Charles Sturt University: ACC515 Accounting and Finance Assignment

VerifiedAdded on 2023/01/17

|15

|2535

|30

Homework Assignment

AI Summary

This assignment solution for ACC515, an accounting and finance course, addresses various financial concepts and calculations. It begins with calculating savings needed for a holiday and analyzing investment decisions using NPV. The solution explores real interest rates, negative gearing in the Australian housing market, and defines investment risk. It further explains the Australian dividend imputation credit system and calculates monthly returns, average returns, and annual holding periods for BHP and the Australian market, including risk measured by standard deviation, CAPM values, and portfolio analysis. The assignment includes graphs illustrating market trends and provides a comprehensive overview of financial analysis and investment strategies. The document covers real interest rate calculations, negative gearing, risk assessment, dividend imputation, CAPM, and portfolio return calculations, and provides a comprehensive analysis of the Australian financial market.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Question 1:.......................................................................................................................................3

a) Calculating the monthly amount needed to save for before the holiday:....................................3

bi) Indicating whether investment will be purchased:.....................................................................3

bii) Indicating what will be value of cash flow at the end of year 2:..............................................4

ci) Calculating the value of Gaye’s financial assets when she retires at the age of 60:..................4

cii) Calculating the monthly pension amount that Gaye will receive on her retirement:................5

Question 2:.......................................................................................................................................5

i) Explaining the concept of Real Rate of Interest with adequate example:....................................5

ii) Defining the negative gearing in context of Australian housing market and provide a general

evaluation of the Australian economy and society:.........................................................................6

Question 3:.......................................................................................................................................7

i) Defining risk in terms of investment:...........................................................................................7

ii) Explaining the Australian dividend imputation credit system, where Australian resident and

international investors:.....................................................................................................................8

iii) Calculating the monthly returns in $ and %:..............................................................................8

iv) Calculating the average monthly return for BHP:......................................................................9

v) Calculating the annual holding period for international shareholders for BHP:.........................9

vi) Calculating the annual holding period for Australian shareholders for BHP:...........................9

vii) Calculating the MKT monthly returns for Australian market:..................................................9

viii) Calculating the average monthly return for MKT:................................................................10

ix) Calculating the annual holding period return for the Australian Share market:......................10

x) Drawing the graph for BHP and MKT:.....................................................................................11

Table of Contents

Question 1:.......................................................................................................................................3

a) Calculating the monthly amount needed to save for before the holiday:....................................3

bi) Indicating whether investment will be purchased:.....................................................................3

bii) Indicating what will be value of cash flow at the end of year 2:..............................................4

ci) Calculating the value of Gaye’s financial assets when she retires at the age of 60:..................4

cii) Calculating the monthly pension amount that Gaye will receive on her retirement:................5

Question 2:.......................................................................................................................................5

i) Explaining the concept of Real Rate of Interest with adequate example:....................................5

ii) Defining the negative gearing in context of Australian housing market and provide a general

evaluation of the Australian economy and society:.........................................................................6

Question 3:.......................................................................................................................................7

i) Defining risk in terms of investment:...........................................................................................7

ii) Explaining the Australian dividend imputation credit system, where Australian resident and

international investors:.....................................................................................................................8

iii) Calculating the monthly returns in $ and %:..............................................................................8

iv) Calculating the average monthly return for BHP:......................................................................9

v) Calculating the annual holding period for international shareholders for BHP:.........................9

vi) Calculating the annual holding period for Australian shareholders for BHP:...........................9

vii) Calculating the MKT monthly returns for Australian market:..................................................9

viii) Calculating the average monthly return for MKT:................................................................10

ix) Calculating the annual holding period return for the Australian Share market:......................10

x) Drawing the graph for BHP and MKT:.....................................................................................11

2ACCOUNTING AND FINANCE

xi) Calculating the risk measured for by standard deviation for both BHP and MKT:.................11

xii) Detecting how risky is BHP:...................................................................................................11

xiii) Calculating the CAPM value for BHP:..................................................................................11

xiv) Plotting the SML in scatter graph:.........................................................................................12

xv) Recreating the graph with actual return of BHP:....................................................................13

xvi) Calculating the return and beta for portfolio:.........................................................................13

References:....................................................................................................................................14

xi) Calculating the risk measured for by standard deviation for both BHP and MKT:.................11

xii) Detecting how risky is BHP:...................................................................................................11

xiii) Calculating the CAPM value for BHP:..................................................................................11

xiv) Plotting the SML in scatter graph:.........................................................................................12

xv) Recreating the graph with actual return of BHP:....................................................................13

xvi) Calculating the return and beta for portfolio:.........................................................................13

References:....................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

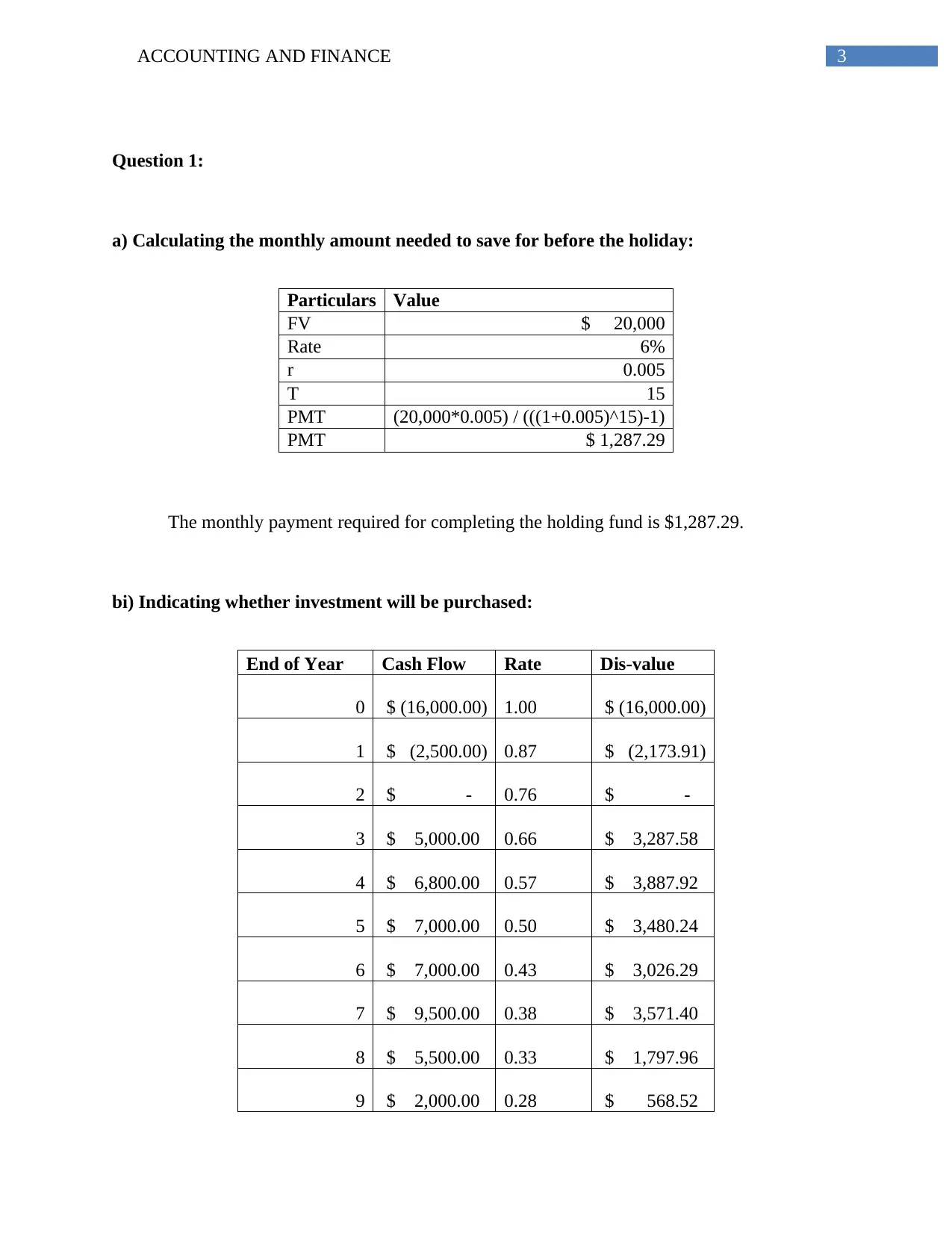

Question 1:

a) Calculating the monthly amount needed to save for before the holiday:

Particulars Value

FV $ 20,000

Rate 6%

r 0.005

T 15

PMT (20,000*0.005) / (((1+0.005)^15)-1)

PMT $ 1,287.29

The monthly payment required for completing the holding fund is $1,287.29.

bi) Indicating whether investment will be purchased:

End of Year Cash Flow Rate Dis-value

0 $ (16,000.00) 1.00 $ (16,000.00)

1 $ (2,500.00) 0.87 $ (2,173.91)

2 $ - 0.76 $ -

3 $ 5,000.00 0.66 $ 3,287.58

4 $ 6,800.00 0.57 $ 3,887.92

5 $ 7,000.00 0.50 $ 3,480.24

6 $ 7,000.00 0.43 $ 3,026.29

7 $ 9,500.00 0.38 $ 3,571.40

8 $ 5,500.00 0.33 $ 1,797.96

9 $ 2,000.00 0.28 $ 568.52

Question 1:

a) Calculating the monthly amount needed to save for before the holiday:

Particulars Value

FV $ 20,000

Rate 6%

r 0.005

T 15

PMT (20,000*0.005) / (((1+0.005)^15)-1)

PMT $ 1,287.29

The monthly payment required for completing the holding fund is $1,287.29.

bi) Indicating whether investment will be purchased:

End of Year Cash Flow Rate Dis-value

0 $ (16,000.00) 1.00 $ (16,000.00)

1 $ (2,500.00) 0.87 $ (2,173.91)

2 $ - 0.76 $ -

3 $ 5,000.00 0.66 $ 3,287.58

4 $ 6,800.00 0.57 $ 3,887.92

5 $ 7,000.00 0.50 $ 3,480.24

6 $ 7,000.00 0.43 $ 3,026.29

7 $ 9,500.00 0.38 $ 3,571.40

8 $ 5,500.00 0.33 $ 1,797.96

9 $ 2,000.00 0.28 $ 568.52

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

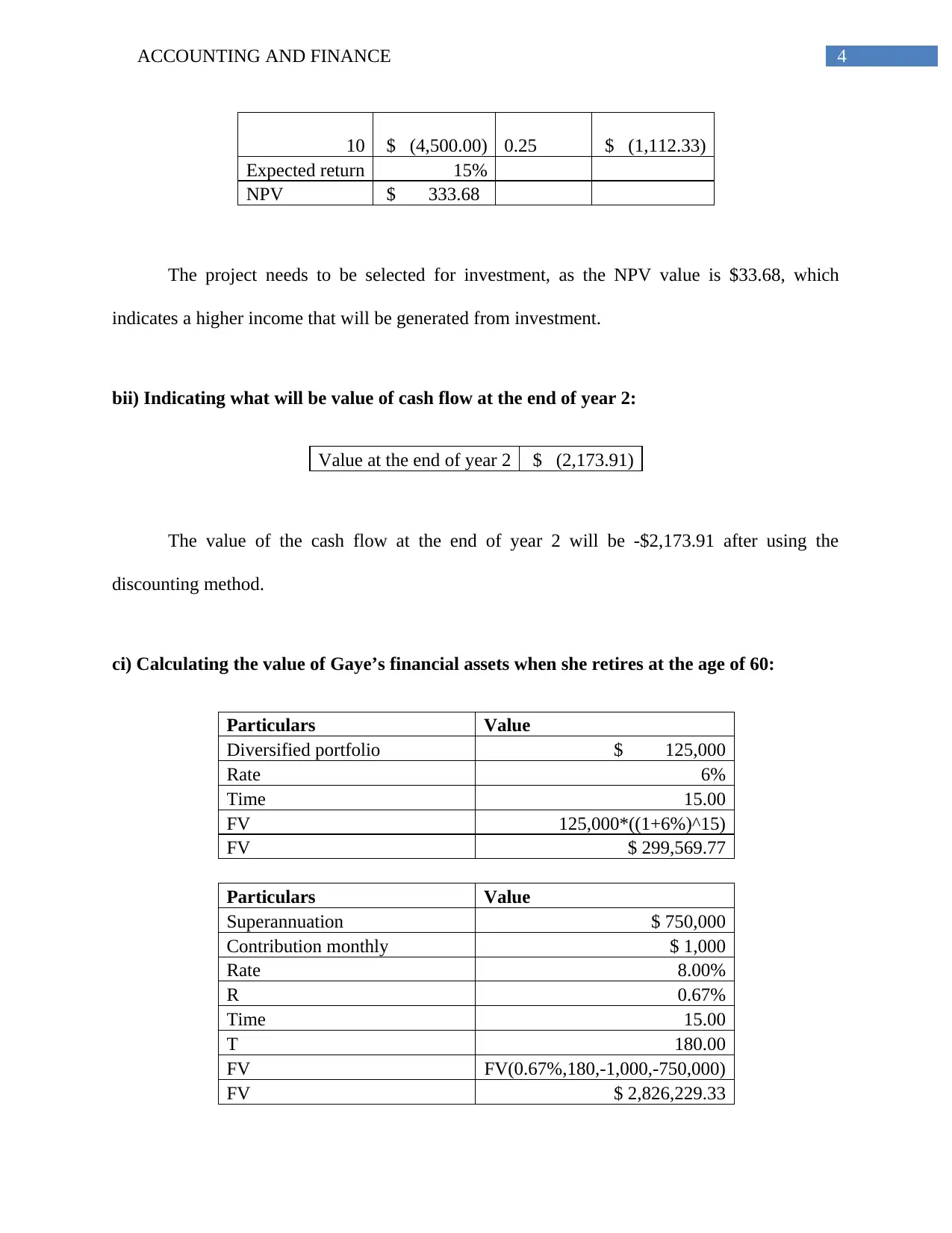

10 $ (4,500.00) 0.25 $ (1,112.33)

Expected return 15%

NPV $ 333.68

The project needs to be selected for investment, as the NPV value is $33.68, which

indicates a higher income that will be generated from investment.

bii) Indicating what will be value of cash flow at the end of year 2:

Value at the end of year 2 $ (2,173.91)

The value of the cash flow at the end of year 2 will be -$2,173.91 after using the

discounting method.

ci) Calculating the value of Gaye’s financial assets when she retires at the age of 60:

Particulars Value

Diversified portfolio $ 125,000

Rate 6%

Time 15.00

FV 125,000*((1+6%)^15)

FV $ 299,569.77

Particulars Value

Superannuation $ 750,000

Contribution monthly $ 1,000

Rate 8.00%

R 0.67%

Time 15.00

T 180.00

FV FV(0.67%,180,-1,000,-750,000)

FV $ 2,826,229.33

10 $ (4,500.00) 0.25 $ (1,112.33)

Expected return 15%

NPV $ 333.68

The project needs to be selected for investment, as the NPV value is $33.68, which

indicates a higher income that will be generated from investment.

bii) Indicating what will be value of cash flow at the end of year 2:

Value at the end of year 2 $ (2,173.91)

The value of the cash flow at the end of year 2 will be -$2,173.91 after using the

discounting method.

ci) Calculating the value of Gaye’s financial assets when she retires at the age of 60:

Particulars Value

Diversified portfolio $ 125,000

Rate 6%

Time 15.00

FV 125,000*((1+6%)^15)

FV $ 299,569.77

Particulars Value

Superannuation $ 750,000

Contribution monthly $ 1,000

Rate 8.00%

R 0.67%

Time 15.00

T 180.00

FV FV(0.67%,180,-1,000,-750,000)

FV $ 2,826,229.33

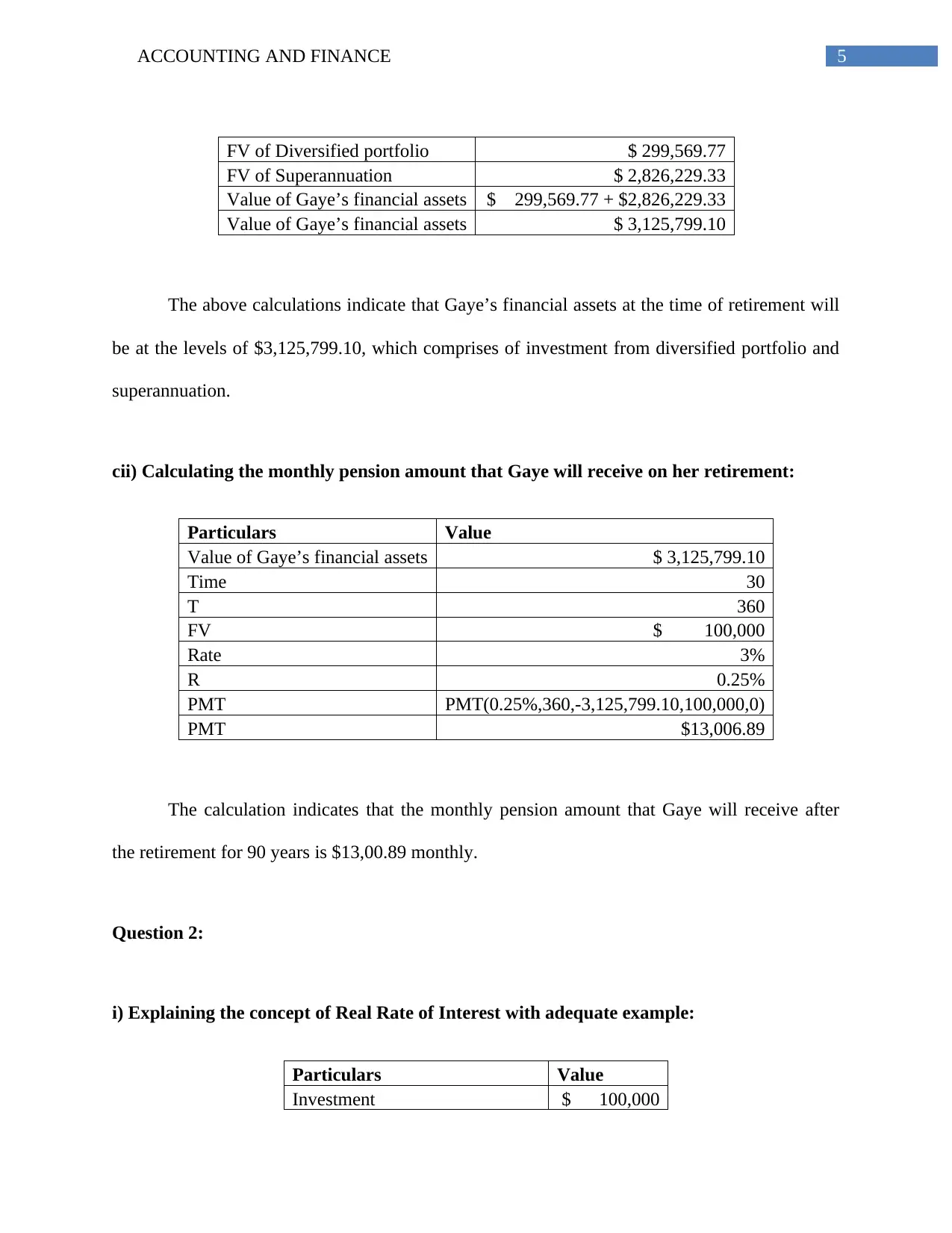

5ACCOUNTING AND FINANCE

FV of Diversified portfolio $ 299,569.77

FV of Superannuation $ 2,826,229.33

Value of Gaye’s financial assets $ 299,569.77 + $2,826,229.33

Value of Gaye’s financial assets $ 3,125,799.10

The above calculations indicate that Gaye’s financial assets at the time of retirement will

be at the levels of $3,125,799.10, which comprises of investment from diversified portfolio and

superannuation.

cii) Calculating the monthly pension amount that Gaye will receive on her retirement:

Particulars Value

Value of Gaye’s financial assets $ 3,125,799.10

Time 30

T 360

FV $ 100,000

Rate 3%

R 0.25%

PMT PMT(0.25%,360,-3,125,799.10,100,000,0)

PMT $13,006.89

The calculation indicates that the monthly pension amount that Gaye will receive after

the retirement for 90 years is $13,00.89 monthly.

Question 2:

i) Explaining the concept of Real Rate of Interest with adequate example:

Particulars Value

Investment $ 100,000

FV of Diversified portfolio $ 299,569.77

FV of Superannuation $ 2,826,229.33

Value of Gaye’s financial assets $ 299,569.77 + $2,826,229.33

Value of Gaye’s financial assets $ 3,125,799.10

The above calculations indicate that Gaye’s financial assets at the time of retirement will

be at the levels of $3,125,799.10, which comprises of investment from diversified portfolio and

superannuation.

cii) Calculating the monthly pension amount that Gaye will receive on her retirement:

Particulars Value

Value of Gaye’s financial assets $ 3,125,799.10

Time 30

T 360

FV $ 100,000

Rate 3%

R 0.25%

PMT PMT(0.25%,360,-3,125,799.10,100,000,0)

PMT $13,006.89

The calculation indicates that the monthly pension amount that Gaye will receive after

the retirement for 90 years is $13,00.89 monthly.

Question 2:

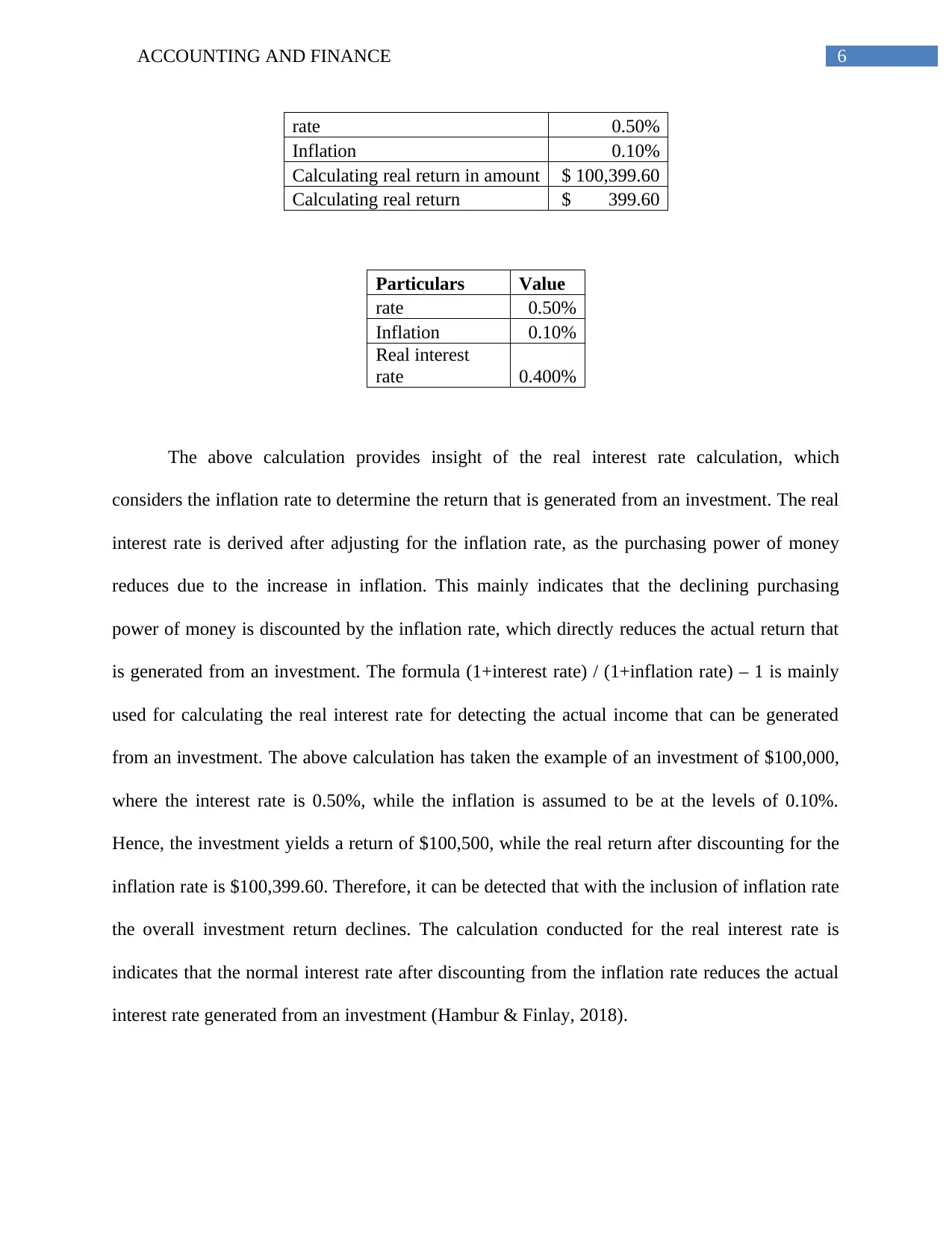

i) Explaining the concept of Real Rate of Interest with adequate example:

Particulars Value

Investment $ 100,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

rate 0.50%

Inflation 0.10%

Calculating real return in amount $ 100,399.60

Calculating real return $ 399.60

Particulars Value

rate 0.50%

Inflation 0.10%

Real interest

rate 0.400%

The above calculation provides insight of the real interest rate calculation, which

considers the inflation rate to determine the return that is generated from an investment. The real

interest rate is derived after adjusting for the inflation rate, as the purchasing power of money

reduces due to the increase in inflation. This mainly indicates that the declining purchasing

power of money is discounted by the inflation rate, which directly reduces the actual return that

is generated from an investment. The formula (1+interest rate) / (1+inflation rate) – 1 is mainly

used for calculating the real interest rate for detecting the actual income that can be generated

from an investment. The above calculation has taken the example of an investment of $100,000,

where the interest rate is 0.50%, while the inflation is assumed to be at the levels of 0.10%.

Hence, the investment yields a return of $100,500, while the real return after discounting for the

inflation rate is $100,399.60. Therefore, it can be detected that with the inclusion of inflation rate

the overall investment return declines. The calculation conducted for the real interest rate is

indicates that the normal interest rate after discounting from the inflation rate reduces the actual

interest rate generated from an investment (Hambur & Finlay, 2018).

rate 0.50%

Inflation 0.10%

Calculating real return in amount $ 100,399.60

Calculating real return $ 399.60

Particulars Value

rate 0.50%

Inflation 0.10%

Real interest

rate 0.400%

The above calculation provides insight of the real interest rate calculation, which

considers the inflation rate to determine the return that is generated from an investment. The real

interest rate is derived after adjusting for the inflation rate, as the purchasing power of money

reduces due to the increase in inflation. This mainly indicates that the declining purchasing

power of money is discounted by the inflation rate, which directly reduces the actual return that

is generated from an investment. The formula (1+interest rate) / (1+inflation rate) – 1 is mainly

used for calculating the real interest rate for detecting the actual income that can be generated

from an investment. The above calculation has taken the example of an investment of $100,000,

where the interest rate is 0.50%, while the inflation is assumed to be at the levels of 0.10%.

Hence, the investment yields a return of $100,500, while the real return after discounting for the

inflation rate is $100,399.60. Therefore, it can be detected that with the inclusion of inflation rate

the overall investment return declines. The calculation conducted for the real interest rate is

indicates that the normal interest rate after discounting from the inflation rate reduces the actual

interest rate generated from an investment (Hambur & Finlay, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

ii) Defining the negative gearing in context of Australian housing market and provide a

general evaluation of the Australian economy and society:

Negative gearing in context of Australian housing market, which indicates that the

investor takes on a debt for acquiring an income generating asset. The negative gearing asset

income is mainly less than the cost of managing the assets. The relevant cost such as interests

and depreciation are higher than the actual income generated from an investment in the housing

market. In addition, the main reason behind the investment in negative gearing is the tax benefits

that can be generated from an investment. Hence, the investment in negative gearing is

conducted for generating income from capital gains after selling the property. Thus, it is

anticipated that after the gains is higher than the actual expenses and losses incurred during the

holding period of property.

During 2016 the negative gearing investment was highlighted, as the Australian investors

were keen on increasing their income from an investment in property. In addition, the negative

gearing investment measure will benefit the wealthy and do not provide benefit to less wealthy.

Hence, the use of negative gearing investment increases the chance of speculations that can be

conducted by investors in the housing market, which in turn raises the possibility of housing

bubble. The rising housing bubble with the inflating housing prices will directly result in

manipulations that can be conducted in the Australian market. The bubble in the housing market

is not appropriate for investors, as seen in the previous financial crisis of 2008. Thus, the tax

benefit that is provided to the rich in form of negative gearing investment should not be provided

in an Australian economy (Blunden, 2016).

ii) Defining the negative gearing in context of Australian housing market and provide a

general evaluation of the Australian economy and society:

Negative gearing in context of Australian housing market, which indicates that the

investor takes on a debt for acquiring an income generating asset. The negative gearing asset

income is mainly less than the cost of managing the assets. The relevant cost such as interests

and depreciation are higher than the actual income generated from an investment in the housing

market. In addition, the main reason behind the investment in negative gearing is the tax benefits

that can be generated from an investment. Hence, the investment in negative gearing is

conducted for generating income from capital gains after selling the property. Thus, it is

anticipated that after the gains is higher than the actual expenses and losses incurred during the

holding period of property.

During 2016 the negative gearing investment was highlighted, as the Australian investors

were keen on increasing their income from an investment in property. In addition, the negative

gearing investment measure will benefit the wealthy and do not provide benefit to less wealthy.

Hence, the use of negative gearing investment increases the chance of speculations that can be

conducted by investors in the housing market, which in turn raises the possibility of housing

bubble. The rising housing bubble with the inflating housing prices will directly result in

manipulations that can be conducted in the Australian market. The bubble in the housing market

is not appropriate for investors, as seen in the previous financial crisis of 2008. Thus, the tax

benefit that is provided to the rich in form of negative gearing investment should not be provided

in an Australian economy (Blunden, 2016).

8ACCOUNTING AND FINANCE

Question 3:

i) Defining risk in terms of investment:

Risk in terms of investment is considered not bad, as the rising risk also raises the level of

returns that can be generated from an investment. In terms of investment perspective, the risk

involved with the investment is directly associated with its risk attributes. The investors for

raising the level of income choose stock that are risky, as they provide higher yield from

investment. Therefore, it can be detected that with the rising level of risk the investors are able to

generate high level of income, where relevant portfolios are prepared for minimizing the

negative impact of risk and maximizing the returns that can be generated from an investment.

Risk is an integral part of investment, as without risk investor are not able to increase the return

that can be generated from an investment (Kim & Zhang, 2016).

ii) Explaining the Australian dividend imputation credit system, where Australian resident

and international investors:

Australian dividend imputation system is a corporate tax system that allows the investors

from Australia to generate tax credits on the dividends. The dividend imputations system mainly

eliminates the tax disadvantage of the dividends to shareholders, who reduces the possibility of

double taxations and minimizes the tax expense of Australian taxpayers. The dividend

imputation system allows the international investors to minimizes the impact of double taxation,

while increasing the benefits from investment (Finsia.com, 2019).

Question 3:

i) Defining risk in terms of investment:

Risk in terms of investment is considered not bad, as the rising risk also raises the level of

returns that can be generated from an investment. In terms of investment perspective, the risk

involved with the investment is directly associated with its risk attributes. The investors for

raising the level of income choose stock that are risky, as they provide higher yield from

investment. Therefore, it can be detected that with the rising level of risk the investors are able to

generate high level of income, where relevant portfolios are prepared for minimizing the

negative impact of risk and maximizing the returns that can be generated from an investment.

Risk is an integral part of investment, as without risk investor are not able to increase the return

that can be generated from an investment (Kim & Zhang, 2016).

ii) Explaining the Australian dividend imputation credit system, where Australian resident

and international investors:

Australian dividend imputation system is a corporate tax system that allows the investors

from Australia to generate tax credits on the dividends. The dividend imputations system mainly

eliminates the tax disadvantage of the dividends to shareholders, who reduces the possibility of

double taxations and minimizes the tax expense of Australian taxpayers. The dividend

imputation system allows the international investors to minimizes the impact of double taxation,

while increasing the benefits from investment (Finsia.com, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

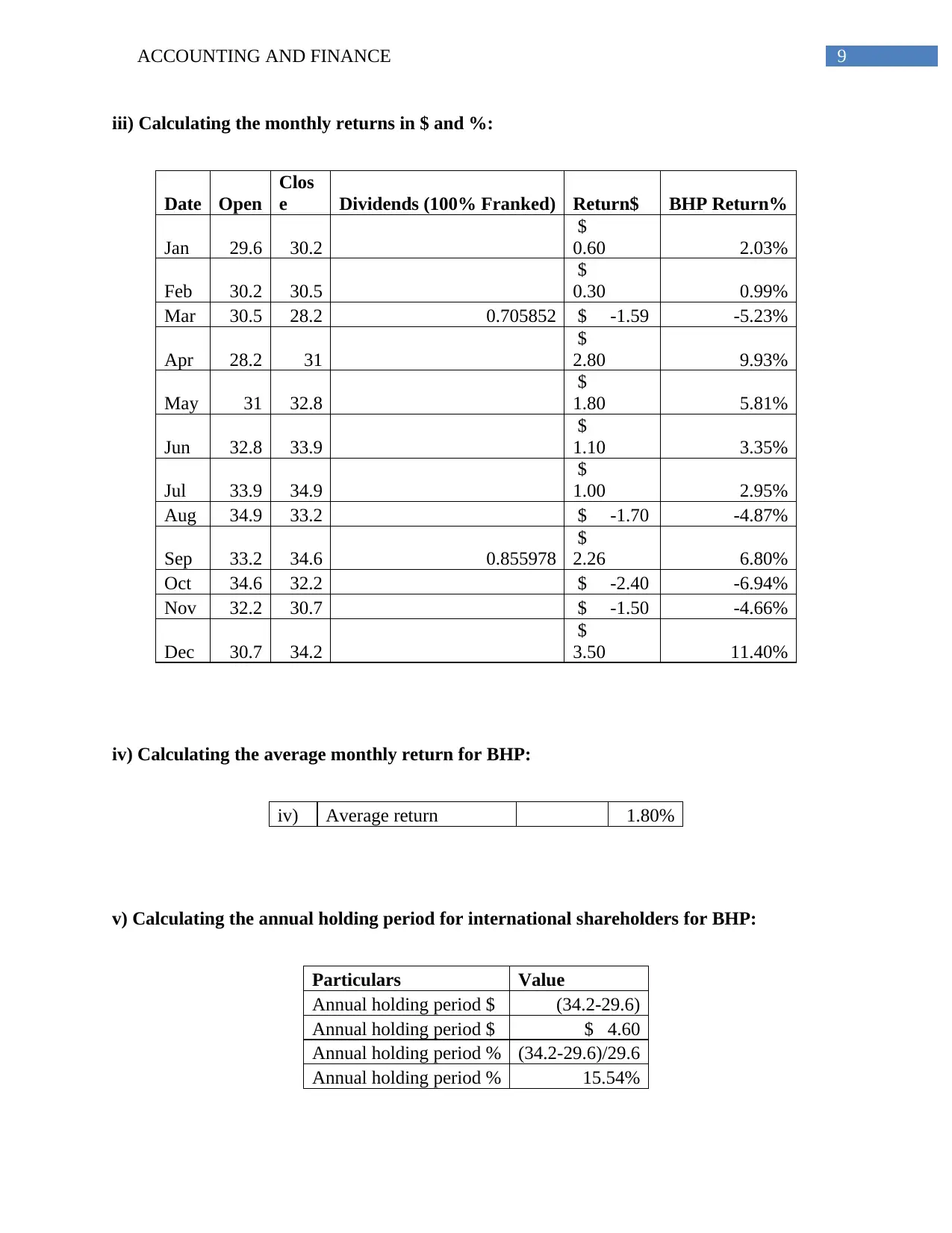

iii) Calculating the monthly returns in $ and %:

Date Open

Clos

e Dividends (100% Franked) Return$ BHP Return%

Jan 29.6 30.2

$

0.60 2.03%

Feb 30.2 30.5

$

0.30 0.99%

Mar 30.5 28.2 0.705852 $ -1.59 -5.23%

Apr 28.2 31

$

2.80 9.93%

May 31 32.8

$

1.80 5.81%

Jun 32.8 33.9

$

1.10 3.35%

Jul 33.9 34.9

$

1.00 2.95%

Aug 34.9 33.2 $ -1.70 -4.87%

Sep 33.2 34.6 0.855978

$

2.26 6.80%

Oct 34.6 32.2 $ -2.40 -6.94%

Nov 32.2 30.7 $ -1.50 -4.66%

Dec 30.7 34.2

$

3.50 11.40%

iv) Calculating the average monthly return for BHP:

iv) Average return 1.80%

v) Calculating the annual holding period for international shareholders for BHP:

Particulars Value

Annual holding period $ (34.2-29.6)

Annual holding period $ $ 4.60

Annual holding period % (34.2-29.6)/29.6

Annual holding period % 15.54%

iii) Calculating the monthly returns in $ and %:

Date Open

Clos

e Dividends (100% Franked) Return$ BHP Return%

Jan 29.6 30.2

$

0.60 2.03%

Feb 30.2 30.5

$

0.30 0.99%

Mar 30.5 28.2 0.705852 $ -1.59 -5.23%

Apr 28.2 31

$

2.80 9.93%

May 31 32.8

$

1.80 5.81%

Jun 32.8 33.9

$

1.10 3.35%

Jul 33.9 34.9

$

1.00 2.95%

Aug 34.9 33.2 $ -1.70 -4.87%

Sep 33.2 34.6 0.855978

$

2.26 6.80%

Oct 34.6 32.2 $ -2.40 -6.94%

Nov 32.2 30.7 $ -1.50 -4.66%

Dec 30.7 34.2

$

3.50 11.40%

iv) Calculating the average monthly return for BHP:

iv) Average return 1.80%

v) Calculating the annual holding period for international shareholders for BHP:

Particulars Value

Annual holding period $ (34.2-29.6)

Annual holding period $ $ 4.60

Annual holding period % (34.2-29.6)/29.6

Annual holding period % 15.54%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

vi) Calculating the annual holding period for Australian shareholders for BHP:

Particulars Value

Annual holding period $ (34.2+0.705852+0.855978-29.6)

Annual holding period $ $ 6.16

Annual holding period

% (6.16)/29.6

Annual holding period

% 20.82%

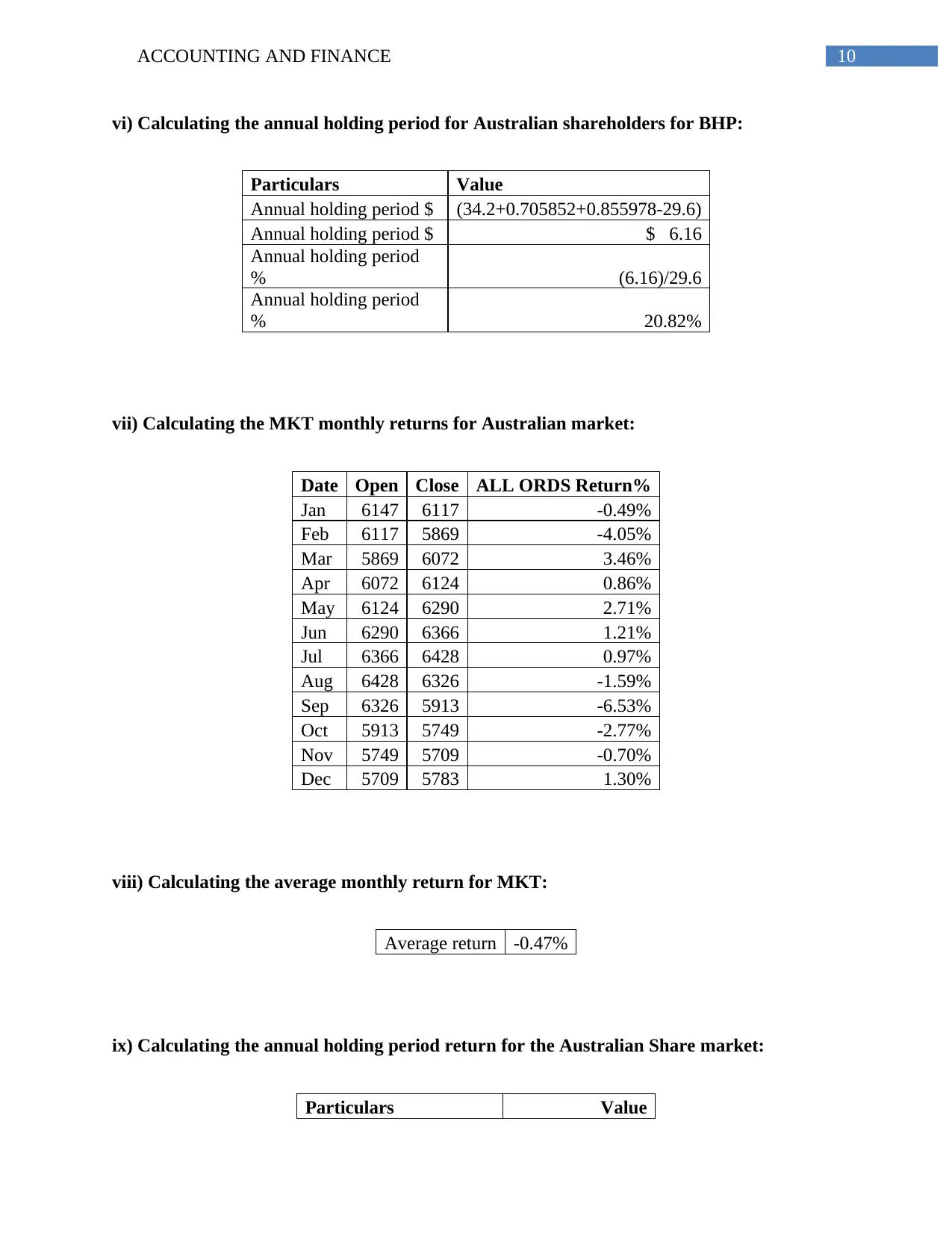

vii) Calculating the MKT monthly returns for Australian market:

Date Open Close ALL ORDS Return%

Jan 6147 6117 -0.49%

Feb 6117 5869 -4.05%

Mar 5869 6072 3.46%

Apr 6072 6124 0.86%

May 6124 6290 2.71%

Jun 6290 6366 1.21%

Jul 6366 6428 0.97%

Aug 6428 6326 -1.59%

Sep 6326 5913 -6.53%

Oct 5913 5749 -2.77%

Nov 5749 5709 -0.70%

Dec 5709 5783 1.30%

viii) Calculating the average monthly return for MKT:

Average return -0.47%

ix) Calculating the annual holding period return for the Australian Share market:

Particulars Value

vi) Calculating the annual holding period for Australian shareholders for BHP:

Particulars Value

Annual holding period $ (34.2+0.705852+0.855978-29.6)

Annual holding period $ $ 6.16

Annual holding period

% (6.16)/29.6

Annual holding period

% 20.82%

vii) Calculating the MKT monthly returns for Australian market:

Date Open Close ALL ORDS Return%

Jan 6147 6117 -0.49%

Feb 6117 5869 -4.05%

Mar 5869 6072 3.46%

Apr 6072 6124 0.86%

May 6124 6290 2.71%

Jun 6290 6366 1.21%

Jul 6366 6428 0.97%

Aug 6428 6326 -1.59%

Sep 6326 5913 -6.53%

Oct 5913 5749 -2.77%

Nov 5749 5709 -0.70%

Dec 5709 5783 1.30%

viii) Calculating the average monthly return for MKT:

Average return -0.47%

ix) Calculating the annual holding period return for the Australian Share market:

Particulars Value

11ACCOUNTING AND FINANCE

Annual holding period % (5783-6147)/6147

Annual holding period % -5.92%

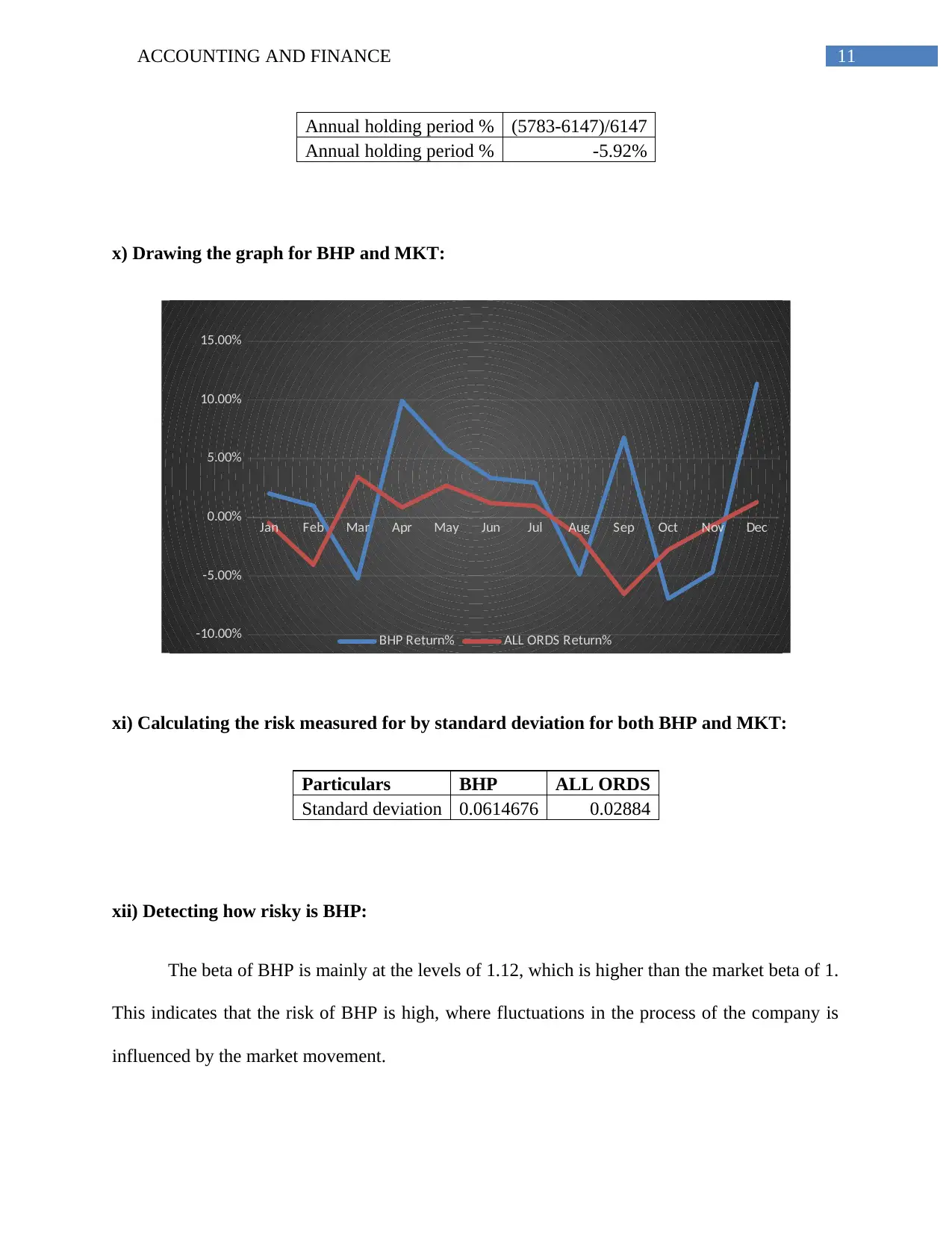

x) Drawing the graph for BHP and MKT:

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

BHP Return% ALL ORDS Return%

xi) Calculating the risk measured for by standard deviation for both BHP and MKT:

Particulars BHP ALL ORDS

Standard deviation 0.0614676 0.02884

xii) Detecting how risky is BHP:

The beta of BHP is mainly at the levels of 1.12, which is higher than the market beta of 1.

This indicates that the risk of BHP is high, where fluctuations in the process of the company is

influenced by the market movement.

Annual holding period % (5783-6147)/6147

Annual holding period % -5.92%

x) Drawing the graph for BHP and MKT:

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

BHP Return% ALL ORDS Return%

xi) Calculating the risk measured for by standard deviation for both BHP and MKT:

Particulars BHP ALL ORDS

Standard deviation 0.0614676 0.02884

xii) Detecting how risky is BHP:

The beta of BHP is mainly at the levels of 1.12, which is higher than the market beta of 1.

This indicates that the risk of BHP is high, where fluctuations in the process of the company is

influenced by the market movement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.