Taxation Analysis: Green Manufacturing Company Income Statement Review

VerifiedAdded on 2022/09/07

|22

|2454

|26

Homework Assignment

AI Summary

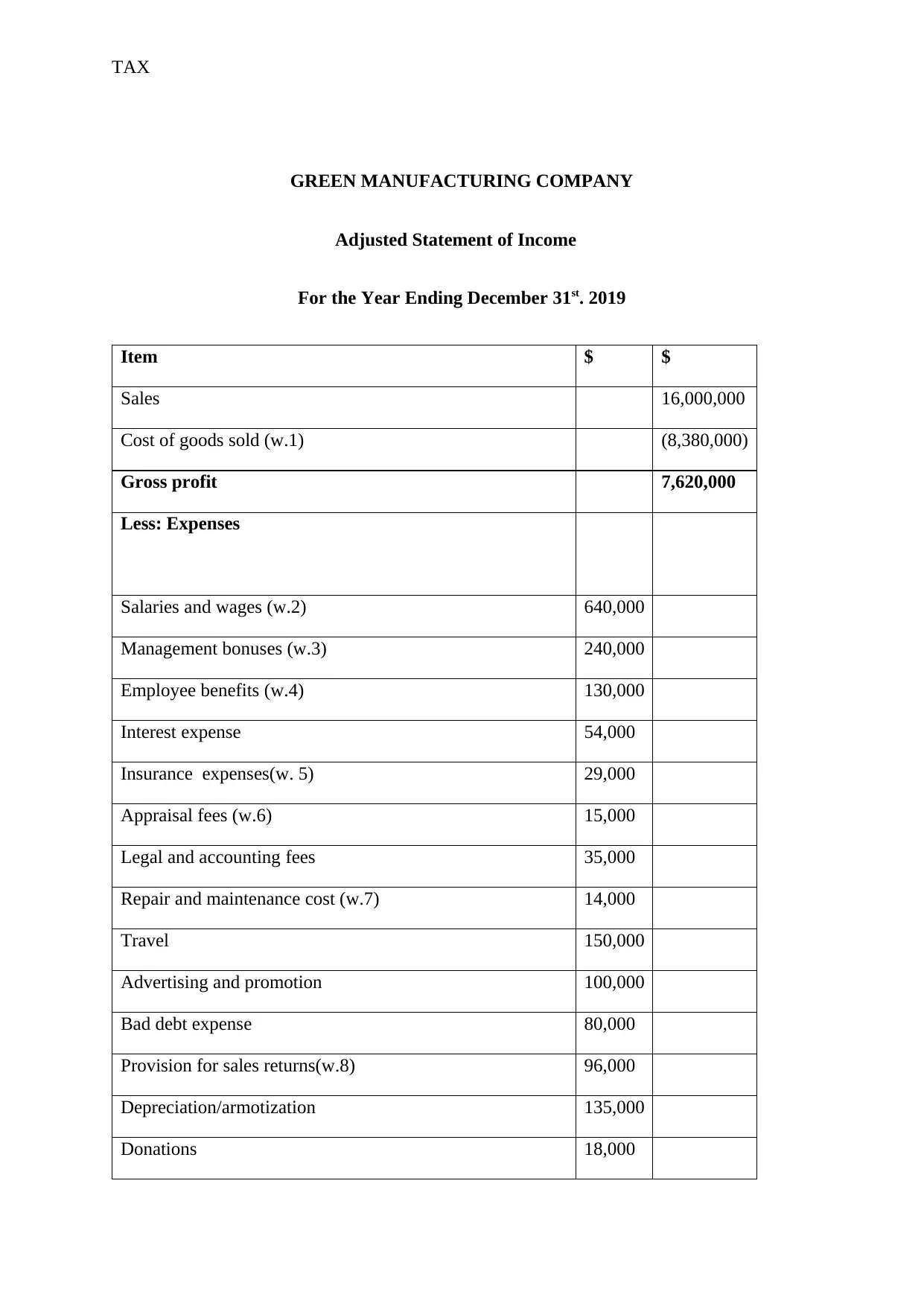

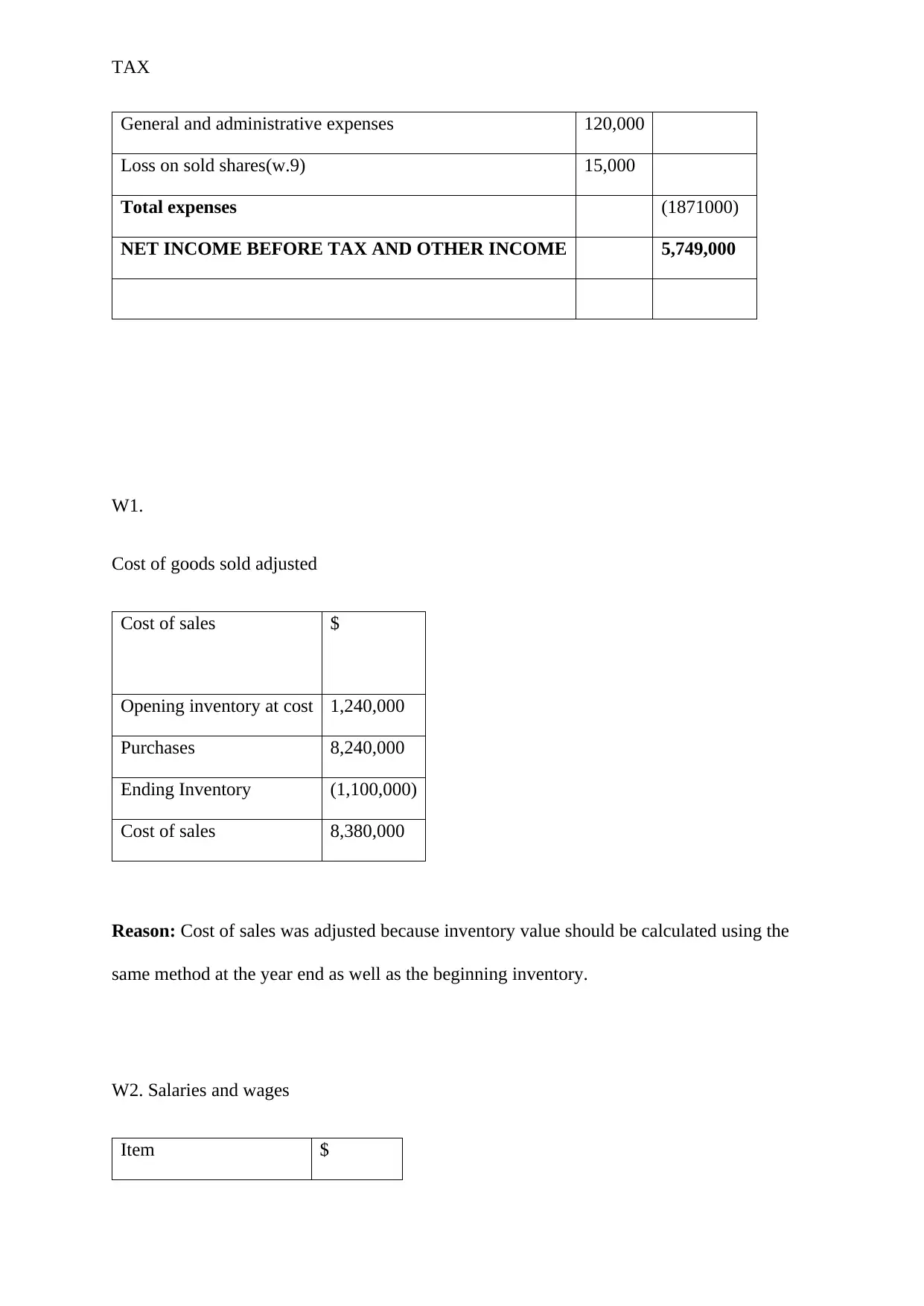

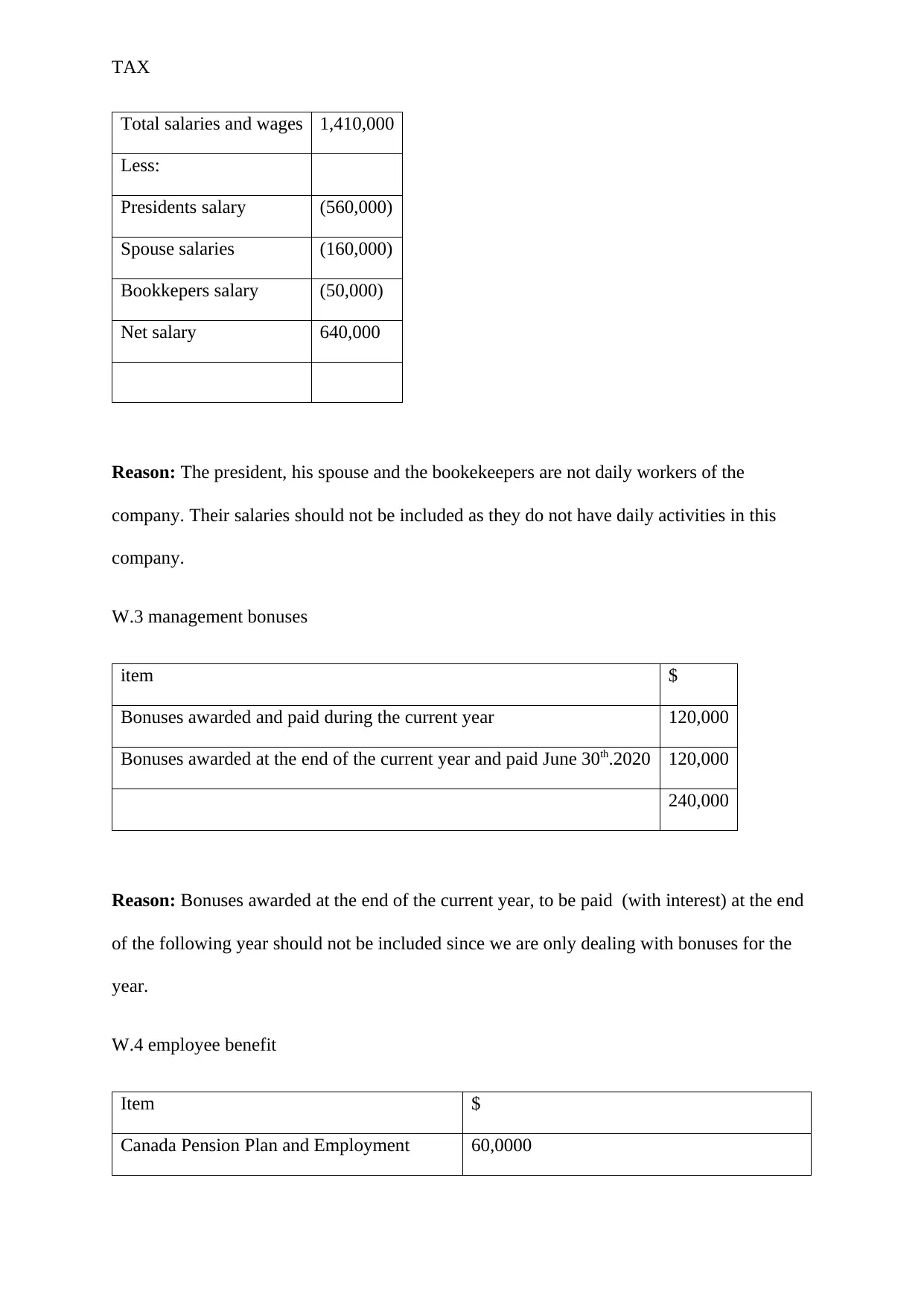

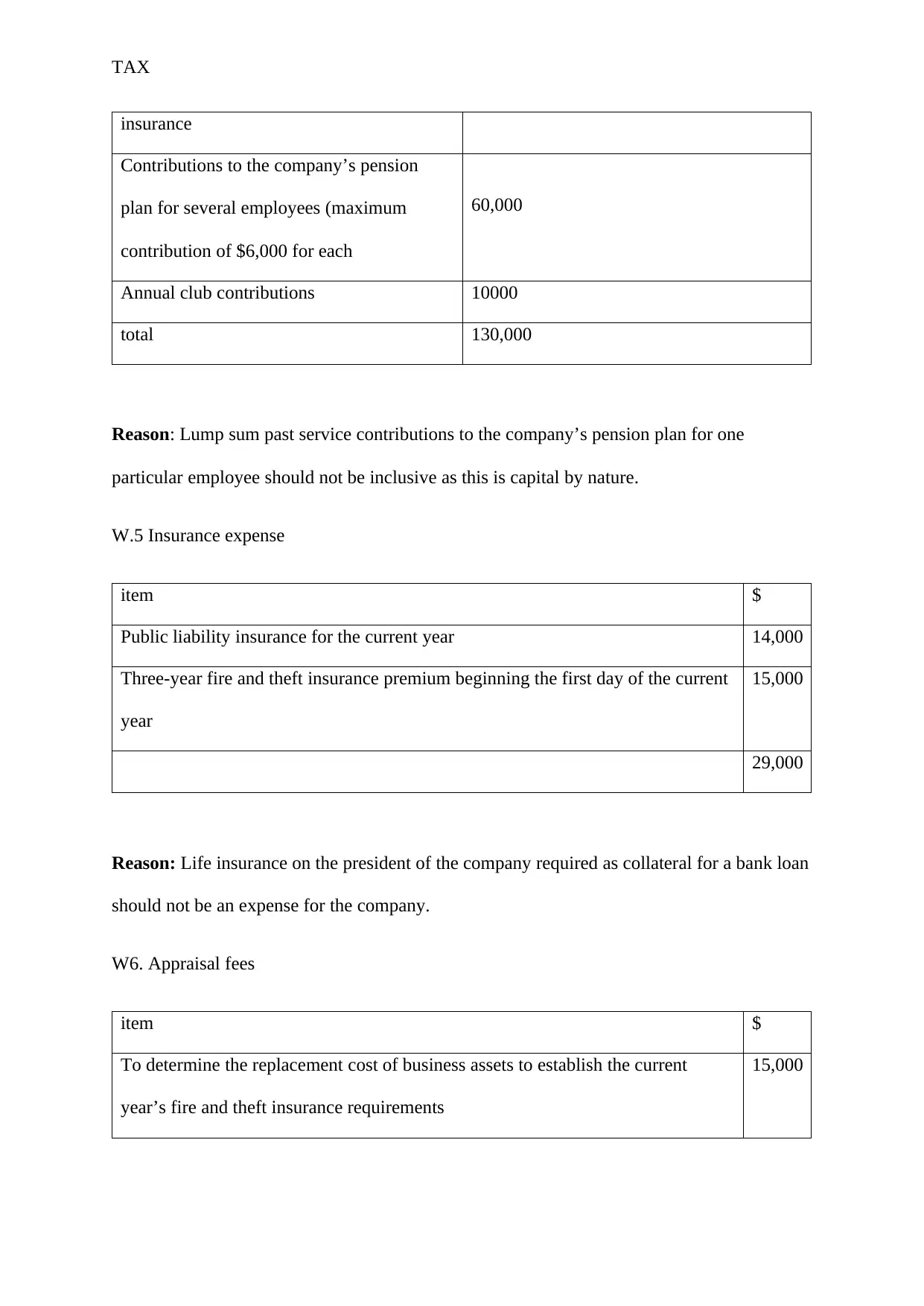

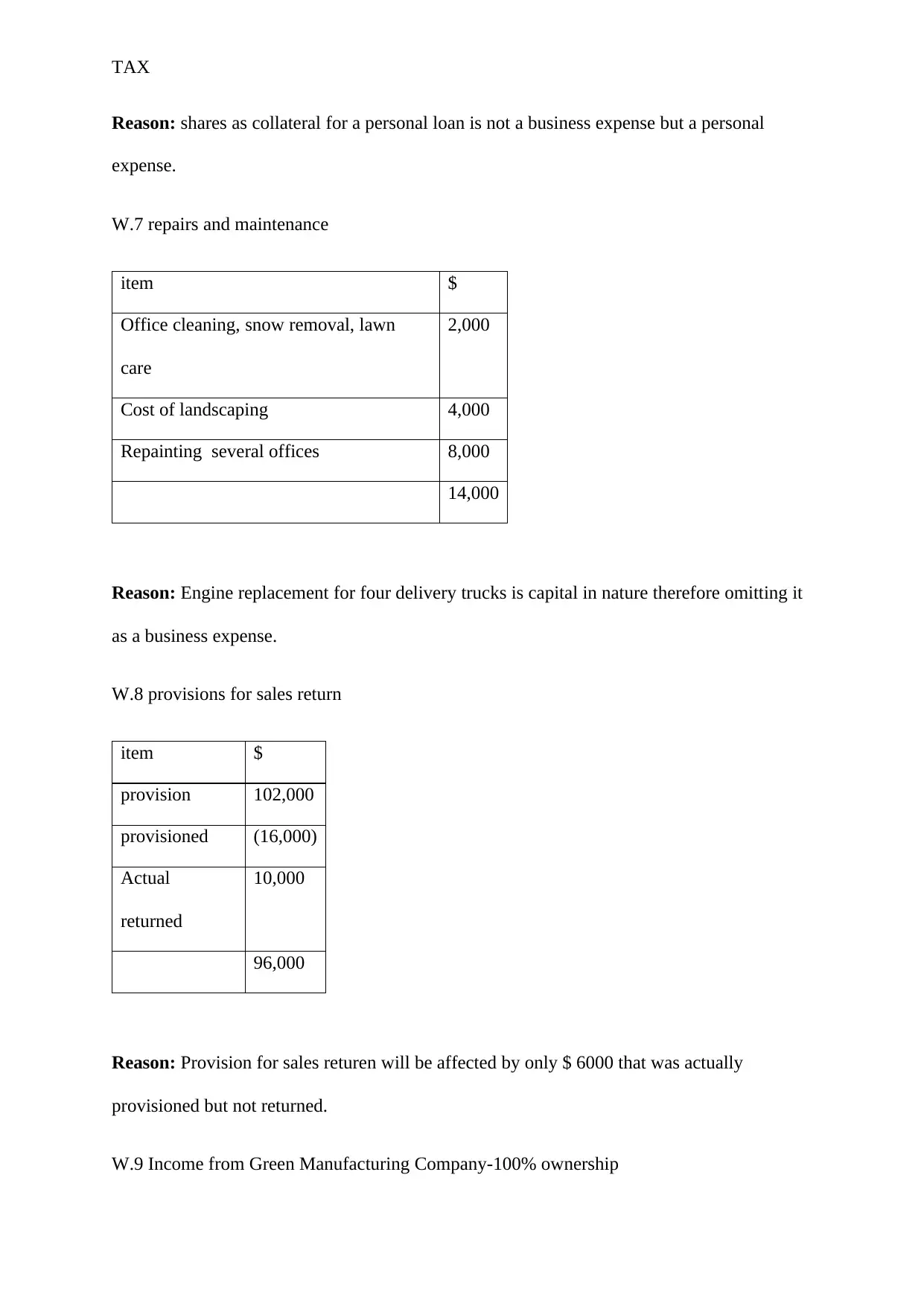

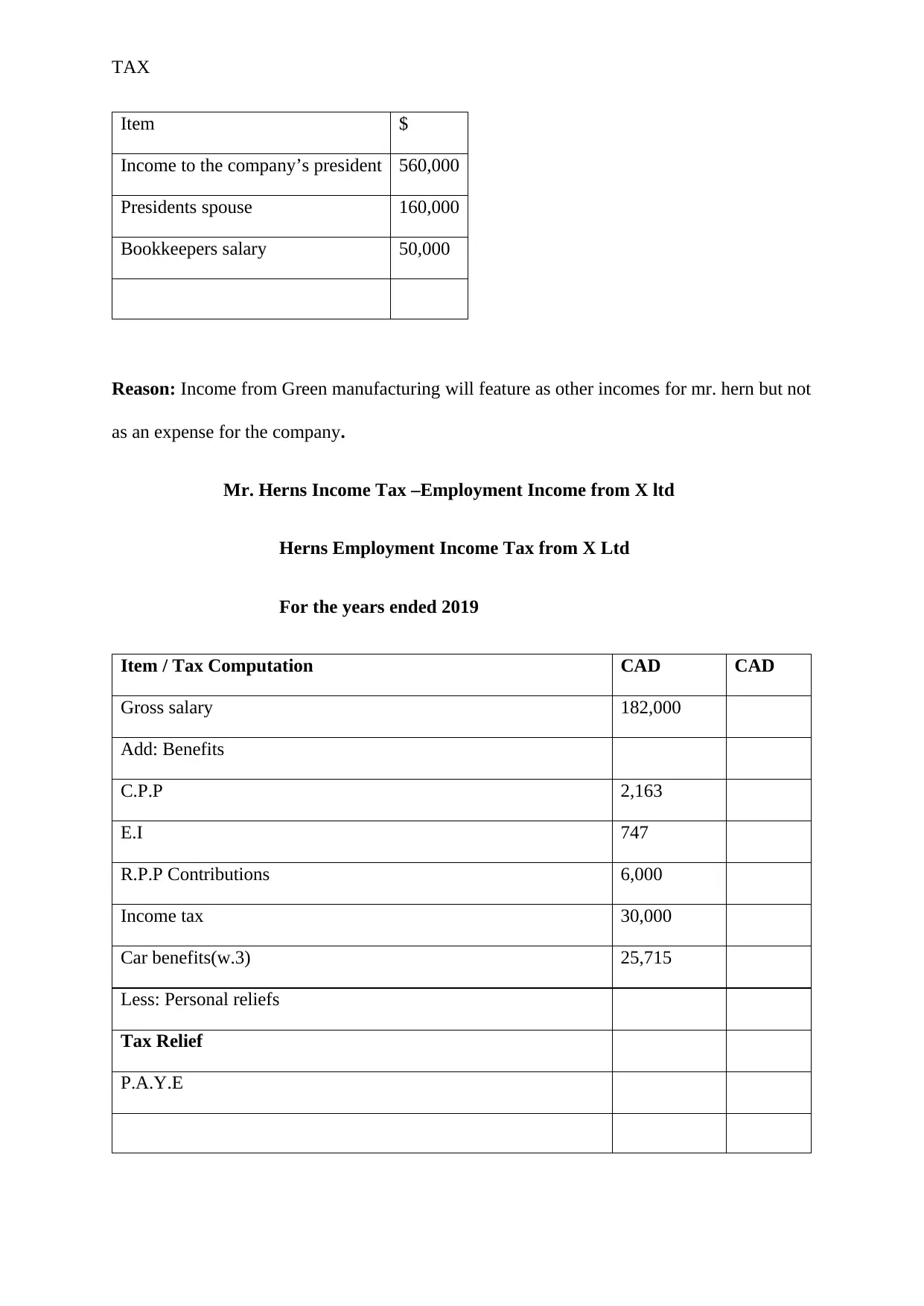

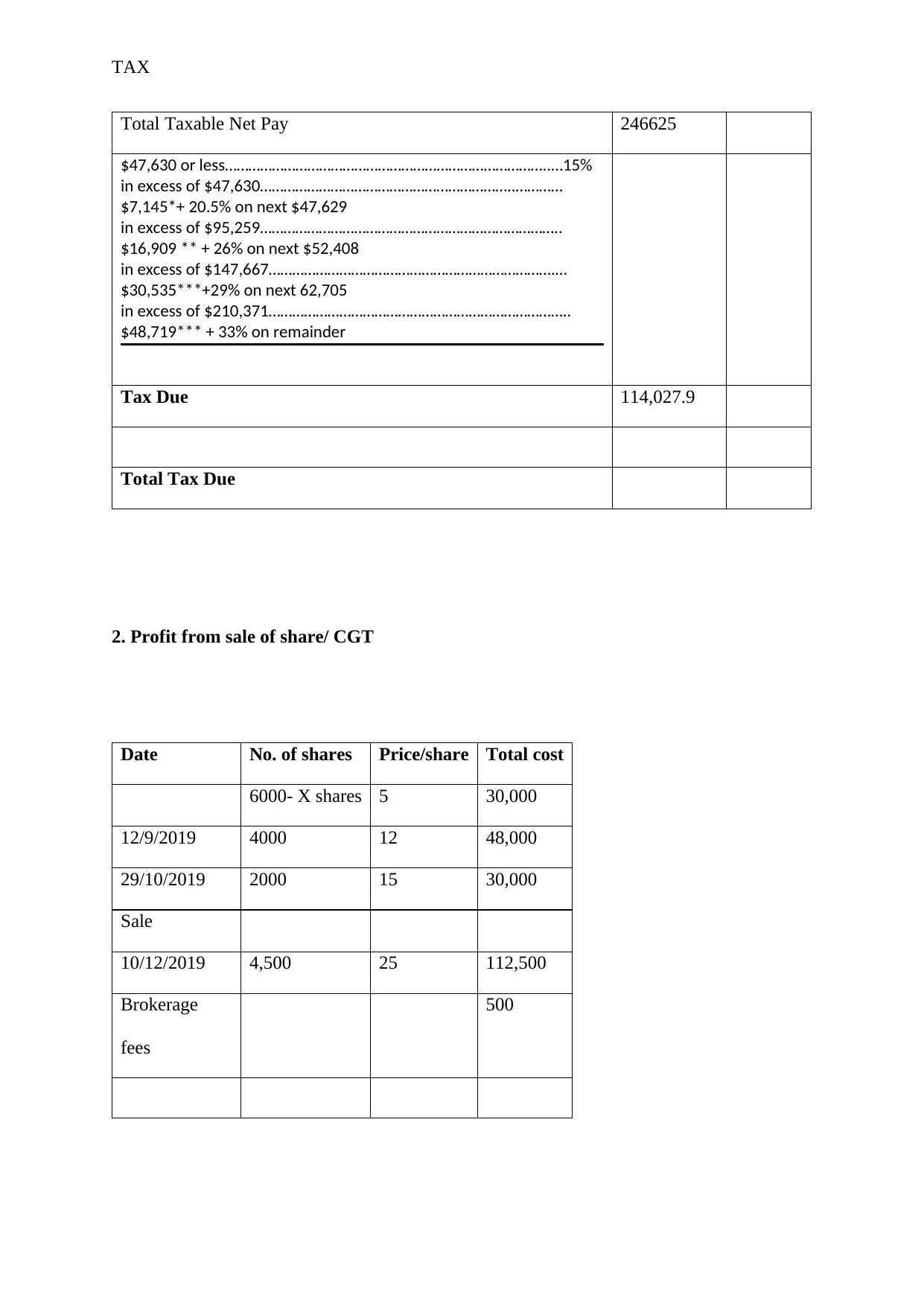

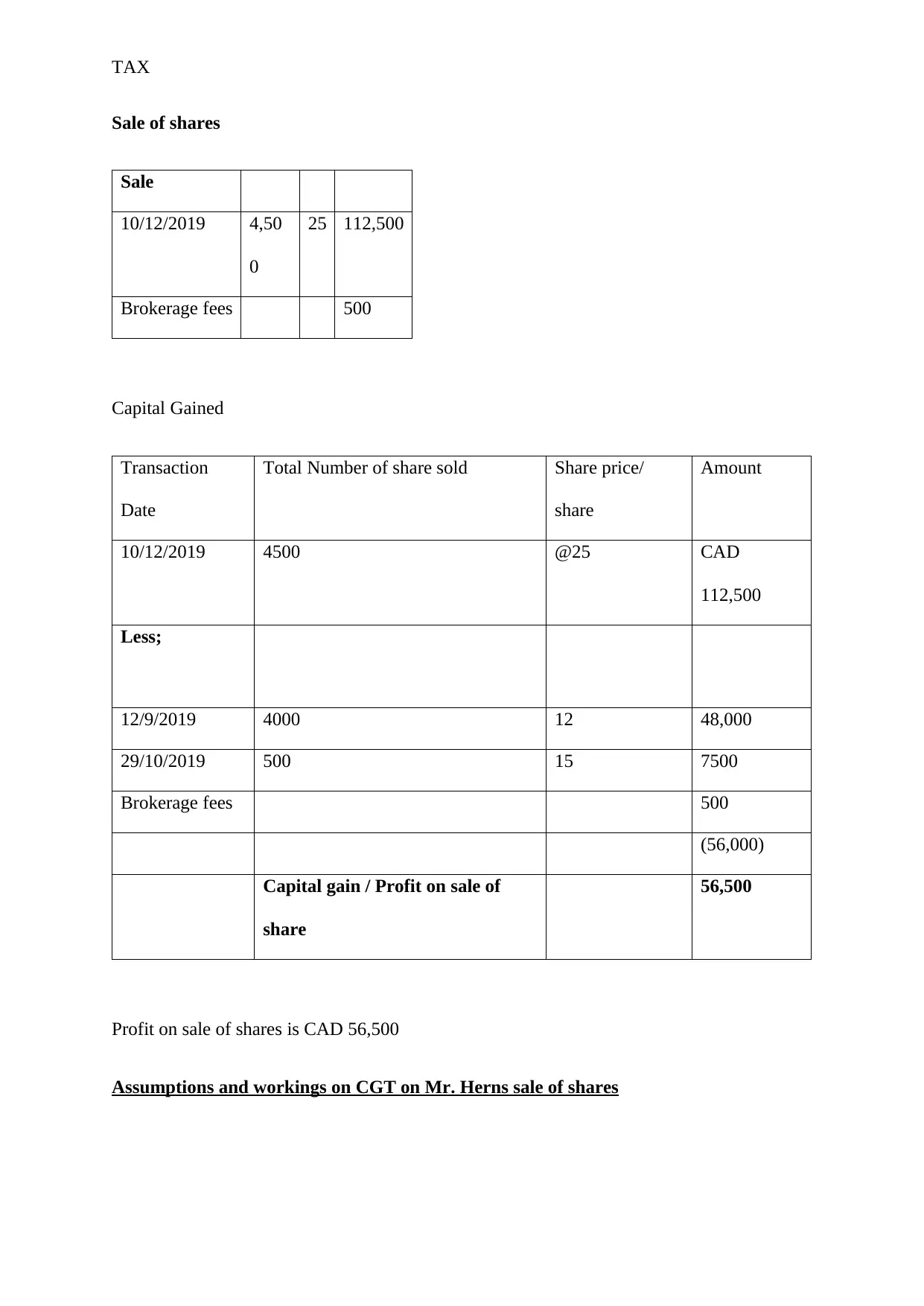

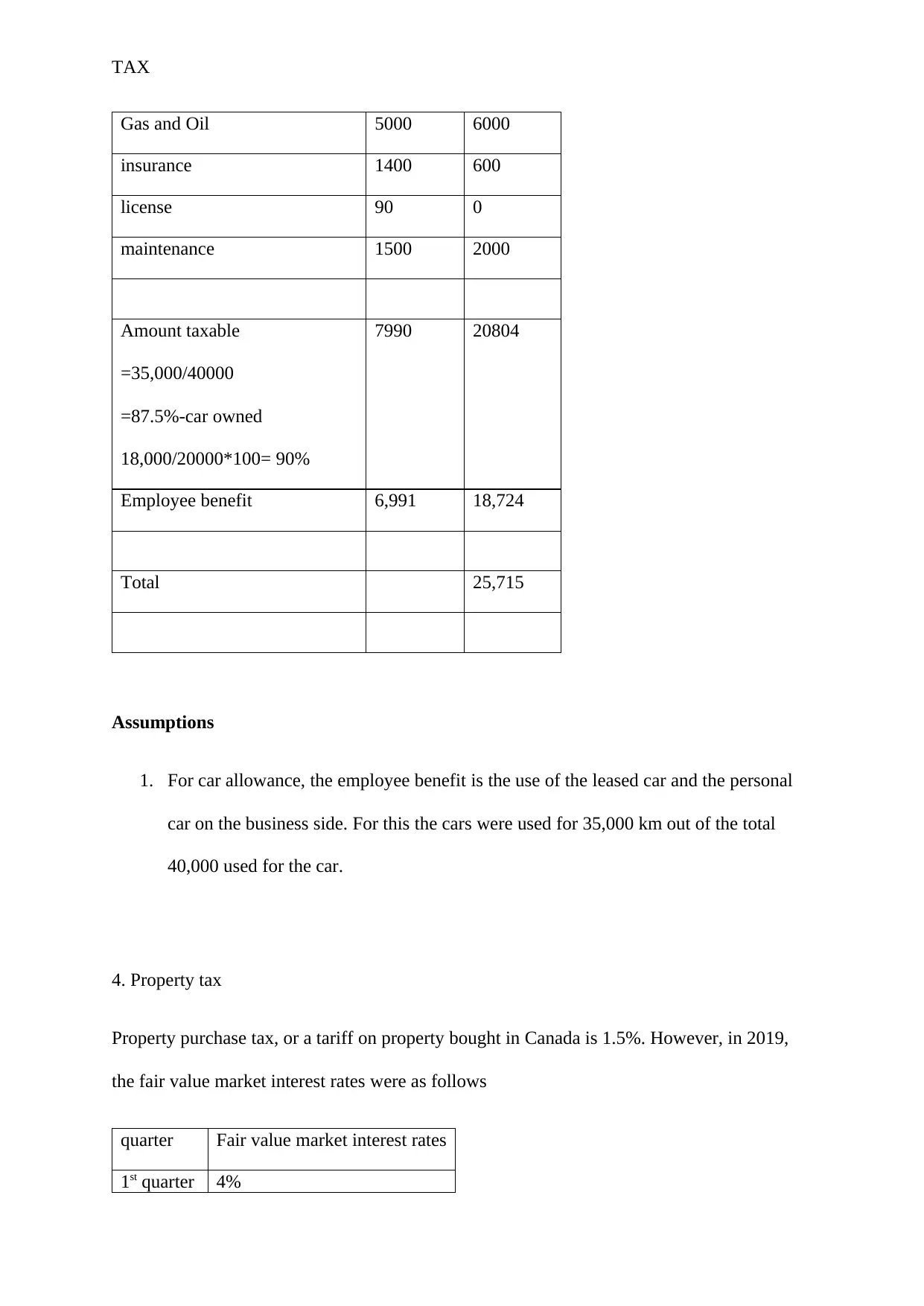

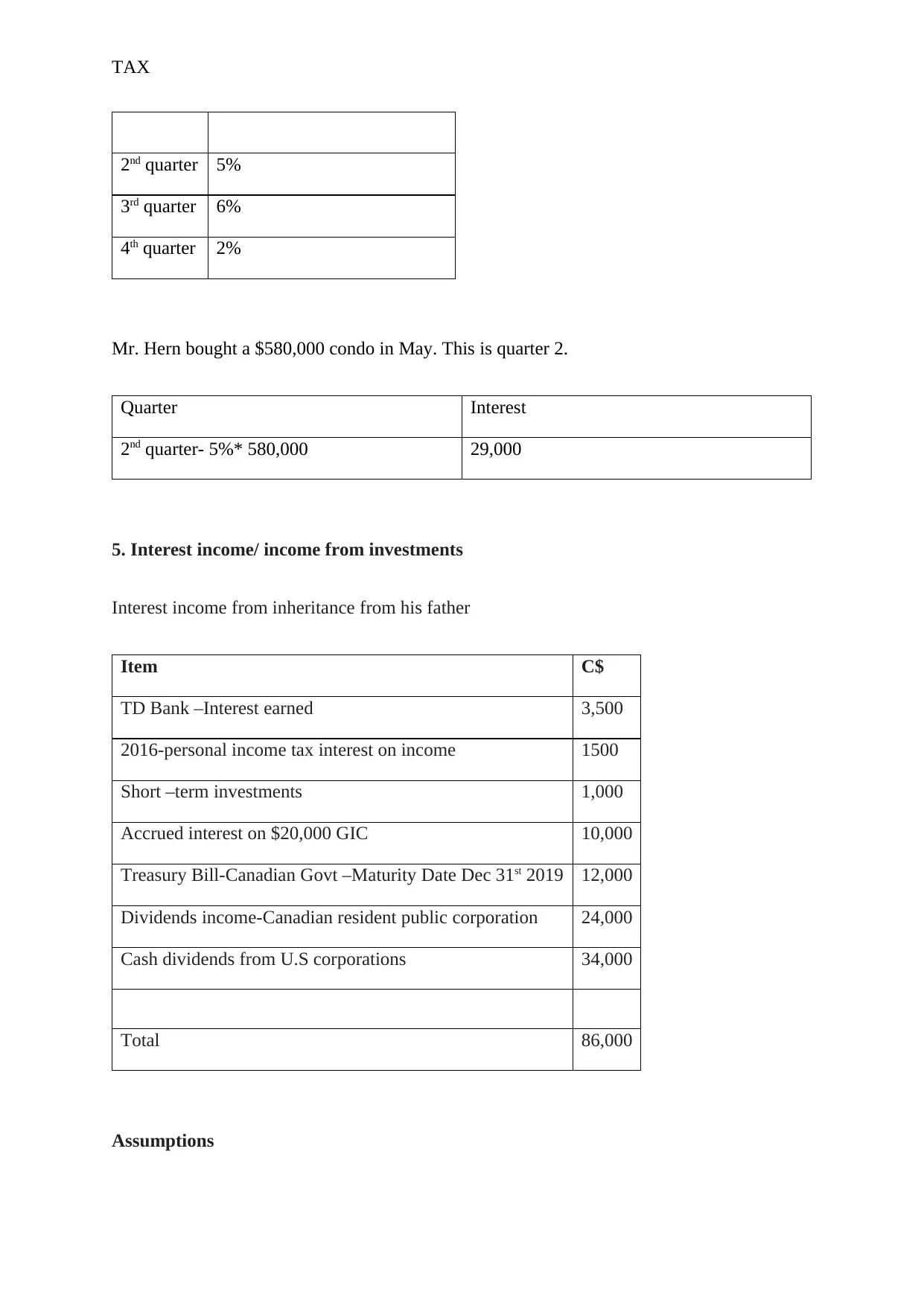

This assignment analyzes the personal taxation of Mr. Douglas Hern, the 100% owner of Green Manufacturing Company, for the year 2019. It begins with an adjusted income statement for the company, detailing sales, cost of goods sold, and various expenses, with explanations for adjustments made to several line items. The assignment then calculates Mr. Hern's employment income tax from another company, including gross salary, benefits, deductions, and tax due. Further calculations involve capital gains tax from the sale of shares, car allowance, property tax, interest income, rental income, and interest expenses. Detailed assumptions and workings are provided for each section. The document also explores gifts and donations, medical expenses, and CCA (Capital Cost Allowance) calculations for various asset classes. It concludes with calculations for contributions to RRP (Registered Retirement Plan) and non-refundable tax credits, including basic personal, spousal, and medical expenses, to arrive at Mr. Hern's total tax liability. The analysis covers various aspects of personal and corporate taxation, providing a comprehensive overview of Mr. Hern's financial situation for the specified tax year.

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.