, RB, Licht, AN and Sagiv L (2011) Shareholders and Stakeholders: How Do Directors Decide?

Strategic Management Journal, 32 (12), pp. 1331-1355

Agle BR, Mitchell RK, Sonnenfeld JA (1999) Who matters to CEOs? An investigation of stakeholder

attributes and salience, corporate performance, and CEO values, Academy of Management 42 (1999)

pp. 507-525

Blair MM (1995) Ownership and Control: Rethinking Governance for the Twenty-First Century , The

Brookings Institution.

Bradley M, Schipani CA, Sundaram AK, Walsh JP (1999) The purposes and accountability of the

Carlsson RH (2007) Swedish corporate governance and value creation: owners still in the driver's seat,

Corporate Governance: An International Review 15 (2007), pp.1038-1055

Carroll AB (1991) "The Pyramid of Corporate Social Responsibility: Toward the Moral Management

of Organizational Stakeholders," Business Horizons , Vol. 34, pp. 39-48.

Charreaux, GJ and Desbrieres, B (1998) Corporate Governance: Stakeholder Value Versus

Shareholder Value, Available at

SSRN: https://ssrn.com/abstract=262902 or http://dx.doi.org/10.2139/ssrn.262902

corporation in contemporary society: corporate governance at a crossroads, Law and Contemporary

Problems 62 (1999), pp.9-86

Donaldson T. and Preston LE (1995), "The Stakeholder's Theory of the Corporation: Concepts,

Evidence and Implications," Academy of Management Review , Vol. 20 (1): 65-91.

Elkington J (1998), Cannibals with Forks: The Triple Bottom Line of 21st Century Business , New

Society Publishers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder value vs Stakeholder value in Modern Corporate Governance 8

Freeman E (1984), Strategic Management: Stakeholder Approach, Massachussetts, Pittman Publishing

Inc.

Jensen M and Meckling W (1976), "Theory of the firm: managerial behavior, agency costs and

ownership structure," Journal of Financial Economics, 3(1976), pp. 305-360.

Milgrom P., Roberts J. (1990), Bargaining costs, Influence Costs and the Organization of the

Economy Activity , Cambridge University Press, pp. 57-59.

Perez R (2005): "Some Reflections on Responsible Management, Sustainable Development and

Corporate Social Responsibility", Journal of Management Science, Vol. 211-212 (January-April): 29-

46.

Pfeffer J and Salancik GR (1978) The External Control of Organizations , New York, Ed. Harpers and

Row.

Porta et al. (1997), "Trust in Large Organizations," American Economic Review, Papers and

Proceedings.

Rajan RG and Zingale L (2001), "The Influence of Financial Revolution on the Nature of the

Firm", American Economic Review, 91(2001), 2.

Freeman E (1984), Strategic Management: Stakeholder Approach, Massachussetts, Pittman Publishing

Inc.

Jensen M and Meckling W (1976), "Theory of the firm: managerial behavior, agency costs and

ownership structure," Journal of Financial Economics, 3(1976), pp. 305-360.

Milgrom P., Roberts J. (1990), Bargaining costs, Influence Costs and the Organization of the

Economy Activity , Cambridge University Press, pp. 57-59.

Perez R (2005): "Some Reflections on Responsible Management, Sustainable Development and

Corporate Social Responsibility", Journal of Management Science, Vol. 211-212 (January-April): 29-

46.

Pfeffer J and Salancik GR (1978) The External Control of Organizations , New York, Ed. Harpers and

Row.

Porta et al. (1997), "Trust in Large Organizations," American Economic Review, Papers and

Proceedings.

Rajan RG and Zingale L (2001), "The Influence of Financial Revolution on the Nature of the

Firm", American Economic Review, 91(2001), 2.

Shareholder value vs Stakeholder value in Modern Corporate Governance 9

Appendix:

Appendix I – Annotated Bibliography for Selected Articles

Author/s Date Title Journal Type of

Paper

(Theoretical

or

Empirical)

If empirical,

dependent &

independent

variables

Summary of contribution to the research

question

Appendix:

Appendix I – Annotated Bibliography for Selected Articles

Author/s Date Title Journal Type of

Paper

(Theoretical

or

Empirical)

If empirical,

dependent &

independent

variables

Summary of contribution to the research

question

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shareholder value vs Stakeholder value in Modern Corporate Governance 10

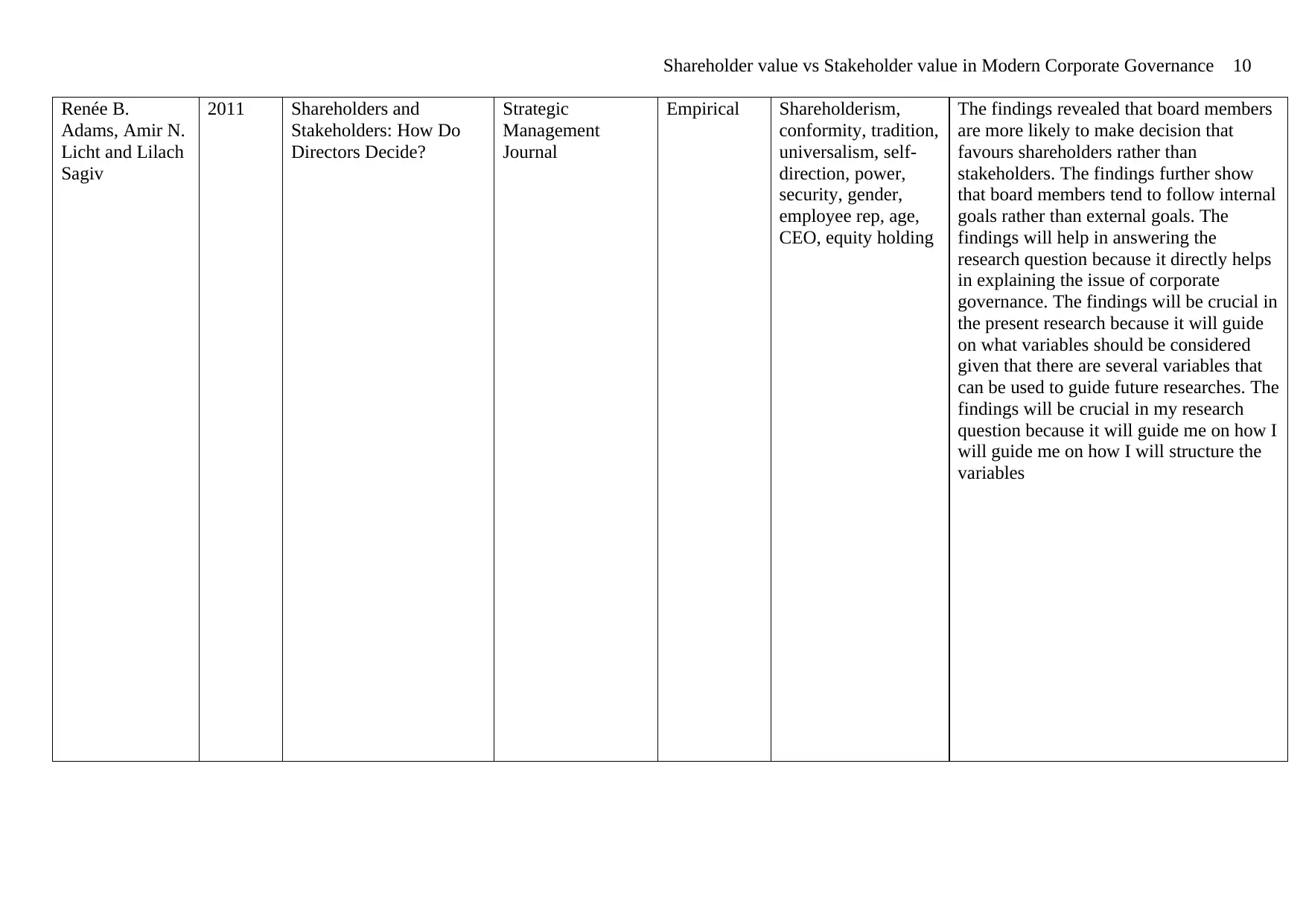

Renée B.

Adams, Amir N.

Licht and Lilach

Sagiv

2011 Shareholders and

Stakeholders: How Do

Directors Decide?

Strategic

Management

Journal

Empirical Shareholderism,

conformity, tradition,

universalism, self-

direction, power,

security, gender,

employee rep, age,

CEO, equity holding

The findings revealed that board members

are more likely to make decision that

favours shareholders rather than

stakeholders. The findings further show

that board members tend to follow internal

goals rather than external goals. The

findings will help in answering the

research question because it directly helps

in explaining the issue of corporate

governance. The findings will be crucial in

the present research because it will guide

on what variables should be considered

given that there are several variables that

can be used to guide future researches. The

findings will be crucial in my research

question because it will guide me on how I

will guide me on how I will structure the

variables

Renée B.

Adams, Amir N.

Licht and Lilach

Sagiv

2011 Shareholders and

Stakeholders: How Do

Directors Decide?

Strategic

Management

Journal

Empirical Shareholderism,

conformity, tradition,

universalism, self-

direction, power,

security, gender,

employee rep, age,

CEO, equity holding

The findings revealed that board members

are more likely to make decision that

favours shareholders rather than

stakeholders. The findings further show

that board members tend to follow internal

goals rather than external goals. The

findings will help in answering the

research question because it directly helps

in explaining the issue of corporate

governance. The findings will be crucial in

the present research because it will guide

on what variables should be considered

given that there are several variables that

can be used to guide future researches. The

findings will be crucial in my research

question because it will guide me on how I

will guide me on how I will structure the

variables

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder value vs Stakeholder value in Modern Corporate Governance 11

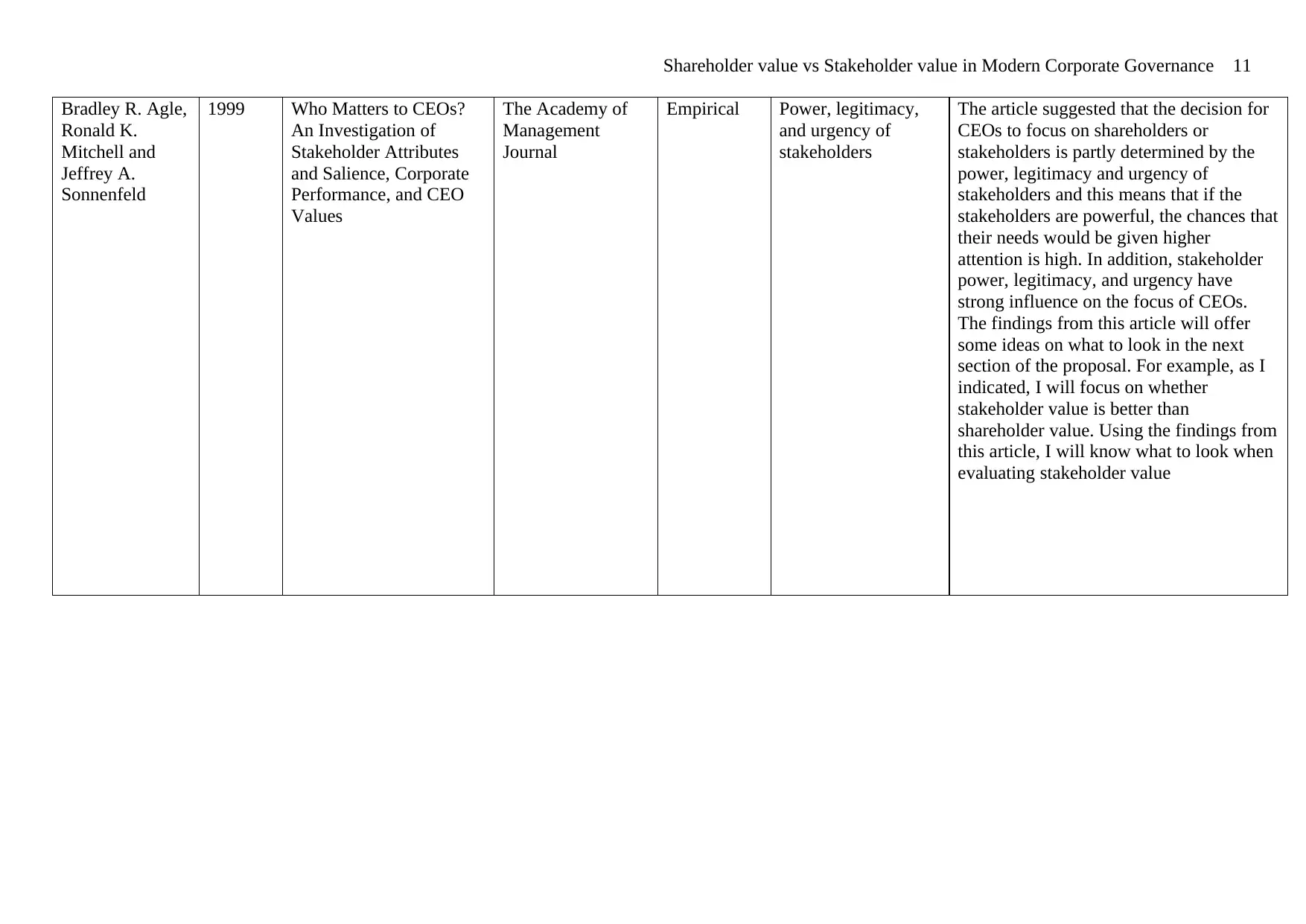

Bradley R. Agle,

Ronald K.

Mitchell and

Jeffrey A.

Sonnenfeld

1999 Who Matters to CEOs?

An Investigation of

Stakeholder Attributes

and Salience, Corporate

Performance, and CEO

Values

The Academy of

Management

Journal

Empirical Power, legitimacy,

and urgency of

stakeholders

The article suggested that the decision for

CEOs to focus on shareholders or

stakeholders is partly determined by the

power, legitimacy and urgency of

stakeholders and this means that if the

stakeholders are powerful, the chances that

their needs would be given higher

attention is high. In addition, stakeholder

power, legitimacy, and urgency have

strong influence on the focus of CEOs.

The findings from this article will offer

some ideas on what to look in the next

section of the proposal. For example, as I

indicated, I will focus on whether

stakeholder value is better than

shareholder value. Using the findings from

this article, I will know what to look when

evaluating stakeholder value

Bradley R. Agle,

Ronald K.

Mitchell and

Jeffrey A.

Sonnenfeld

1999 Who Matters to CEOs?

An Investigation of

Stakeholder Attributes

and Salience, Corporate

Performance, and CEO

Values

The Academy of

Management

Journal

Empirical Power, legitimacy,

and urgency of

stakeholders

The article suggested that the decision for

CEOs to focus on shareholders or

stakeholders is partly determined by the

power, legitimacy and urgency of

stakeholders and this means that if the

stakeholders are powerful, the chances that

their needs would be given higher

attention is high. In addition, stakeholder

power, legitimacy, and urgency have

strong influence on the focus of CEOs.

The findings from this article will offer

some ideas on what to look in the next

section of the proposal. For example, as I

indicated, I will focus on whether

stakeholder value is better than

shareholder value. Using the findings from

this article, I will know what to look when

evaluating stakeholder value

Shareholder value vs Stakeholder value in Modern Corporate Governance 12

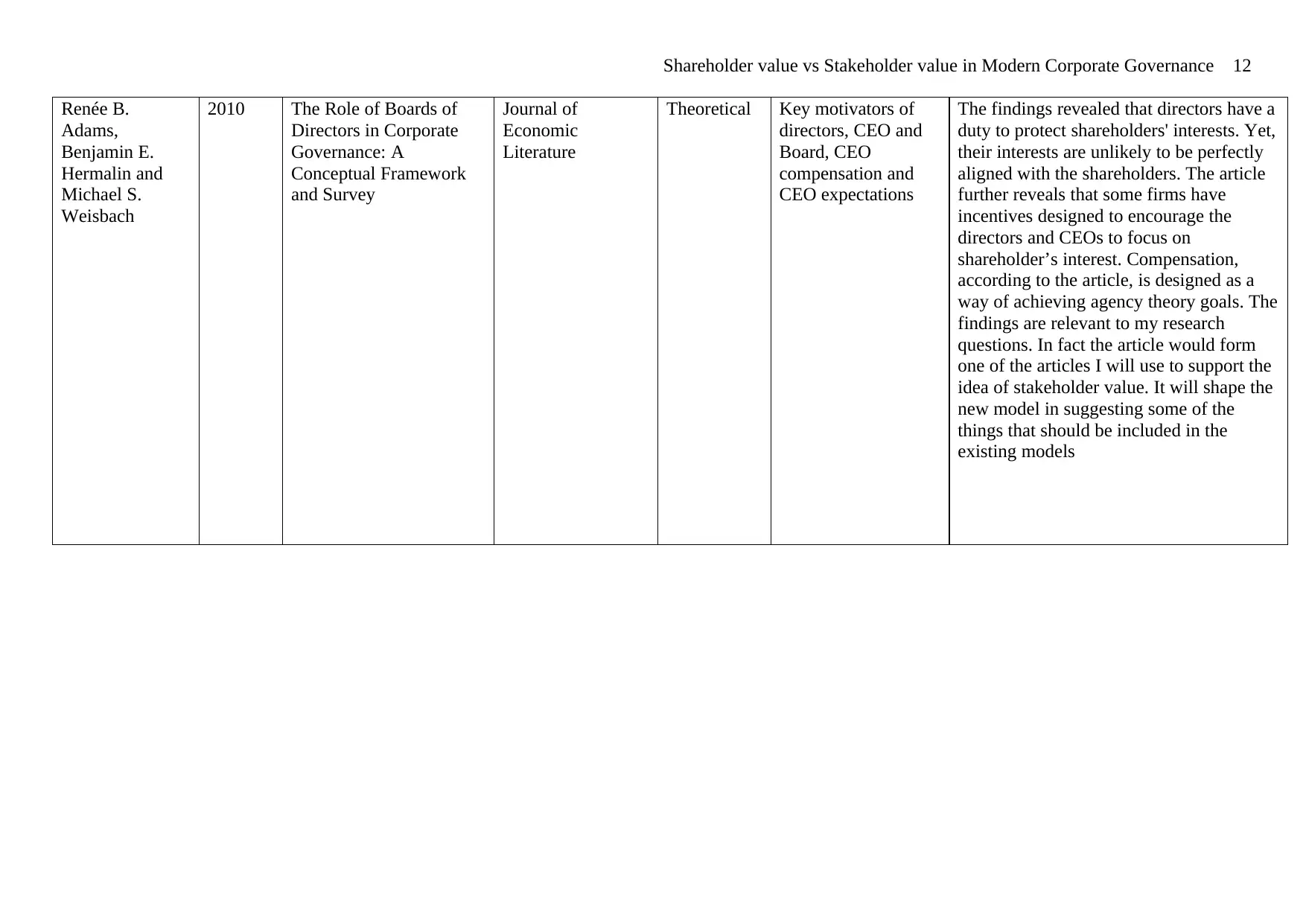

Renée B.

Adams,

Benjamin E.

Hermalin and

Michael S.

Weisbach

2010 The Role of Boards of

Directors in Corporate

Governance: A

Conceptual Framework

and Survey

Journal of

Economic

Literature

Theoretical Key motivators of

directors, CEO and

Board, CEO

compensation and

CEO expectations

The findings revealed that directors have a

duty to protect shareholders' interests. Yet,

their interests are unlikely to be perfectly

aligned with the shareholders. The article

further reveals that some firms have

incentives designed to encourage the

directors and CEOs to focus on

shareholder’s interest. Compensation,

according to the article, is designed as a

way of achieving agency theory goals. The

findings are relevant to my research

questions. In fact the article would form

one of the articles I will use to support the

idea of stakeholder value. It will shape the

new model in suggesting some of the

things that should be included in the

existing models

Renée B.

Adams,

Benjamin E.

Hermalin and

Michael S.

Weisbach

2010 The Role of Boards of

Directors in Corporate

Governance: A

Conceptual Framework

and Survey

Journal of

Economic

Literature

Theoretical Key motivators of

directors, CEO and

Board, CEO

compensation and

CEO expectations

The findings revealed that directors have a

duty to protect shareholders' interests. Yet,

their interests are unlikely to be perfectly

aligned with the shareholders. The article

further reveals that some firms have

incentives designed to encourage the

directors and CEOs to focus on

shareholder’s interest. Compensation,

according to the article, is designed as a

way of achieving agency theory goals. The

findings are relevant to my research

questions. In fact the article would form

one of the articles I will use to support the

idea of stakeholder value. It will shape the

new model in suggesting some of the

things that should be included in the

existing models

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.