ACC568 Auditing and Assurance Report: API Audit Risks and Procedures

VerifiedAdded on 2023/03/20

|19

|3694

|56

Report

AI Summary

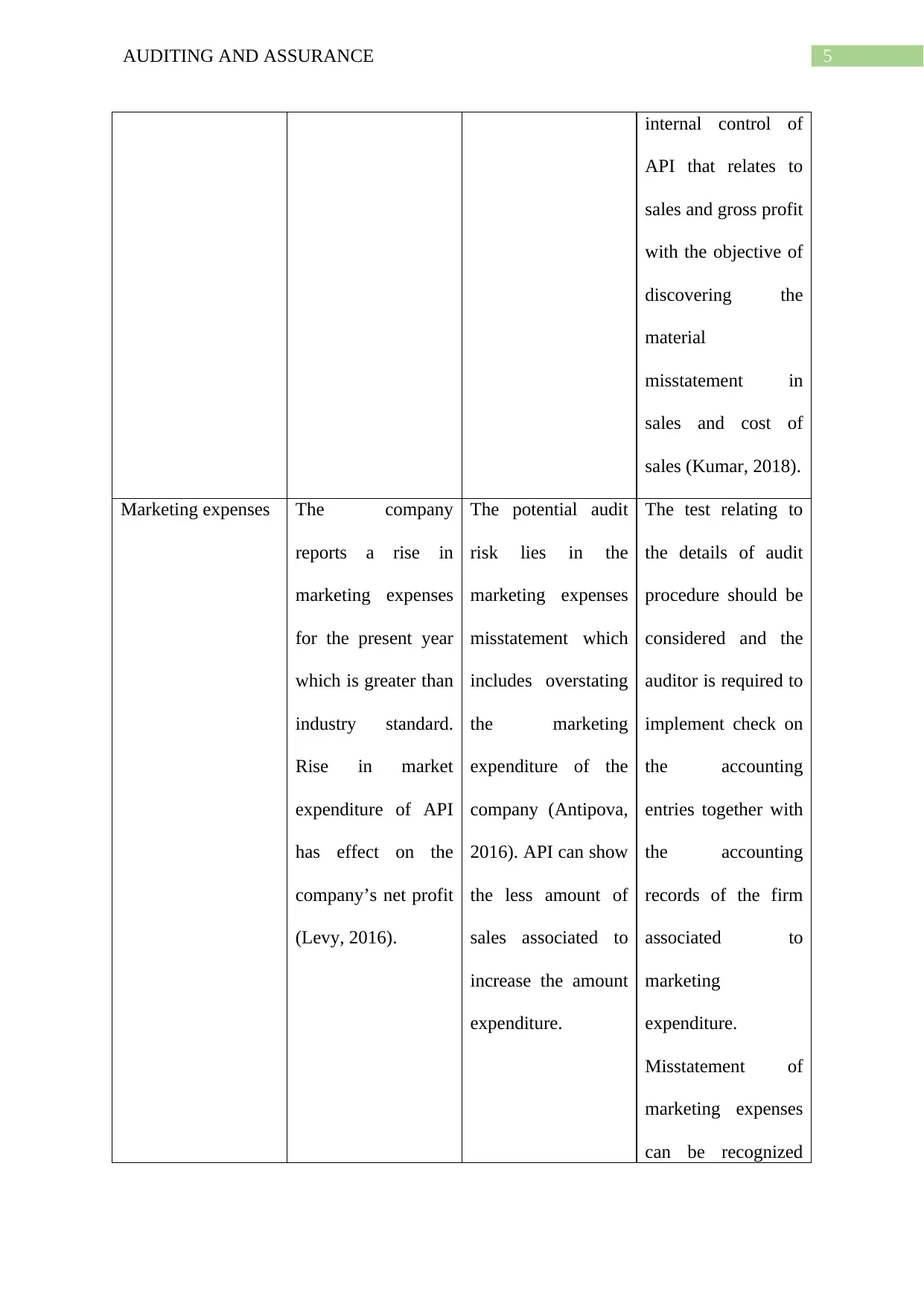

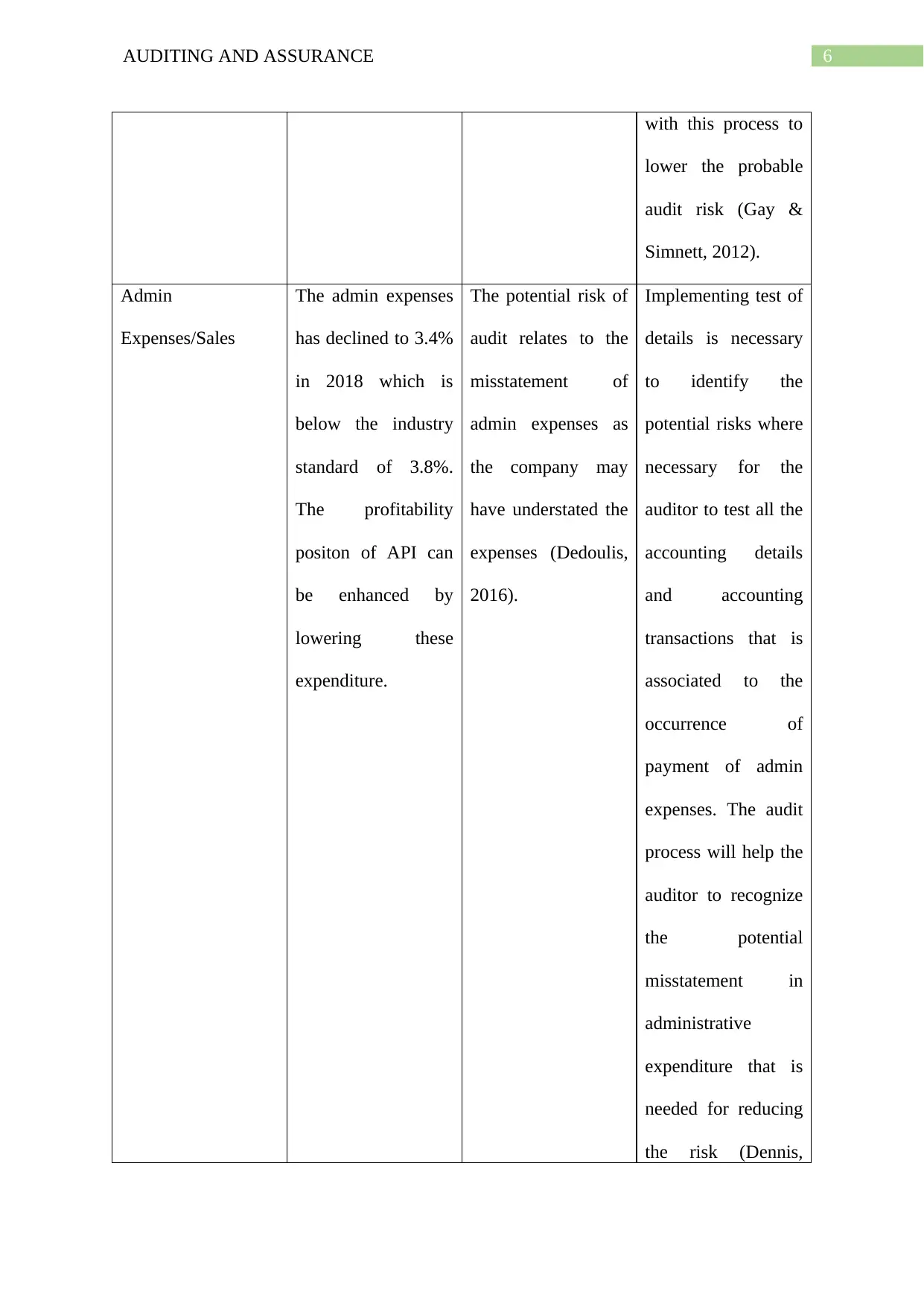

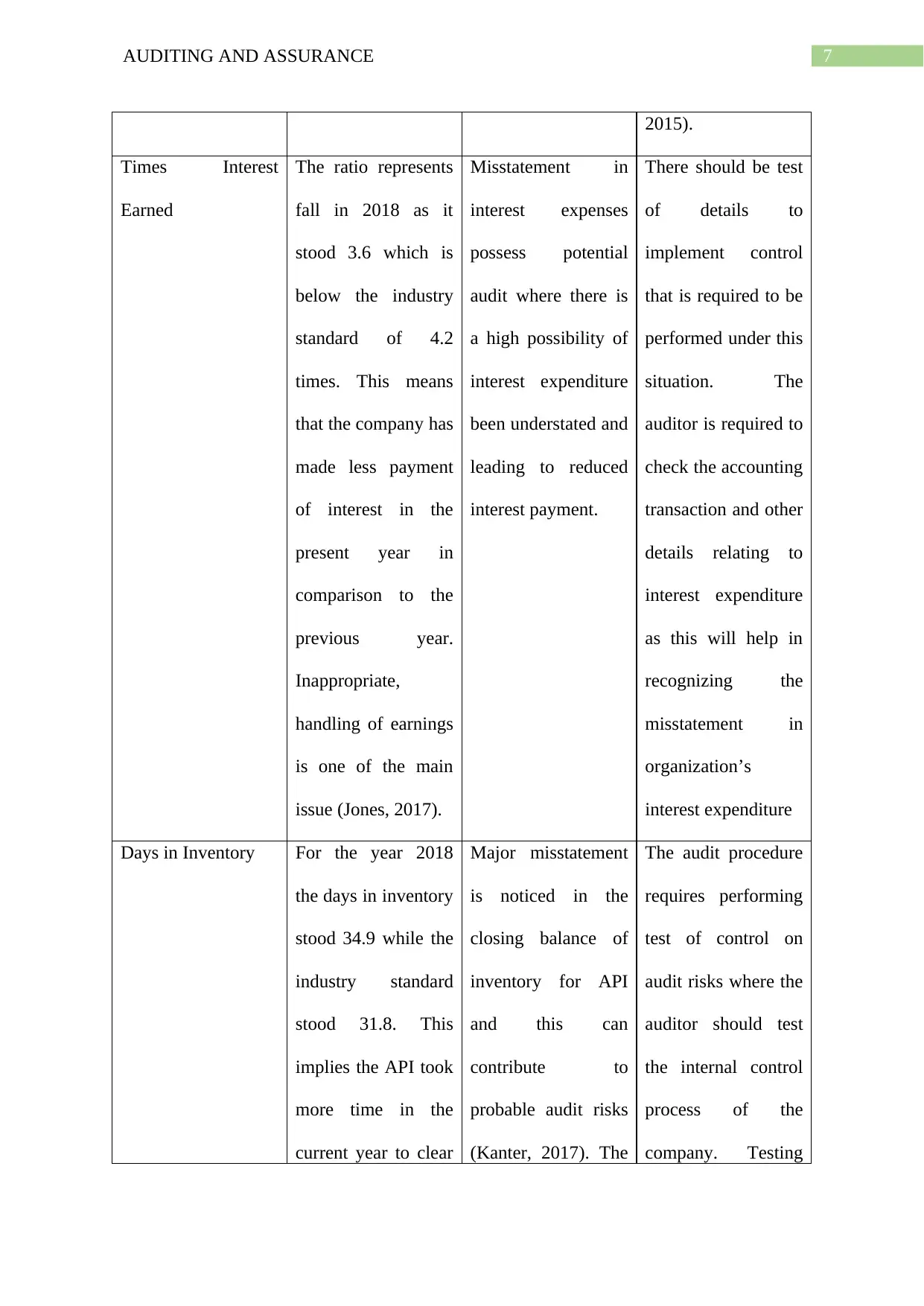

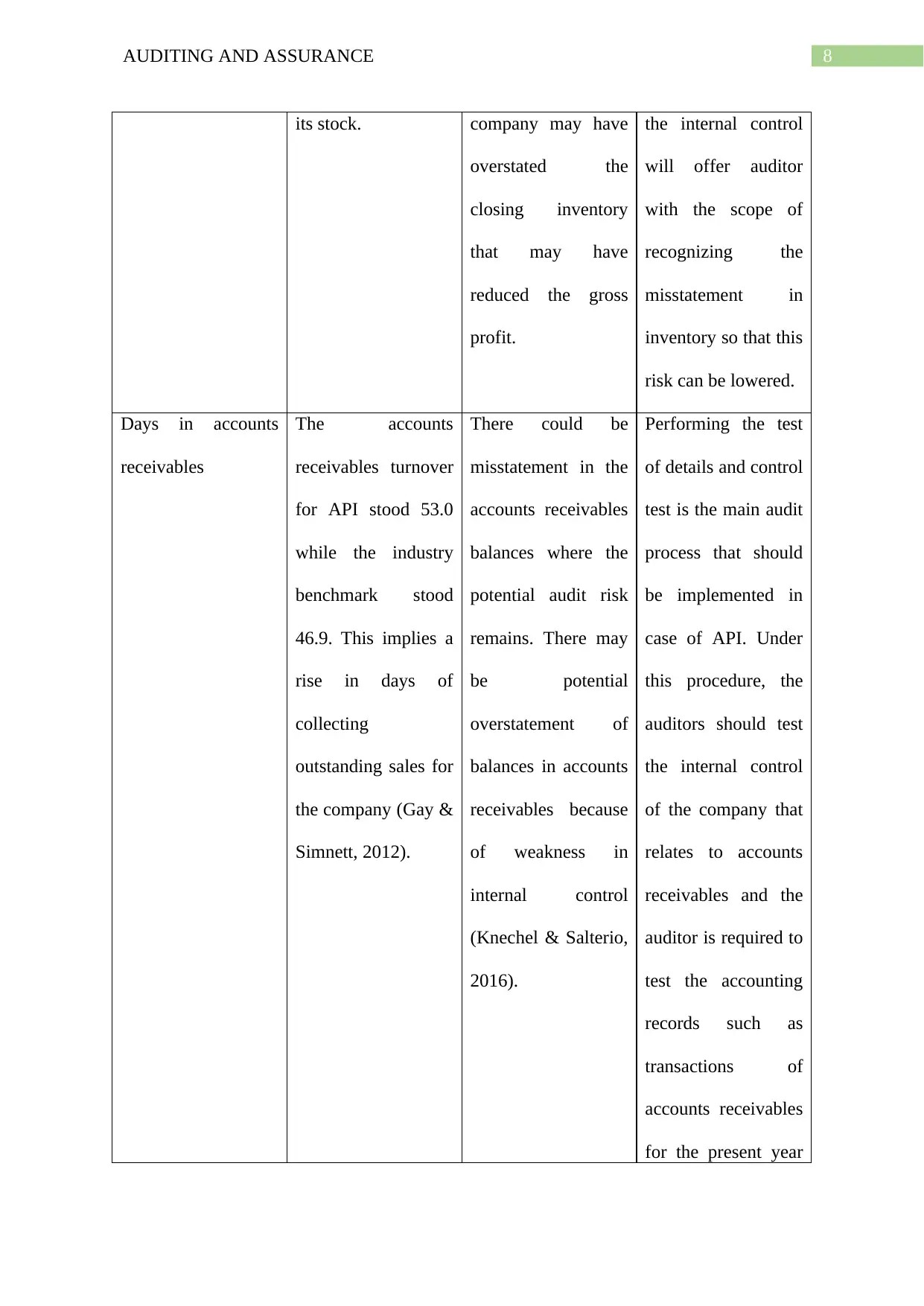

This report, prepared for the Audit Manager, Wayne Wiadrowski, assesses the audit risks associated with Always Precise Instruments Pty Limited (API). The analysis focuses on material misstatements and errors, examining audit risks arising from ratio analysis, internal control weaknesses related to inventory, and discusses appropriate sampling methods. The report provides a detailed breakdown of audit risks identified through various financial ratios, including current ratio, quick asset ratio, return on equity, return on assets, gross margin, marketing expenses, admin expenses, times interest earned, days in inventory, days in receivables and debt-to-equity ratio, and outlines corresponding audit procedures to mitigate these risks. Furthermore, it highlights weaknesses in API's inventory internal controls, particularly those related to the computerised system and supplier selection, detailing associated audit risks and recommending specific audit procedures. The report emphasizes the importance of thorough testing of internal controls and accounting records to identify and address potential misstatements, ultimately aiming to provide a comprehensive understanding of the audit process and potential risks in API's financial reporting. The report also covers the importance of test of details and control to address the potential misstatements.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.