ACC5202 Accounting Assignment: Trial Balance and Error Correction

VerifiedAdded on 2023/06/13

|25

|5001

|146

Homework Assignment

AI Summary

This document provides a comprehensive solution to an accounting assignment, addressing key concepts such as trial balance analysis, error correction, and financial statement preparation. It includes detailed explanations of accounting principles, such as the matching concept and the conceptual framework, with examples of enhancing qualities of financial statements. The assignment covers practical tasks like identifying and rectifying errors in a trial balance, adjusting profit figures based on accounting principles, and preparing journal entries. It includes a thorough examination of accounts receivable management, the impact of credit cards on financial risk, and the importance of providing for bad debts. The solution offers a detailed step-by-step guide to solving accounting problems, making it a valuable resource for students. Desklib provides a platform to explore more solved assignments and past papers.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING

Table of Contents

Question 1........................................................................................................................................3

Requirement A.............................................................................................................................3

Requirement B.............................................................................................................................4

Question 2........................................................................................................................................4

Requirement A.............................................................................................................................4

Requirement B.............................................................................................................................5

Question 3........................................................................................................................................7

Requirement A.............................................................................................................................7

Requirement B.............................................................................................................................8

Question 4......................................................................................................................................10

Requirement A...........................................................................................................................10

Requirement B...........................................................................................................................11

Question 5......................................................................................................................................15

Requirement A...........................................................................................................................15

Requirement B – Journal Entries...............................................................................................18

Journal Entries...........................................................................................................................19

Question 6......................................................................................................................................20

Requirement A...........................................................................................................................20

Requirement B...........................................................................................................................23

ACCOUNTING

Table of Contents

Question 1........................................................................................................................................3

Requirement A.............................................................................................................................3

Requirement B.............................................................................................................................4

Question 2........................................................................................................................................4

Requirement A.............................................................................................................................4

Requirement B.............................................................................................................................5

Question 3........................................................................................................................................7

Requirement A.............................................................................................................................7

Requirement B.............................................................................................................................8

Question 4......................................................................................................................................10

Requirement A...........................................................................................................................10

Requirement B...........................................................................................................................11

Question 5......................................................................................................................................15

Requirement A...........................................................................................................................15

Requirement B – Journal Entries...............................................................................................18

Journal Entries...........................................................................................................................19

Question 6......................................................................................................................................20

Requirement A...........................................................................................................................20

Requirement B...........................................................................................................................23

2

ACCOUNTING

Reference.......................................................................................................................................24

ACCOUNTING

Reference.......................................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING

Question 1

Requirement A

A trial balance is a statement which is prepared with taking the closing balance of the

different ledger accounts where the debit total balance matches the credit total balance. In simple

words, a trial balance uses closing balance of different ledger accounts which have debit or credit

balances and the statement tallies. If the statement does not tally then there may be certain errors

in the statement. The main use of a trial balance is to check the mathematical accuracy of the

transactions as recorded in the ledger accounts. Every business prepares a trial balance

periodically to ensure that the books of accounts which are made following double entry system

are free from errors which may be due to calculations. This is possible because under double

entry system, the total of debit side will always be equal to the total of credit side. This the

principle which is followed by a trial balance (Needles, Powers and Crosson 2013).

If the trial matches it only means that the mathematical accuracy is there but it does not

mean that their may not be any accounting errors. The matching of trial balance only shows that

there are no calculation errors but there still maty be material errors present in the books of

accounts. For example, an error of omission of an entry will not be identifiable as the trial

balance will match. Another example which can be given is that of bookkeeping error which

means that equal debit and credit been entered into wrong accounts. In this case also, the trial

balance will match but still there is an error in the financial statements.

ACCOUNTING

Question 1

Requirement A

A trial balance is a statement which is prepared with taking the closing balance of the

different ledger accounts where the debit total balance matches the credit total balance. In simple

words, a trial balance uses closing balance of different ledger accounts which have debit or credit

balances and the statement tallies. If the statement does not tally then there may be certain errors

in the statement. The main use of a trial balance is to check the mathematical accuracy of the

transactions as recorded in the ledger accounts. Every business prepares a trial balance

periodically to ensure that the books of accounts which are made following double entry system

are free from errors which may be due to calculations. This is possible because under double

entry system, the total of debit side will always be equal to the total of credit side. This the

principle which is followed by a trial balance (Needles, Powers and Crosson 2013).

If the trial matches it only means that the mathematical accuracy is there but it does not

mean that their may not be any accounting errors. The matching of trial balance only shows that

there are no calculation errors but there still maty be material errors present in the books of

accounts. For example, an error of omission of an entry will not be identifiable as the trial

balance will match. Another example which can be given is that of bookkeeping error which

means that equal debit and credit been entered into wrong accounts. In this case also, the trial

balance will match but still there is an error in the financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING

Requirement B

Yes No Debit Credit

1. The Accrued Wages account with a

balance of $500 was omitted from the

Trial Balance

Yes Accrued Wages Accrued Wages of $500 should be

paosted in the credit side of trial

balance 500

2. A payment of $490 for Prepaid Rent was

only posted to the Cash at Bank account

and not to Prepaid Rent

Yes Prepaid Rent Debit side of Prepaid Rent should be

increased by $490

490

3. A debit of $458 to Cash at Bank was

posted as $485. The credit entry was

correct.

Yes Cash at Bank Debit Side of Cash at Bank should be

reduced by ($485 - $458) $27

-27

4. A credit of $600 to Accounts Payable

should have been made to Fees Revenue

No Accounts

Payable, Fees

Revenue

Accounts Payable should be debited

and Fees Revenue should be credited

by $600

5. A Dr. for a cash receipt of $500 from

customers in settlement their accounts

was posted twice as a Dr. to the Cash at

Bank and a Dr. to Accounts Receivable

accounts

Yes Cash at Bank,

Accounts

Receivable

Debit side of Cash at Bank should be

decreased by $500, whereas, the

debit balance of accounts receivable

should be reduced by ($500 x 2) $1000

-1500

6. The Prepaid Expense balance of $7280

was listed in the Trial Balance as $7820

Yes Prepaid Expense The prepaid expense balance in Trial

Balance should be reduced by ($7820 -

$7280) $540 -540

7. A $5210 credit to Fees Revenue was

posted as a $521 credit. The debit entry to

Accounts Receivable was made correctly.

Yes Fees Revenue The credit side of Fees Revenue

should be increased by ($5210-$521)

$4689. 4689

8. A purchase of offi ce equipment for

$3300 on credit was not recorded.

No Offi ce

Equipment,

Accounts Payable

Offi ce Equipment should be debited

and Accounts Payable should be

credited by $3300

9. A purchase of Furniture for $7500 using

a loan was posted as a debit to the Loan

Payable account and a debit to the

Equipment account.

Yes Loan Payable Credit side should be increased by

($7500 x 2) $15000

15000

10. The drawings account balance was

listed as a credit for $1500

Yes Drawings Drawings account should be replaced

to debit side of trial balance for $1500

1500

Would the error cause

the Trial Balance not to

balance

Which accounts

would be

affected and

how?

How would the error be corrected

Effect on Trial

Balance totals

Question 2

Requirement A

As per the matching concept of account all the expenses should be reported in the same

period in which the income which is related to such an expense is realized. In other words, this is

an accounting principle which requires to recognize expenses and income in a related way

(Shipman, Swanquist and Whited 2016). As per the matching concept two methods which are

ACCOUNTING

Requirement B

Yes No Debit Credit

1. The Accrued Wages account with a

balance of $500 was omitted from the

Trial Balance

Yes Accrued Wages Accrued Wages of $500 should be

paosted in the credit side of trial

balance 500

2. A payment of $490 for Prepaid Rent was

only posted to the Cash at Bank account

and not to Prepaid Rent

Yes Prepaid Rent Debit side of Prepaid Rent should be

increased by $490

490

3. A debit of $458 to Cash at Bank was

posted as $485. The credit entry was

correct.

Yes Cash at Bank Debit Side of Cash at Bank should be

reduced by ($485 - $458) $27

-27

4. A credit of $600 to Accounts Payable

should have been made to Fees Revenue

No Accounts

Payable, Fees

Revenue

Accounts Payable should be debited

and Fees Revenue should be credited

by $600

5. A Dr. for a cash receipt of $500 from

customers in settlement their accounts

was posted twice as a Dr. to the Cash at

Bank and a Dr. to Accounts Receivable

accounts

Yes Cash at Bank,

Accounts

Receivable

Debit side of Cash at Bank should be

decreased by $500, whereas, the

debit balance of accounts receivable

should be reduced by ($500 x 2) $1000

-1500

6. The Prepaid Expense balance of $7280

was listed in the Trial Balance as $7820

Yes Prepaid Expense The prepaid expense balance in Trial

Balance should be reduced by ($7820 -

$7280) $540 -540

7. A $5210 credit to Fees Revenue was

posted as a $521 credit. The debit entry to

Accounts Receivable was made correctly.

Yes Fees Revenue The credit side of Fees Revenue

should be increased by ($5210-$521)

$4689. 4689

8. A purchase of offi ce equipment for

$3300 on credit was not recorded.

No Offi ce

Equipment,

Accounts Payable

Offi ce Equipment should be debited

and Accounts Payable should be

credited by $3300

9. A purchase of Furniture for $7500 using

a loan was posted as a debit to the Loan

Payable account and a debit to the

Equipment account.

Yes Loan Payable Credit side should be increased by

($7500 x 2) $15000

15000

10. The drawings account balance was

listed as a credit for $1500

Yes Drawings Drawings account should be replaced

to debit side of trial balance for $1500

1500

Would the error cause

the Trial Balance not to

balance

Which accounts

would be

affected and

how?

How would the error be corrected

Effect on Trial

Balance totals

Question 2

Requirement A

As per the matching concept of account all the expenses should be reported in the same

period in which the income which is related to such an expense is realized. In other words, this is

an accounting principle which requires to recognize expenses and income in a related way

(Shipman, Swanquist and Whited 2016). As per the matching concept two methods which are

5

ACCOUNTING

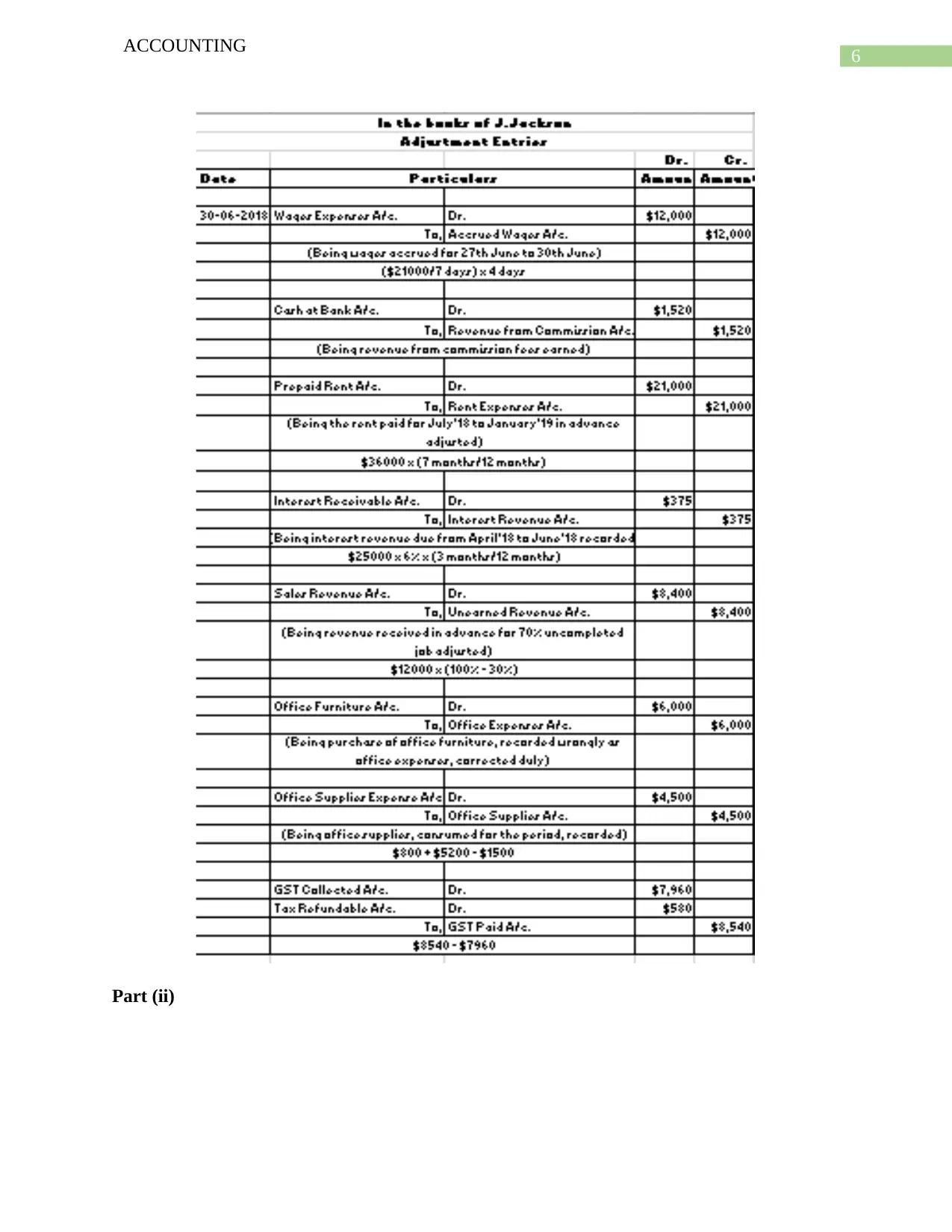

popularly used in accounting are Accrual system of recognizing and Cash system of

Recognizing.

Under the accrual system of accounting the expenses are recognizes in the year in which

such an expense has been incurred and it does not matter whether cash is paid for such

transaction. In other words, accrual basis of accounting is not dependent on the cash received or

cash paid for recognizing and recording of transactions. Whereas in the case of cash basis of

accounting expenses are recorded when cash is actually paid by the business irrespective of the

fact when the expenses was incurred. Therefore, the major difference between cash basis and

accrual basis is the timing of recognition of transactions.

Requirement B

Part (i)

ACCOUNTING

popularly used in accounting are Accrual system of recognizing and Cash system of

Recognizing.

Under the accrual system of accounting the expenses are recognizes in the year in which

such an expense has been incurred and it does not matter whether cash is paid for such

transaction. In other words, accrual basis of accounting is not dependent on the cash received or

cash paid for recognizing and recording of transactions. Whereas in the case of cash basis of

accounting expenses are recorded when cash is actually paid by the business irrespective of the

fact when the expenses was incurred. Therefore, the major difference between cash basis and

accrual basis is the timing of recognition of transactions.

Requirement B

Part (i)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING

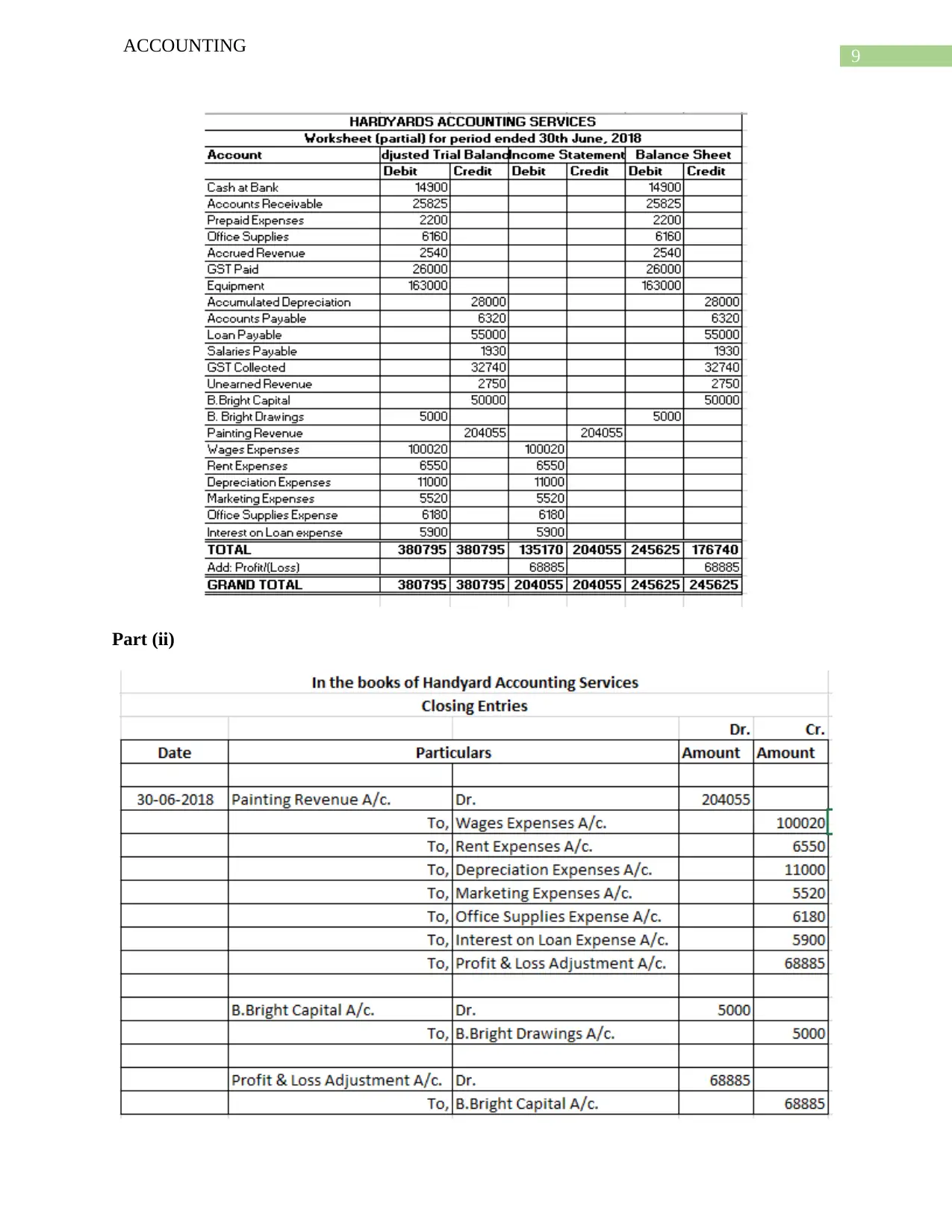

Part (ii)

ACCOUNTING

Part (ii)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING

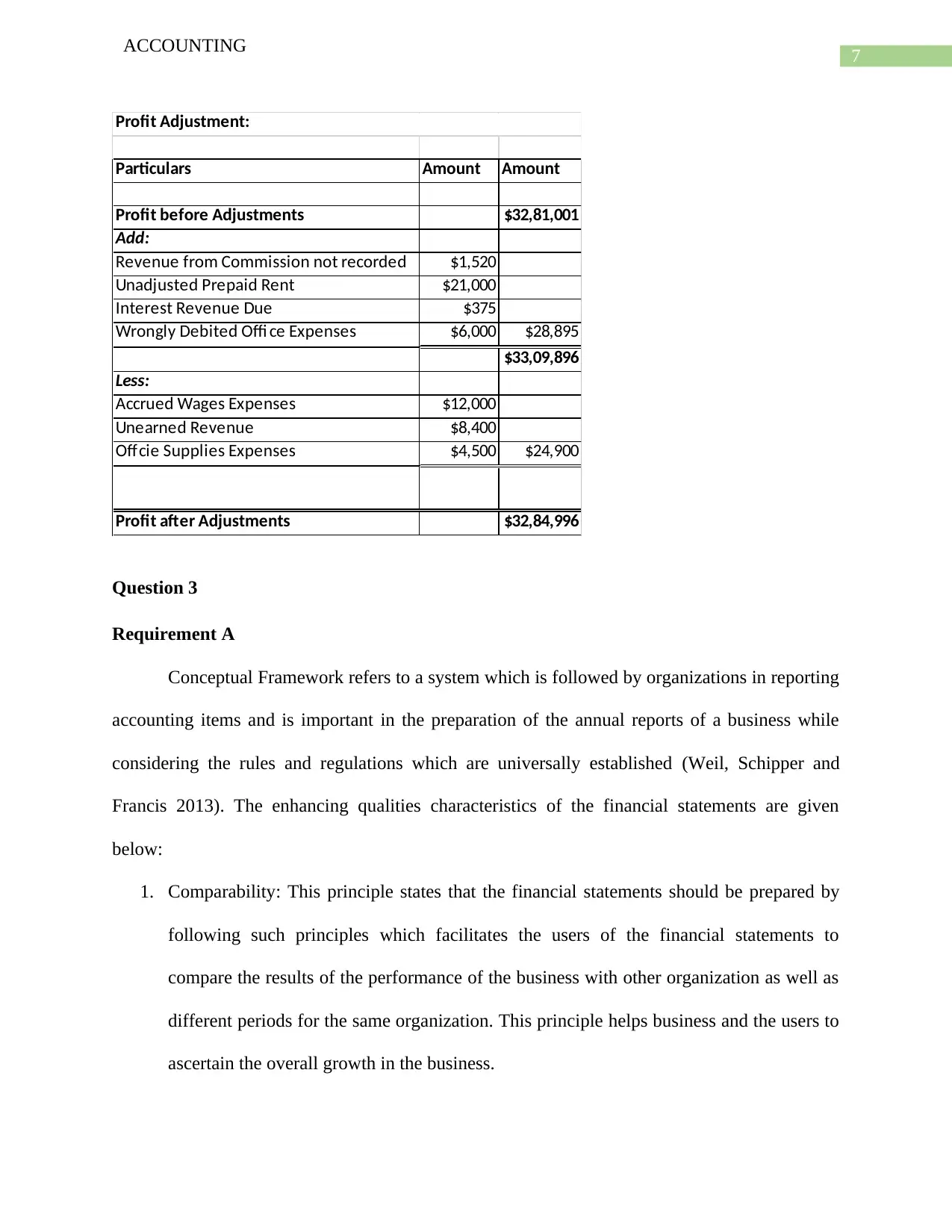

Particulars Amount Amount

Profit before Adjustments $32,81,001

Add:

Revenue from Commission not recorded $1,520

Unadjusted Prepaid Rent $21,000

Interest Revenue Due $375

Wrongly Debited Offi ce Expenses $6,000 $28,895

$33,09,896

Less:

Accrued Wages Expenses $12,000

Unearned Revenue $8,400

Offcie Supplies Expenses $4,500 $24,900

Profit after Adjustments $32,84,996

Profit Adjustment:

Question 3

Requirement A

Conceptual Framework refers to a system which is followed by organizations in reporting

accounting items and is important in the preparation of the annual reports of a business while

considering the rules and regulations which are universally established (Weil, Schipper and

Francis 2013). The enhancing qualities characteristics of the financial statements are given

below:

1. Comparability: This principle states that the financial statements should be prepared by

following such principles which facilitates the users of the financial statements to

compare the results of the performance of the business with other organization as well as

different periods for the same organization. This principle helps business and the users to

ascertain the overall growth in the business.

ACCOUNTING

Particulars Amount Amount

Profit before Adjustments $32,81,001

Add:

Revenue from Commission not recorded $1,520

Unadjusted Prepaid Rent $21,000

Interest Revenue Due $375

Wrongly Debited Offi ce Expenses $6,000 $28,895

$33,09,896

Less:

Accrued Wages Expenses $12,000

Unearned Revenue $8,400

Offcie Supplies Expenses $4,500 $24,900

Profit after Adjustments $32,84,996

Profit Adjustment:

Question 3

Requirement A

Conceptual Framework refers to a system which is followed by organizations in reporting

accounting items and is important in the preparation of the annual reports of a business while

considering the rules and regulations which are universally established (Weil, Schipper and

Francis 2013). The enhancing qualities characteristics of the financial statements are given

below:

1. Comparability: This principle states that the financial statements should be prepared by

following such principles which facilitates the users of the financial statements to

compare the results of the performance of the business with other organization as well as

different periods for the same organization. This principle helps business and the users to

ascertain the overall growth in the business.

8

ACCOUNTING

2. Verifiability: The principle suggest that the information which are presented in the

financial statements of the company should be such that it can be easily be verified by the

business. Any financial information is verifiable if the shareholders of the company can

confirm that the financial information are fairly represented.

3. Timeliness: The principle states that financial information if not presented to the

shareholders in time of their decision-making process, then it is not at all useful. The

principle makes it clear that the information should be provided to the investors before

they are able to take decisions.

4. Understandability: As per this principle, the financial information which are depicted in

the annual reports should be simple and easy to understand and no such information

should be included without appropriate notes and explanations which are complex in

nature and difficult to understand.

Requirement B

Part (i)

ACCOUNTING

2. Verifiability: The principle suggest that the information which are presented in the

financial statements of the company should be such that it can be easily be verified by the

business. Any financial information is verifiable if the shareholders of the company can

confirm that the financial information are fairly represented.

3. Timeliness: The principle states that financial information if not presented to the

shareholders in time of their decision-making process, then it is not at all useful. The

principle makes it clear that the information should be provided to the investors before

they are able to take decisions.

4. Understandability: As per this principle, the financial information which are depicted in

the annual reports should be simple and easy to understand and no such information

should be included without appropriate notes and explanations which are complex in

nature and difficult to understand.

Requirement B

Part (i)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING

Part (ii)

ACCOUNTING

Part (ii)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING

Question 4

Requirement A

a. The use of credit cards will definitely reduce the risks which are associated with normal

credit facilities. The loan amount can directly be dealt with the credit card company. the

process of credit which was previously available will change due to the new credit card

facilities. The credit card facilities will be making the e-commerce facility much easier.

The cost which are to be incurred in case of credit card is related to interest which is

charged at the end of the month. The credit cards are normally protected with a pin code

which is different for different individuals.

b. Account Receivables forms a major part of the financial statements of the company as it

is related to credit sales of the business. The recording and monitoring of account

receivable will not be affected by the introduction of credit cards in the business (Hope,

Thomas and Vyas 2013). This because credit card can be used up to a certain limit which

is not that much in most of the cases, however account receivables transaction may be of

lumpsum amount due to a big order. Therefore, it is necessary for the business to keep

track of the account receivables as effective management of such items results in

increased generation of sales.

Factoring may be defined as a source of financing wherein the account receivables of the

business are sold to financial intermediary who are known as factors at a discount. In simple

words, it is a source of procuring funds by selling off the receivables of the business. It is to be

clearly understood that factoring is not same as a loan and the funds which are received are not to

be considered as debt capital of the business (Michalski 2014).

ACCOUNTING

Question 4

Requirement A

a. The use of credit cards will definitely reduce the risks which are associated with normal

credit facilities. The loan amount can directly be dealt with the credit card company. the

process of credit which was previously available will change due to the new credit card

facilities. The credit card facilities will be making the e-commerce facility much easier.

The cost which are to be incurred in case of credit card is related to interest which is

charged at the end of the month. The credit cards are normally protected with a pin code

which is different for different individuals.

b. Account Receivables forms a major part of the financial statements of the company as it

is related to credit sales of the business. The recording and monitoring of account

receivable will not be affected by the introduction of credit cards in the business (Hope,

Thomas and Vyas 2013). This because credit card can be used up to a certain limit which

is not that much in most of the cases, however account receivables transaction may be of

lumpsum amount due to a big order. Therefore, it is necessary for the business to keep

track of the account receivables as effective management of such items results in

increased generation of sales.

Factoring may be defined as a source of financing wherein the account receivables of the

business are sold to financial intermediary who are known as factors at a discount. In simple

words, it is a source of procuring funds by selling off the receivables of the business. It is to be

clearly understood that factoring is not same as a loan and the funds which are received are not to

be considered as debt capital of the business (Michalski 2014).

11

ACCOUNTING

c. Provision for bad debt are allowed in financial statements in order to estimate the losses

which the business might incur. As per the principle of Conservatism, a business must

always recognize probable losses or liabilities and record the same ahead of income or

assets. Therefore, the business has to recognize such a doubtful debt as a provision. If the

provision is not allowed than it will affect the profit which is generated by the business

which will be showing profits in excess and also impact the value of debtors in the

balance sheet of the company.

Requirement B

Part (i)

ACCOUNTING

c. Provision for bad debt are allowed in financial statements in order to estimate the losses

which the business might incur. As per the principle of Conservatism, a business must

always recognize probable losses or liabilities and record the same ahead of income or

assets. Therefore, the business has to recognize such a doubtful debt as a provision. If the

provision is not allowed than it will affect the profit which is generated by the business

which will be showing profits in excess and also impact the value of debtors in the

balance sheet of the company.

Requirement B

Part (i)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.