ACC322 Project Report: Company Accounting Analysis

VerifiedAdded on 2022/11/16

|20

|3778

|72

Project

AI Summary

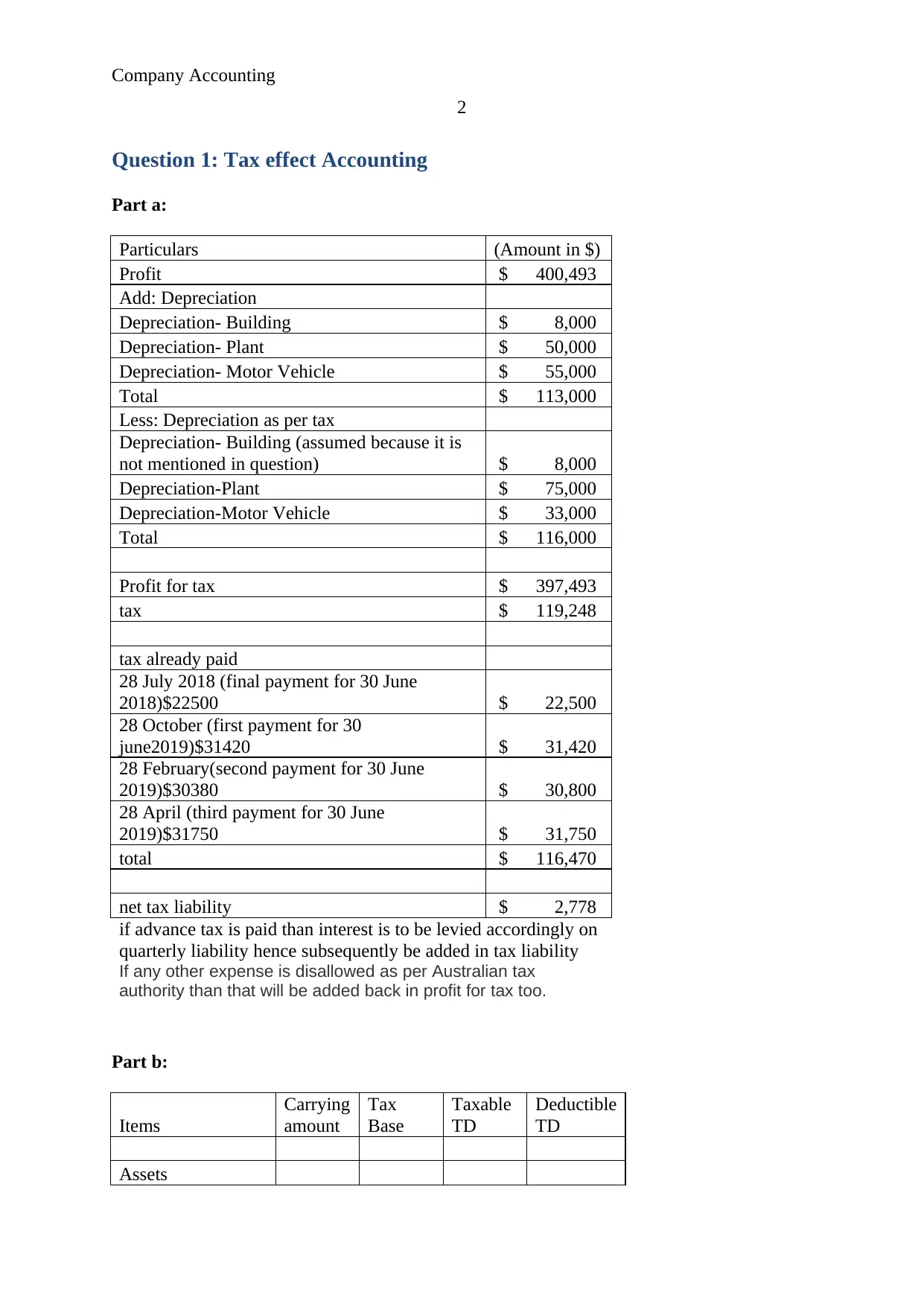

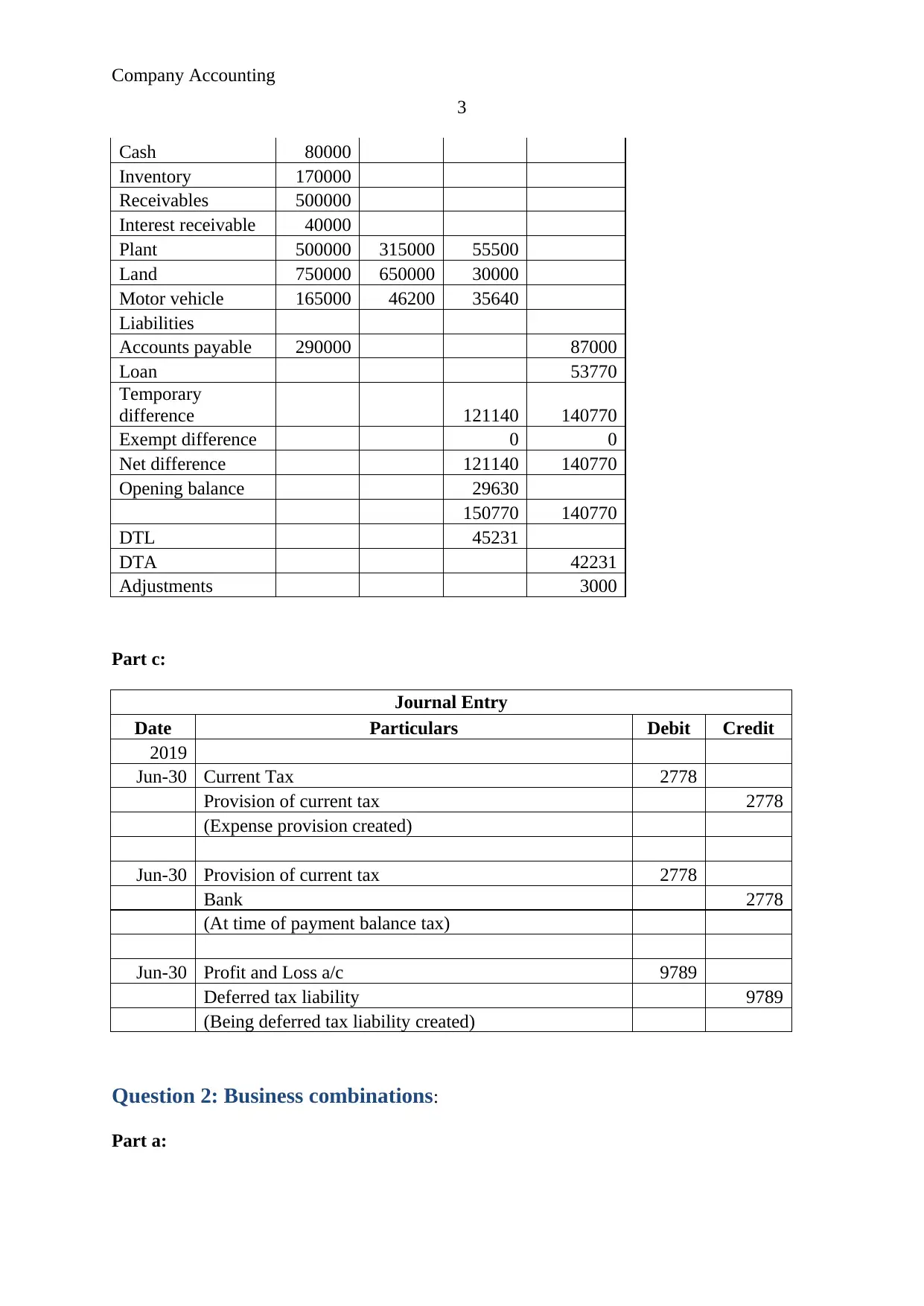

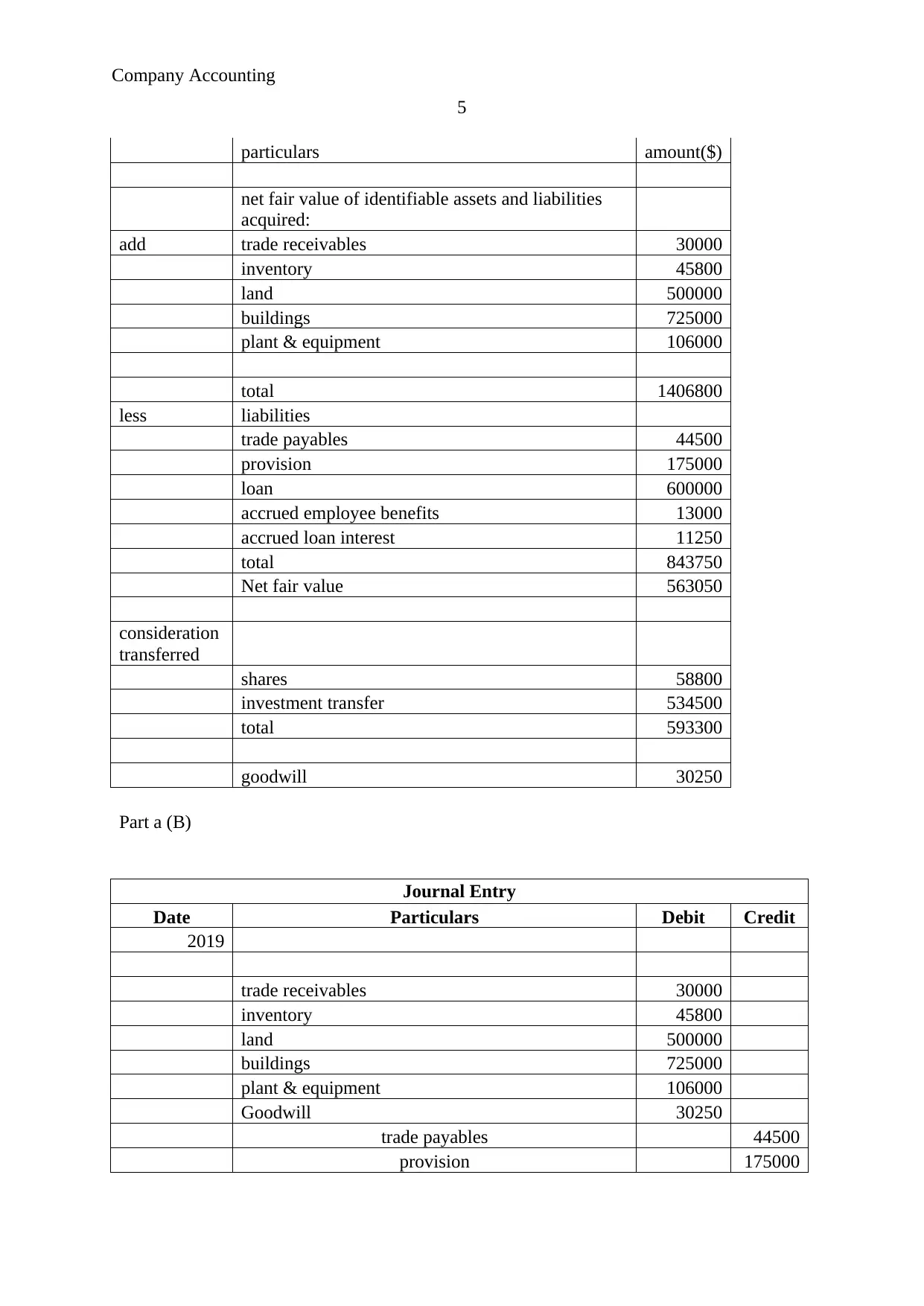

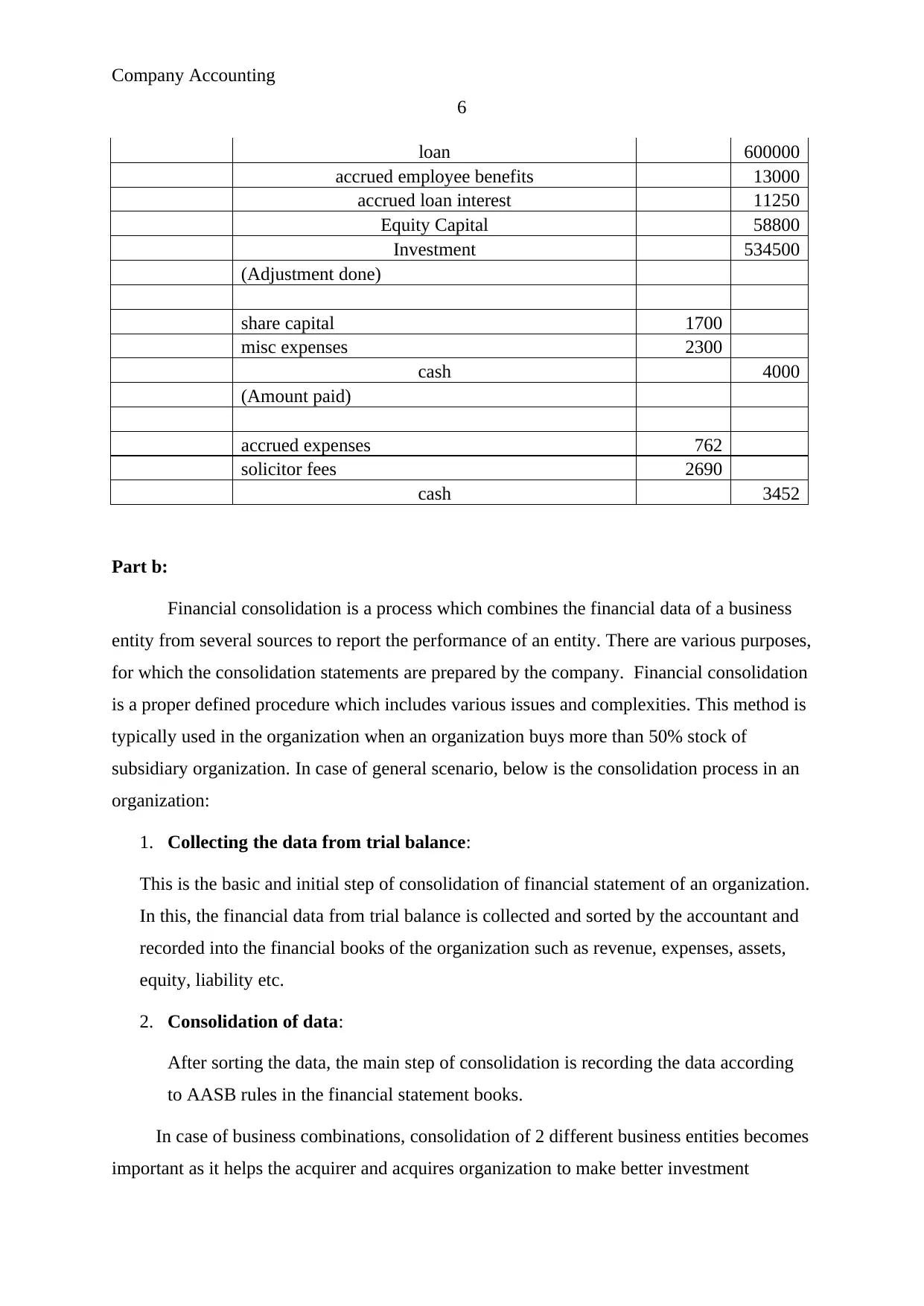

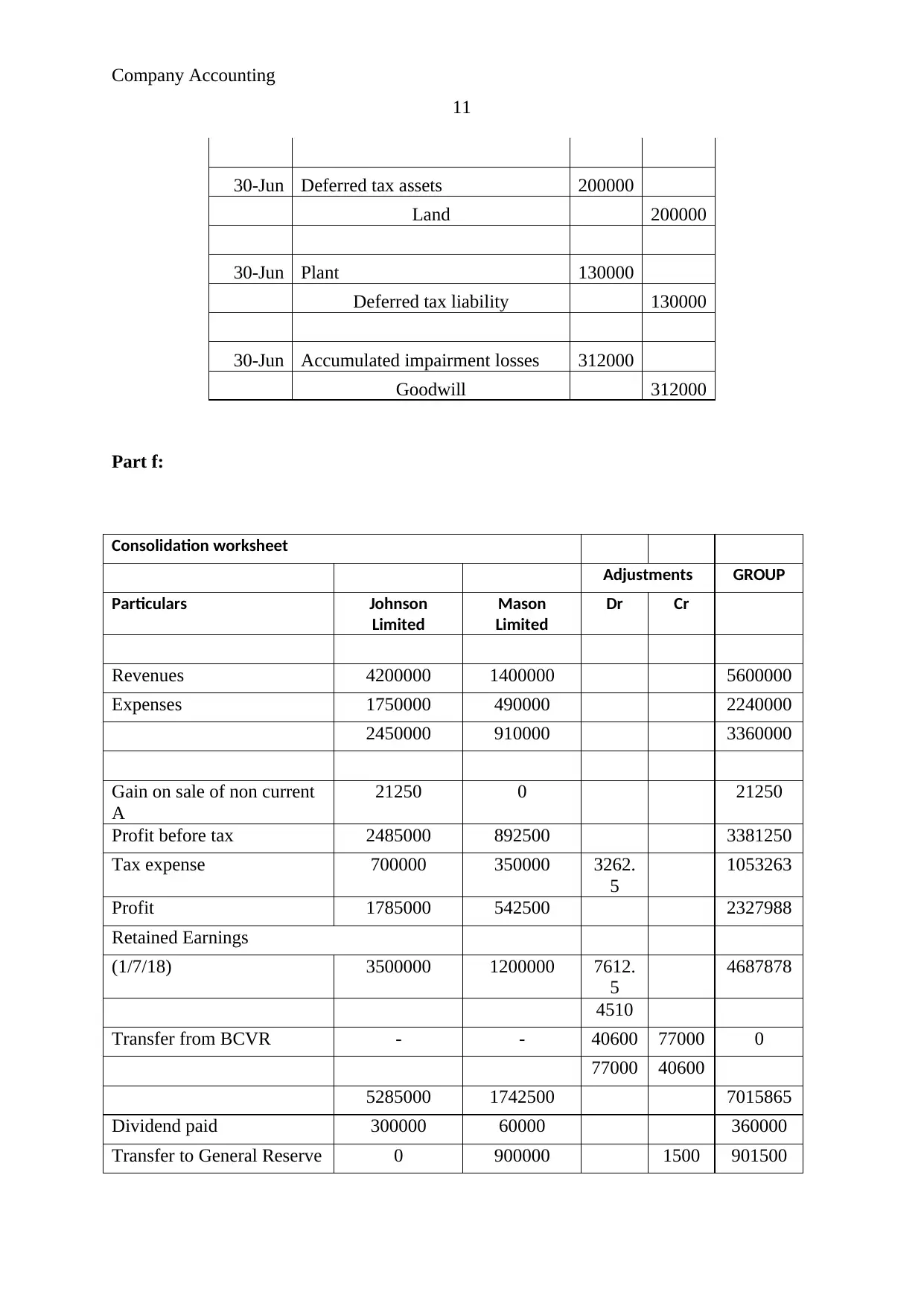

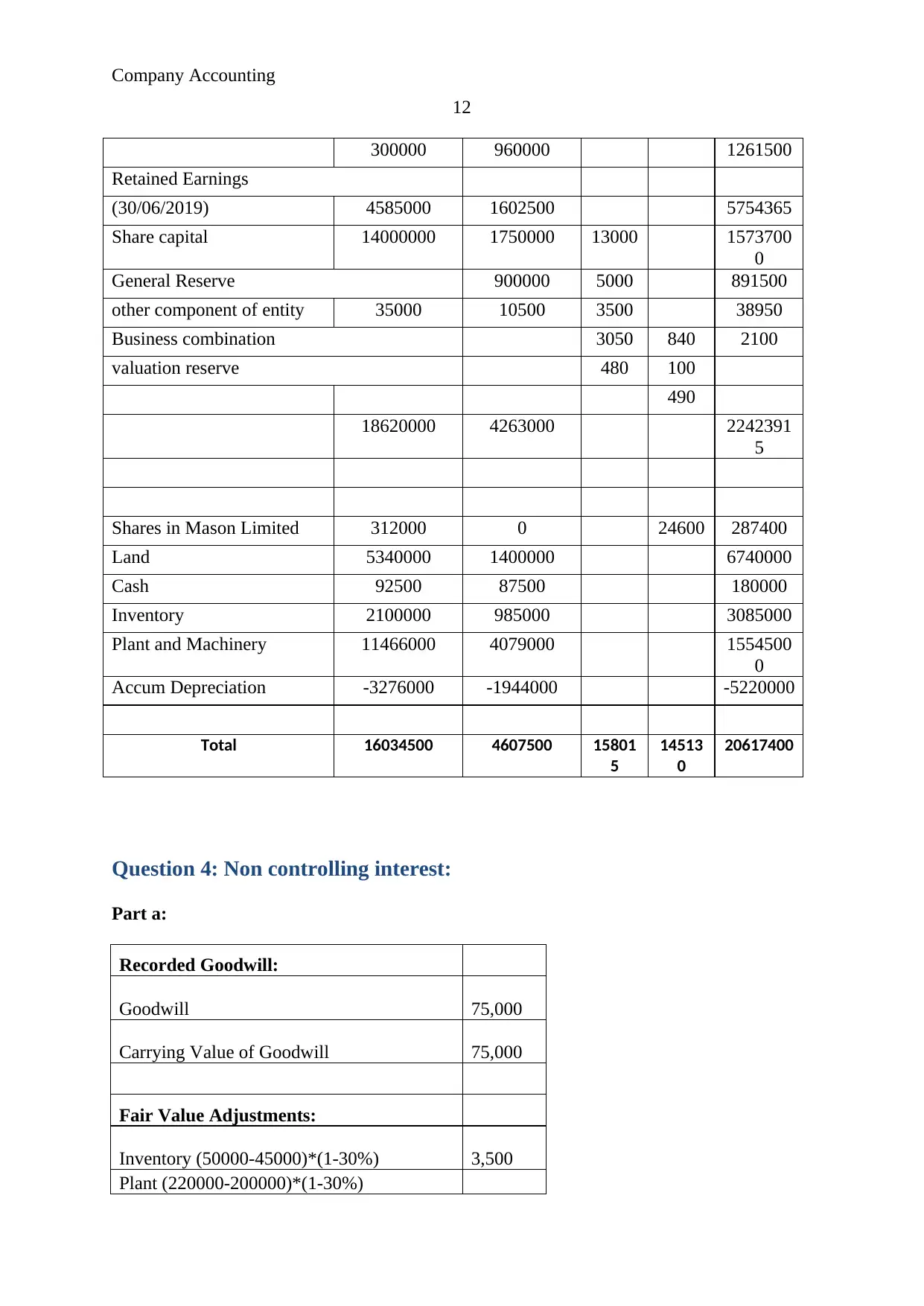

This project report addresses a comprehensive company accounting assignment, encompassing three key areas: tax effect accounting, business combinations, and consolidation. The tax effect accounting section includes calculations for profit for tax, tax liabilities, and journal entries related to current and deferred tax. The business combinations section covers the acquisition of net assets, journal entries for the acquisition, and an explanation of financial consolidation processes. This includes the collection and consolidation of data, and the process of consolidation in business combinations. Finally, the consolidation section analyzes goodwill, including carrying values, fair value adjustments, and acquisition analysis, with detailed journal entries and a consolidation worksheet to illustrate the combined financial statements. The report offers a thorough analysis and provides a clear understanding of the accounting principles involved in each area.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.