ACC511 Financial Management: Capital Investment Decisions Analysis

VerifiedAdded on 2023/06/15

|20

|3256

|300

Project

AI Summary

This project provides a comprehensive analysis of capital investment decisions in two different cases. The first case, Dukeview Corporation Limited (DCL), evaluates a new contract opportunity using techniques like net present value (NPV), payback period, internal rate of return (IRR), accounting rate of return (ARR), and profitability index (PI). The analysis reveals mixed results, with some techniques favoring acceptance and others suggesting rejection. The second case, Curtis Industries Limited (CIL), assesses the financial feasibility of investing in a new contract, including NPV calculation and sensitivity analysis to changes in unit sales, selling price, and cost of capital. The project also includes a scenario analysis comparing it with sensitivity analysis and pricing of risk. The solution provides detailed calculations and explanations for each technique, offering valuable insights into the decision-making process for capital investments.

Running Head: Financial Management

Capital Investment Decisions

Capital Investment Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 1

Executive Summary:

In this project, two different cases will be analysed on the basis of various capital budgeting

techniques. In the first case of Dukeview Corporation Limited (DCL), the new contract

opportunity will be assessed on the basis of techniques like net present value, payback period,

internal rate of return, accounting rate of return and profitability index. Few of these

techniques will provide favourable results for the acceptance of the project and few of them

will be offering unfavourable results for the acceptance of the project. In the other case of

Curtis Industries Limited (CIL), the investment in new contract will be analysed to determine

its financial feasibility. Under this part, along with net present value calculation of cash flows

of project, the sensitivity analysis of the project will also be carried to assess the sensitivity of

project to the change in number of units sold or change in selling price and also change in

cost of capital.

Executive Summary:

In this project, two different cases will be analysed on the basis of various capital budgeting

techniques. In the first case of Dukeview Corporation Limited (DCL), the new contract

opportunity will be assessed on the basis of techniques like net present value, payback period,

internal rate of return, accounting rate of return and profitability index. Few of these

techniques will provide favourable results for the acceptance of the project and few of them

will be offering unfavourable results for the acceptance of the project. In the other case of

Curtis Industries Limited (CIL), the investment in new contract will be analysed to determine

its financial feasibility. Under this part, along with net present value calculation of cash flows

of project, the sensitivity analysis of the project will also be carried to assess the sensitivity of

project to the change in number of units sold or change in selling price and also change in

cost of capital.

Financial Management 2

Table of Contents

Executive Summary...............................................................................................................................1

Question 1:............................................................................................................................................3

Loan Schedule....................................................................................................................................3

1) Net Present Value Calculation...................................................................................................3

2) Internal Rate of Return Calculation...........................................................................................4

3) Payback Period..........................................................................................................................5

4) Accounting Rate of Return.........................................................................................................5

5) Profitability Index......................................................................................................................6

6) Analysis......................................................................................................................................7

Question 2...........................................................................................................................................10

Table showing calculations of cash flows after tax..........................................................................11

Part 1: Calculation of NPV................................................................................................................12

Part 2: Sensitivity Analysis...............................................................................................................13

Part 3: Scenario Analysis over Sensitivity Analysis...........................................................................18

Part 4: Pricing of Risk.......................................................................................................................18

References...........................................................................................................................................20

Table of Contents

Executive Summary...............................................................................................................................1

Question 1:............................................................................................................................................3

Loan Schedule....................................................................................................................................3

1) Net Present Value Calculation...................................................................................................3

2) Internal Rate of Return Calculation...........................................................................................4

3) Payback Period..........................................................................................................................5

4) Accounting Rate of Return.........................................................................................................5

5) Profitability Index......................................................................................................................6

6) Analysis......................................................................................................................................7

Question 2...........................................................................................................................................10

Table showing calculations of cash flows after tax..........................................................................11

Part 1: Calculation of NPV................................................................................................................12

Part 2: Sensitivity Analysis...............................................................................................................13

Part 3: Scenario Analysis over Sensitivity Analysis...........................................................................18

Part 4: Pricing of Risk.......................................................................................................................18

References...........................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 3

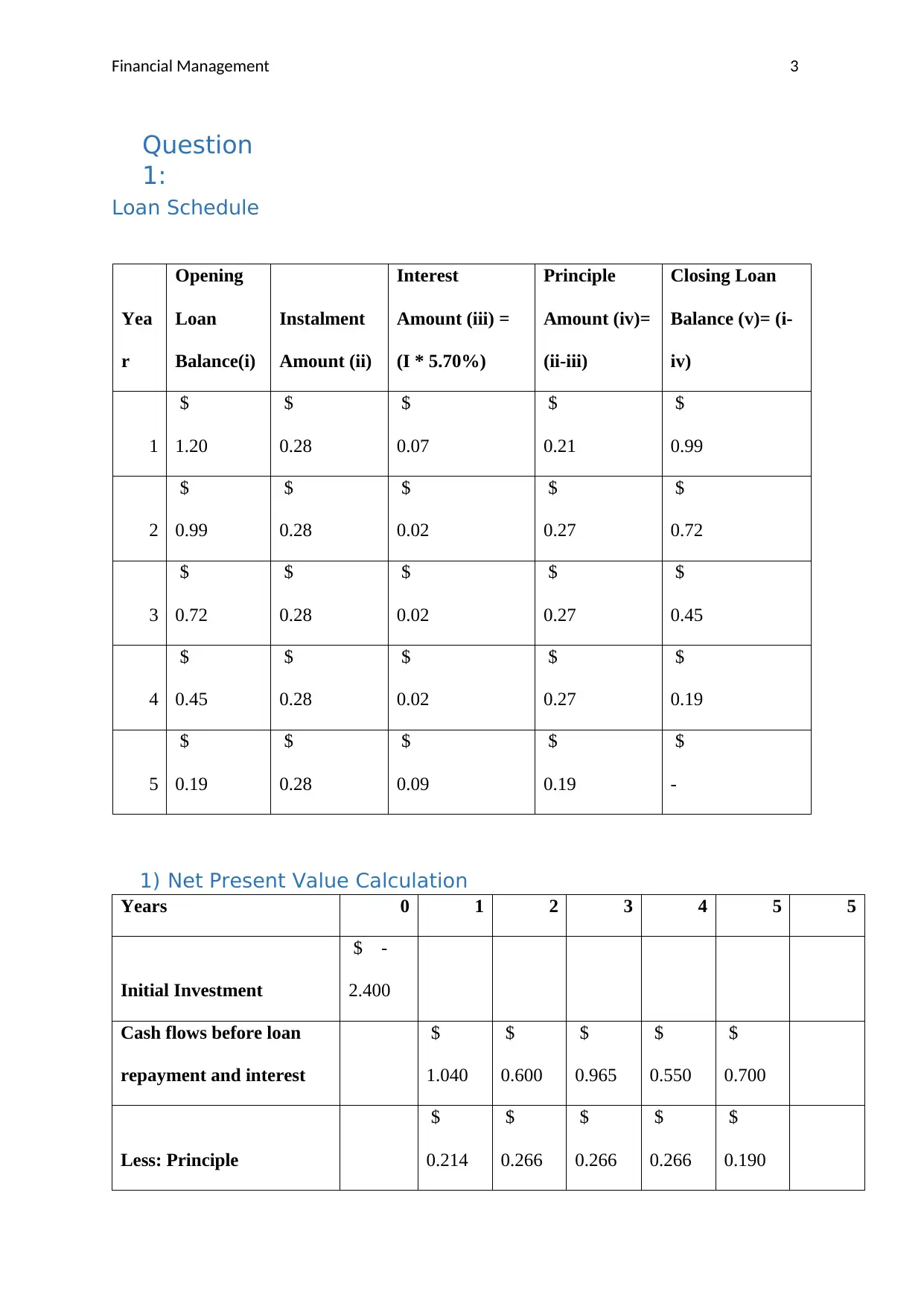

Question

1:

Loan Schedule

Yea

r

Opening

Loan

Balance(i)

Instalment

Amount (ii)

Interest

Amount (iii) =

(I * 5.70%)

Principle

Amount (iv)=

(ii-iii)

Closing Loan

Balance (v)= (i-

iv)

1

$

1.20

$

0.28

$

0.07

$

0.21

$

0.99

2

$

0.99

$

0.28

$

0.02

$

0.27

$

0.72

3

$

0.72

$

0.28

$

0.02

$

0.27

$

0.45

4

$

0.45

$

0.28

$

0.02

$

0.27

$

0.19

5

$

0.19

$

0.28

$

0.09

$

0.19

$

-

1) Net Present Value Calculation

Years 0 1 2 3 4 5 5

Initial Investment

$ -

2.400

Cash flows before loan

repayment and interest

$

1.040

$

0.600

$

0.965

$

0.550

$

0.700

Less: Principle

$

0.214

$

0.266

$

0.266

$

0.266

$

0.190

Question

1:

Loan Schedule

Yea

r

Opening

Loan

Balance(i)

Instalment

Amount (ii)

Interest

Amount (iii) =

(I * 5.70%)

Principle

Amount (iv)=

(ii-iii)

Closing Loan

Balance (v)= (i-

iv)

1

$

1.20

$

0.28

$

0.07

$

0.21

$

0.99

2

$

0.99

$

0.28

$

0.02

$

0.27

$

0.72

3

$

0.72

$

0.28

$

0.02

$

0.27

$

0.45

4

$

0.45

$

0.28

$

0.02

$

0.27

$

0.19

5

$

0.19

$

0.28

$

0.09

$

0.19

$

-

1) Net Present Value Calculation

Years 0 1 2 3 4 5 5

Initial Investment

$ -

2.400

Cash flows before loan

repayment and interest

$

1.040

$

0.600

$

0.965

$

0.550

$

0.700

Less: Principle

$

0.214

$

0.266

$

0.266

$

0.266

$

0.190

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

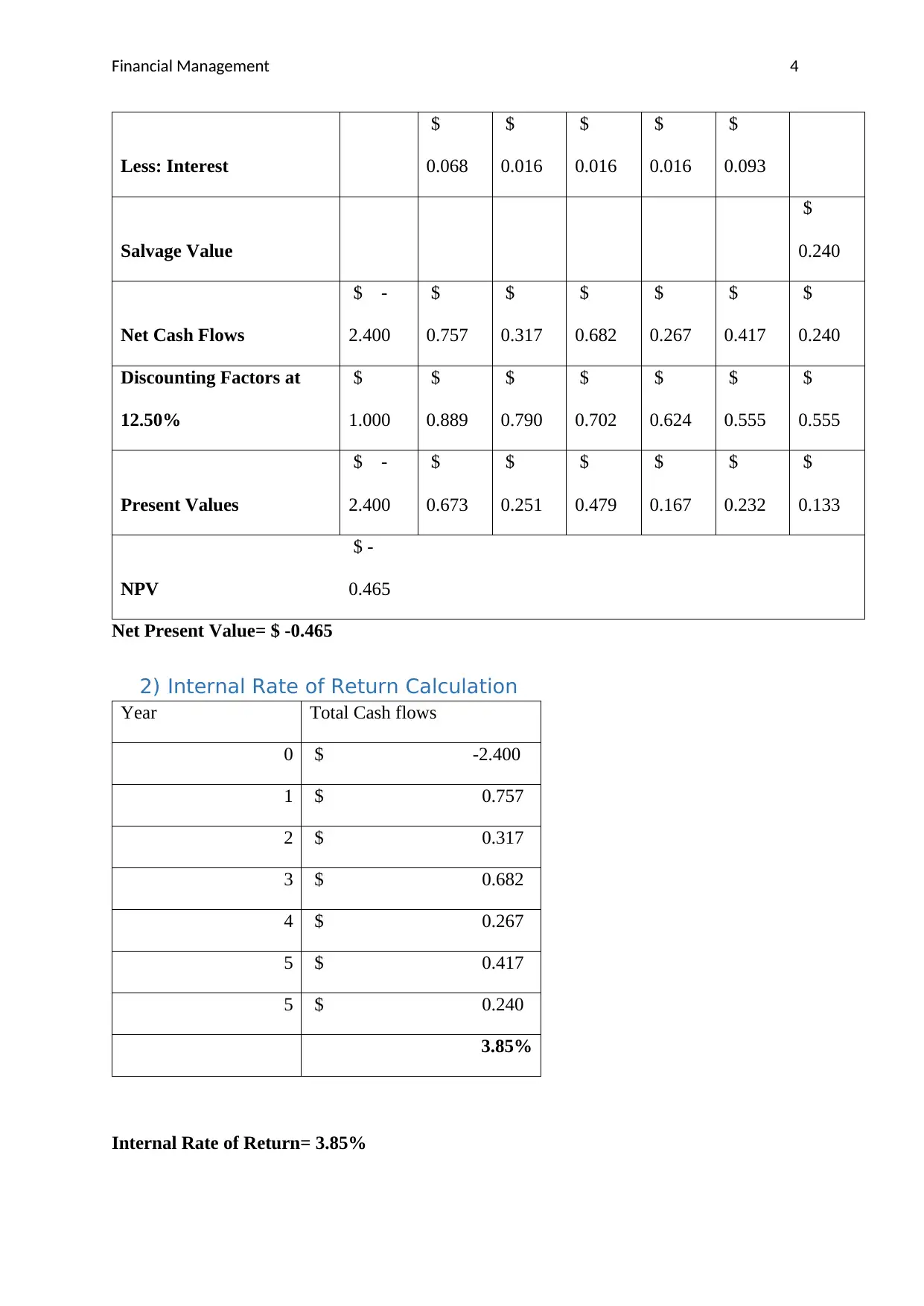

Financial Management 4

Less: Interest

$

0.068

$

0.016

$

0.016

$

0.016

$

0.093

Salvage Value

$

0.240

Net Cash Flows

$ -

2.400

$

0.757

$

0.317

$

0.682

$

0.267

$

0.417

$

0.240

Discounting Factors at

12.50%

$

1.000

$

0.889

$

0.790

$

0.702

$

0.624

$

0.555

$

0.555

Present Values

$ -

2.400

$

0.673

$

0.251

$

0.479

$

0.167

$

0.232

$

0.133

NPV

$ -

0.465

Net Present Value= $ -0.465

2) Internal Rate of Return Calculation

Year Total Cash flows

0 $ -2.400

1 $ 0.757

2 $ 0.317

3 $ 0.682

4 $ 0.267

5 $ 0.417

5 $ 0.240

3.85%

Internal Rate of Return= 3.85%

Less: Interest

$

0.068

$

0.016

$

0.016

$

0.016

$

0.093

Salvage Value

$

0.240

Net Cash Flows

$ -

2.400

$

0.757

$

0.317

$

0.682

$

0.267

$

0.417

$

0.240

Discounting Factors at

12.50%

$

1.000

$

0.889

$

0.790

$

0.702

$

0.624

$

0.555

$

0.555

Present Values

$ -

2.400

$

0.673

$

0.251

$

0.479

$

0.167

$

0.232

$

0.133

NPV

$ -

0.465

Net Present Value= $ -0.465

2) Internal Rate of Return Calculation

Year Total Cash flows

0 $ -2.400

1 $ 0.757

2 $ 0.317

3 $ 0.682

4 $ 0.267

5 $ 0.417

5 $ 0.240

3.85%

Internal Rate of Return= 3.85%

Financial Management 5

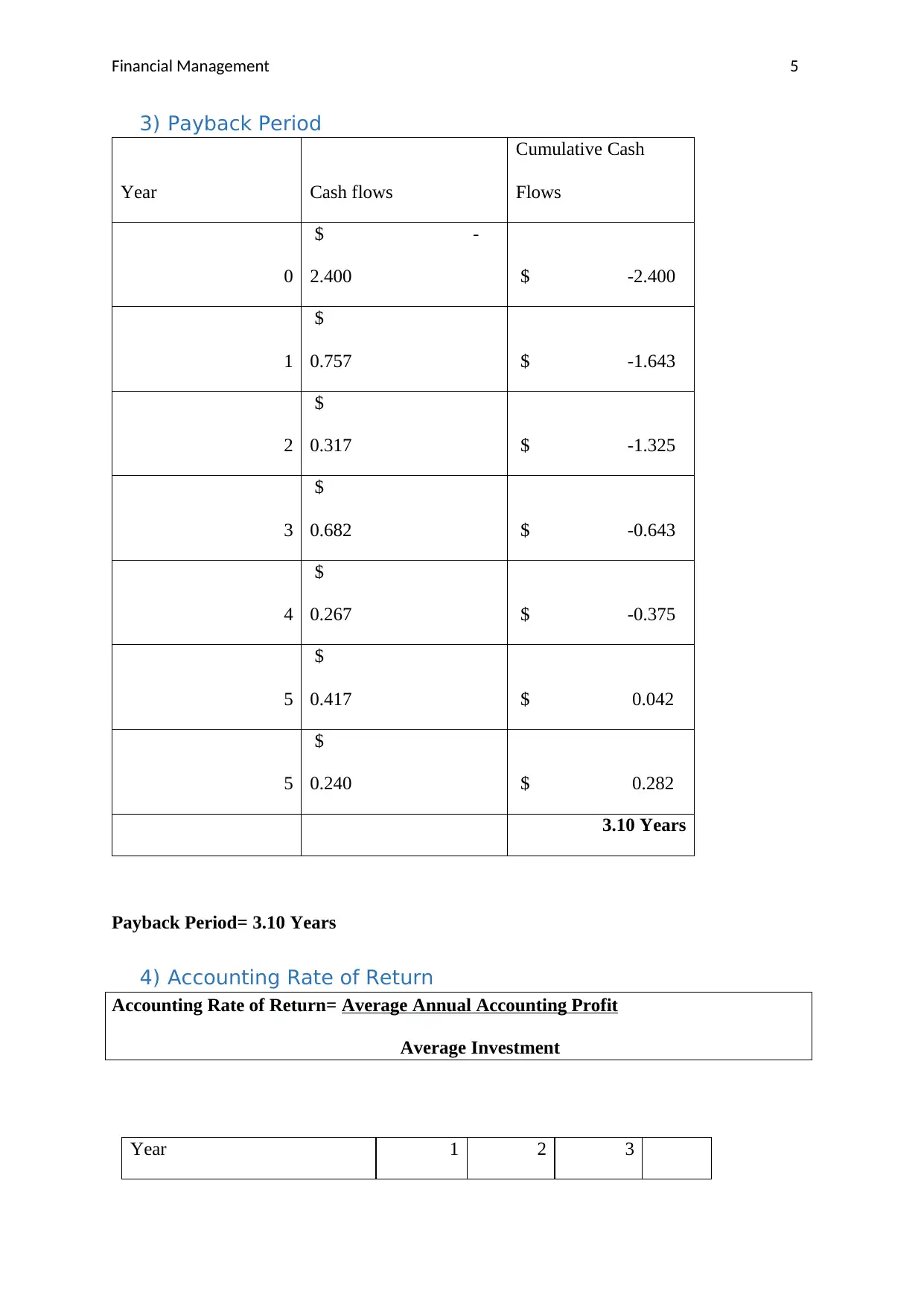

3) Payback Period

Year Cash flows

Cumulative Cash

Flows

0

$ -

2.400 $ -2.400

1

$

0.757 $ -1.643

2

$

0.317 $ -1.325

3

$

0.682 $ -0.643

4

$

0.267 $ -0.375

5

$

0.417 $ 0.042

5

$

0.240 $ 0.282

3.10 Years

Payback Period= 3.10 Years

4) Accounting Rate of Return

Accounting Rate of Return= Average Annual Accounting Profit

Average Investment

Year 1 2 3

3) Payback Period

Year Cash flows

Cumulative Cash

Flows

0

$ -

2.400 $ -2.400

1

$

0.757 $ -1.643

2

$

0.317 $ -1.325

3

$

0.682 $ -0.643

4

$

0.267 $ -0.375

5

$

0.417 $ 0.042

5

$

0.240 $ 0.282

3.10 Years

Payback Period= 3.10 Years

4) Accounting Rate of Return

Accounting Rate of Return= Average Annual Accounting Profit

Average Investment

Year 1 2 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 6

Cash Flows

$

1.0400

$

0.6000

$

0.9650

$

0.5500

Less: Depreciation

$

0.960

$

0.576

$

0.346

$

0.207

Less: Interest

$

0.068

$

0.016

$

0.016

$

0.016

Net Profits

$

0.012

$

0.008

$

0.603

$

0.327

Average Profits = 0.012 + 0.008 + 0.603 + 0.327 + 0.483 =$ 0.286

5

Average Investment= salvage value + 0.5 (Initial investment – salvage value)

= .0240 + 0.5 (2.40-.0240)

= $ 1.32

Accounting Rate of Return= 22%

5) Profitability Index

Profitability Index =

NPV + Initial investment

Initial investment

= 1.935

2.40

= .81

Cash Flows

$

1.0400

$

0.6000

$

0.9650

$

0.5500

Less: Depreciation

$

0.960

$

0.576

$

0.346

$

0.207

Less: Interest

$

0.068

$

0.016

$

0.016

$

0.016

Net Profits

$

0.012

$

0.008

$

0.603

$

0.327

Average Profits = 0.012 + 0.008 + 0.603 + 0.327 + 0.483 =$ 0.286

5

Average Investment= salvage value + 0.5 (Initial investment – salvage value)

= .0240 + 0.5 (2.40-.0240)

= $ 1.32

Accounting Rate of Return= 22%

5) Profitability Index

Profitability Index =

NPV + Initial investment

Initial investment

= 1.935

2.40

= .81

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 7

6) Analysis

The net present value of the project is negative ($ -0.465) and it indicates that the project will

not generate sufficient cash inflows to recover its cash outflows and hence it must not be

accepted (Bierman & Smidt, 2012).

The payback period of 3.10 years whereas DCL has a policy of repaying its capital

investment within 2.50 years. Payback of 3.10 years signifies that the project will recover its

initial outlays in 3.10 years and after this period it will start generating returns. Hence, it must

not be accepted (Kahraman, 2001).

The internal rate of return of the project is 3.85% which is quite lesser than the required rate

of return of the project i.e. 12.50% and hence it must not be accepted as IRR is the

discounting rate at which the project has no profit and no loss (Ryan & Ryan, 2002).

The accounting rate of return of the project is 21.70% which is greater than the project’s

desired rate of return. Hence, the project can be accepted from the standpoint of ARR.

Lastly, the profitability index of any project must be at least one for its acceptance by the

managers. However, in the present project, the PI is 0.81. Hence, the project must not be

accepted from the viewpoint of profitability index (Graham & Harvey, 2002).

The four out of five capital budgeting techniques which are mostly used to evaluate the

appropriateness of capital investment decision are providing unfavourable results for the

acceptance of the project. Those techniques are NPV, IRR, Payback period and Profitability

index.

The treatment of loan repayments and salvage value of the project equipment is explained as

below:

The loan instalment includes both interest and principle element. The entire instalment

amount of the loan per year is deducted from the cash flow amount of each particular year to

6) Analysis

The net present value of the project is negative ($ -0.465) and it indicates that the project will

not generate sufficient cash inflows to recover its cash outflows and hence it must not be

accepted (Bierman & Smidt, 2012).

The payback period of 3.10 years whereas DCL has a policy of repaying its capital

investment within 2.50 years. Payback of 3.10 years signifies that the project will recover its

initial outlays in 3.10 years and after this period it will start generating returns. Hence, it must

not be accepted (Kahraman, 2001).

The internal rate of return of the project is 3.85% which is quite lesser than the required rate

of return of the project i.e. 12.50% and hence it must not be accepted as IRR is the

discounting rate at which the project has no profit and no loss (Ryan & Ryan, 2002).

The accounting rate of return of the project is 21.70% which is greater than the project’s

desired rate of return. Hence, the project can be accepted from the standpoint of ARR.

Lastly, the profitability index of any project must be at least one for its acceptance by the

managers. However, in the present project, the PI is 0.81. Hence, the project must not be

accepted from the viewpoint of profitability index (Graham & Harvey, 2002).

The four out of five capital budgeting techniques which are mostly used to evaluate the

appropriateness of capital investment decision are providing unfavourable results for the

acceptance of the project. Those techniques are NPV, IRR, Payback period and Profitability

index.

The treatment of loan repayments and salvage value of the project equipment is explained as

below:

The loan instalment includes both interest and principle element. The entire instalment

amount of the loan per year is deducted from the cash flow amount of each particular year to

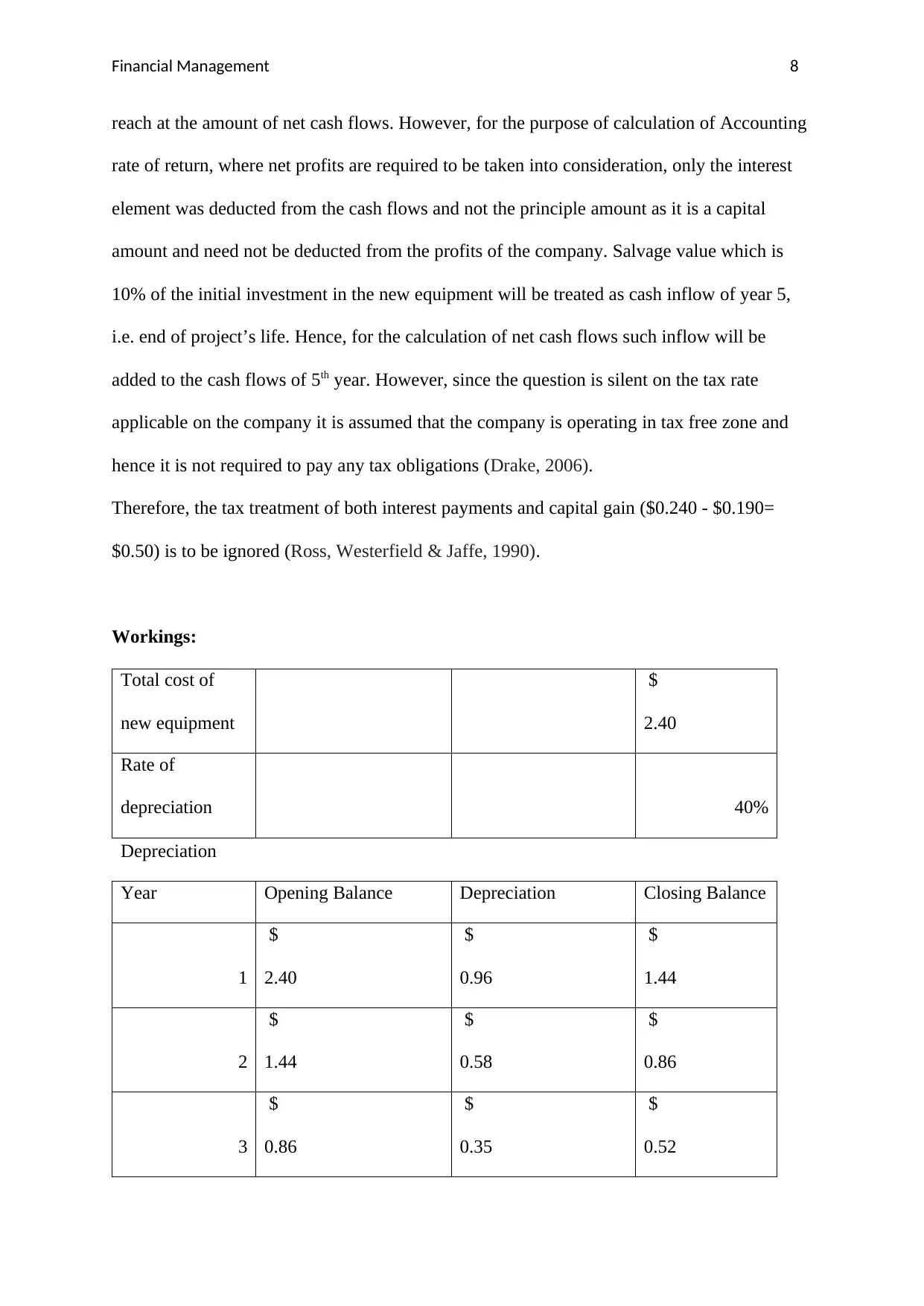

Financial Management 8

reach at the amount of net cash flows. However, for the purpose of calculation of Accounting

rate of return, where net profits are required to be taken into consideration, only the interest

element was deducted from the cash flows and not the principle amount as it is a capital

amount and need not be deducted from the profits of the company. Salvage value which is

10% of the initial investment in the new equipment will be treated as cash inflow of year 5,

i.e. end of project’s life. Hence, for the calculation of net cash flows such inflow will be

added to the cash flows of 5th year. However, since the question is silent on the tax rate

applicable on the company it is assumed that the company is operating in tax free zone and

hence it is not required to pay any tax obligations (Drake, 2006).

Therefore, the tax treatment of both interest payments and capital gain ($0.240 - $0.190=

$0.50) is to be ignored (Ross, Westerfield & Jaffe, 1990).

Workings:

Total cost of

new equipment

$

2.40

Rate of

depreciation 40%

Depreciation

Year Opening Balance Depreciation Closing Balance

1

$

2.40

$

0.96

$

1.44

2

$

1.44

$

0.58

$

0.86

3

$

0.86

$

0.35

$

0.52

reach at the amount of net cash flows. However, for the purpose of calculation of Accounting

rate of return, where net profits are required to be taken into consideration, only the interest

element was deducted from the cash flows and not the principle amount as it is a capital

amount and need not be deducted from the profits of the company. Salvage value which is

10% of the initial investment in the new equipment will be treated as cash inflow of year 5,

i.e. end of project’s life. Hence, for the calculation of net cash flows such inflow will be

added to the cash flows of 5th year. However, since the question is silent on the tax rate

applicable on the company it is assumed that the company is operating in tax free zone and

hence it is not required to pay any tax obligations (Drake, 2006).

Therefore, the tax treatment of both interest payments and capital gain ($0.240 - $0.190=

$0.50) is to be ignored (Ross, Westerfield & Jaffe, 1990).

Workings:

Total cost of

new equipment

$

2.40

Rate of

depreciation 40%

Depreciation

Year Opening Balance Depreciation Closing Balance

1

$

2.40

$

0.96

$

1.44

2

$

1.44

$

0.58

$

0.86

3

$

0.86

$

0.35

$

0.52

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 9

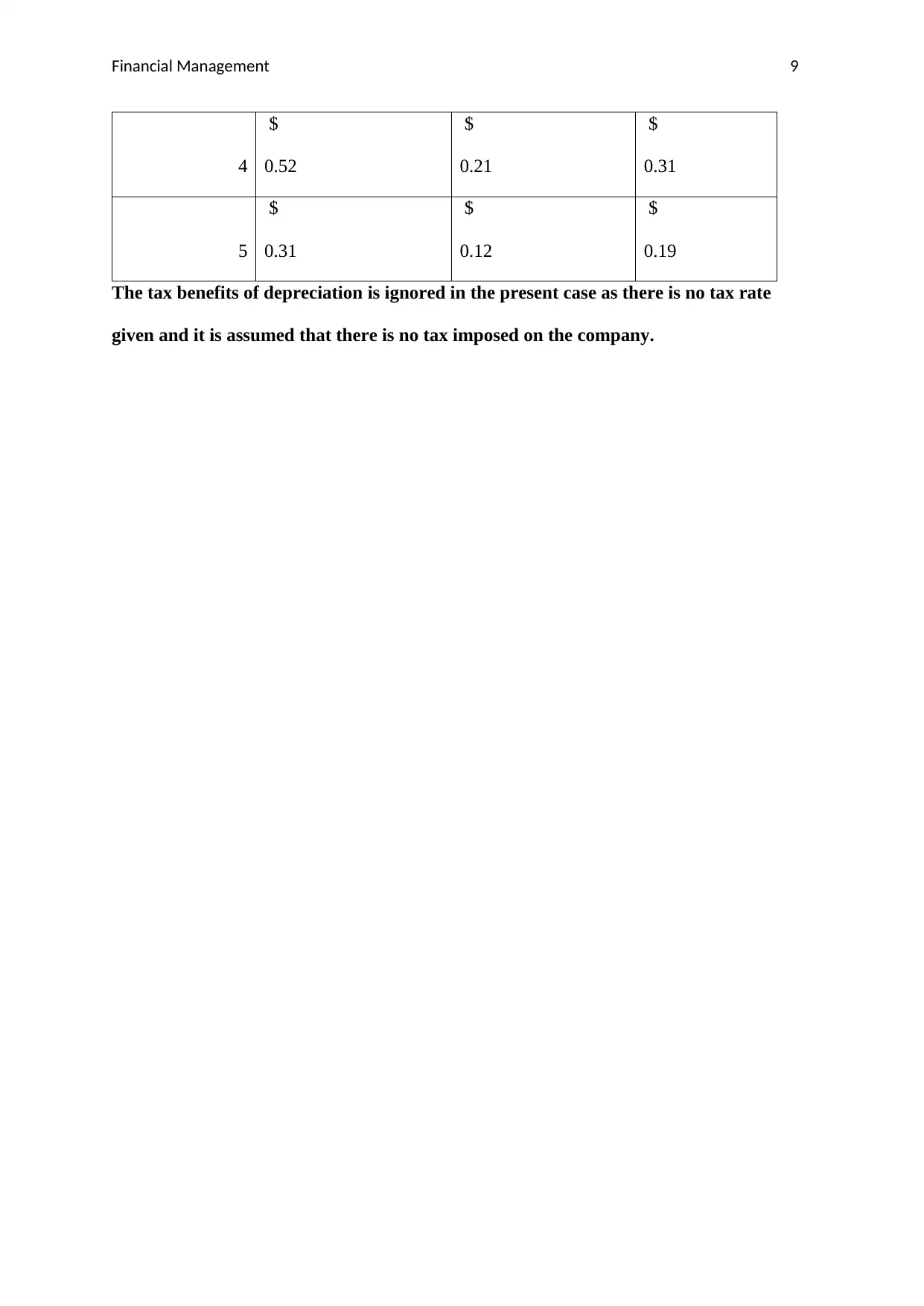

4

$

0.52

$

0.21

$

0.31

5

$

0.31

$

0.12

$

0.19

The tax benefits of depreciation is ignored in the present case as there is no tax rate

given and it is assumed that there is no tax imposed on the company.

4

$

0.52

$

0.21

$

0.31

5

$

0.31

$

0.12

$

0.19

The tax benefits of depreciation is ignored in the present case as there is no tax rate

given and it is assumed that there is no tax imposed on the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 10

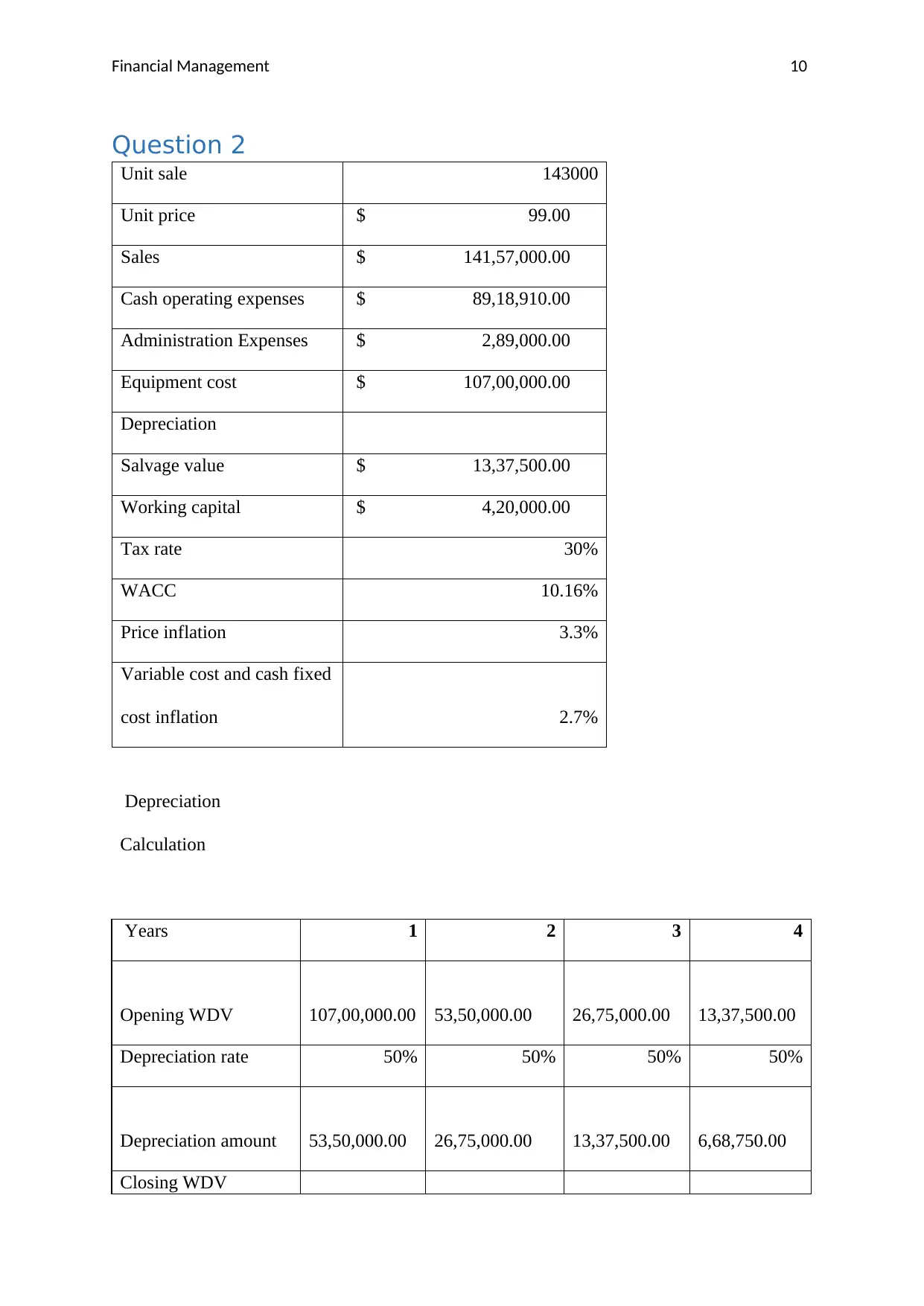

Question 2

Unit sale 143000

Unit price $ 99.00

Sales $ 141,57,000.00

Cash operating expenses $ 89,18,910.00

Administration Expenses $ 2,89,000.00

Equipment cost $ 107,00,000.00

Depreciation

Salvage value $ 13,37,500.00

Working capital $ 4,20,000.00

Tax rate 30%

WACC 10.16%

Price inflation 3.3%

Variable cost and cash fixed

cost inflation 2.7%

Depreciation

Calculation

Years 1 2 3 4

Opening WDV 107,00,000.00 53,50,000.00 26,75,000.00 13,37,500.00

Depreciation rate 50% 50% 50% 50%

Depreciation amount 53,50,000.00 26,75,000.00 13,37,500.00 6,68,750.00

Closing WDV

Question 2

Unit sale 143000

Unit price $ 99.00

Sales $ 141,57,000.00

Cash operating expenses $ 89,18,910.00

Administration Expenses $ 2,89,000.00

Equipment cost $ 107,00,000.00

Depreciation

Salvage value $ 13,37,500.00

Working capital $ 4,20,000.00

Tax rate 30%

WACC 10.16%

Price inflation 3.3%

Variable cost and cash fixed

cost inflation 2.7%

Depreciation

Calculation

Years 1 2 3 4

Opening WDV 107,00,000.00 53,50,000.00 26,75,000.00 13,37,500.00

Depreciation rate 50% 50% 50% 50%

Depreciation amount 53,50,000.00 26,75,000.00 13,37,500.00 6,68,750.00

Closing WDV

Financial Management 11

53,50,000.00 26,75,000.00 13,37,500.00 6,68,750.00

Depreciation is calculated in the following manner:

First of all, the rate of depreciation as per Straight line method is calculated by dividing the

whole percentage by years of useful life i.e. years. This provided SLM depreciation rate of

25% p.a. This rate was then doubled as per the requirement of method of depreciation given

in the question. The doubled rate of depreciation i.e. 50% was applied according to the

diminishing balance method of depreciation.

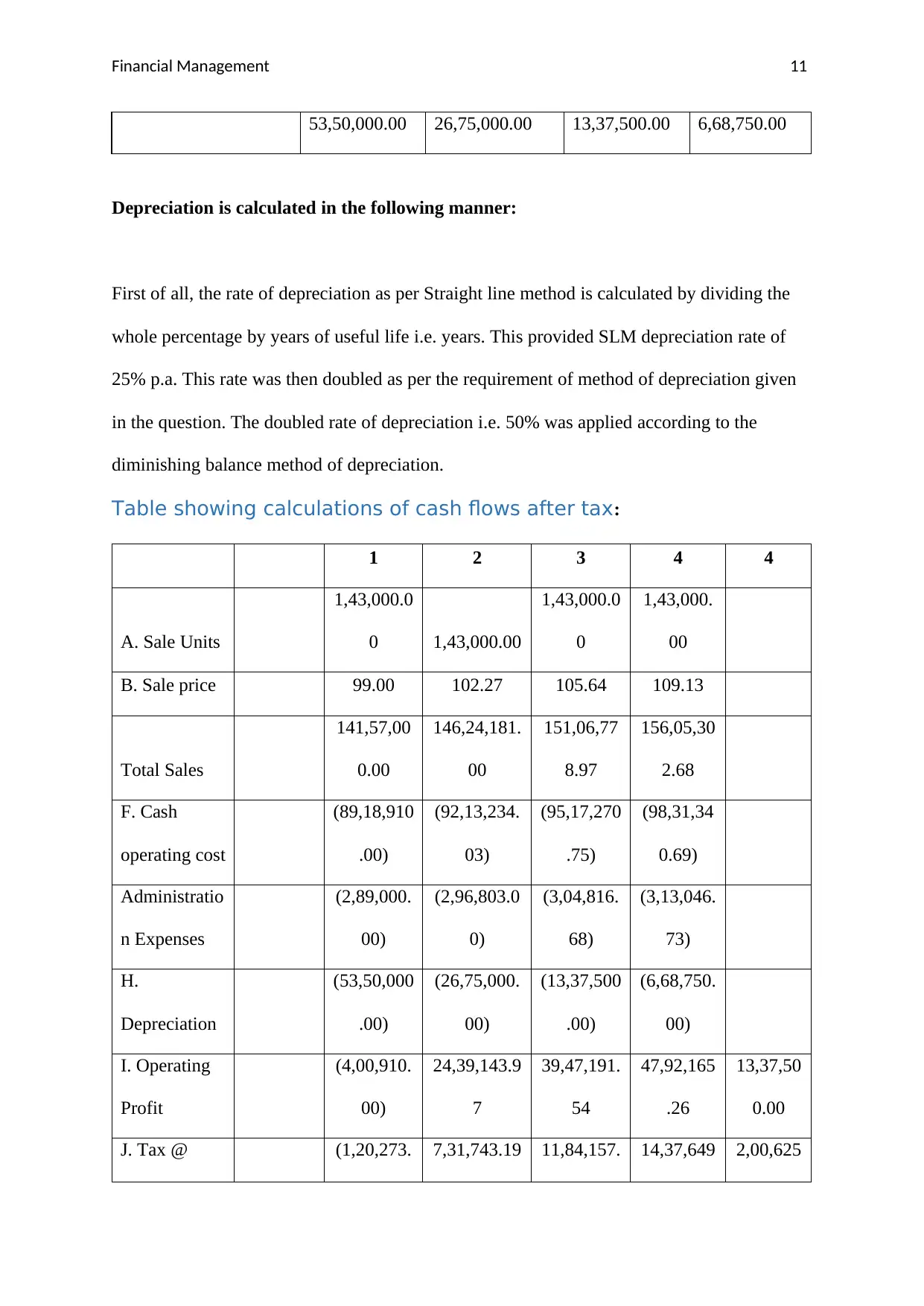

Table showing calculations of cash flows after tax:

1 2 3 4 4

A. Sale Units

1,43,000.0

0 1,43,000.00

1,43,000.0

0

1,43,000.

00

B. Sale price 99.00 102.27 105.64 109.13

Total Sales

141,57,00

0.00

146,24,181.

00

151,06,77

8.97

156,05,30

2.68

F. Cash

operating cost

(89,18,910

.00)

(92,13,234.

03)

(95,17,270

.75)

(98,31,34

0.69)

Administratio

n Expenses

(2,89,000.

00)

(2,96,803.0

0)

(3,04,816.

68)

(3,13,046.

73)

H.

Depreciation

(53,50,000

.00)

(26,75,000.

00)

(13,37,500

.00)

(6,68,750.

00)

I. Operating

Profit

(4,00,910.

00)

24,39,143.9

7

39,47,191.

54

47,92,165

.26

13,37,50

0.00

J. Tax @ (1,20,273. 7,31,743.19 11,84,157. 14,37,649 2,00,625

53,50,000.00 26,75,000.00 13,37,500.00 6,68,750.00

Depreciation is calculated in the following manner:

First of all, the rate of depreciation as per Straight line method is calculated by dividing the

whole percentage by years of useful life i.e. years. This provided SLM depreciation rate of

25% p.a. This rate was then doubled as per the requirement of method of depreciation given

in the question. The doubled rate of depreciation i.e. 50% was applied according to the

diminishing balance method of depreciation.

Table showing calculations of cash flows after tax:

1 2 3 4 4

A. Sale Units

1,43,000.0

0 1,43,000.00

1,43,000.0

0

1,43,000.

00

B. Sale price 99.00 102.27 105.64 109.13

Total Sales

141,57,00

0.00

146,24,181.

00

151,06,77

8.97

156,05,30

2.68

F. Cash

operating cost

(89,18,910

.00)

(92,13,234.

03)

(95,17,270

.75)

(98,31,34

0.69)

Administratio

n Expenses

(2,89,000.

00)

(2,96,803.0

0)

(3,04,816.

68)

(3,13,046.

73)

H.

Depreciation

(53,50,000

.00)

(26,75,000.

00)

(13,37,500

.00)

(6,68,750.

00)

I. Operating

Profit

(4,00,910.

00)

24,39,143.9

7

39,47,191.

54

47,92,165

.26

13,37,50

0.00

J. Tax @ (1,20,273. 7,31,743.19 11,84,157. 14,37,649 2,00,625

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.