ACC510 Report: Financial Statement Analysis of Provisions, Leases

VerifiedAdded on 2024/05/31

|10

|1863

|181

Report

AI Summary

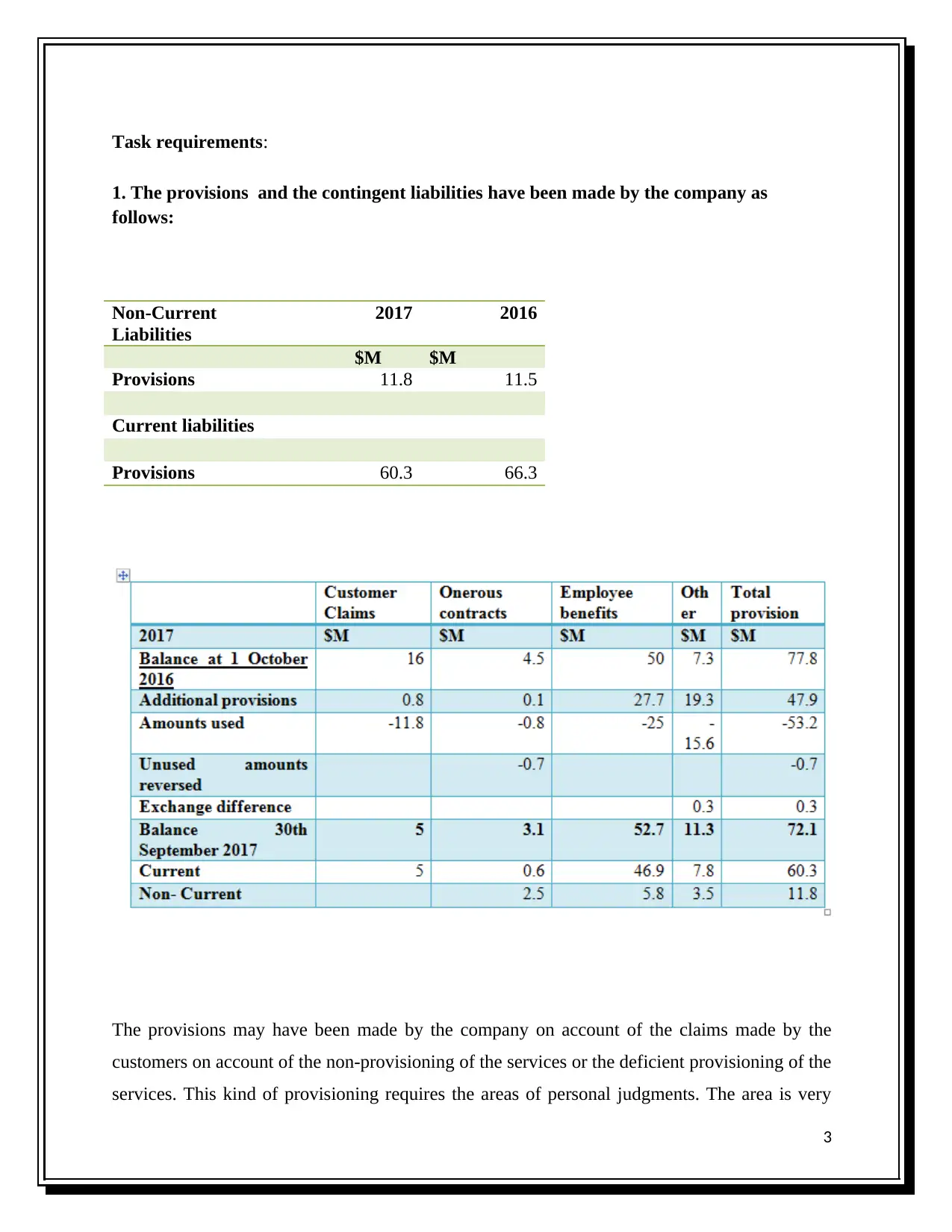

This ACC510 report provides a detailed analysis of provisions, contingent liabilities, and leased items within a company's financial statements. It examines the recognition criteria and measurement issues associated with provisions and contingencies, discussing arguments for and against their inclusion in financial reports. The report also delves into leased items, covering classification, presentation requirements, and potential reclassification scenarios. Furthermore, it analyzes a selected non-current asset, detailing its valuation method and arguing for alternative valuation methods based on qualitative characteristics. References to AASB standards and other relevant sources are included to support the analysis and conclusions presented in the report.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.