ACC518: Current Developments in Accounting Thoughts Analysis

VerifiedAdded on 2022/11/24

|28

|3823

|291

Homework Assignment

AI Summary

This assignment analyzes current developments in accounting, focusing on two key questions. The first question examines a news article concerning Pioneer Credit Ltd's accounting practices, specifically their use of fair value accounting for debt portfolios, which led to disputes with the Australian Securities and Investment Commission (ASIC). The analysis connects these issues to accounting theories, particularly the stakeholder theory, emphasizing the importance of considering all stakeholders' interests. The second question analyzes an exposure draft related to IAS 37 Provisions, Contingent Liabilities and Contingent Assets, specifically focusing on onerous contracts. It evaluates comments from four respondents regarding the proposed amendments, including the costs of fulfilling a contract, and assesses whether their views align with the draft's recommendations. The report provides a critical evaluation of the theories included in the exposure draft, focusing on consistency in accounting standards.

Running head: CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Current Developments in Accounting Thoughts

Name of the Student:

Name of the Student:

Author’s Note

Current Developments in Accounting Thoughts

Name of the Student:

Name of the Student:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Table of Contents

Answer to Question 1................................................................................................................1

Answer to Question 2:...............................................................................................................6

Executive Summary...............................................................................................................7

Introduction:..........................................................................................................................7

Proposal:................................................................................................................................8

Comments to the proposed amendment................................................................................8

Conclusion...............................................................................................................................21

Reference.................................................................................................................................23

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Table of Contents

Answer to Question 1................................................................................................................1

Answer to Question 2:...............................................................................................................6

Executive Summary...............................................................................................................7

Introduction:..........................................................................................................................7

Proposal:................................................................................................................................8

Comments to the proposed amendment................................................................................8

Conclusion...............................................................................................................................21

Reference.................................................................................................................................23

2

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Answer to Question 1

The article which is chosen for this part of the assignment deals with the accounting system

which is followed by Pioneer Ltd for the purpose of accounting information of the business. This

specific article has been obtained from the Financial Review and it has been published on 3rd

April 2019. The article provides adequate information related to the wrong accounting process

which is followed by Pioneer Ltd which operates in Australia ("About us", 2019a). The article

further shows that the issues which the company faces due to its controversial accounting policy

and how the auditors and ASIC dealt with the situation.

Pioneer Credit Ltd is an Australian based company which provides financial services to

residents of Australia and New Zealand. The company follows an approach for providing the

best services to the clients and thereby is known for the services which is provided by the

business (Pioneer Credit Limited, 2018). The report deals with the controversial accounting

practices which was followed by the management of the company for showing the assets of the

business ("About the AASB", 2019). The policy which was followed by the business was not as

per the accounting standards nor the same was consistent with the conceptual framework which

is followed by most of the companies globally. As per the article which is available, the Perth

based business has followed unorthodox accounting treatment for measuring the financial assets

of the business which is not followed in generally accepted accounting framework. This

adversely affects the principle of understandability of the financial statements of the business

(ASIC, 2013). The article further shows that the accounting policy which is followed by the

business is not approved by the auditor of the business

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Answer to Question 1

The article which is chosen for this part of the assignment deals with the accounting system

which is followed by Pioneer Ltd for the purpose of accounting information of the business. This

specific article has been obtained from the Financial Review and it has been published on 3rd

April 2019. The article provides adequate information related to the wrong accounting process

which is followed by Pioneer Ltd which operates in Australia ("About us", 2019a). The article

further shows that the issues which the company faces due to its controversial accounting policy

and how the auditors and ASIC dealt with the situation.

Pioneer Credit Ltd is an Australian based company which provides financial services to

residents of Australia and New Zealand. The company follows an approach for providing the

best services to the clients and thereby is known for the services which is provided by the

business (Pioneer Credit Limited, 2018). The report deals with the controversial accounting

practices which was followed by the management of the company for showing the assets of the

business ("About the AASB", 2019). The policy which was followed by the business was not as

per the accounting standards nor the same was consistent with the conceptual framework which

is followed by most of the companies globally. As per the article which is available, the Perth

based business has followed unorthodox accounting treatment for measuring the financial assets

of the business which is not followed in generally accepted accounting framework. This

adversely affects the principle of understandability of the financial statements of the business

(ASIC, 2013). The article further shows that the accounting policy which is followed by the

business is not approved by the auditor of the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

The accounting policies and treatments which is made by the management of the company in

the financial statement of the business has attracted the attention of Australia Stock Exchange

(ASX) and also its auditor. The ASIC has been following the corporate reporting framework

which is applied by the business since November 2017 as per the article which is considered.

The corporate regulator contacted the company recently for expressing the concerns of the board

regarding thee accounting policies which is followed by the company and how the same impacts

the consistency principle which is followed in the process of accounting ("About ASIC", 2019).

The management of Pioneer Credit ltd however, disclosed that the business would not be making

any changes in the valuation methods which is followed for assets in the annual report. This

resulted in a direct conflict of the business with the corporate regulators operating in the country.

The ASIC has confronted a whistle blower from the company in order to get more information

regarding the accounting policy which is followed by the business (Frost, 2019a). The

management of the Pioneer Credit ltd needs to make changes in the valuation policies so that the

same are as per the requirement of accounting regulations and standards which are closely

followed in Australia

The business of Pioneer Credit ltd mainly operates on purchasing impaired books of retail

credit and utilities often in cents in the dollar and then effectively works with the debtors for

collecting outstanding debts. The company in such cases values the debt portfolios which are

essential income generating sources for the business at fair value or the price agreed between

buyer and seller rather than amortised cost. As per amortised cost method, the value of the asset

is written down over time. The policies of the business have been highlighted by the auditor

PwC which stated that the auditor was not able to collect sufficient and appropriate information

for the purpose if determining whether the financial statements represented in the annual is

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

The accounting policies and treatments which is made by the management of the company in

the financial statement of the business has attracted the attention of Australia Stock Exchange

(ASX) and also its auditor. The ASIC has been following the corporate reporting framework

which is applied by the business since November 2017 as per the article which is considered.

The corporate regulator contacted the company recently for expressing the concerns of the board

regarding thee accounting policies which is followed by the company and how the same impacts

the consistency principle which is followed in the process of accounting ("About ASIC", 2019).

The management of Pioneer Credit ltd however, disclosed that the business would not be making

any changes in the valuation methods which is followed for assets in the annual report. This

resulted in a direct conflict of the business with the corporate regulators operating in the country.

The ASIC has confronted a whistle blower from the company in order to get more information

regarding the accounting policy which is followed by the business (Frost, 2019a). The

management of the Pioneer Credit ltd needs to make changes in the valuation policies so that the

same are as per the requirement of accounting regulations and standards which are closely

followed in Australia

The business of Pioneer Credit ltd mainly operates on purchasing impaired books of retail

credit and utilities often in cents in the dollar and then effectively works with the debtors for

collecting outstanding debts. The company in such cases values the debt portfolios which are

essential income generating sources for the business at fair value or the price agreed between

buyer and seller rather than amortised cost. As per amortised cost method, the value of the asset

is written down over time. The policies of the business have been highlighted by the auditor

PwC which stated that the auditor was not able to collect sufficient and appropriate information

for the purpose if determining whether the financial statements represented in the annual is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

appropriate or not. This resulted in a qualified opinion which was provided by the auditor of the

business (Henderson et al, 2014). The article clearly shows that the business follows fair value

approach for valuing the assets which actually should be valued at amortised costs and this has

lead to a dispute case between ASIC and the company. The company has also made it clear that

it has no intention of revising the accounting policy thereby making things more difficult.

The main outcome of the auditor’s report and the dispute which the company is facing with

the corporate regulators has resulted the business to lose tremendously in terms of market share

in the stock exchange. The share price of the company has rapidly declined and most of the

investors of the business has opted short position while considering the condition of the business.

As per the article which is considered, the company has lost 46% of its values in just 12 months.

This shows the overall decline which the company has faced over the period and has lost

significant revenue generation source (IFRS, 2018a). The management of the company needs to

appropriate represent the financial statement which is to be followed so that appropriate

disclosures are provided and a level of simplicity can be maintained in the organization.

The article effectively shows that the management of Pioneer ltd follows in appropriate

accounting valuation of the assets at fair value when the same is actually supposed to be at

amortised cost. This policy adversely affects the consistency of the financial reporting process

and in a way hampers the presentability of the reporting framework which the business follows.

As per the provisions which is stated in para 15 of AASB 101, Financial statements needs to be

presented fairly depicting the financial position, financial performance and cash flows of an

entity ("About the AASB", 2019). In other words, fair representation means accurate disclosures

and figured needs to be stated in the financial statement of the business in order to ensure that the

users of the financial statement get an accurate presentation of the financial position of the

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

appropriate or not. This resulted in a qualified opinion which was provided by the auditor of the

business (Henderson et al, 2014). The article clearly shows that the business follows fair value

approach for valuing the assets which actually should be valued at amortised costs and this has

lead to a dispute case between ASIC and the company. The company has also made it clear that

it has no intention of revising the accounting policy thereby making things more difficult.

The main outcome of the auditor’s report and the dispute which the company is facing with

the corporate regulators has resulted the business to lose tremendously in terms of market share

in the stock exchange. The share price of the company has rapidly declined and most of the

investors of the business has opted short position while considering the condition of the business.

As per the article which is considered, the company has lost 46% of its values in just 12 months.

This shows the overall decline which the company has faced over the period and has lost

significant revenue generation source (IFRS, 2018a). The management of the company needs to

appropriate represent the financial statement which is to be followed so that appropriate

disclosures are provided and a level of simplicity can be maintained in the organization.

The article effectively shows that the management of Pioneer ltd follows in appropriate

accounting valuation of the assets at fair value when the same is actually supposed to be at

amortised cost. This policy adversely affects the consistency of the financial reporting process

and in a way hampers the presentability of the reporting framework which the business follows.

As per the provisions which is stated in para 15 of AASB 101, Financial statements needs to be

presented fairly depicting the financial position, financial performance and cash flows of an

entity ("About the AASB", 2019). In other words, fair representation means accurate disclosures

and figured needs to be stated in the financial statement of the business in order to ensure that the

users of the financial statement get an accurate presentation of the financial position of the

5

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

business ("Who we are", 2019d). The article shows that ASIC is also involved with the dispute

which surrounds the wrong treatment of assets which are not valued appropriately. In such a

situation, the ASIC would be enforcing action in order to ensure that reporting framework which

is followed by the business is appropriate. The information which are presented are considered

by the users of the financial statements and it is to be noted that important investment decisions

are taken by the users on the basis of the information which is presented in the annual reports.

The fair value measurement policy of the business would affect the financial statements and will

be disclosing different values which can mislead the users. Therefore, a level of consistency

needs to be maintained in the reporting framework which is followed by the business.

In this case, the stakeholder theory can be applied as employee and staff members are also

considered to be stakeholders of the business. As per the stakeholder’s theory any group of

people who are affected by the activities of the business are considered to be stakeholders of the

company. Therefore, the management of the company needs to take appropriate consideration

regarding the same while taking important decisions related to business activities. The

stakeholder theory is very important in this global world as businesses should not just consider

the interest of the shareholders of the business but also the interest of the other stakeholders of

the business. The companies needs to treat the stakeholders equally and should take decisions

after considering the best interest of all. The case which is presented in the article shows that

Pioneer credit ltd has followed inappropriate accounting policies for reporting the assts related to

debt portfolio of the business ("Leadership Principles", 2019b). The information which is

presented in not appropriate and it would confuse the shareholders of the business. In addition to

this, the management of the company would also need to consider the interest of the clients and

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

business ("Who we are", 2019d). The article shows that ASIC is also involved with the dispute

which surrounds the wrong treatment of assets which are not valued appropriately. In such a

situation, the ASIC would be enforcing action in order to ensure that reporting framework which

is followed by the business is appropriate. The information which are presented are considered

by the users of the financial statements and it is to be noted that important investment decisions

are taken by the users on the basis of the information which is presented in the annual reports.

The fair value measurement policy of the business would affect the financial statements and will

be disclosing different values which can mislead the users. Therefore, a level of consistency

needs to be maintained in the reporting framework which is followed by the business.

In this case, the stakeholder theory can be applied as employee and staff members are also

considered to be stakeholders of the business. As per the stakeholder’s theory any group of

people who are affected by the activities of the business are considered to be stakeholders of the

company. Therefore, the management of the company needs to take appropriate consideration

regarding the same while taking important decisions related to business activities. The

stakeholder theory is very important in this global world as businesses should not just consider

the interest of the shareholders of the business but also the interest of the other stakeholders of

the business. The companies needs to treat the stakeholders equally and should take decisions

after considering the best interest of all. The case which is presented in the article shows that

Pioneer credit ltd has followed inappropriate accounting policies for reporting the assts related to

debt portfolio of the business ("Leadership Principles", 2019b). The information which is

presented in not appropriate and it would confuse the shareholders of the business. In addition to

this, the management of the company would also need to consider the interest of the clients and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

also the regulating bodies as the same also come under the definition of a stakeholder of a

business.

Therefore, after analysing the article which is presented in this case, it can be said that if

the required amendment is made by the business of Pioneer credit ltd than it would bring about

consistency and transparency in the accounting treatments which is followed in the business. The

analysis further reveals that in case the company does not make the necessary changes in the

reporting framework which is followed, legal charges and even dissolution of the business can

also take place depending on the decision which is taken by ASIC. In addition to this, the

implementation process also satisfies the stakeholder theory as clients are also considered to be

one of the stakeholders of the business and therefore the interest of the same should also be

considered for taking major decisions of the business.

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

also the regulating bodies as the same also come under the definition of a stakeholder of a

business.

Therefore, after analysing the article which is presented in this case, it can be said that if

the required amendment is made by the business of Pioneer credit ltd than it would bring about

consistency and transparency in the accounting treatments which is followed in the business. The

analysis further reveals that in case the company does not make the necessary changes in the

reporting framework which is followed, legal charges and even dissolution of the business can

also take place depending on the decision which is taken by ASIC. In addition to this, the

implementation process also satisfies the stakeholder theory as clients are also considered to be

one of the stakeholders of the business and therefore the interest of the same should also be

considered for taking major decisions of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Answer to Question 2:

Executive Summary

This report is prepared to show the critical analysis of recent changes which have been

made in accounting practices and standards. The report would be focusing on the amendments

which are made on exposure draft. The assessment would be focusing on the important

amendments which are made in the standards IAS 37 Provisions, Contingent Liabilities and

Contingent Assets (AASB, 2014). There are four respondents, which have been taken into

account to provide comments on the exposure draft so their arguments can be analysed. The

exposure draft is concerned with situation which arises in case of an onerous contract and how

the costs of the contract and how the cost of the contract is to be treated in the accounting records

of the business.

Introduction:

The main criteria for this part is to analyse the exposure draft which is issued by International

Accounting Standard Board (IASB) for consideration to the public regarding the appropriateness

of the reporting framework of the business. The exposure draft which is considered is open for

the comments of the respondents so as to ensure that the same are satisfied with the amendments

suggested. The exposure draft which is considered in the assessment would be about

amendments which can be brought about in IAS 37 Provisions, Contingent Liabilities and

Contingent Assets ("Onerous Contracts- IAS 37", IFRS, 2019a). The assessment goes into detail

about Onerous Contracts—Cost of Fulfilling a contract. The assessment would be pointing out

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Answer to Question 2:

Executive Summary

This report is prepared to show the critical analysis of recent changes which have been

made in accounting practices and standards. The report would be focusing on the amendments

which are made on exposure draft. The assessment would be focusing on the important

amendments which are made in the standards IAS 37 Provisions, Contingent Liabilities and

Contingent Assets (AASB, 2014). There are four respondents, which have been taken into

account to provide comments on the exposure draft so their arguments can be analysed. The

exposure draft is concerned with situation which arises in case of an onerous contract and how

the costs of the contract and how the cost of the contract is to be treated in the accounting records

of the business.

Introduction:

The main criteria for this part is to analyse the exposure draft which is issued by International

Accounting Standard Board (IASB) for consideration to the public regarding the appropriateness

of the reporting framework of the business. The exposure draft which is considered is open for

the comments of the respondents so as to ensure that the same are satisfied with the amendments

suggested. The exposure draft which is considered in the assessment would be about

amendments which can be brought about in IAS 37 Provisions, Contingent Liabilities and

Contingent Assets ("Onerous Contracts- IAS 37", IFRS, 2019a). The assessment goes into detail

about Onerous Contracts—Cost of Fulfilling a contract. The assessment would be pointing out

8

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

whether the views of the respondents and whether the same are for or against the

recommendations which is provided in the exposure draft. This part would also be providing a

critical evaluation of the theories which are included in the exposure draft

Proposal:

The provisions which are covered under IAS 37 effectively discusses that an onerous

contract as a contract in which the unavoidable costs of meeting the obligations under the

contract exceed the economic benefits expected to be received under it. IAS 37 also states that

the unavoidable costs under a contract portrays the least net cost of exiting from the contract,

which is the lower of the cost of performing the contract and any payment which is result of

penalty arising from the non-performance of the contract. The accounting standard does not

specify the costs which is required for fulfilling a contract of a business (Deegan, 2014). The

main concern in such a section is in terms of the contracts which are related to construction. The

main issues which arouse was identification of the costs in IAS 37. The IFRS recognised that

there cost treatment process was different for different businesses and therefore a clarification

was required in respect to such costs.

In order to bring about and maintain consistency in the accounting process which is

followed in different countries, alteration is required to be made in the measurement and

treatment of the costs which are associated with such kinds of onerous contracts. The

modification which is made by the committee incorporates appropriate definition of the onerous

contracts and also methods which can be adopted by the business for measuring the costs of

fulfilling the contracts of the business.

Comments to the proposed amendment

Comment of BDO Network

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

whether the views of the respondents and whether the same are for or against the

recommendations which is provided in the exposure draft. This part would also be providing a

critical evaluation of the theories which are included in the exposure draft

Proposal:

The provisions which are covered under IAS 37 effectively discusses that an onerous

contract as a contract in which the unavoidable costs of meeting the obligations under the

contract exceed the economic benefits expected to be received under it. IAS 37 also states that

the unavoidable costs under a contract portrays the least net cost of exiting from the contract,

which is the lower of the cost of performing the contract and any payment which is result of

penalty arising from the non-performance of the contract. The accounting standard does not

specify the costs which is required for fulfilling a contract of a business (Deegan, 2014). The

main concern in such a section is in terms of the contracts which are related to construction. The

main issues which arouse was identification of the costs in IAS 37. The IFRS recognised that

there cost treatment process was different for different businesses and therefore a clarification

was required in respect to such costs.

In order to bring about and maintain consistency in the accounting process which is

followed in different countries, alteration is required to be made in the measurement and

treatment of the costs which are associated with such kinds of onerous contracts. The

modification which is made by the committee incorporates appropriate definition of the onerous

contracts and also methods which can be adopted by the business for measuring the costs of

fulfilling the contracts of the business.

Comments to the proposed amendment

Comment of BDO Network

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

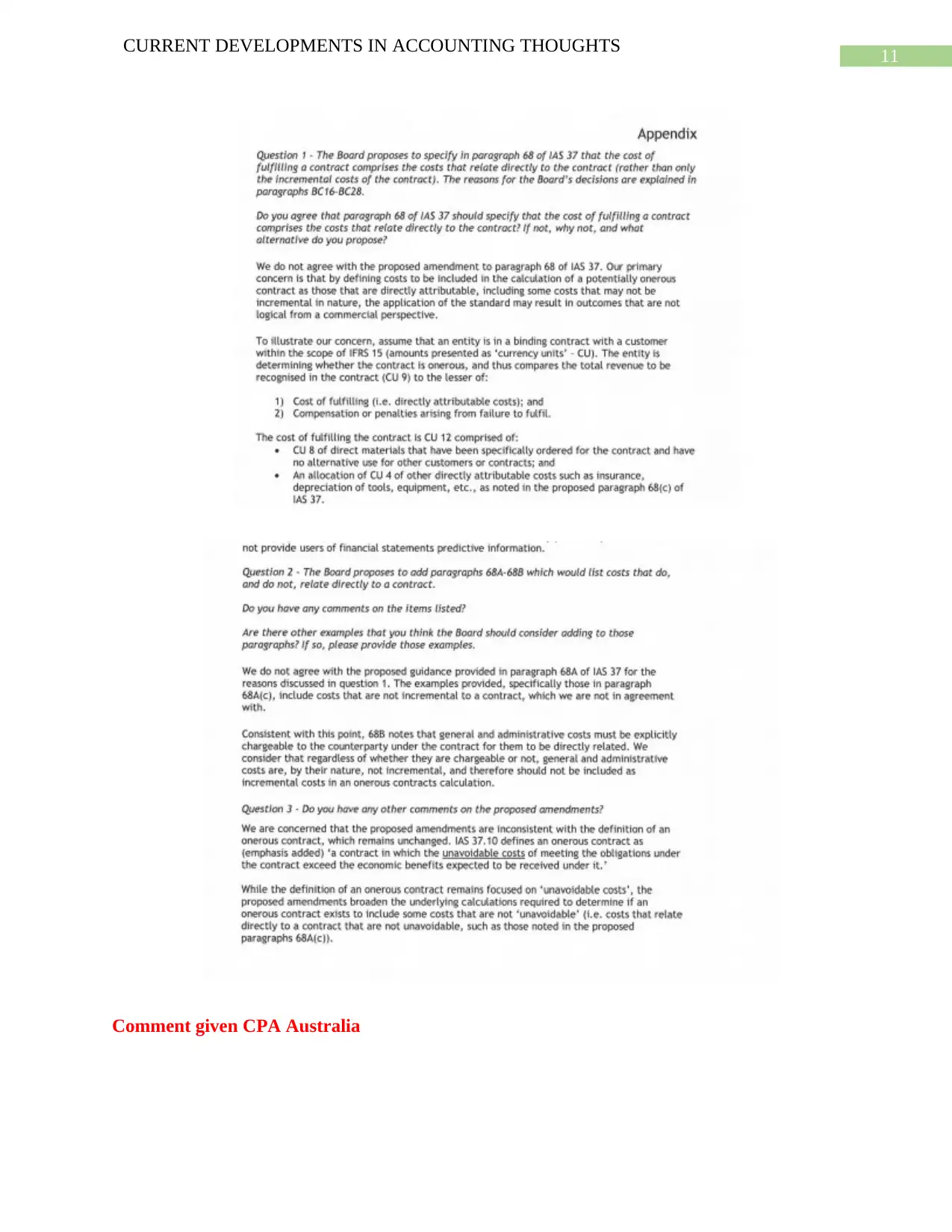

In the amendment which is suggested by the IASB, BDO network has made a comment

and is not satisfied with the changes that is being suggested by the IASB. The reasons which can

be provided for such an agreement are listed below in details:

The amendment which is proposed by IASB is not relevant and logical as those which are

directly attributable to the costs of the contract must be included in the estimation of

costs. It is also to be noted that some costs are incremental in nature.

The onerous contract provision represents only non-incremental costs to be incurred in

the future at the discretion of the which is inconsistent with Para 63 IAS 37. Therefore,

the amendment which is made is not considering the operating losses which can be

incurred by the business in future period (Buchanan, 2019). The provisions of

recognising the costs related to fulfilling the obligations of the contract and inclusion of

the same is not realistic from commercial point of view and therefore not appropriate.

The proposed amendments are inconsistent with the definition of an onerous contract,

which remains unchanged (Hoogervorst & Prada, 2015). The definition deals with

unavoidable costs while the amendment which is suggested by the board required

detailed computation of cists which are not unavoidable in nature.

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

In the amendment which is suggested by the IASB, BDO network has made a comment

and is not satisfied with the changes that is being suggested by the IASB. The reasons which can

be provided for such an agreement are listed below in details:

The amendment which is proposed by IASB is not relevant and logical as those which are

directly attributable to the costs of the contract must be included in the estimation of

costs. It is also to be noted that some costs are incremental in nature.

The onerous contract provision represents only non-incremental costs to be incurred in

the future at the discretion of the which is inconsistent with Para 63 IAS 37. Therefore,

the amendment which is made is not considering the operating losses which can be

incurred by the business in future period (Buchanan, 2019). The provisions of

recognising the costs related to fulfilling the obligations of the contract and inclusion of

the same is not realistic from commercial point of view and therefore not appropriate.

The proposed amendments are inconsistent with the definition of an onerous contract,

which remains unchanged (Hoogervorst & Prada, 2015). The definition deals with

unavoidable costs while the amendment which is suggested by the board required

detailed computation of cists which are not unavoidable in nature.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

11

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Comment given CPA Australia

CURRENT DEVELOPMENTS IN ACCOUNTING THOUGHTS

Comment given CPA Australia

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.