Managerial Finance: Dell Inc. Manufacturing Plant Project Evaluation

VerifiedAdded on 2023/03/17

|11

|2466

|38

Report

AI Summary

This report evaluates the feasibility of a new laptop manufacturing plant for Dell Inc. The analysis includes calculating depreciation, cash flows, and key financial metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), and payback periods to determine the project's profitability and financial viability. The report also assesses the impact of borrowing on the project's financial discipline and provides recommendations regarding the project's acceptance and the company's discount rate practices. The conclusion suggests that the project is acceptable based on its positive NPV, high IRR, and reasonable payback period, while also recommending adjustments to the discount rate to account for project-specific risks.

Running head: MANAGERIAL FINANCE

Managerial finance

Name of the student

Name of the university

Student ID

Author note

Managerial finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL FINANCE

Executive summary

The report is prepared for carrying out the feasibility of the manufacturing plant that is analysed

by Dell Inc. for starting up. It is found from the project evaluation that the NPV of the project is

$ 258,659,222.81. It is signifying that the project will be able to generate the amount of initial

investment for the project IRR of the project is 26% whereas the cost of capital of the company

is 16%. Looking into the payback period computation it is found that the payback period is 3.66

years and the discounted payback period is 5.88 years. Hence, the project is able to recover the

amount of initial expenses within the useful life of the project. From all the aspect the project is

therefore acceptable. Further, from the computation in question 2 it is found that for the project

to meet financial discipline it can borrow the amount maximum at interest rate of 15%.

Executive summary

The report is prepared for carrying out the feasibility of the manufacturing plant that is analysed

by Dell Inc. for starting up. It is found from the project evaluation that the NPV of the project is

$ 258,659,222.81. It is signifying that the project will be able to generate the amount of initial

investment for the project IRR of the project is 26% whereas the cost of capital of the company

is 16%. Looking into the payback period computation it is found that the payback period is 3.66

years and the discounted payback period is 5.88 years. Hence, the project is able to recover the

amount of initial expenses within the useful life of the project. From all the aspect the project is

therefore acceptable. Further, from the computation in question 2 it is found that for the project

to meet financial discipline it can borrow the amount maximum at interest rate of 15%.

2MANAGERIAL FINANCE

Introduction

The main objective of this professional report is to answer some question related to

evaluation of the project that is projected to be started by Dell Inc. It is planning for setting up of

new plant for manufacturing laptop. The report will analyse the profitability of the project

through considering different approaches like Net present value, internal rate of return and

discounted payback period. Based on the results from these approaches recommendation will be

provided regarding acceptability of the projects (Žižlavský 2014)

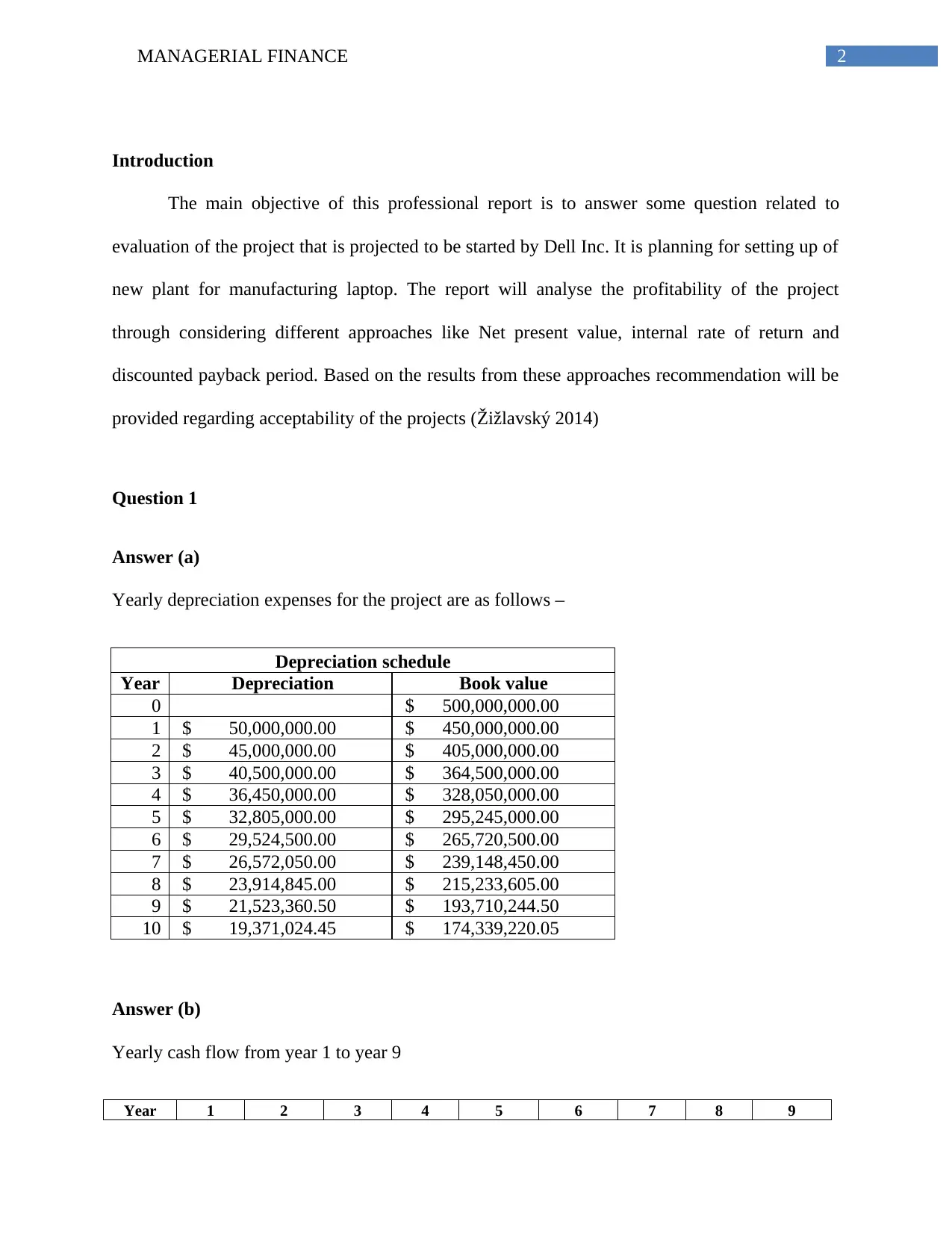

Question 1

Answer (a)

Yearly depreciation expenses for the project are as follows –

Depreciation schedule

Year Depreciation Book value

0 $ 500,000,000.00

1 $ 50,000,000.00 $ 450,000,000.00

2 $ 45,000,000.00 $ 405,000,000.00

3 $ 40,500,000.00 $ 364,500,000.00

4 $ 36,450,000.00 $ 328,050,000.00

5 $ 32,805,000.00 $ 295,245,000.00

6 $ 29,524,500.00 $ 265,720,500.00

7 $ 26,572,050.00 $ 239,148,450.00

8 $ 23,914,845.00 $ 215,233,605.00

9 $ 21,523,360.50 $ 193,710,244.50

10 $ 19,371,024.45 $ 174,339,220.05

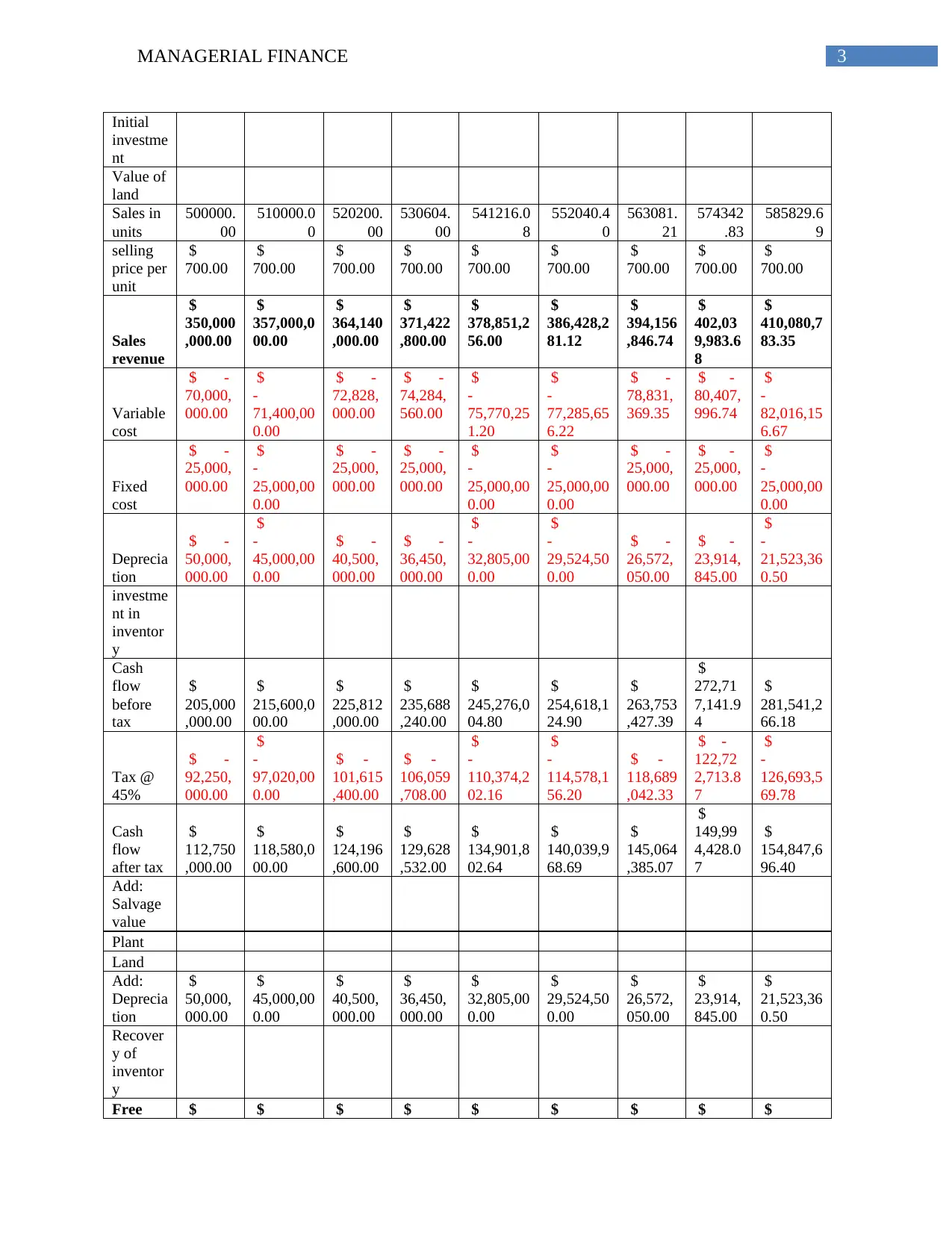

Answer (b)

Yearly cash flow from year 1 to year 9

Year 1 2 3 4 5 6 7 8 9

Introduction

The main objective of this professional report is to answer some question related to

evaluation of the project that is projected to be started by Dell Inc. It is planning for setting up of

new plant for manufacturing laptop. The report will analyse the profitability of the project

through considering different approaches like Net present value, internal rate of return and

discounted payback period. Based on the results from these approaches recommendation will be

provided regarding acceptability of the projects (Žižlavský 2014)

Question 1

Answer (a)

Yearly depreciation expenses for the project are as follows –

Depreciation schedule

Year Depreciation Book value

0 $ 500,000,000.00

1 $ 50,000,000.00 $ 450,000,000.00

2 $ 45,000,000.00 $ 405,000,000.00

3 $ 40,500,000.00 $ 364,500,000.00

4 $ 36,450,000.00 $ 328,050,000.00

5 $ 32,805,000.00 $ 295,245,000.00

6 $ 29,524,500.00 $ 265,720,500.00

7 $ 26,572,050.00 $ 239,148,450.00

8 $ 23,914,845.00 $ 215,233,605.00

9 $ 21,523,360.50 $ 193,710,244.50

10 $ 19,371,024.45 $ 174,339,220.05

Answer (b)

Yearly cash flow from year 1 to year 9

Year 1 2 3 4 5 6 7 8 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL FINANCE

Initial

investme

nt

Value of

land

Sales in

units

500000.

00

510000.0

0

520200.

00

530604.

00

541216.0

8

552040.4

0

563081.

21

574342

.83

585829.6

9

selling

price per

unit

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

Sales

revenue

$

350,000

,000.00

$

357,000,0

00.00

$

364,140

,000.00

$

371,422

,800.00

$

378,851,2

56.00

$

386,428,2

81.12

$

394,156

,846.74

$

402,03

9,983.6

8

$

410,080,7

83.35

Variable

cost

$ -

70,000,

000.00

$

-

71,400,00

0.00

$ -

72,828,

000.00

$ -

74,284,

560.00

$

-

75,770,25

1.20

$

-

77,285,65

6.22

$ -

78,831,

369.35

$ -

80,407,

996.74

$

-

82,016,15

6.67

Fixed

cost

$ -

25,000,

000.00

$

-

25,000,00

0.00

$ -

25,000,

000.00

$ -

25,000,

000.00

$

-

25,000,00

0.00

$

-

25,000,00

0.00

$ -

25,000,

000.00

$ -

25,000,

000.00

$

-

25,000,00

0.00

Deprecia

tion

$ -

50,000,

000.00

$

-

45,000,00

0.00

$ -

40,500,

000.00

$ -

36,450,

000.00

$

-

32,805,00

0.00

$

-

29,524,50

0.00

$ -

26,572,

050.00

$ -

23,914,

845.00

$

-

21,523,36

0.50

investme

nt in

inventor

y

Cash

flow

before

tax

$

205,000

,000.00

$

215,600,0

00.00

$

225,812

,000.00

$

235,688

,240.00

$

245,276,0

04.80

$

254,618,1

24.90

$

263,753

,427.39

$

272,71

7,141.9

4

$

281,541,2

66.18

Tax @

45%

$ -

92,250,

000.00

$

-

97,020,00

0.00

$ -

101,615

,400.00

$ -

106,059

,708.00

$

-

110,374,2

02.16

$

-

114,578,1

56.20

$ -

118,689

,042.33

$ -

122,72

2,713.8

7

$

-

126,693,5

69.78

Cash

flow

after tax

$

112,750

,000.00

$

118,580,0

00.00

$

124,196

,600.00

$

129,628

,532.00

$

134,901,8

02.64

$

140,039,9

68.69

$

145,064

,385.07

$

149,99

4,428.0

7

$

154,847,6

96.40

Add:

Salvage

value

Plant

Land

Add:

Deprecia

tion

$

50,000,

000.00

$

45,000,00

0.00

$

40,500,

000.00

$

36,450,

000.00

$

32,805,00

0.00

$

29,524,50

0.00

$

26,572,

050.00

$

23,914,

845.00

$

21,523,36

0.50

Recover

y of

inventor

y

Free $ $ $ $ $ $ $ $ $

Initial

investme

nt

Value of

land

Sales in

units

500000.

00

510000.0

0

520200.

00

530604.

00

541216.0

8

552040.4

0

563081.

21

574342

.83

585829.6

9

selling

price per

unit

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

$

700.00

Sales

revenue

$

350,000

,000.00

$

357,000,0

00.00

$

364,140

,000.00

$

371,422

,800.00

$

378,851,2

56.00

$

386,428,2

81.12

$

394,156

,846.74

$

402,03

9,983.6

8

$

410,080,7

83.35

Variable

cost

$ -

70,000,

000.00

$

-

71,400,00

0.00

$ -

72,828,

000.00

$ -

74,284,

560.00

$

-

75,770,25

1.20

$

-

77,285,65

6.22

$ -

78,831,

369.35

$ -

80,407,

996.74

$

-

82,016,15

6.67

Fixed

cost

$ -

25,000,

000.00

$

-

25,000,00

0.00

$ -

25,000,

000.00

$ -

25,000,

000.00

$

-

25,000,00

0.00

$

-

25,000,00

0.00

$ -

25,000,

000.00

$ -

25,000,

000.00

$

-

25,000,00

0.00

Deprecia

tion

$ -

50,000,

000.00

$

-

45,000,00

0.00

$ -

40,500,

000.00

$ -

36,450,

000.00

$

-

32,805,00

0.00

$

-

29,524,50

0.00

$ -

26,572,

050.00

$ -

23,914,

845.00

$

-

21,523,36

0.50

investme

nt in

inventor

y

Cash

flow

before

tax

$

205,000

,000.00

$

215,600,0

00.00

$

225,812

,000.00

$

235,688

,240.00

$

245,276,0

04.80

$

254,618,1

24.90

$

263,753

,427.39

$

272,71

7,141.9

4

$

281,541,2

66.18

Tax @

45%

$ -

92,250,

000.00

$

-

97,020,00

0.00

$ -

101,615

,400.00

$ -

106,059

,708.00

$

-

110,374,2

02.16

$

-

114,578,1

56.20

$ -

118,689

,042.33

$ -

122,72

2,713.8

7

$

-

126,693,5

69.78

Cash

flow

after tax

$

112,750

,000.00

$

118,580,0

00.00

$

124,196

,600.00

$

129,628

,532.00

$

134,901,8

02.64

$

140,039,9

68.69

$

145,064

,385.07

$

149,99

4,428.0

7

$

154,847,6

96.40

Add:

Salvage

value

Plant

Land

Add:

Deprecia

tion

$

50,000,

000.00

$

45,000,00

0.00

$

40,500,

000.00

$

36,450,

000.00

$

32,805,00

0.00

$

29,524,50

0.00

$

26,572,

050.00

$

23,914,

845.00

$

21,523,36

0.50

Recover

y of

inventor

y

Free $ $ $ $ $ $ $ $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL FINANCE

cash

flow

162,750

,000.00

163,580,0

00.00

164,696

,600.00

166,078

,532.00

167,706,8

02.64

169,564,4

68.69

171,636

,435.07

149,99

4,428.0

7

176,371,0

56.90

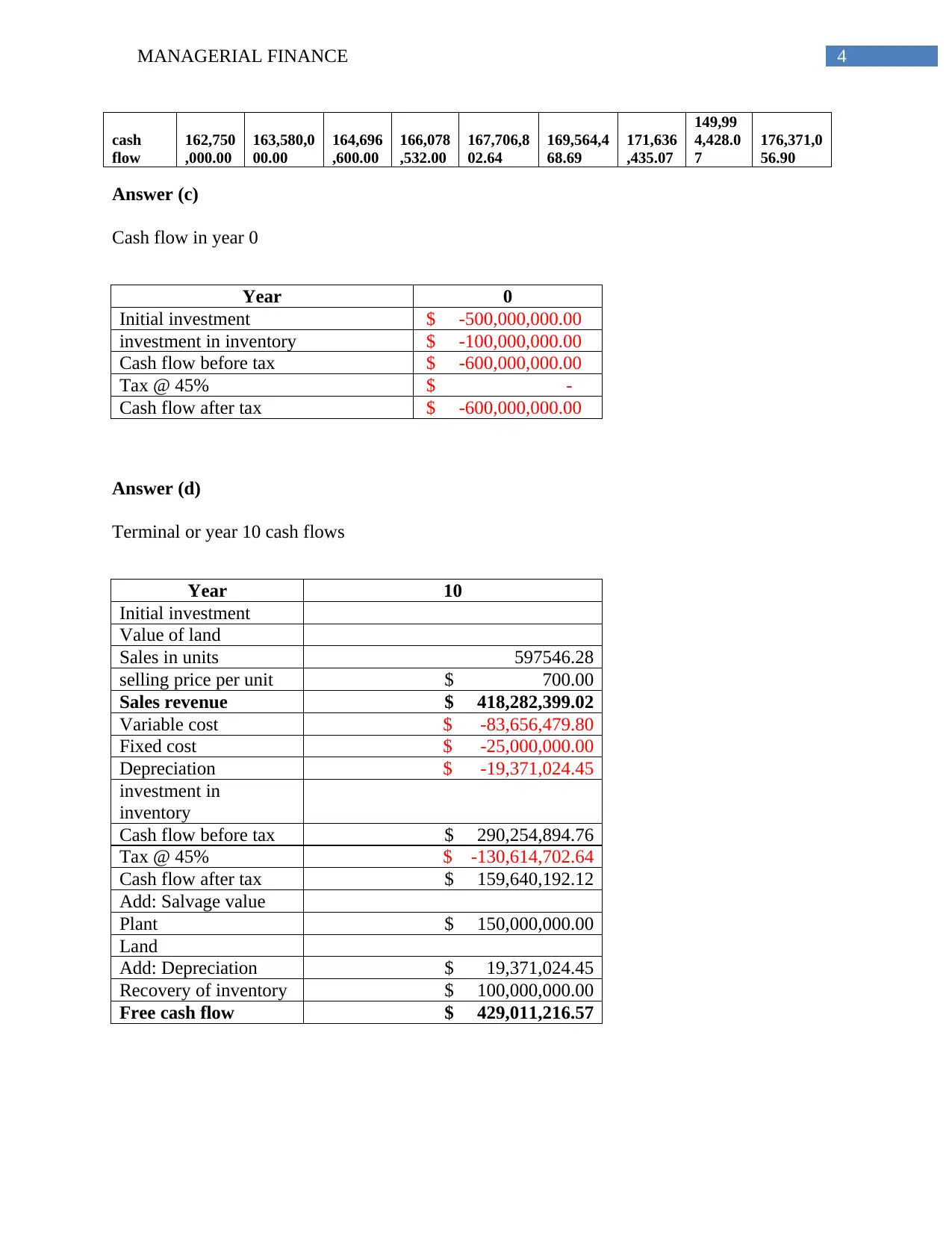

Answer (c)

Cash flow in year 0

Year 0

Initial investment $ -500,000,000.00

investment in inventory $ -100,000,000.00

Cash flow before tax $ -600,000,000.00

Tax @ 45% $ -

Cash flow after tax $ -600,000,000.00

Answer (d)

Terminal or year 10 cash flows

Year 10

Initial investment

Value of land

Sales in units 597546.28

selling price per unit $ 700.00

Sales revenue $ 418,282,399.02

Variable cost $ -83,656,479.80

Fixed cost $ -25,000,000.00

Depreciation $ -19,371,024.45

investment in

inventory

Cash flow before tax $ 290,254,894.76

Tax @ 45% $ -130,614,702.64

Cash flow after tax $ 159,640,192.12

Add: Salvage value

Plant $ 150,000,000.00

Land

Add: Depreciation $ 19,371,024.45

Recovery of inventory $ 100,000,000.00

Free cash flow $ 429,011,216.57

cash

flow

162,750

,000.00

163,580,0

00.00

164,696

,600.00

166,078

,532.00

167,706,8

02.64

169,564,4

68.69

171,636

,435.07

149,99

4,428.0

7

176,371,0

56.90

Answer (c)

Cash flow in year 0

Year 0

Initial investment $ -500,000,000.00

investment in inventory $ -100,000,000.00

Cash flow before tax $ -600,000,000.00

Tax @ 45% $ -

Cash flow after tax $ -600,000,000.00

Answer (d)

Terminal or year 10 cash flows

Year 10

Initial investment

Value of land

Sales in units 597546.28

selling price per unit $ 700.00

Sales revenue $ 418,282,399.02

Variable cost $ -83,656,479.80

Fixed cost $ -25,000,000.00

Depreciation $ -19,371,024.45

investment in

inventory

Cash flow before tax $ 290,254,894.76

Tax @ 45% $ -130,614,702.64

Cash flow after tax $ 159,640,192.12

Add: Salvage value

Plant $ 150,000,000.00

Land

Add: Depreciation $ 19,371,024.45

Recovery of inventory $ 100,000,000.00

Free cash flow $ 429,011,216.57

5MANAGERIAL FINANCE

Answer (e)

Net present value (NPV)

NPV is the difference among present value of future cash flows from any investment and

the amount invested for the acquiring the project. Present value of expected cash flow is

calculated through discounting the cash flows at the required return rate. Positive NPV signifies

better return and the negative NPV signifies worse return that is lower than zero. While any

manager requires comparing the projects and deciding regarding which one is to be selected. It

can be considered as a good approach for analysing the profitability of any investment in the

entity or any new project of the entity (Leyman and Vanhoucke 2016). NPV approach provides

various advantages like it considers the discounted cash flows while computing the computing

the value of net cash flows. Further, it considers the cost of capital and the inherent risk while

making the projections regarding future. Projection of the cash flows for 10 years into future is

definitely lower as compared to the cash flow for the next year. Looking into the NPV

calculation for the manufacturing plant of Dell Inc. it can be identified that the NPV of the

project is $ 258,659,222.81. It is signifying that the project will be able to generate the amount of

initial investment for the project. Hence, if the project is taken up it will increase the

shareholder’s wealth. Hence, considering the NPV only the project shall be accepted (Leyman

and Vanhoucke 2017)

Answer (f)

Internal rate of return and payback period

Internal rate of return (IRR) – IRR is the rate used for estimating the profitability of any

investment. It makes the discount rate of all the cash flows from the particular project equal to

Answer (e)

Net present value (NPV)

NPV is the difference among present value of future cash flows from any investment and

the amount invested for the acquiring the project. Present value of expected cash flow is

calculated through discounting the cash flows at the required return rate. Positive NPV signifies

better return and the negative NPV signifies worse return that is lower than zero. While any

manager requires comparing the projects and deciding regarding which one is to be selected. It

can be considered as a good approach for analysing the profitability of any investment in the

entity or any new project of the entity (Leyman and Vanhoucke 2016). NPV approach provides

various advantages like it considers the discounted cash flows while computing the computing

the value of net cash flows. Further, it considers the cost of capital and the inherent risk while

making the projections regarding future. Projection of the cash flows for 10 years into future is

definitely lower as compared to the cash flow for the next year. Looking into the NPV

calculation for the manufacturing plant of Dell Inc. it can be identified that the NPV of the

project is $ 258,659,222.81. It is signifying that the project will be able to generate the amount of

initial investment for the project. Hence, if the project is taken up it will increase the

shareholder’s wealth. Hence, considering the NPV only the project shall be accepted (Leyman

and Vanhoucke 2017)

Answer (f)

Internal rate of return and payback period

Internal rate of return (IRR) – IRR is the rate used for estimating the profitability of any

investment. It makes the discount rate of all the cash flows from the particular project equal to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL FINANCE

zero. For analysing any project on the basis of IRR, it is accepted if the IRR of the project is

more than the project’s cost of capital. Looking into the IRR of the entity it is found that the IRR

of the project is 26% whereas the cost of capital of the company is 16%. Hence, the project shall

be taken up if the IRR is considered for taking up the project (Patrick and French 2016)

Payback period – payback period is the time taken by the project for recovering the investment

cost. To be more specific, payback period is length of time taken by the project to reach the point

of break-even. Desirability of any project is directly associated with the payback period. Shorter

payback period signifies that the investment is attractive as it takes less time to recover the

amount of initial investment. Looking into the payback period computation it is found that the

payback period is 3.66 years and the discounted payback period is 5.88 years. Hence, the project

is able to recover the amount of initial expenses within the useful life of the project (Mellichamp

2017)

Hence it can be identified that from all the aspects the project is acceptable as the NPV of

the project is in positive, IRR of the project is more than the cost of capital and the payback

period is less than the useful life of the project (Magni 2016).

Answer (g)

While analysing any project or investment for the purpose of investment, the cash flows

from the projects are discounted to the present value for assuring that the undertaking’s true

value is captured. Generally, discount rate applied is based on the market rate. However, on the

basis of circumstances associated with the investment or project it is required to utilize the risk

adjusted rate of discount. Risk adjusted rate of discount reveals the relationship among return

and risk (Gorshkov et al. 2014). Practically, an investor is willing to exposed herself or himself

zero. For analysing any project on the basis of IRR, it is accepted if the IRR of the project is

more than the project’s cost of capital. Looking into the IRR of the entity it is found that the IRR

of the project is 26% whereas the cost of capital of the company is 16%. Hence, the project shall

be taken up if the IRR is considered for taking up the project (Patrick and French 2016)

Payback period – payback period is the time taken by the project for recovering the investment

cost. To be more specific, payback period is length of time taken by the project to reach the point

of break-even. Desirability of any project is directly associated with the payback period. Shorter

payback period signifies that the investment is attractive as it takes less time to recover the

amount of initial investment. Looking into the payback period computation it is found that the

payback period is 3.66 years and the discounted payback period is 5.88 years. Hence, the project

is able to recover the amount of initial expenses within the useful life of the project (Mellichamp

2017)

Hence it can be identified that from all the aspects the project is acceptable as the NPV of

the project is in positive, IRR of the project is more than the cost of capital and the payback

period is less than the useful life of the project (Magni 2016).

Answer (g)

While analysing any project or investment for the purpose of investment, the cash flows

from the projects are discounted to the present value for assuring that the undertaking’s true

value is captured. Generally, discount rate applied is based on the market rate. However, on the

basis of circumstances associated with the investment or project it is required to utilize the risk

adjusted rate of discount. Risk adjusted rate of discount reveals the relationship among return

and risk (Gorshkov et al. 2014). Practically, an investor is willing to exposed herself or himself

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL FINANCE

to more risk and it will be rewarded through higher return as greater losses can take place. This is

reflected under risk adjusted discount rate as the adjustment will make changes to the discount

rate that is based on the risk faced. Further the expected return on the investment in enhances

with the increase risk of the project. Most common adjustment to the risk is done due to the

uncertainty to timing, duration of the cash flows and dollar amount. Apart from that, uncertainty

is also there for the long term projects regarding future market scenario, level of inflation and

profitability on investment (Lane and Rosewall 2015). The risk shall be adjusted for the risk

adjusted projects based on the liquidity of the entity and the risk of default from the other parties.

Hence, the entity shall adjust the discount rate for reflecting the investment with potential to

damage the reputation of the entity that may lead to lawsuit or results into the regulatory issues.

Hence, the company’s approach of using the same discount rate for all the projects is not

appropriate and shall adjust the same based on the specific risks of the projects (Gorshkov et al.

2016).

Answer 2

Answer (a)

Total amount required to be raised through bank loan is 600 million. It is to be repaid in

10 equal instalments that is each instalment require payment of (600/10) = 60 million along with

interest. For the project to meet financial discipline, the lowest amount of cash flow that is $

14,99,94,428.07 that is the cash flow of year 8 will be considered. Hence after paying 600,00,000

as principle repayment it will left with 899,94,428.07 for meeting the interest expense. This

amount can meet up the interest rate of 15% as computed in excel.

to more risk and it will be rewarded through higher return as greater losses can take place. This is

reflected under risk adjusted discount rate as the adjustment will make changes to the discount

rate that is based on the risk faced. Further the expected return on the investment in enhances

with the increase risk of the project. Most common adjustment to the risk is done due to the

uncertainty to timing, duration of the cash flows and dollar amount. Apart from that, uncertainty

is also there for the long term projects regarding future market scenario, level of inflation and

profitability on investment (Lane and Rosewall 2015). The risk shall be adjusted for the risk

adjusted projects based on the liquidity of the entity and the risk of default from the other parties.

Hence, the entity shall adjust the discount rate for reflecting the investment with potential to

damage the reputation of the entity that may lead to lawsuit or results into the regulatory issues.

Hence, the company’s approach of using the same discount rate for all the projects is not

appropriate and shall adjust the same based on the specific risks of the projects (Gorshkov et al.

2016).

Answer 2

Answer (a)

Total amount required to be raised through bank loan is 600 million. It is to be repaid in

10 equal instalments that is each instalment require payment of (600/10) = 60 million along with

interest. For the project to meet financial discipline, the lowest amount of cash flow that is $

14,99,94,428.07 that is the cash flow of year 8 will be considered. Hence after paying 600,00,000

as principle repayment it will left with 899,94,428.07 for meeting the interest expense. This

amount can meet up the interest rate of 15% as computed in excel.

8MANAGERIAL FINANCE

Answer (b)

Pros of the new system are –

Payment of interest and principle amount can be met comfortably with the cash flow

available with the company

The company will never fall short of the amount for making payment towards the loan

over the useful life of the project.

Cons of the new system are –

Cash is just the projection and based on the same deciding regarding the loan and its

interest rate will not be appropriate.

Due to market changes or other unfavourable circumstances sales as well as cash flow in

any year may not be as expected. In such scenario the company will face liquidity issue

in meeting its debt expenses.

Conclusion and recommendation

Based on the above discussion it can be identified that in question 1, where the entity was

considering taking up the project related to manufacturing plant, it is found that from all the

aspects the project is acceptable as the NPV of the project is in positive, IRR of the project is

more than the cost of capital and the payback period is less than the useful life of the project.

Hence, it is recommended that the project shall be taken up. However, the system used by the

entity that is applying same discount rate for all projects is not appropriate and it is

recommended that it shall adjust the same based on the specific risks of the projects.

Answer (b)

Pros of the new system are –

Payment of interest and principle amount can be met comfortably with the cash flow

available with the company

The company will never fall short of the amount for making payment towards the loan

over the useful life of the project.

Cons of the new system are –

Cash is just the projection and based on the same deciding regarding the loan and its

interest rate will not be appropriate.

Due to market changes or other unfavourable circumstances sales as well as cash flow in

any year may not be as expected. In such scenario the company will face liquidity issue

in meeting its debt expenses.

Conclusion and recommendation

Based on the above discussion it can be identified that in question 1, where the entity was

considering taking up the project related to manufacturing plant, it is found that from all the

aspects the project is acceptable as the NPV of the project is in positive, IRR of the project is

more than the cost of capital and the payback period is less than the useful life of the project.

Hence, it is recommended that the project shall be taken up. However, the system used by the

entity that is applying same discount rate for all projects is not appropriate and it is

recommended that it shall adjust the same based on the specific risks of the projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL FINANCE

Reference

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of calculating

the payback period of investment for renovation of building facades. Stroitel'stvo Unikal'nyh

Zdanij i Sooruzenij, (2), p.82.

Gorshkov, A.S., Vatin, N.I., Rymkevich, P.P. and Kydrevich, O.O., 2018. Payback period of

investments in energy saving. Magazine of Civil Engineering, 78(2).

Lane, K. and Rosewall, T., 2015. Firms’ investment decisions and interest rates. Reserve Bank of

Australia Bulletin. June quarter, pp.1-7.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization for

resource-constrained project scheduling. Computers & Industrial Engineering, 91, pp.139-153.

Leyman, P. and Vanhoucke, M., 2017. Capital-and resource-constrained project scheduling with

net present value optimization. European Journal of Operational Research, 256(3), pp.757-776.

Magni, C.A., 2016. Capital depreciation and the underdetermination of rate of return: A unifying

perspective. Journal of Mathematical Economics, 67, pp.54-79.

Mellichamp, D.A., 2017. Internal rate of return: Good and bad features, and a new way of

interpreting the historic measure. Computers & Chemical Engineering, 106, pp.396-406.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks and

pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

Žižlavský, O., 2014. Net present value approach: method for economic assessment of innovation

projects. Procedia-Social and Behavioral Sciences, 156, pp.506-512.

Reference

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of calculating

the payback period of investment for renovation of building facades. Stroitel'stvo Unikal'nyh

Zdanij i Sooruzenij, (2), p.82.

Gorshkov, A.S., Vatin, N.I., Rymkevich, P.P. and Kydrevich, O.O., 2018. Payback period of

investments in energy saving. Magazine of Civil Engineering, 78(2).

Lane, K. and Rosewall, T., 2015. Firms’ investment decisions and interest rates. Reserve Bank of

Australia Bulletin. June quarter, pp.1-7.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization for

resource-constrained project scheduling. Computers & Industrial Engineering, 91, pp.139-153.

Leyman, P. and Vanhoucke, M., 2017. Capital-and resource-constrained project scheduling with

net present value optimization. European Journal of Operational Research, 256(3), pp.757-776.

Magni, C.A., 2016. Capital depreciation and the underdetermination of rate of return: A unifying

perspective. Journal of Mathematical Economics, 67, pp.54-79.

Mellichamp, D.A., 2017. Internal rate of return: Good and bad features, and a new way of

interpreting the historic measure. Computers & Chemical Engineering, 106, pp.396-406.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks and

pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

Žižlavský, O., 2014. Net present value approach: method for economic assessment of innovation

projects. Procedia-Social and Behavioral Sciences, 156, pp.506-512.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL FINANCE

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.